- Investment criteria (lecture 5)

Содержание

- 2. Lecture 5. Investment criteria

- 3. How should a firm make an investment decision What assets do we buy? What is the

- 4. Capital Budgeting: The process of planning for purchases of long-term assets. Example: Suppose our firm must

- 5. Decision-making Criteria in Capital Budgeting How do we decide if a capital investment project should be

- 6. Decision-making Criteria in Capital Budgeting The ideal evaluation method should: include all cash flows that occur

- 7. Decision-making Criteria in Capital Budgeting Firms invest in 2 categories of projects: Independent projects – do

- 8. Techniques in Capital Budgeting Payback period Discounted Payback Period Net Present Value (NPV) Profitability Index (PI)

- 9. 1) Payback Period The payback method simply measures how long (in years and/or months) it takes

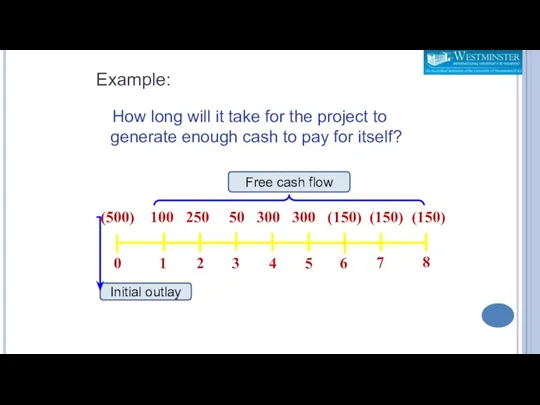

- 10. How long will it take for the project to generate enough cash to pay for itself?

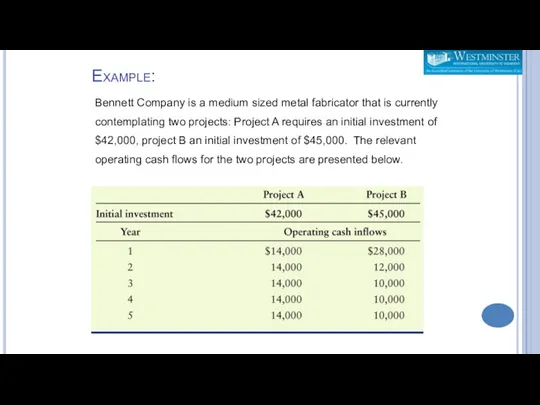

- 11. Bennett Company is a medium sized metal fabricator that is currently contemplating two projects: Project A

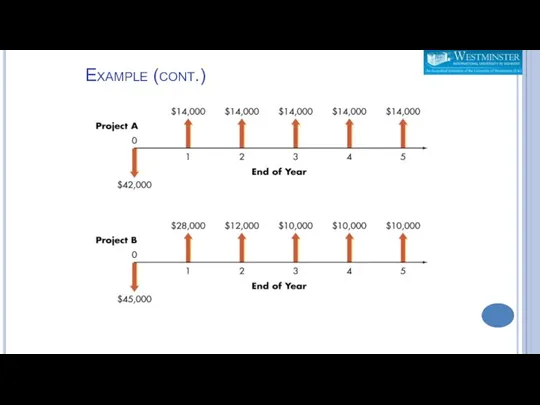

- 12. Example (cont.)

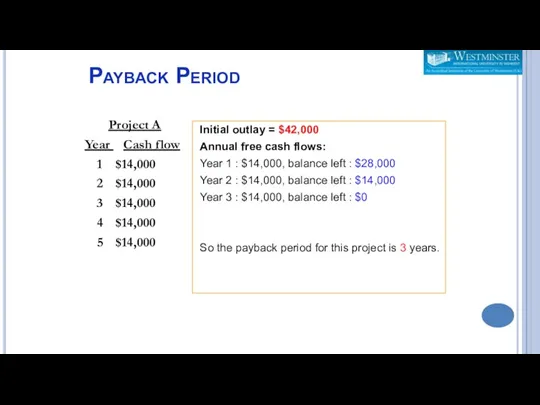

- 13. Payback Period Project A Year Cash flow 1 $14,000 2 $14,000 3 $14,000 4 $14,000 5

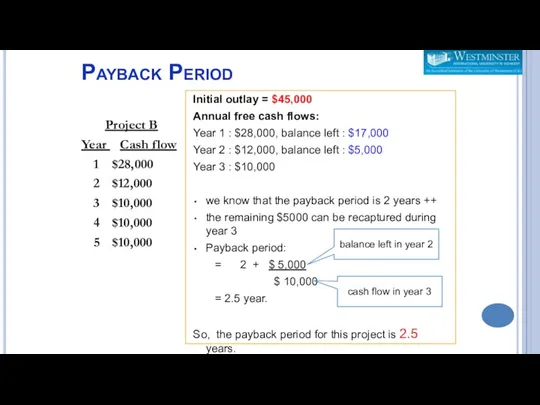

- 14. Payback Period Project B Year Cash flow 1 $28,000 2 $12,000 3 $10,000 4 $10,000 5

- 15. Payback Period Is the payback period good? Is it acceptable? Firms that use this method will

- 16. Pros and Cons of Payback Periods The payback method is widely used by large firms to

- 17. Pros and Cons of Payback Periods (cont.) One major weakness of the payback method is that

- 18. 2) Discounted Payback Period The number of years needed to recover initial cash outlay from the

