- The Financial Sector

Содержание

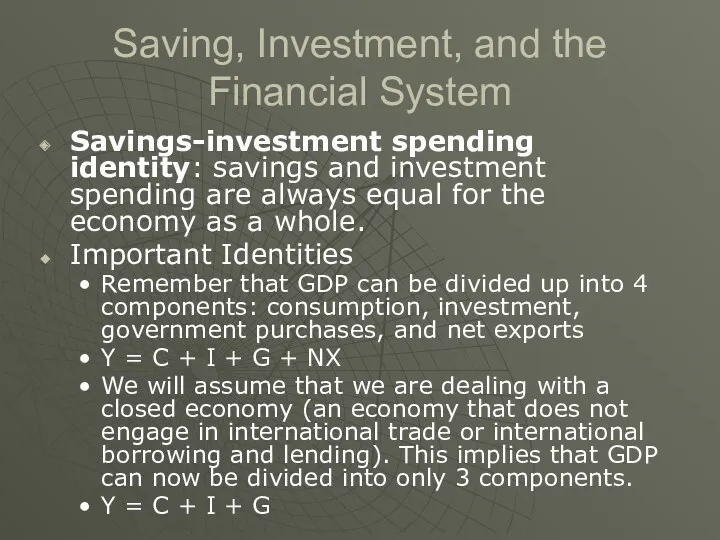

- 2. Saving, Investment, and the Financial System Savings-investment spending identity: savings and investment spending are always equal

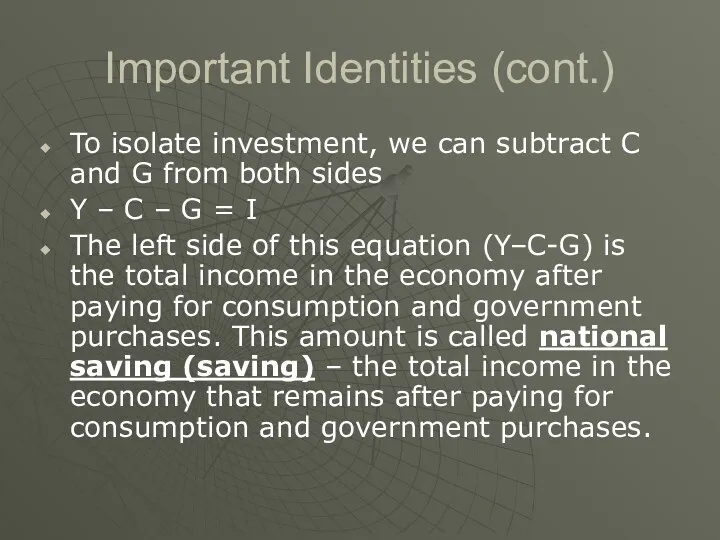

- 3. Important Identities (cont.) To isolate investment, we can subtract C and G from both sides Y

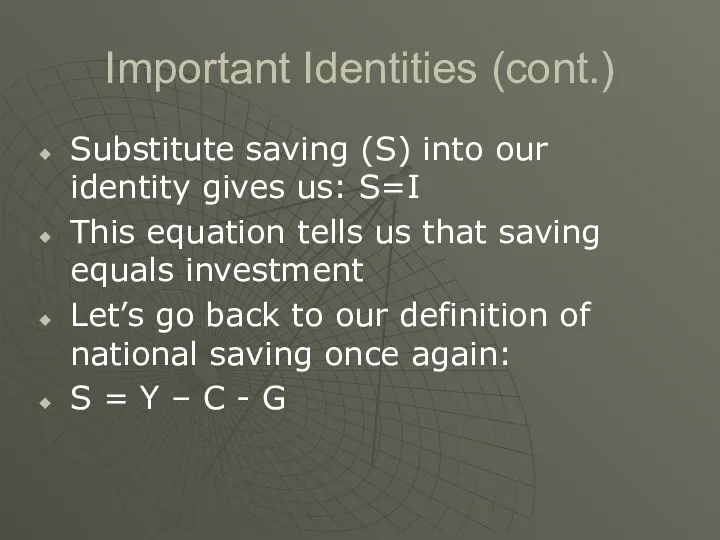

- 4. Important Identities (cont.) Substitute saving (S) into our identity gives us: S=I This equation tells us

