- Risk and Return

Содержание

- 2. Topics Covered Markowitz Portfolio Theory Risk and Return Relationship Testing the CAPM CAPM Alternatives

- 3. Markowitz Portfolio Theory Combining stocks into portfolios can reduce standard deviation, below the level obtained from

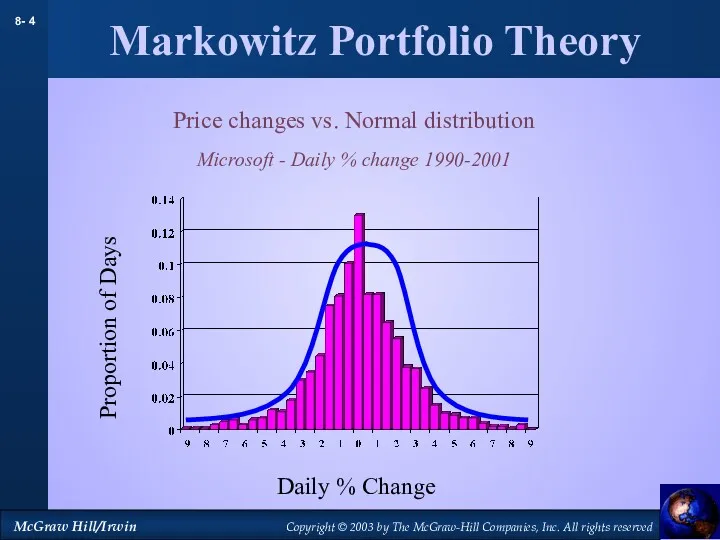

- 4. Markowitz Portfolio Theory Price changes vs. Normal distribution Microsoft - Daily % change 1990-2001 Proportion of

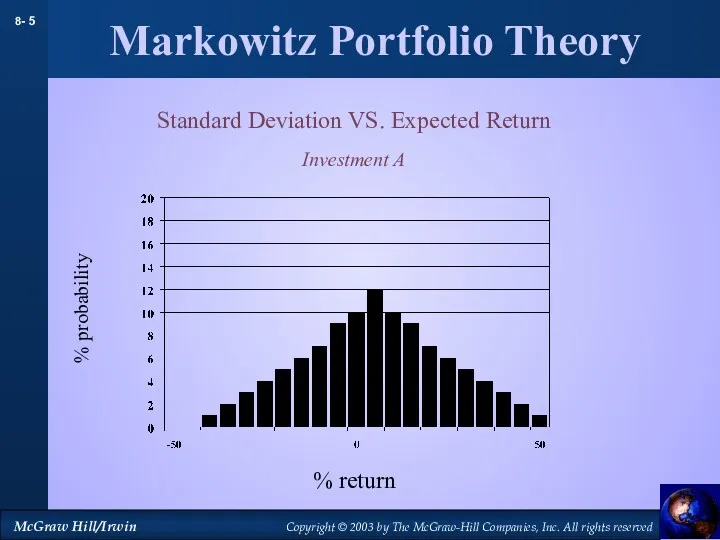

- 5. Markowitz Portfolio Theory Standard Deviation VS. Expected Return Investment A % probability % return

- 6. Markowitz Portfolio Theory Standard Deviation VS. Expected Return Investment B % probability % return

- 7. Markowitz Portfolio Theory Standard Deviation VS. Expected Return Investment C % probability % return

- 8. Markowitz Portfolio Theory Standard Deviation VS. Expected Return Investment D % probability % return

- 9. Markowitz Portfolio Theory Coca Cola Reebok Standard Deviation Expected Return (%) 35% in Reebok Expected Returns

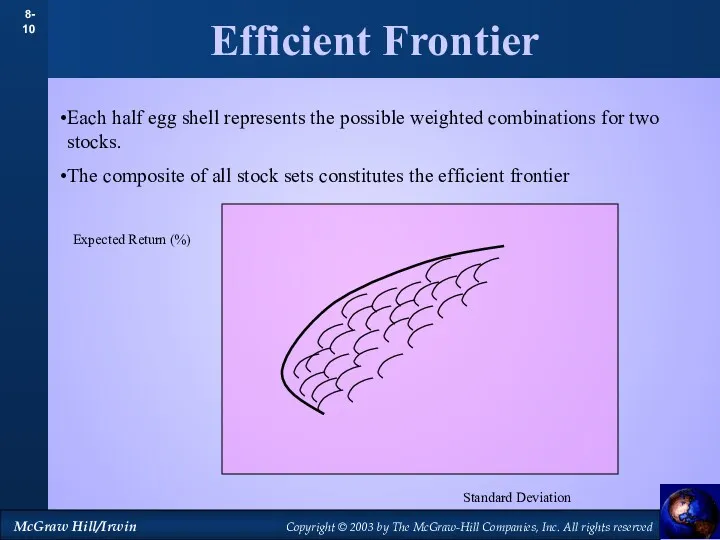

- 10. Efficient Frontier Standard Deviation Expected Return (%) Each half egg shell represents the possible weighted combinations

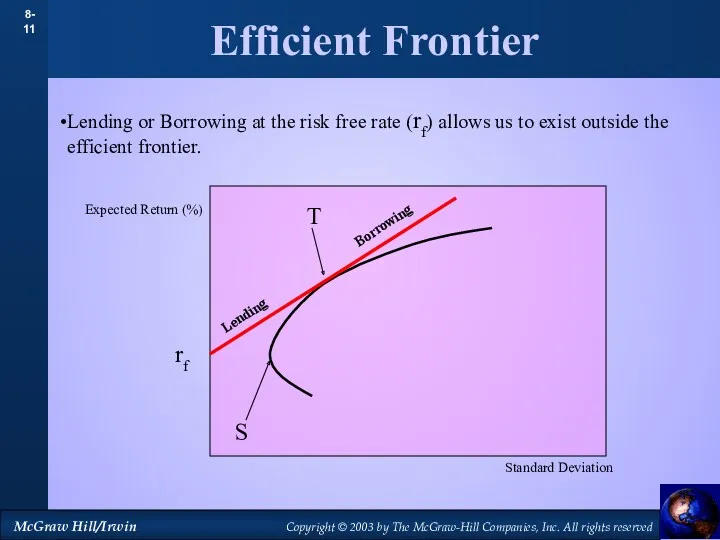

- 11. Efficient Frontier Standard Deviation Expected Return (%) Lending or Borrowing at the risk free rate (rf)

