- The cost of goods sold

Содержание

- 2. is a product of activity (including works, services) intended for sale or exchange. The product

- 3. THE COST OF GOODS SOLD The cost of goods sold refers to the carrying value of

- 4. THE COST OF GOODS FOR RESALE The cost of goods purchased for resale includes purchase price

- 5. Since the financial statements of aims such period costs as purchasing Department, warehouse, and other operational

- 6. Identification of the agreement In some cases, the cost of goods sold may be identified with

- 7. Certain identification. Under this method, special items and costs tracked for each item. This may require

- 8. Method of "first come - first out" (FIFO) assumes that goods purchased or produced first are

- 9. LIFO Dollar value. With this change LIFO increase or decrease in the LIFO reserve are determined

- 11. Скачать презентацию

is a product of activity (including works, services) intended for sale

is a product of activity (including works, services) intended for sale

THE COST OF GOODS SOLD

The cost of goods sold refers to

THE COST OF GOODS SOLD

The cost of goods sold refers to

THE COST OF GOODS FOR RESALE

The cost of goods purchased

THE COST OF GOODS FOR RESALE

The cost of goods purchased

Since the financial statements of aims such period costs as

Since the financial statements of aims such period costs as

Identification of the agreement

In some cases, the cost of goods

Identification of the agreement

In some cases, the cost of goods

Certain identification. Under this method, special items and costs tracked for

Certain identification. Under this method, special items and costs tracked for

Method of "first come - first out" (FIFO) assumes that goods

Method of "first come - first out" (FIFO) assumes that goods

LIFO Dollar value. With this change LIFO increase or decrease in

LIFO Dollar value. With this change LIFO increase or decrease in

Банк, как система одного окна. Промсвязьбанк

Банк, как система одного окна. Промсвязьбанк Развитие денежных и финансовых отношений в XV-XVI веках. (Тема 3)

Развитие денежных и финансовых отношений в XV-XVI веках. (Тема 3) Тәуекел осындай жағымсыз нәтижелерді алу ықтималдығы

Тәуекел осындай жағымсыз нәтижелерді алу ықтималдығы Примеры успешного краудсорсинга

Примеры успешного краудсорсинга Финансовая устойчивость, платежеспособность и рентабельность предприятия ИГиТ

Финансовая устойчивость, платежеспособность и рентабельность предприятия ИГиТ Государственная финансовая система. Бюджетно-налоговая политика

Государственная финансовая система. Бюджетно-налоговая политика Денежные потоки инвестиционного проекта. Критерии оценки инвестиций

Денежные потоки инвестиционного проекта. Критерии оценки инвестиций Методические приемы ревизии и контроля

Методические приемы ревизии и контроля Форма расчета 6-НДФЛ, порядок заполнения и форматы

Форма расчета 6-НДФЛ, порядок заполнения и форматы Top-10 мировых криптобирж за 6 месяцев 2019 года

Top-10 мировых криптобирж за 6 месяцев 2019 года Прибыль организации. Тема 5

Прибыль организации. Тема 5 Javne finansije. Lekcija 10

Javne finansije. Lekcija 10 Банковские и страховые продукты

Банковские и страховые продукты Определение ожидаемой доходности бизнеса (ставки дисконтирования)

Определение ожидаемой доходности бизнеса (ставки дисконтирования) Социальная защита и социальное страхование

Социальная защита и социальное страхование Цели и задачи управления государственным долгом

Цели и задачи управления государственным долгом Зарплатный проект. Альфа-Банк сегодня

Зарплатный проект. Альфа-Банк сегодня Бюджет для граждан к отчету об исполнении Юрьевецкого бюджета района за 2018 год

Бюджет для граждан к отчету об исполнении Юрьевецкого бюджета района за 2018 год Финансовые рынки

Финансовые рынки Sequence of accounts & aggregates: practice part

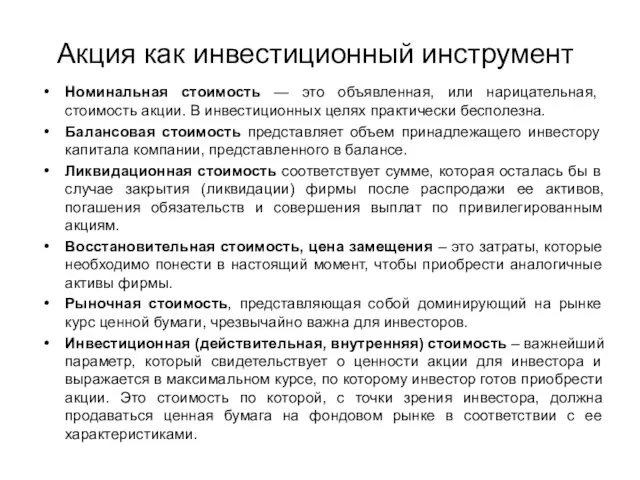

Sequence of accounts & aggregates: practice part Акция как инвестиционный инструмент

Акция как инвестиционный инструмент Основы бюджетных отношений

Основы бюджетных отношений Сервисы

Сервисы Тема 3. Общегосударственный финансовый контроль. Тема 3.2. Органы осуществляющие общегосударственный контроль и их сфера надзора

Тема 3. Общегосударственный финансовый контроль. Тема 3.2. Органы осуществляющие общегосударственный контроль и их сфера надзора Исследовательская работа: Выгодно ли жить на съемной квартире или лучше взять в её ипотеку?

Исследовательская работа: Выгодно ли жить на съемной квартире или лучше взять в её ипотеку? Облигации, их виды и особенности

Облигации, их виды и особенности Государственные меры социальной поддержки населения в период распространения короновирусной инфекции (2019-nCoV)

Государственные меры социальной поддержки населения в период распространения короновирусной инфекции (2019-nCoV) Финансовые рынки

Финансовые рынки