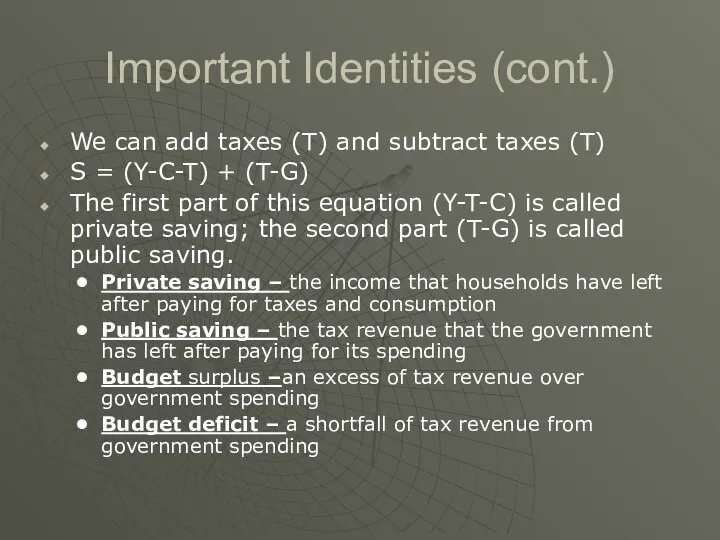

- 5. Important Identities (cont.) We can add taxes (T) and subtract taxes (T) S = (Y-C-T) +

- 6. Important Identities (cont.) The fact that S=I means that for the economy as a whole saving

- 7. Open Economy: Savings and Investments Savings of people in one country can be used to finance

- 8. The Meaning of Saving and Investment In macroeconomics, investment refers to the purchase of new capital,

- 9. The Meaning of Saving and Investment Private saving is the income remaining after households pay their

- 10. Saving and Investment Investment is the purchase of new capital. Examples of investment: General Motors spends