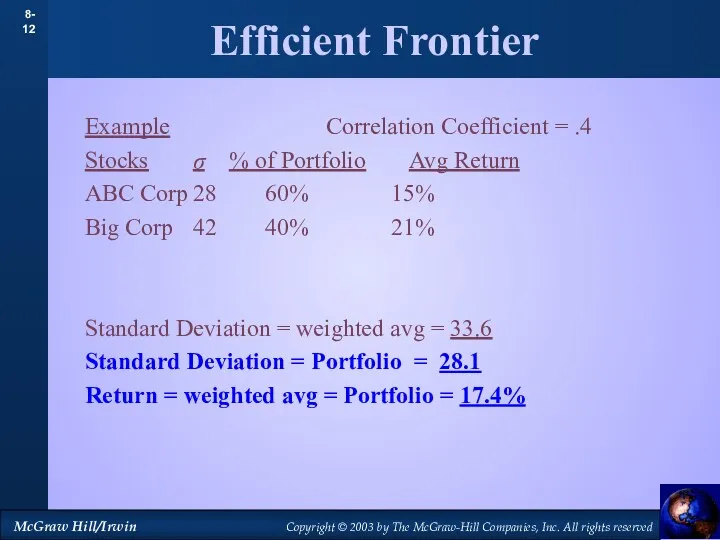

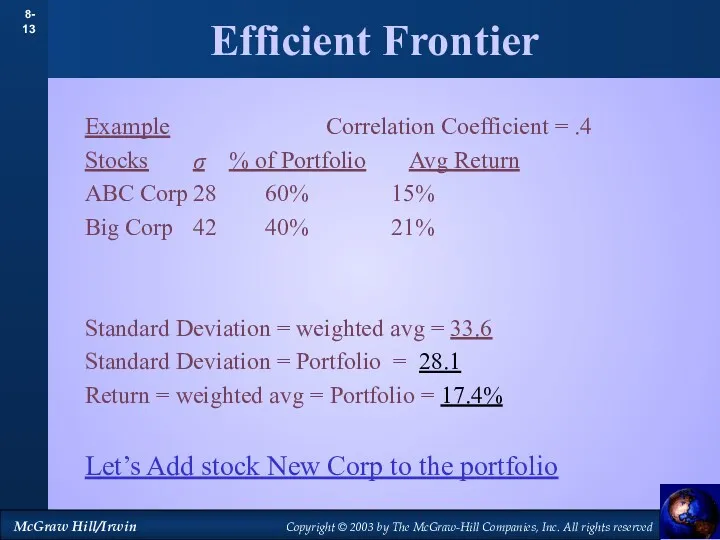

- 12. Efficient Frontier Example Correlation Coefficient = .4 Stocks σ % of Portfolio Avg Return ABC Corp

- 13. Efficient Frontier Example Correlation Coefficient = .4 Stocks σ % of Portfolio Avg Return ABC Corp

- 14. Efficient Frontier Example Correlation Coefficient = .3 Stocks σ % of Portfolio Avg Return Portfolio 28.1

- 15. Efficient Frontier Example Correlation Coefficient = .3 Stocks σ % of Portfolio Avg Return Portfolio 28.1

- 16. Efficient Frontier A B Return Risk (measured as σ)