- 19. Discounted Payback Period Year Free Cash Discounted Flow CF (14%) 0 -500 1 250 219.30 2

- 20. Discounted Payback Period Discounted payback period is 2.52 years. Is it acceptable? ACCEPT if discounted payback

- 21. Discounted Payback Period Advantages: Uses free cash flows Easy to calculate and to understand Considers time

- 22. Other Methods 3) Net Present Value (NPV) 4) Profitability Index (PI) 5) Internal Rate of Return

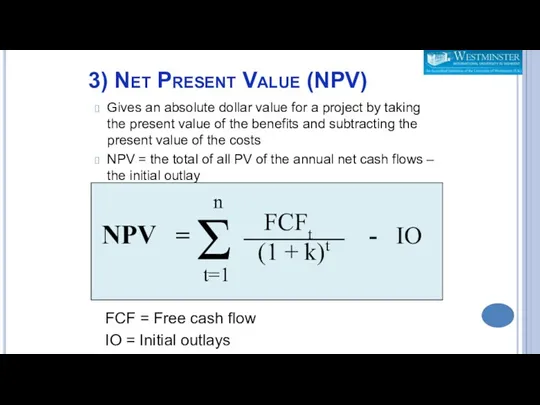

- 23. 3) Net Present Value (NPV) Gives an absolute dollar value for a project by taking the

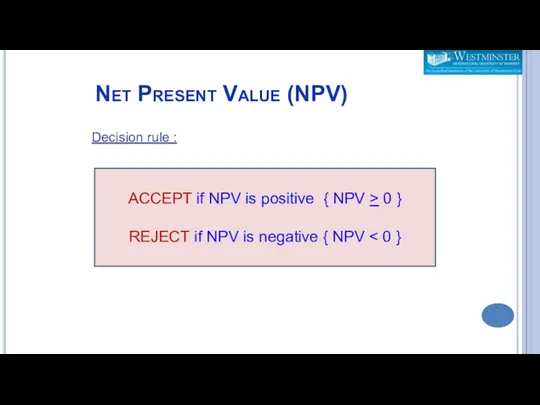

- 24. Net Present Value (NPV) Decision rule : ACCEPT if NPV is positive { NPV > 0

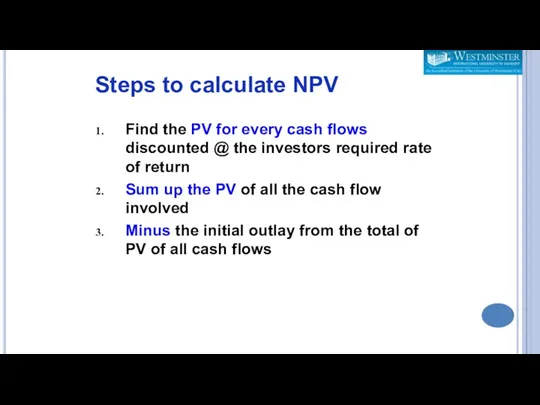

- 25. Find the PV for every cash flows discounted @ the investors required rate of return Sum

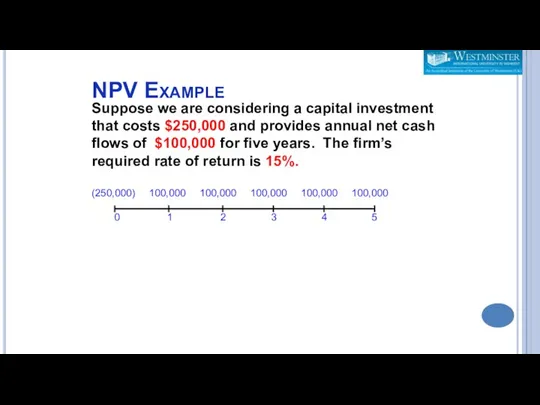

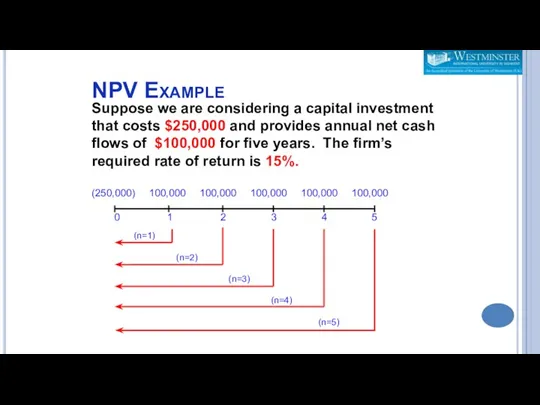

- 26. NPV Example Suppose we are considering a capital investment that costs $250,000 and provides annual net

- 27. NPV Example Suppose we are considering a capital investment that costs $250,000 and provides annual net

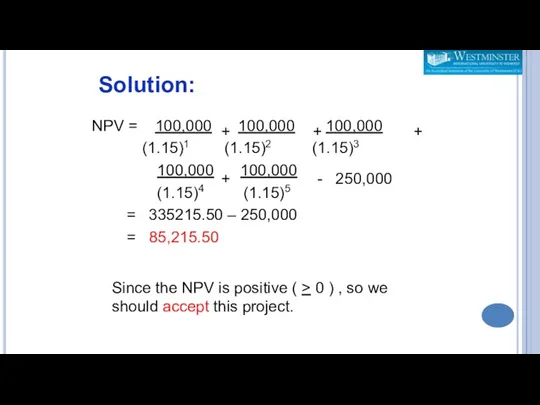

- 28. NPV = 100,000 100,000 100,000 (1.15)1 (1.15)2 (1.15)3 100,000 100,000 (1.15)4 (1.15)5 = 335215.50 – 250,000

- 29. n = 5 k = 15% PMT = 100,000 PV of cash flows = 100,000 (PVIFA15%,5)