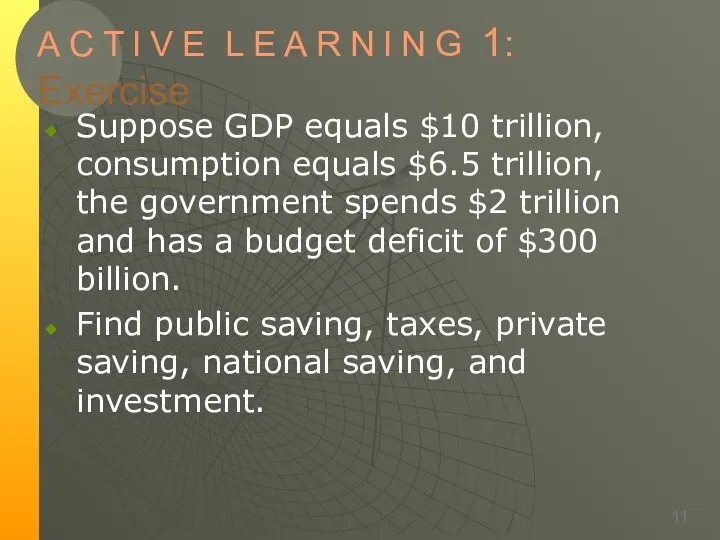

- 11. A C T I V E L E A R N I N G 1: Exercise

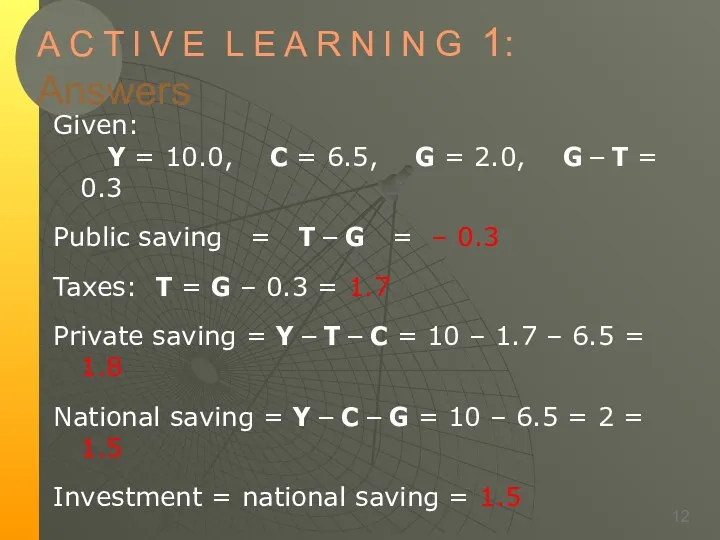

- 12. A C T I V E L E A R N I N G 1: Answers

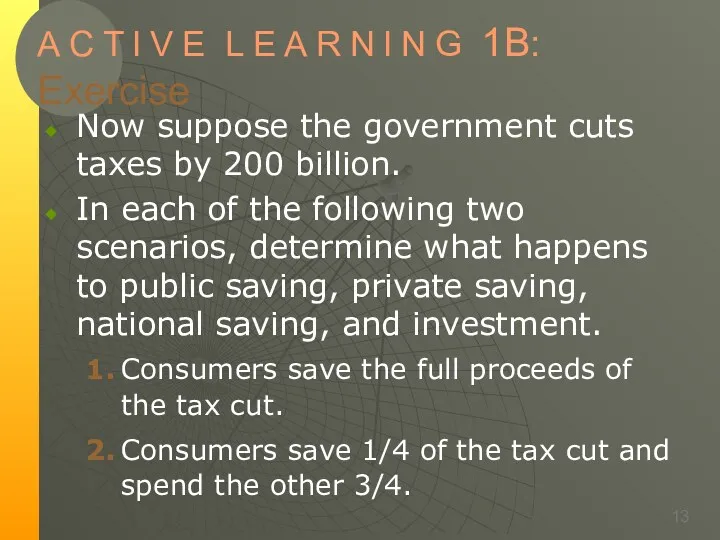

- 13. A C T I V E L E A R N I N G 1B: Exercise

- 14. A C T I V E L E A R N I N G 1B: Answers

- 15. A C T I V E L E A R N I N G 1C: Discussion

- 16. Financial System Financial System – the group of institutions in the economy that help to match

- 17. Three Tasks of a Financial System 3 Problems facing borrowers and lenders: transactions costs, risk, and

- 18. Three Tasks of a Financial System 2) Reducing Risk Financial risk – uncertainty about future outcomes

- 19. Risk Aversion Most people are risk averse – they dislike uncertainty. Example: You are offered the

- 20. The Utility Function Utility is a subjective measure of well-being that depends on wealth. As wealth

- 21. The Utility Function and Risk Aversion Because of diminishing marginal utility, a $1000 loss reduces utility

- 22. Three Tasks of a Financial System 3) Providing Liquidity Liquid asset is an asset that can

- 23. Degrees of Liquidity

- 24. Liquidity Liquidity – the ease with which an asset can be converted into the economy’s medium

- 25. Financial markets The Bond Market Bond – a certificate of indebtedness A bond identifies the date

- 26. Characteristics of a Bond One characteristic that determines a bond’s value is its term. The term

- 27. Financial Markets Stock Market Stock – a claim to partial ownership in a firm The sale

- 28. Financial Assets Stock Bond Loan – a lending agreement between an individual lender and an individual

- 29. Financial Intermediaries Banks The primary role of banks is to take in deposits from people who

- 30. Financial Intermediaries Mutual funds – an institution that sells shares to the public and uses the

- 31. Financial Intermediaries Pension fund: a type of mutual fund that holds assets in order to provide

- 32. Definition and Measurement of Money Money: the set of assets in an economy that people regularly

- 33. Types of Money

- 34. The Functions of Money Medium of exchange – an item that buyers give to sellers when

- 35. Kinds of Money Commodity money: takes the form of a commodity with intrinsic value Examples: gold

- 36. Money is the U.S. Economy The quantity of money circulating in the United States is sometimes

- 37. Credit Cards, Debit Cards, and Money Credit cards are not a form of money; when a

- 38. Measures of the U.S. Money Supply M1: currency, demand deposits, traveler’s checks, and other checkable deposits.

- 39. Composition of the U.S. M1 and M2 Money Supply, 2011

- 40. Financial markets coordinate saving and investment Financial decisions involve two elements – time and risk. For

- 41. Present Value: Measuring the Time Value of Money The present value of any future value is

- 42. Present Value: Measuring the Time Value of Money r = the interest rate expressed in decimal

- 43. EXAMPLE 1: A simple deposit Deposit $100 in the bank at 5% interest. What is the

- 44. EXAMPLE 1: A Simple Deposit Deposit $100 in the bank at 5% interest. What is the

- 45. EXAMPLE 2: Investment Decision Suppose r = 0.06. Should General Motors spend $100 million to build

- 46. EXAMPLE 2: Investment Decision Instead, suppose r = 0.09. Should General Motors spend $100 million to