- 17. Efficient Frontier A B Return Risk AB

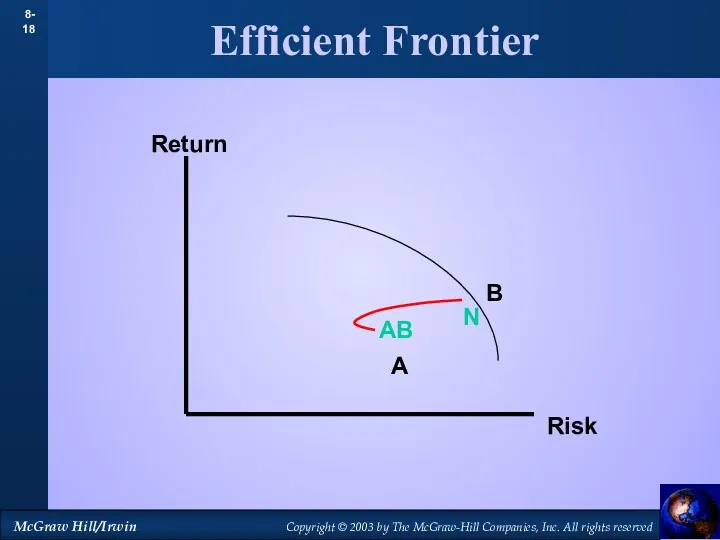

- 18. Efficient Frontier A B N Return Risk AB

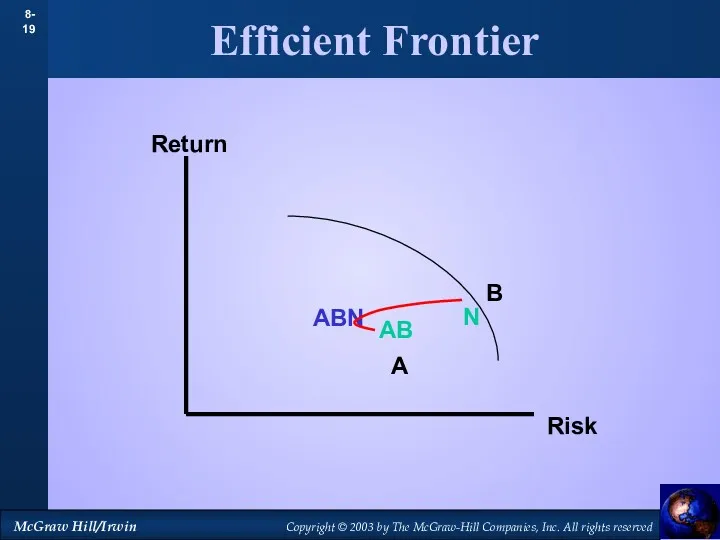

- 19. Efficient Frontier A B N Return Risk AB ABN

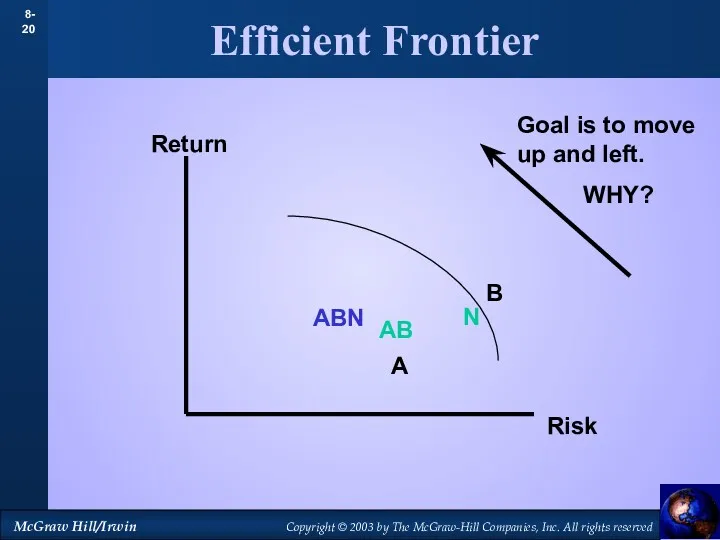

- 20. Efficient Frontier A B N Return Risk AB Goal is to move up and left. WHY?

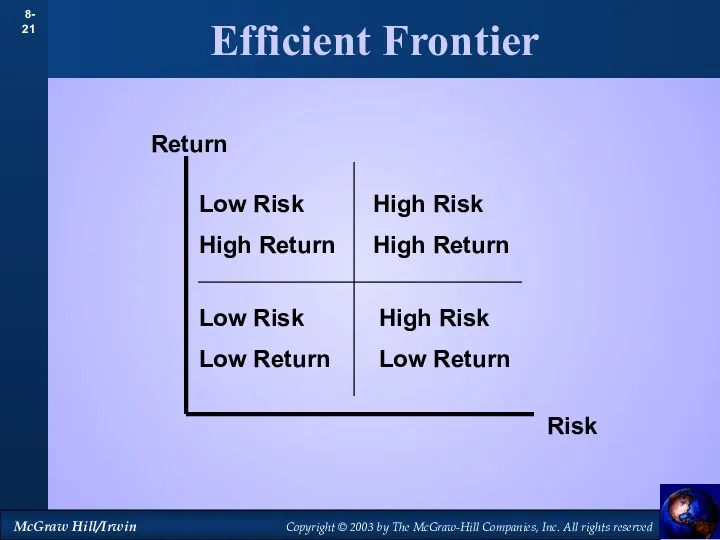

- 21. Efficient Frontier Return Risk Low Risk High Return High Risk High Return Low Risk Low Return

- 22. Efficient Frontier Return Risk Low Risk High Return High Risk High Return Low Risk Low Return

- 23. Efficient Frontier Return Risk A B N AB ABN

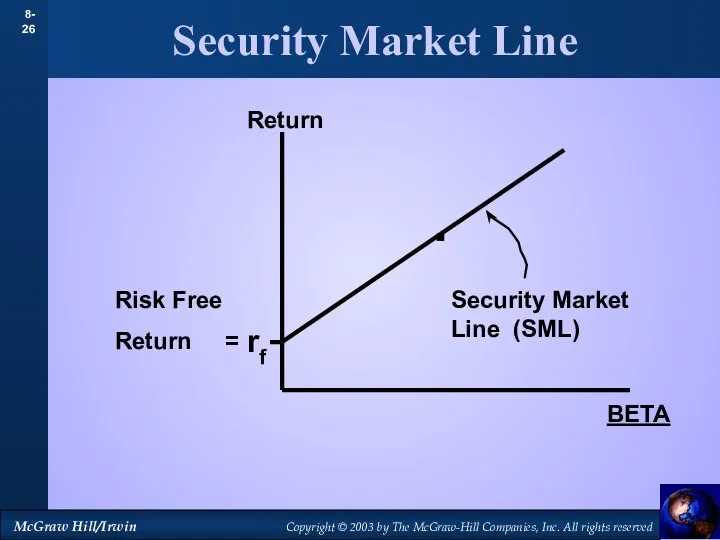

- 24. Security Market Line Return Risk . rf Risk Free Return = Efficient Portfolio

- 25. Security Market Line Return . rf Risk Free Return = Efficient Portfolio BETA 1.0

- 26. Security Market Line Return . rf Risk Free Return = BETA Security Market Line (SML)