- 30. Net Present Value Advantages: Uses free cash flows Recognizes the time value of money Consistent with

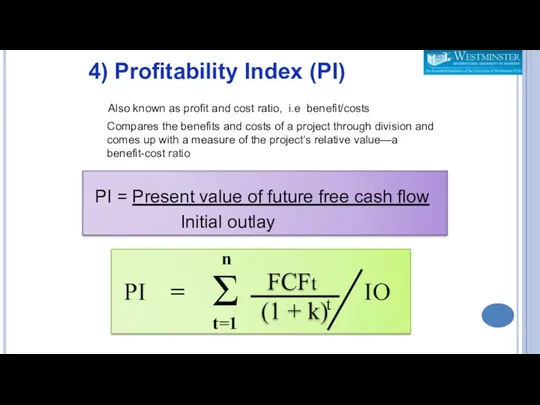

- 31. Also known as profit and cost ratio, i.e benefit/costs Compares the benefits and costs of a

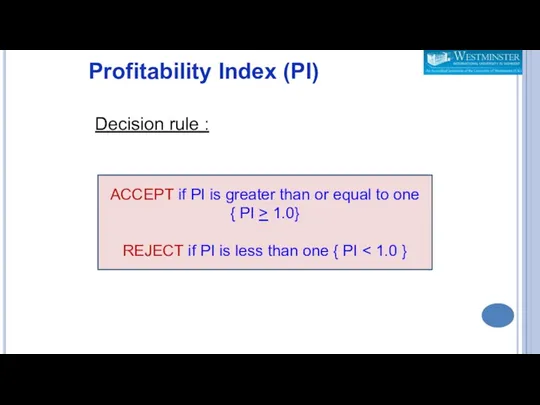

- 32. Profitability Index (PI) Decision rule : ACCEPT if PI is greater than or equal to one

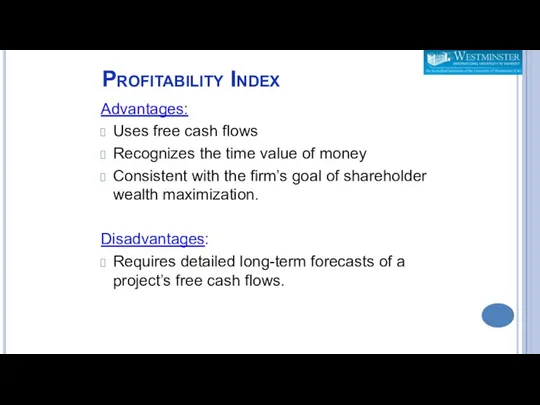

- 33. Profitability Index Advantages: Uses free cash flows Recognizes the time value of money Consistent with the

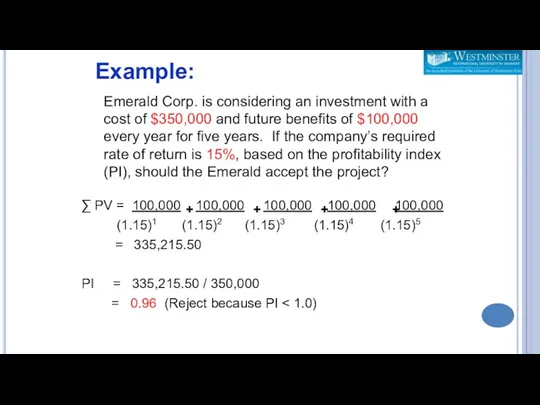

- 34. Emerald Corp. is considering an investment with a cost of $350,000 and future benefits of $100,000

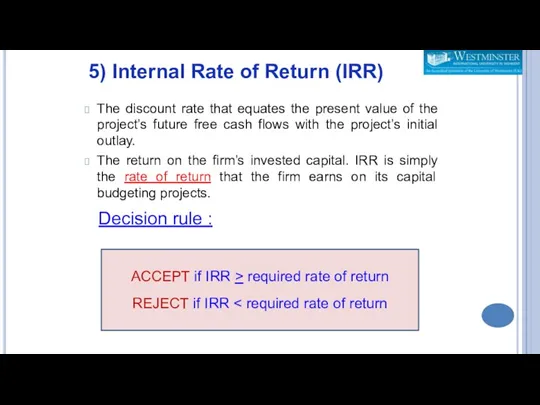

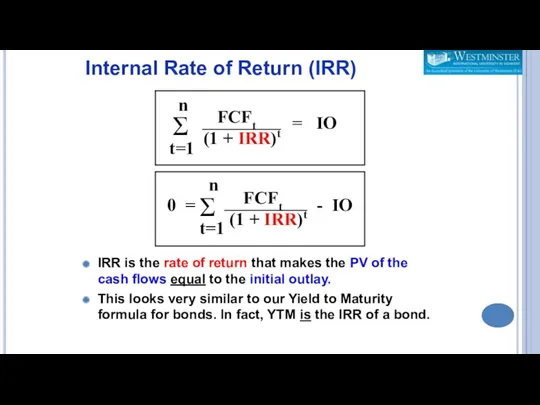

- 35. The discount rate that equates the present value of the project’s future free cash flows with