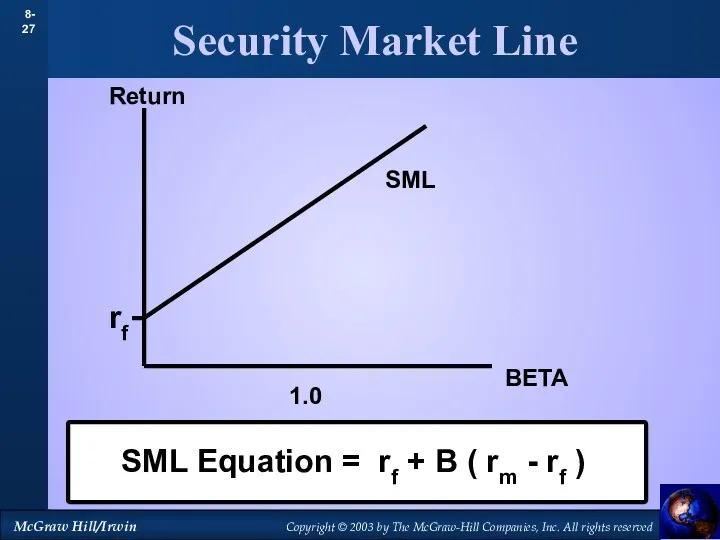

- 27. Security Market Line Return BETA rf 1.0 SML SML Equation = rf + B ( rm

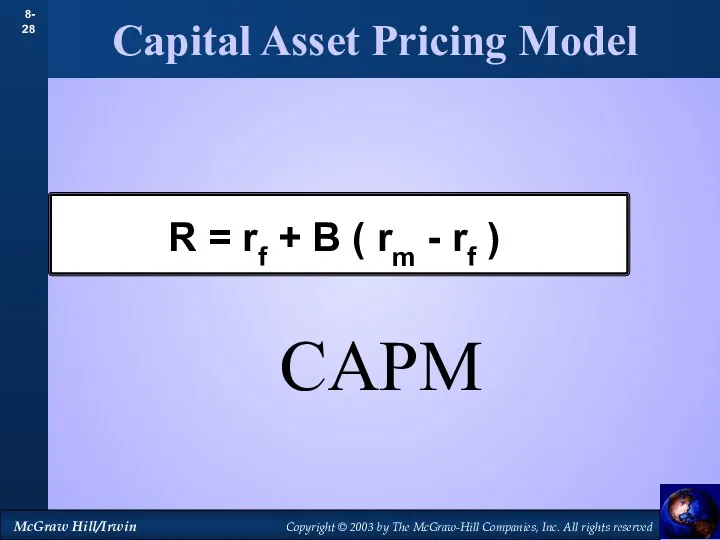

- 28. Capital Asset Pricing Model R = rf + B ( rm - rf ) CAPM

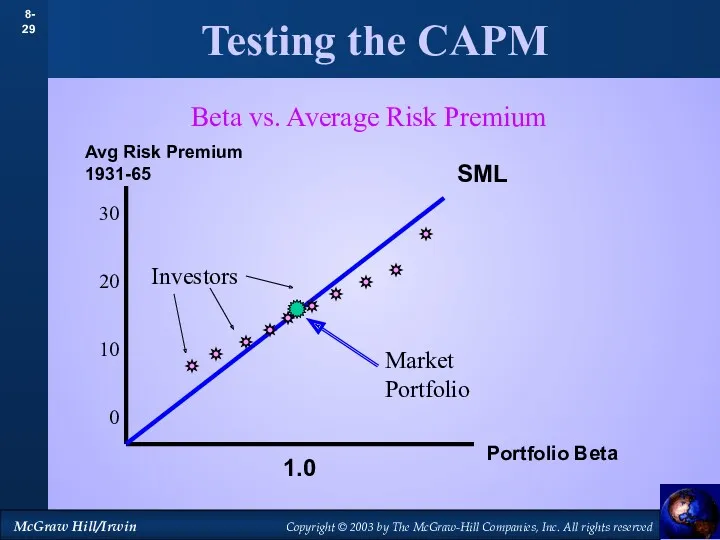

- 29. Testing the CAPM Avg Risk Premium 1931-65 Portfolio Beta 1.0 SML 30 20 10 0 Investors

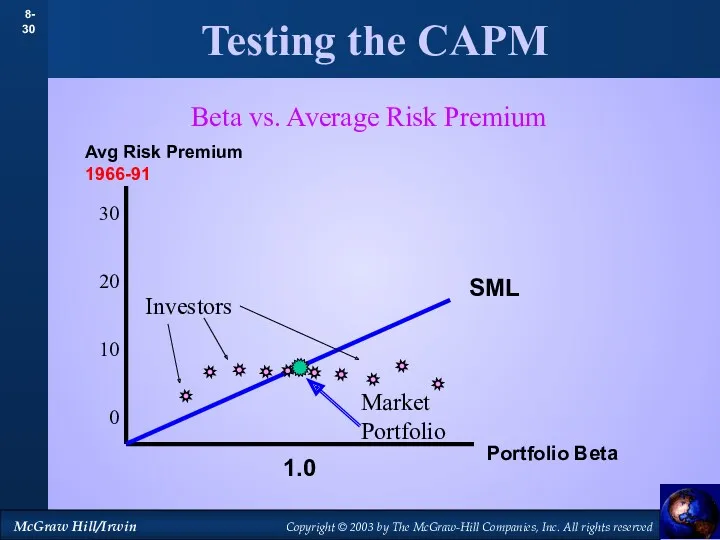

- 30. Testing the CAPM Avg Risk Premium 1966-91 Portfolio Beta 1.0 SML 30 20 10 0 Investors

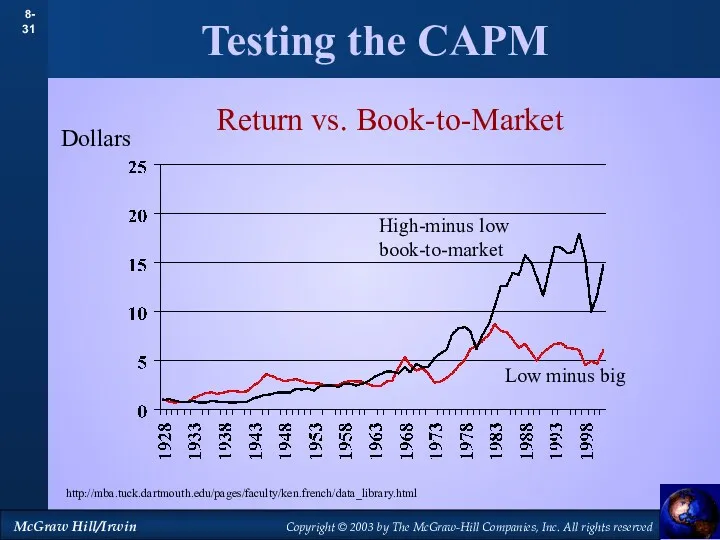

- 31. Testing the CAPM High-minus low book-to-market Return vs. Book-to-Market Dollars Low minus big http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

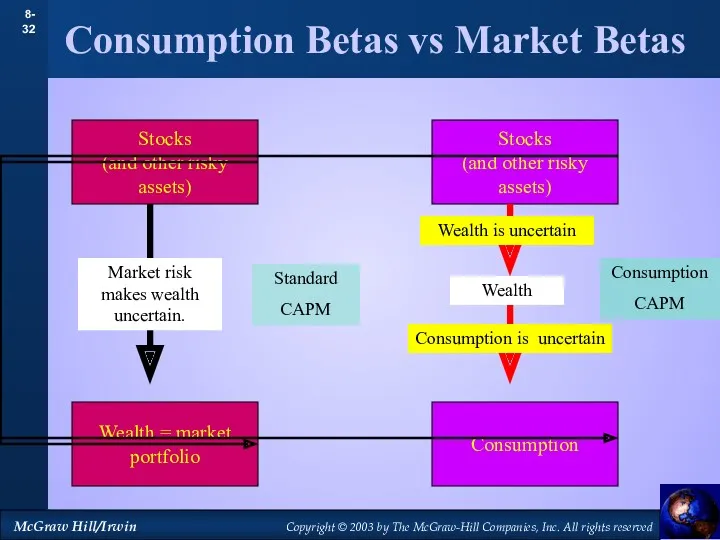

- 32. Consumption Betas vs Market Betas Stocks (and other risky assets) Wealth = market portfolio

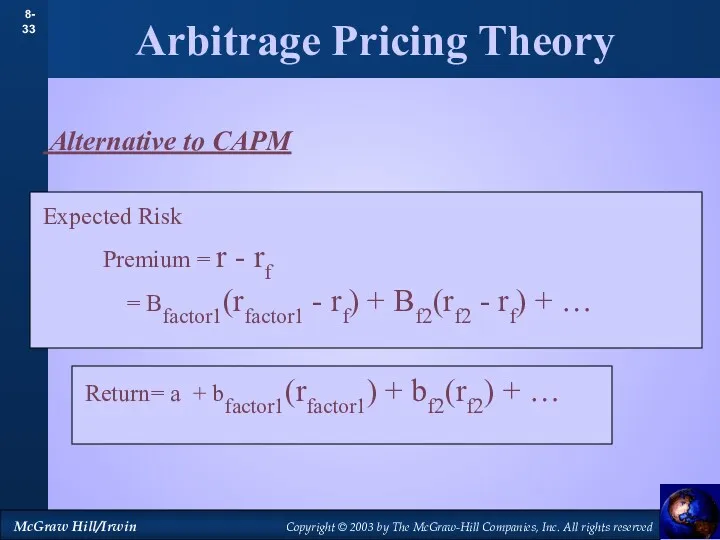

- 33. Arbitrage Pricing Theory Alternative to CAPM Expected Risk Premium = r - rf = Bfactor1(rfactor1 -