- 36. IRR is the rate of return that makes the PV of the cash flows equal to

- 37. Calculating IRR Bennett Company is a medium sized metal fabricator that is currently contemplating two projects:

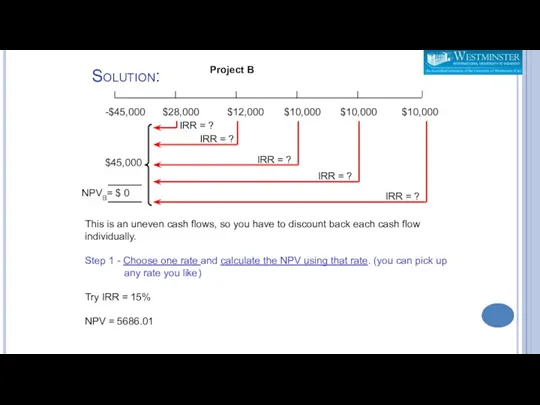

- 38. Solution: -$42,000 $14,000 $14,000 $14,000 $14,000 $14,000 -$45,000 $28,000 $12,000 $10,000 $10,000 $10,000 $45,000 NPVB= $

- 39. Method: trial and error Choose one rate and calculate the NPV using that rate. If your

- 40. Solution: -$42,000 $14,000 $14,000 $14,000 $14,000 $14,000 NPVA= $ 0 $42,000 IRR = ? Project A

- 41. Solution: -$42,000 $14,000 $14,000 $14,000 $14,000 $14,000 NPVA= $ 0 $42,000 IRR = ? Project A

- 42. Solution: -$42,000 $14,000 $14,000 $14,000 $14,000 $14,000 NPVA= $ 0 $42,000 IRR = ? Project A

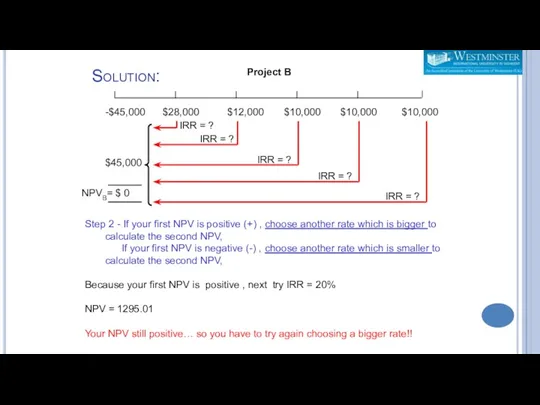

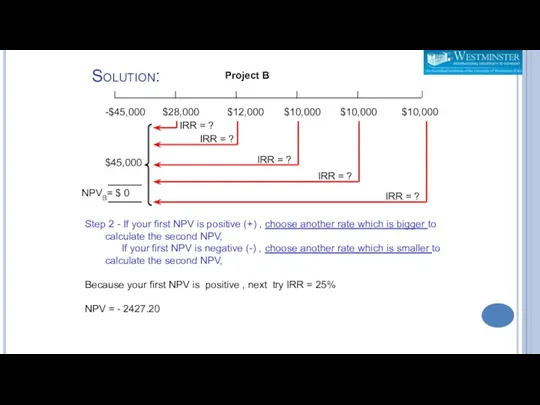

- 43. Solution: -$45,000 $28,000 $12,000 $10,000 $10,000 $10,000 $45,000 NPVB= $ 0 IRR = ? IRR =

- 44. Solution: -$45,000 $28,000 $12,000 $10,000 $10,000 $10,000 $45,000 NPVB= $ 0 IRR = ? IRR =

- 45. Solution: -$45,000 $28,000 $12,000 $10,000 $10,000 $10,000 $45,000 NPVB= $ 0 IRR = ? IRR =

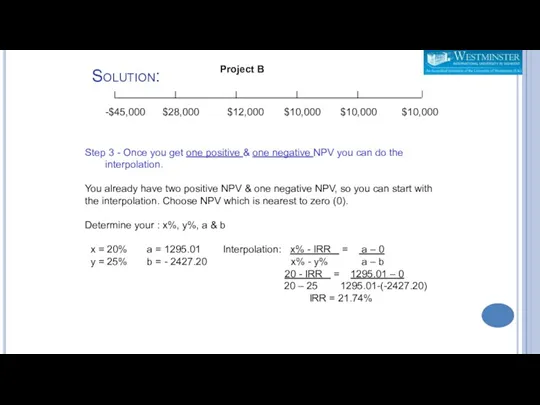

- 46. Solution: -$45,000 $28,000 $12,000 $10,000 $10,000 $10,000 Project B Step 3 - Once you get one

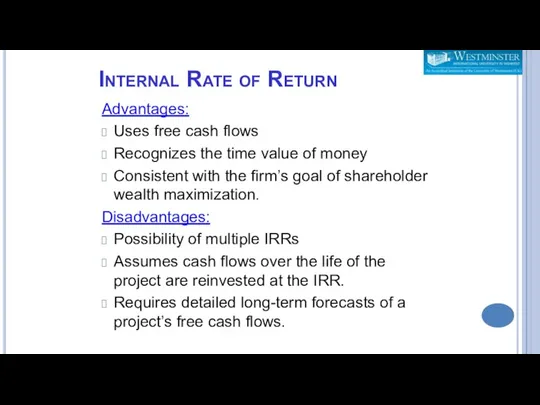

- 47. Internal Rate of Return Advantages: Uses free cash flows Recognizes the time value of money Consistent