- 35. Скачать презентацию

Topics Covered

Markowitz Portfolio Theory

Risk and Return Relationship

Testing the CAPM

CAPM Alternatives

Topics Covered

Markowitz Portfolio Theory

Risk and Return Relationship

Testing the CAPM

CAPM Alternatives

Markowitz Portfolio Theory

Combining stocks into portfolios can reduce standard deviation, below

Markowitz Portfolio Theory

Combining stocks into portfolios can reduce standard deviation, below

Markowitz Portfolio Theory

Price changes vs. Normal distribution

Microsoft - Daily % change

Markowitz Portfolio Theory

Price changes vs. Normal distribution

Microsoft - Daily % change

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment A

% probability

% return

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment A

% probability

% return

Markowitz Portfolio Theory

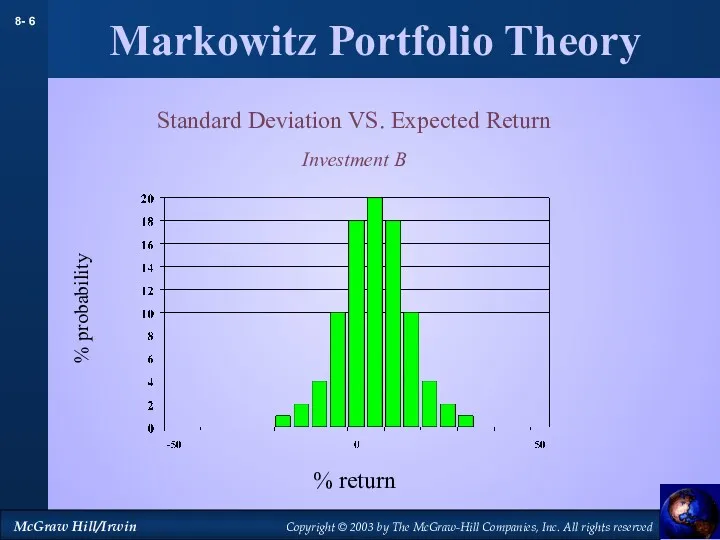

Standard Deviation VS. Expected Return

Investment B

% probability

% return

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment B

% probability

% return

Markowitz Portfolio Theory

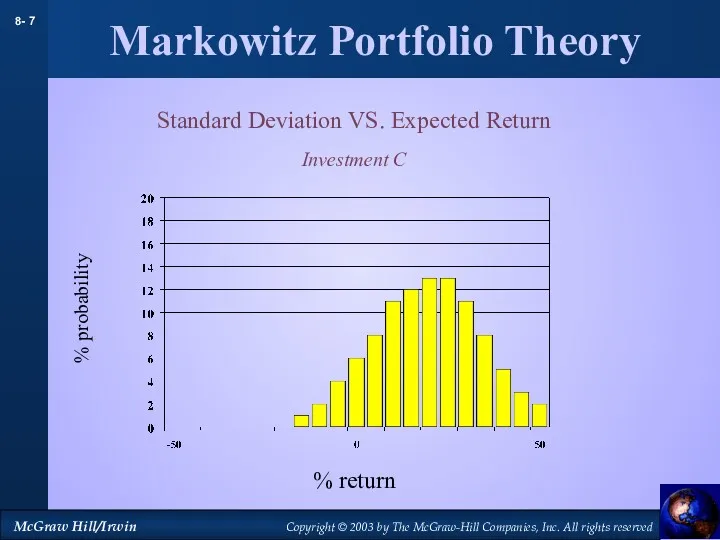

Standard Deviation VS. Expected Return

Investment C

% probability

% return

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment C

% probability

% return

Markowitz Portfolio Theory

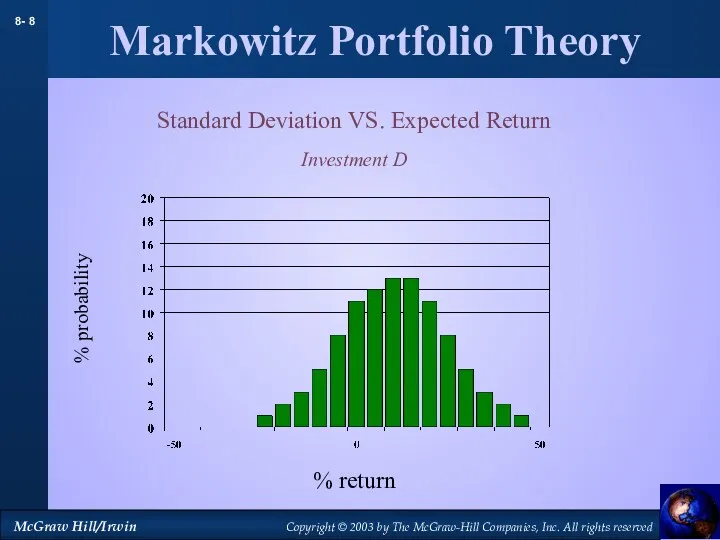

Standard Deviation VS. Expected Return

Investment D

% probability

% return

Markowitz Portfolio Theory

Standard Deviation VS. Expected Return

Investment D

% probability

% return

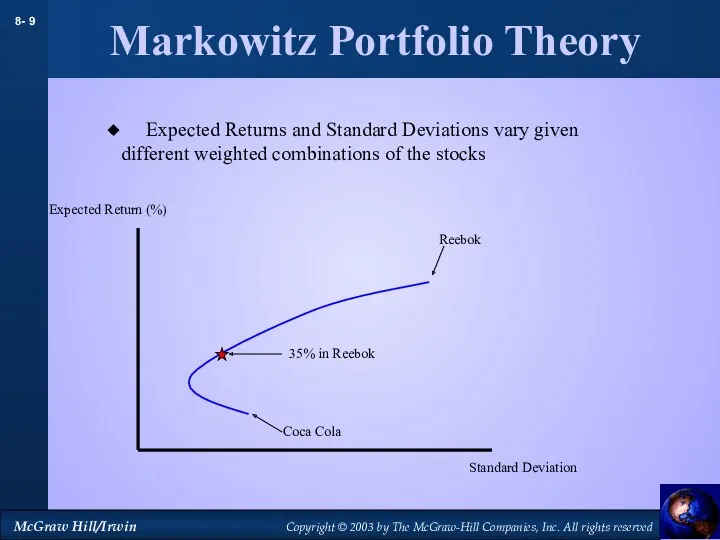

Markowitz Portfolio Theory

Coca Cola

Reebok

Standard Deviation

Expected Return (%)

35% in Reebok

Expected Returns

Markowitz Portfolio Theory

Coca Cola

Reebok

Standard Deviation

Expected Return (%)

35% in Reebok

Expected Returns

Efficient Frontier

Standard Deviation

Expected Return (%)

Each half egg shell represents the possible

Efficient Frontier

Standard Deviation

Expected Return (%)

Each half egg shell represents the possible

Efficient Frontier

Standard Deviation

Expected Return (%)

Lending or Borrowing at the risk free

Efficient Frontier

Standard Deviation

Expected Return (%)

Lending or Borrowing at the risk free

Efficient Frontier

Example Correlation Coefficient = .4

Stocks σ % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big

Efficient Frontier

Example Correlation Coefficient = .4

Stocks σ % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big

Efficient Frontier

Example Correlation Coefficient = .4

Stocks σ % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big

Efficient Frontier

Example Correlation Coefficient = .4

Stocks σ % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big

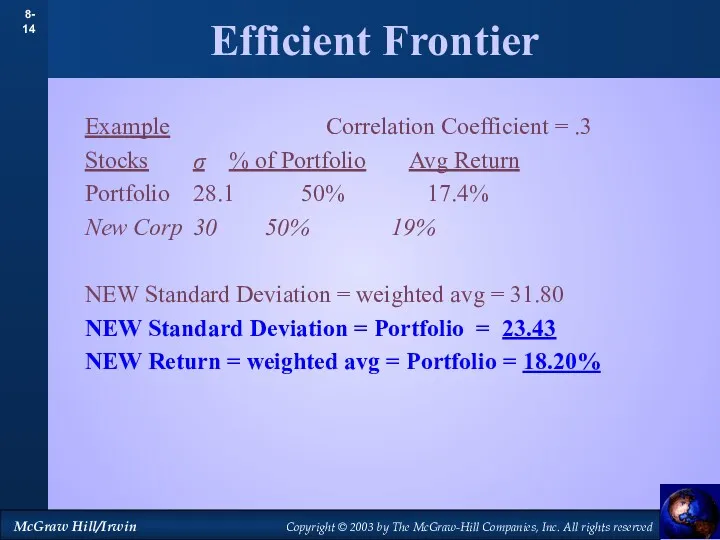

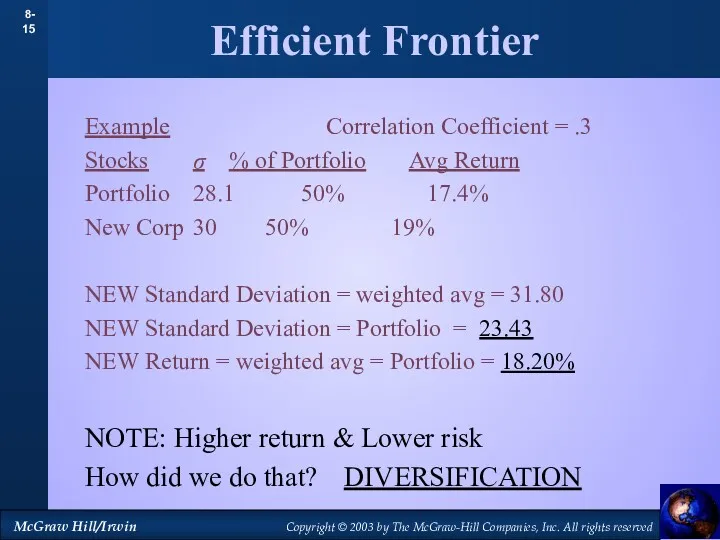

Efficient Frontier

Example Correlation Coefficient = .3

Stocks σ % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30

Efficient Frontier

Example Correlation Coefficient = .3

Stocks σ % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30

Efficient Frontier

Example Correlation Coefficient = .3

Stocks σ % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30

Efficient Frontier

Example Correlation Coefficient = .3

Stocks σ % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30

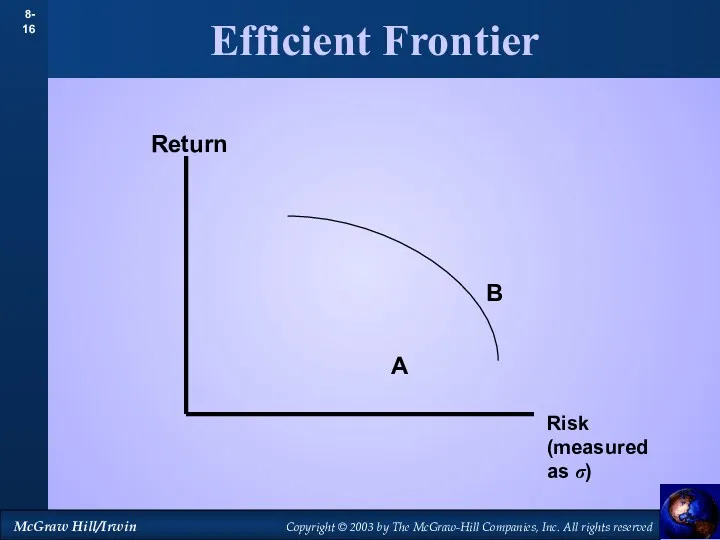

Efficient Frontier

A

B

Return

Risk (measured as σ)