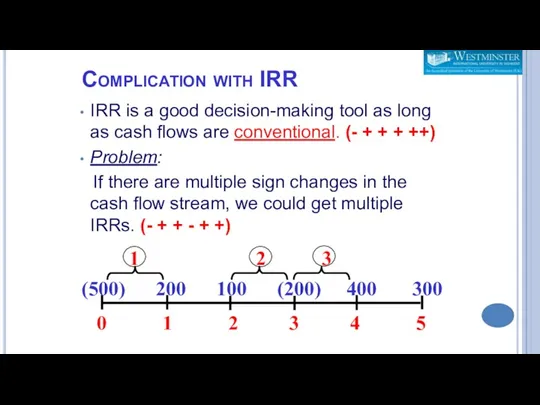

- 48. IRR is a good decision-making tool as long as cash flows are conventional. (- + +

- 49. Modified Internal Rate of Return (MIRR) IRR assumes that all cash flows are reinvested at the

- 50. Modified Internal Rate of Return (MIRR)

- 52. Скачать презентацию

Lecture 5. Investment criteria

Lecture 5. Investment criteria

How should a firm make an investment decision

What assets do we

How should a firm make an investment decision

What assets do we

Capital Budgeting:

The process of planning for purchases of long-term assets.

Example:

Capital Budgeting:

The process of planning for purchases of long-term assets.

Example:

Decision-making Criteria in Capital Budgeting

How do we decide if a capital

Decision-making Criteria in Capital Budgeting

How do we decide if a capital

Decision-making Criteria in Capital Budgeting

The ideal evaluation method should:

include all cash

Decision-making Criteria in Capital Budgeting

The ideal evaluation method should:

include all cash

Decision-making Criteria in Capital Budgeting

Firms invest in 2 categories of projects:

Independent

Decision-making Criteria in Capital Budgeting

Firms invest in 2 categories of projects:

Independent

Techniques in Capital Budgeting

Payback period

Discounted Payback Period

Net Present Value (NPV)

Profitability Index

Techniques in Capital Budgeting

Payback period

Discounted Payback Period

Net Present Value (NPV)

Profitability Index

1) Payback Period

The payback method simply measures how long (in years

1) Payback Period

The payback method simply measures how long (in years

How long will it take for the project to generate

How long will it take for the project to generate

Bennett Company is a medium sized metal fabricator that is currently

Bennett Company is a medium sized metal fabricator that is currently

Example (cont.)

Example (cont.)

Payback Period

Project A

Year Cash flow

1 $14,000

2 $14,000

3 $14,000

4 $14,000

5 $14,000

Initial

Payback Period

Project A

Year Cash flow

1 $14,000

2 $14,000

3 $14,000

4 $14,000

5 $14,000

Initial

Payback Period

Project B

Year Cash flow

1 $28,000

2 $12,000

3 $10,000

4 $10,000

5 $10,000

Initial

Payback Period

Project B

Year Cash flow

1 $28,000

2 $12,000

3 $10,000

4 $10,000

5 $10,000

Initial

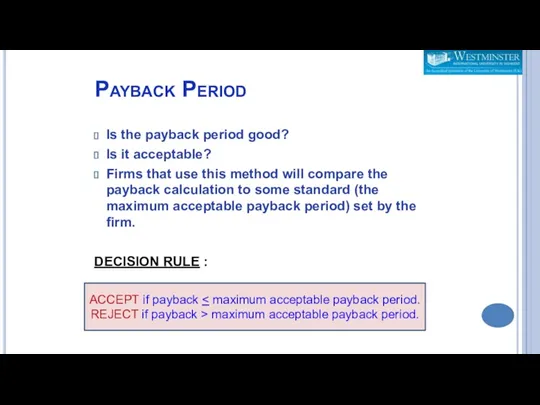

Payback Period

Is the payback period good?

Is it acceptable?

Firms that use this

Payback Period

Is the payback period good?

Is it acceptable?

Firms that use this

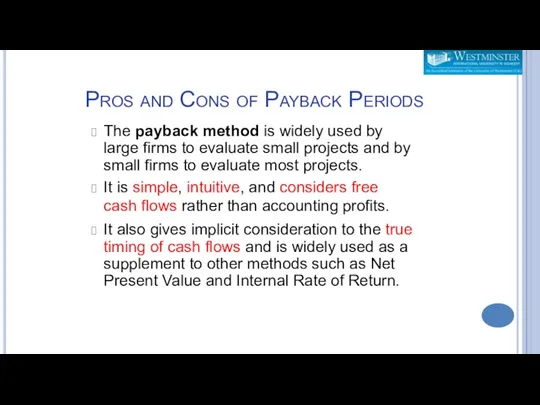

Pros and Cons of Payback Periods

The payback method is widely used

Pros and Cons of Payback Periods

The payback method is widely used

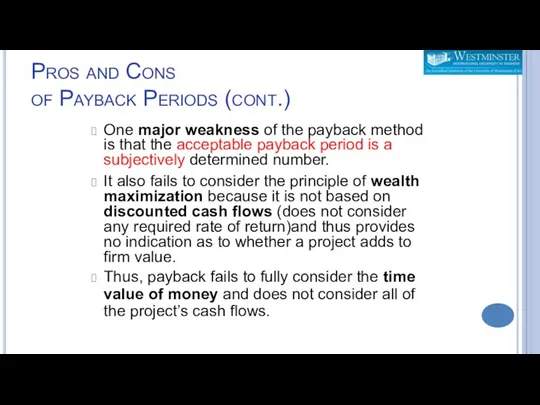

Pros and Cons

of Payback Periods (cont.)

One major weakness of the

Pros and Cons

of Payback Periods (cont.)

One major weakness of the

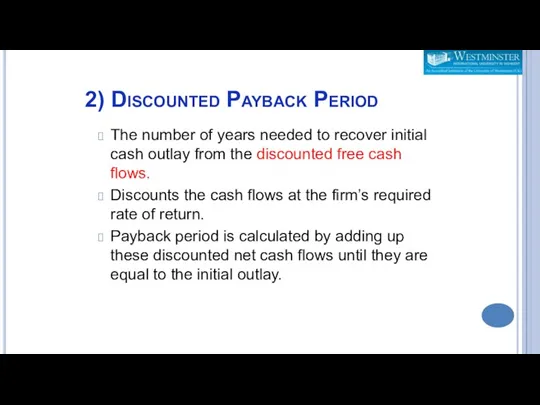

2) Discounted Payback Period

The number of years needed to recover initial

2) Discounted Payback Period

The number of years needed to recover initial

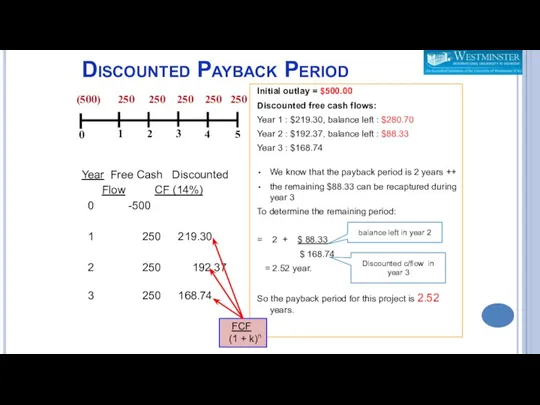

Discounted Payback Period

Year Free Cash Discounted

Flow CF (14%)

Discounted Payback Period

Year Free Cash Discounted

Flow CF (14%)

Discounted Payback Period

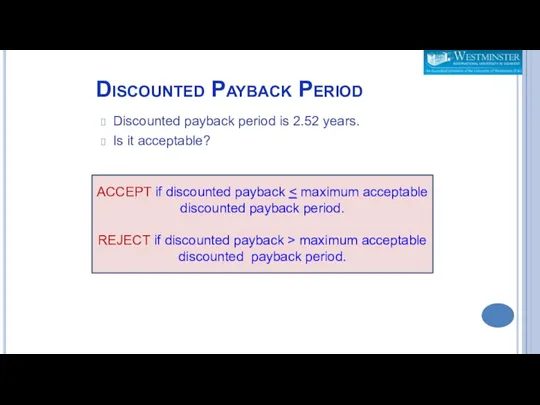

Discounted payback period is 2.52 years.

Is it acceptable?

ACCEPT if

Discounted Payback Period

Discounted payback period is 2.52 years.

Is it acceptable?

ACCEPT if

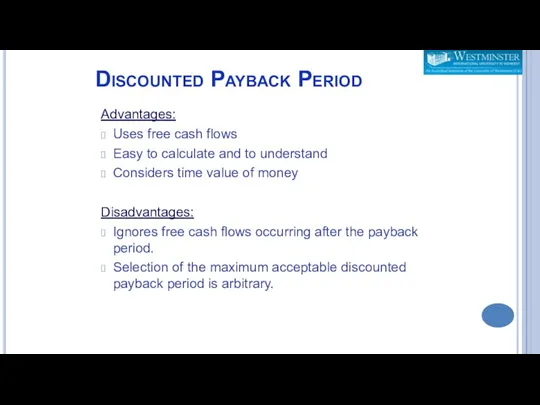

Discounted Payback Period

Advantages:

Uses free cash flows

Easy to calculate and to understand

Considers

Discounted Payback Period

Advantages:

Uses free cash flows

Easy to calculate and to understand

Considers

Other Methods

3) Net Present Value (NPV)

4) Profitability Index (PI)

5) Internal Rate

Other Methods

3) Net Present Value (NPV)

4) Profitability Index (PI)

5) Internal Rate

3) Net Present Value (NPV)

Gives an absolute dollar value for a

3) Net Present Value (NPV)

Gives an absolute dollar value for a

Net Present Value (NPV)

Decision rule :

ACCEPT if NPV is positive {

Net Present Value (NPV)

Decision rule :