Efficient Frontier

A

B

Return

Risk (measured as σ)

Efficient Frontier

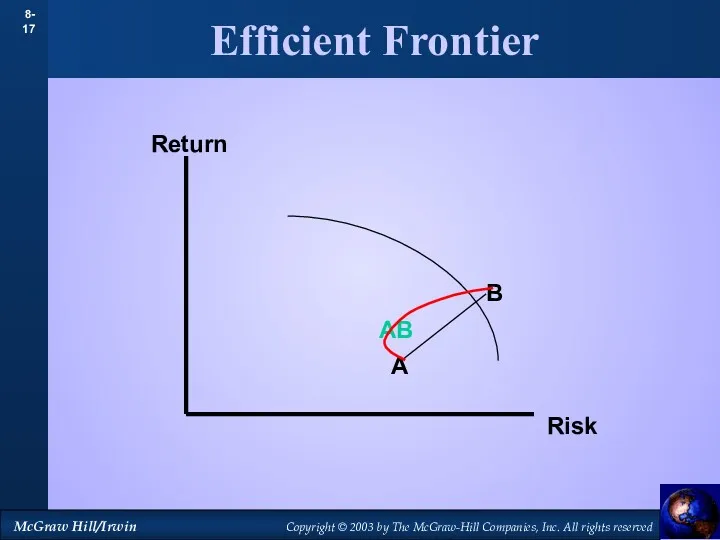

A

B

Return

Risk

AB

Efficient Frontier

A

B

Return

Risk

AB

Efficient Frontier

A

B

N

Return

Risk

AB

Efficient Frontier

A

B

N

Return

Risk

AB

Efficient Frontier

A

B

N

Return

Risk

AB

ABN

Efficient Frontier

A

B

N

Return

Risk

AB

ABN

Efficient Frontier

A

B

N

Return

Risk

AB

Goal is to move up and left.

WHY?

ABN

Efficient Frontier

A

B

N

Return

Risk

AB

Goal is to move up and left.

WHY?

ABN

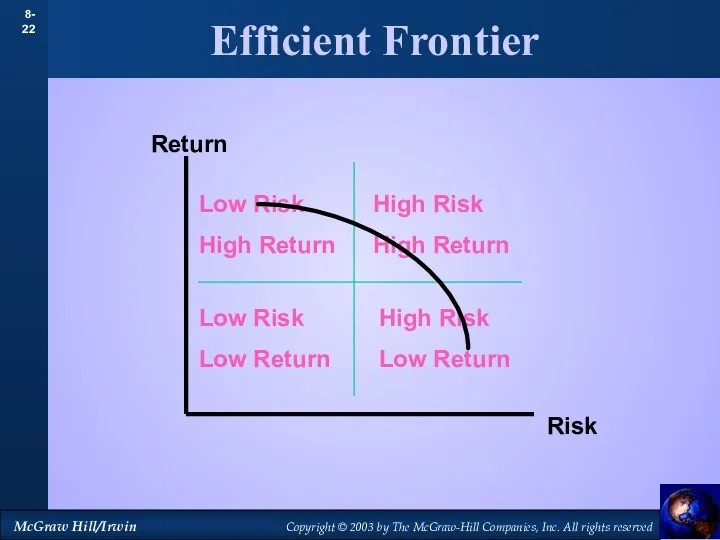

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

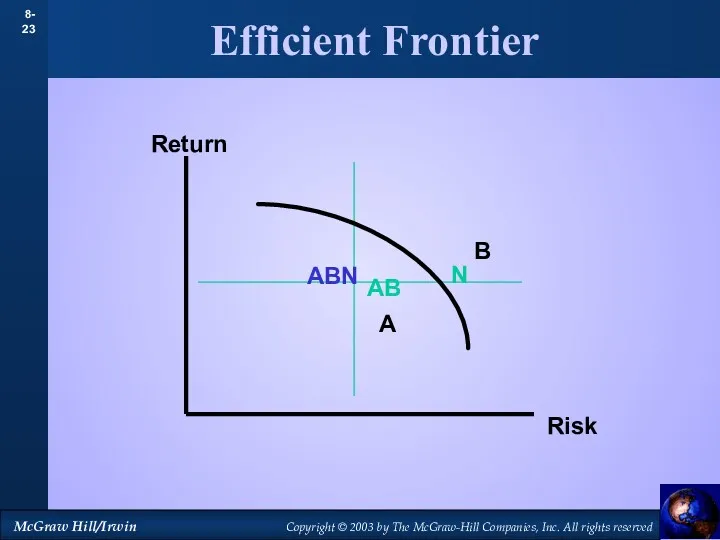

Efficient Frontier

Return

Risk

A

B

N

AB

ABN

Efficient Frontier

Return

Risk

A

B

N

AB

ABN

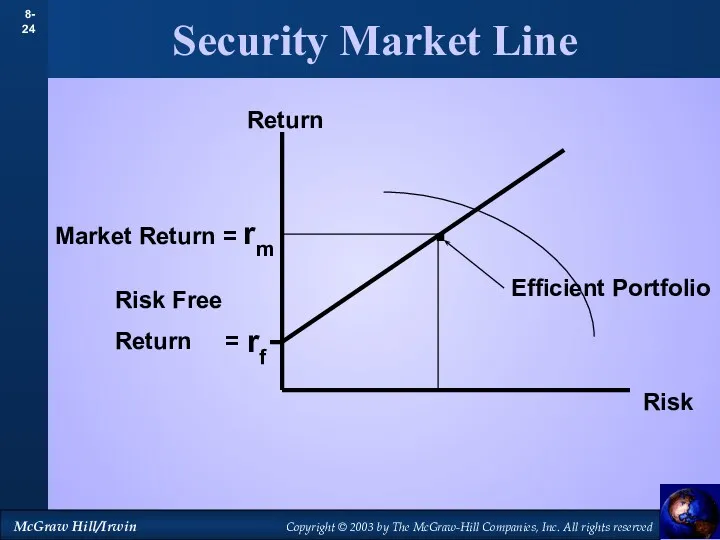

Security Market Line

Return

Risk

.