ACCEPT if NPV is positive {

Find the PV for every cash flows discounted @ the investors

Find the PV for every cash flows discounted @ the investors

NPV Example

Suppose we are considering a capital investment that costs $250,000

NPV Example

Suppose we are considering a capital investment that costs $250,000

NPV Example

Suppose we are considering a capital investment that costs $250,000

NPV Example

Suppose we are considering a capital investment that costs $250,000

NPV = 100,000 100,000 100,000

(1.15)1 (1.15)2 (1.15)3

100,000

NPV = 100,000 100,000 100,000

(1.15)1 (1.15)2 (1.15)3

100,000

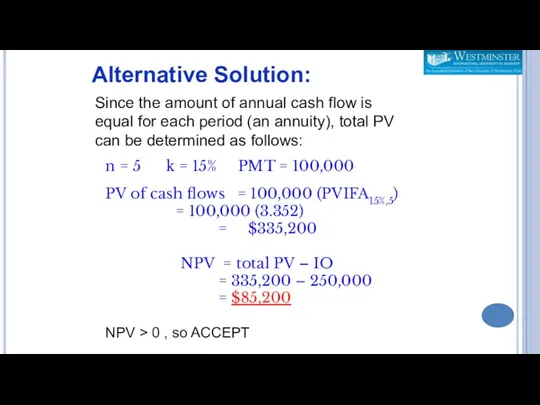

n = 5 k = 15% PMT = 100,000

PV of cash

n = 5 k = 15% PMT = 100,000

PV of cash

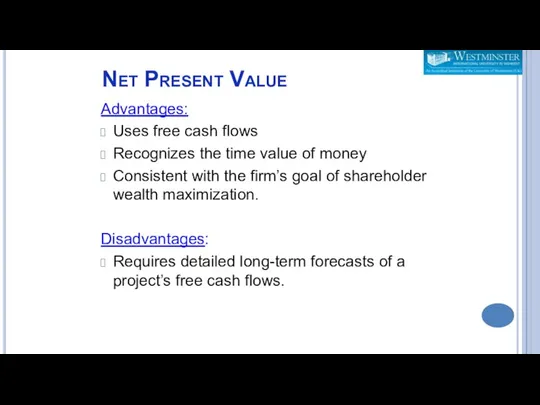

Net Present Value

Advantages:

Uses free cash flows

Recognizes the time value of money

Consistent

Net Present Value

Advantages:

Uses free cash flows

Recognizes the time value of money

Consistent

Also known as profit and cost ratio, i.e benefit/costs

Compares the

Also known as profit and cost ratio, i.e benefit/costs

Compares the

Profitability Index (PI)

Decision rule :

ACCEPT if PI is greater than or

Profitability Index (PI)

Decision rule :

ACCEPT if PI is greater than or

Profitability Index

Advantages:

Uses free cash flows

Recognizes the time value of money

Consistent with

Profitability Index

Advantages:

Uses free cash flows

Recognizes the time value of money

Consistent with

Emerald Corp. is considering an investment with a cost of $350,000

Emerald Corp. is considering an investment with a cost of $350,000

The discount rate that equates the present value of the project’s

The discount rate that equates the present value of the project’s

IRR is the rate of return that makes the PV of

IRR is the rate of return that makes the PV of

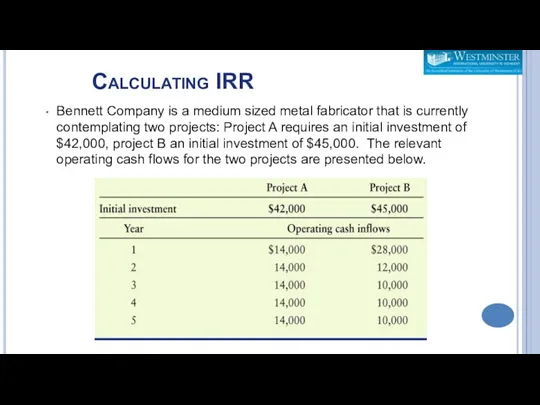

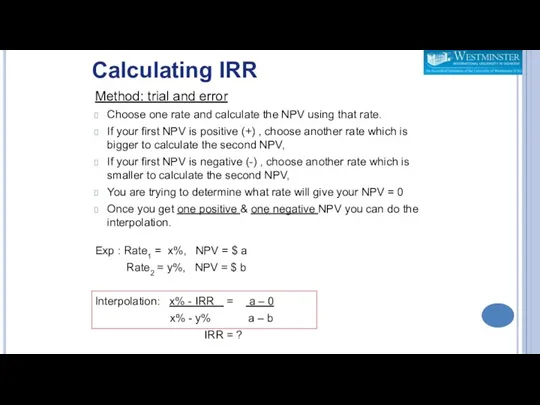

Calculating IRR

Bennett Company is a medium sized metal fabricator that is

Calculating IRR

Bennett Company is a medium sized metal fabricator that is

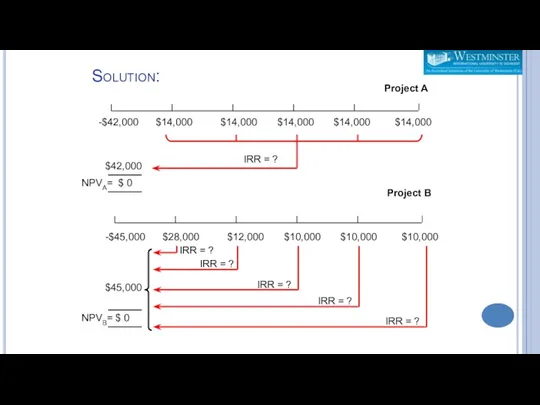

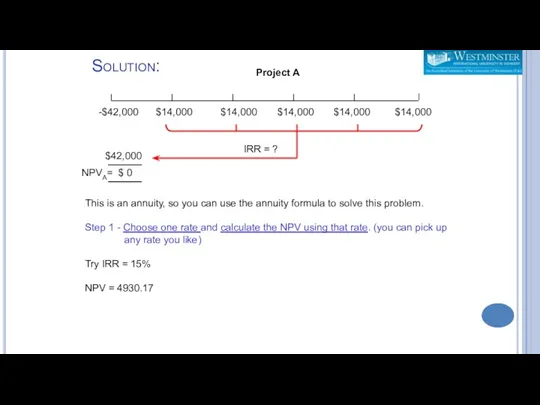

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB=

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB=

Method: trial and error

Choose one rate and calculate the NPV using

Method: trial and error

Choose one rate and calculate the NPV using

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

This

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

This

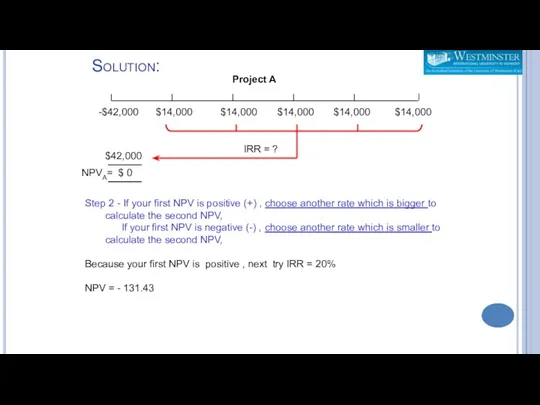

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

Step

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

Step

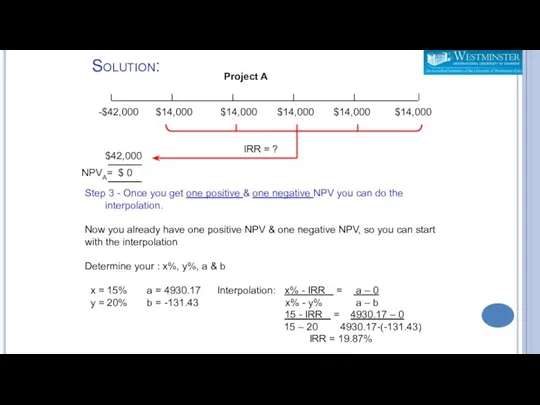

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

Step

Solution:

-$42,000 $14,000 $14,000 $14,000 $14,000 $14,000

NPVA= $ 0

$42,000

IRR = ?

Project A

Step

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

$45,000

NPVB= $ 0

IRR = ?

IRR =

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

Project B

Step 3 - Once you

Solution:

-$45,000 $28,000 $12,000 $10,000 $10,000 $10,000

Project B

Step 3 - Once you

Internal Rate of Return

Advantages:

Uses free cash flows

Recognizes the time value of

Internal Rate of Return

Advantages:

Uses free cash flows

Recognizes the time value of

IRR is a good decision-making tool as long as cash flows

IRR is a good decision-making tool as long as cash flows

Modified Internal Rate of Return (MIRR)

IRR assumes that all cash flows

Modified Internal Rate of Return (MIRR)

IRR assumes that all cash flows

Modified Internal Rate of Return (MIRR)

Modified Internal Rate of Return (MIRR)

Актуальные проблемы налогового контроля в РФ

Актуальные проблемы налогового контроля в РФ Анализ капитальных вложений

Анализ капитальных вложений Банк қызметінің құқықтық негіздері

Банк қызметінің құқықтық негіздері Методика SIGMA

Методика SIGMA Фонд развития промышленности Республики Карелия

Фонд развития промышленности Республики Карелия Бизнес-планирование инновационных проектов

Бизнес-планирование инновационных проектов Лекция 16. Японские свечи

Лекция 16. Японские свечи Доходность и риск финансовой операции

Доходность и риск финансовой операции Денежная система

Денежная система Оценка гудвилла

Оценка гудвилла Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа

Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа Аналіз джерел формування капіталу. Лекція 5

Аналіз джерел формування капіталу. Лекція 5 Управление стоимостью компании

Управление стоимостью компании Вклад Альянса ФМС УрФО в развитие местных сообществ

Вклад Альянса ФМС УрФО в развитие местных сообществ Оборотные средства гостиничного предприятия

Оборотные средства гостиничного предприятия Налог на доходы физических лиц (НДФЛ)

Налог на доходы физических лиц (НДФЛ) Семейный бюджет

Семейный бюджет Концептуальні основи оподаткування

Концептуальні основи оподаткування Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3)

Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3) Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1)

Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1) Activity-Based Costing and Activity-Based Management

Activity-Based Costing and Activity-Based Management Президентские гранты для ННО

Президентские гранты для ННО Салық салу саласындағы мемлекеттік басқару түсінігі,маңызы,міндеттері

Салық салу саласындағы мемлекеттік басқару түсінігі,маңызы,міндеттері Региональная бюджетная система

Региональная бюджетная система Налог на добавленную стоимость

Налог на добавленную стоимость Такафул – исламское страхование

Такафул – исламское страхование ТОО КазМунайГаз-Сервис. Активы компании

ТОО КазМунайГаз-Сервис. Активы компании Фінансові інвестиції

Фінансові інвестиції