rf

Risk Free

Return =

Efficient Portfolio

Security Market Line

Return

Risk

.

rf

Risk Free

Return =

Efficient Portfolio

Security Market Line

Return

.

rf

Risk Free

Return =

Efficient Portfolio

BETA

1.0

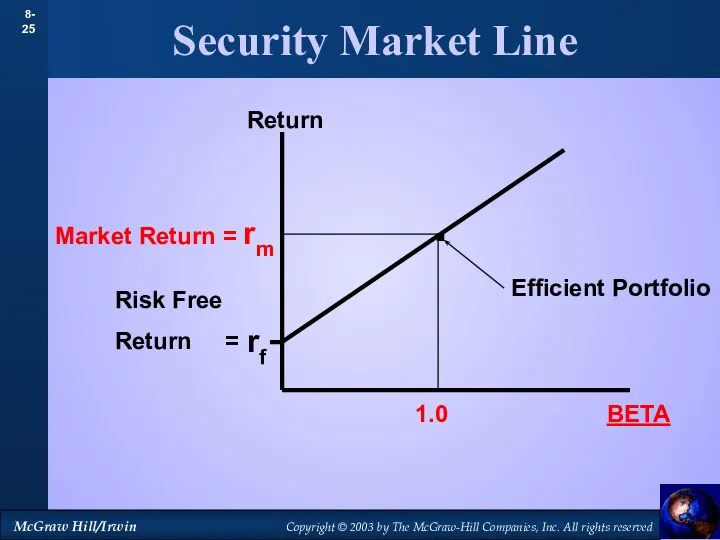

Security Market Line

Return

.

rf

Risk Free

Return =

Efficient Portfolio

BETA

1.0

Security Market Line

Return

.

rf

Risk Free

Return =

BETA

Security Market Line (SML)

Security Market Line

Return

.

rf

Risk Free

Return =

BETA

Security Market Line (SML)

Security Market Line

Return

BETA

rf

1.0

SML

SML Equation = rf + B ( rm -

Security Market Line

Return

BETA

rf

1.0

SML

SML Equation = rf + B ( rm -

Capital Asset Pricing Model

R = rf + B ( rm

Capital Asset Pricing Model

R = rf + B ( rm

Testing the CAPM

Avg Risk Premium 1931-65

Portfolio Beta

1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk

Testing the CAPM

Avg Risk Premium 1931-65

Portfolio Beta

1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk

Testing the CAPM

Avg Risk Premium 1966-91

Portfolio Beta

1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk

Testing the CAPM

Avg Risk Premium 1966-91

Portfolio Beta

1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk

Testing the CAPM

High-minus low book-to-market

Return vs. Book-to-Market

Dollars

Low minus big

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

Testing the CAPM

High-minus low book-to-market

Return vs. Book-to-Market

Dollars

Low minus big

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

Consumption Betas vs Market Betas

Stocks

(and other risky assets)

Wealth = market

portfolio

Consumption Betas vs Market Betas

Stocks

(and other risky assets)

Wealth = market

portfolio

Arbitrage Pricing Theory

Alternative to CAPM

Expected Risk

Premium = r

Arbitrage Pricing Theory

Alternative to CAPM

Expected Risk

Premium = r

Structuring. Transaction Framework

Structuring. Transaction Framework Контрольно-кассовые машины

Контрольно-кассовые машины Школа инвестиций НИУ-ВШЭ: программа и преимущества

Школа инвестиций НИУ-ВШЭ: программа и преимущества Долгосрочные внеоборотные активы

Долгосрочные внеоборотные активы Экологический сбор

Экологический сбор Базы оценки, отличные от рыночной стоимости

Базы оценки, отличные от рыночной стоимости Налог на доходы физических лиц

Налог на доходы физических лиц Счета бухгалтерского учета и план счетов

Счета бухгалтерского учета и план счетов Государственные и муниципальные финансы как элемент финансово-кредитной системы

Государственные и муниципальные финансы как элемент финансово-кредитной системы International, national and contractual frameworks of investment protection. Class 2

International, national and contractual frameworks of investment protection. Class 2 Основы организации бухгалтерского учета в кредитных организациях

Основы организации бухгалтерского учета в кредитных организациях Повышенная стипендия за достижения в научно-исследовательской деятельности

Повышенная стипендия за достижения в научно-исследовательской деятельности Баланс как основная форма финансовой отчетности. Часть 2. Пассив

Баланс как основная форма финансовой отчетности. Часть 2. Пассив Стандарты аудиторской деятельности, регулирующие форму, содержание, предоставление аудиторского заключения

Стандарты аудиторской деятельности, регулирующие форму, содержание, предоставление аудиторского заключения Доллар США

Доллар США Введение налога на профессиональный доход для самозанятых граждан

Введение налога на профессиональный доход для самозанятых граждан Земельный налог

Земельный налог Организация бюджетного процесса в поселении. (Тема 4.6)

Организация бюджетного процесса в поселении. (Тема 4.6) Бухгалтерская (финансовая) отчетность

Бухгалтерская (финансовая) отчетность Эмиссия ценных бумаг. (Тема 6)

Эмиссия ценных бумаг. (Тема 6) Финансовая система, характеристика звеньев. Тема 4

Финансовая система, характеристика звеньев. Тема 4 Сметное дело. Методы составления смет и сметной документации. (Лекция 11)

Сметное дело. Методы составления смет и сметной документации. (Лекция 11) Эволюция мировой валютной системы и современные валютные проблемы. Лекция 3

Эволюция мировой валютной системы и современные валютные проблемы. Лекция 3 Финансовая работа в первичной профсоюзной организации

Финансовая работа в первичной профсоюзной организации Поддержка малого и среднего предпринимательства в Московской области в 2018 году

Поддержка малого и среднего предпринимательства в Московской области в 2018 году Государственный бюджет. Тест №50. 3 класс

Государственный бюджет. Тест №50. 3 класс Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа

Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа Валютные курсы и эффективность экспортных и импортных операций. Страхование валютных рисков. Хеджирование

Валютные курсы и эффективность экспортных и импортных операций. Страхование валютных рисков. Хеджирование