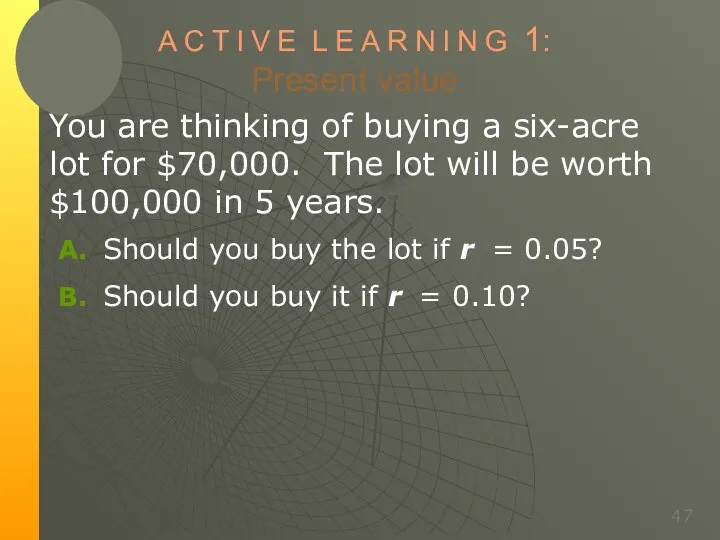

- 47. A C T I V E L E A R N I N G 1: Present

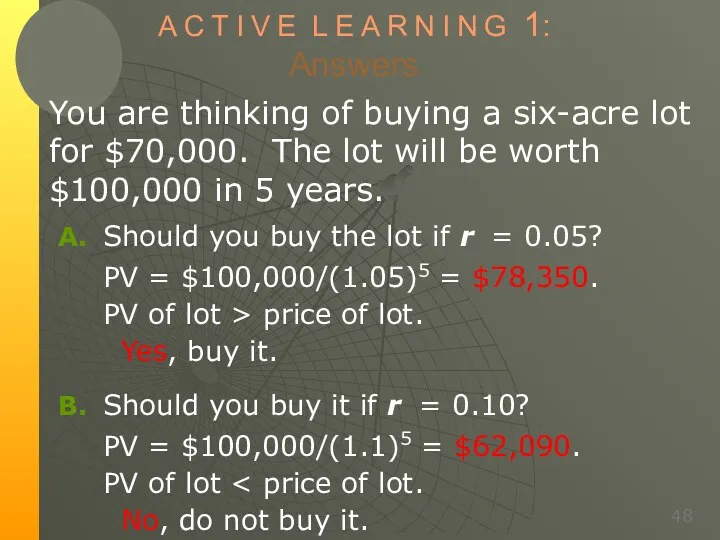

- 48. A C T I V E L E A R N I N G 1: Answers

- 49. Compounding Compounding: the accumulation of a sum of money where the interest earned on the sum

- 50. The Rule of 70 The Rule of 70: If a variable grows at a rate of

- 51. Banks and the Money Supply The simple case of 100 percent reserve banking A bank is

- 52. Banks and the Money Supply The money supply in this economy is unchanged by the creation

- 53. Money Creation with Fractional-Reserve Banking Fractional-reserve banking – a banking system in which banks hold only

- 54. Money Creation with Fractional-Reserve Banking When the bank makes these loans, the money supply changes. Before

- 55. The Money Multiplier The creation of money does not stop at this point. Borrowers usually borrow

- 56. The Money Multiplier Each time the money is deposited and a bank loan is created, more

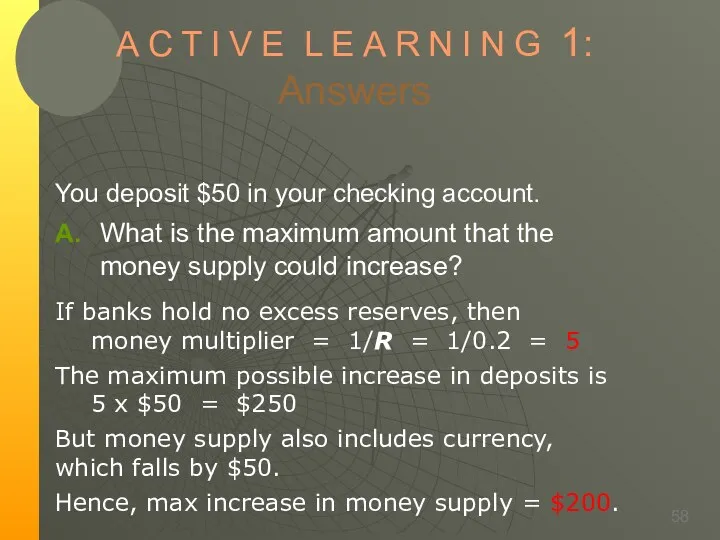

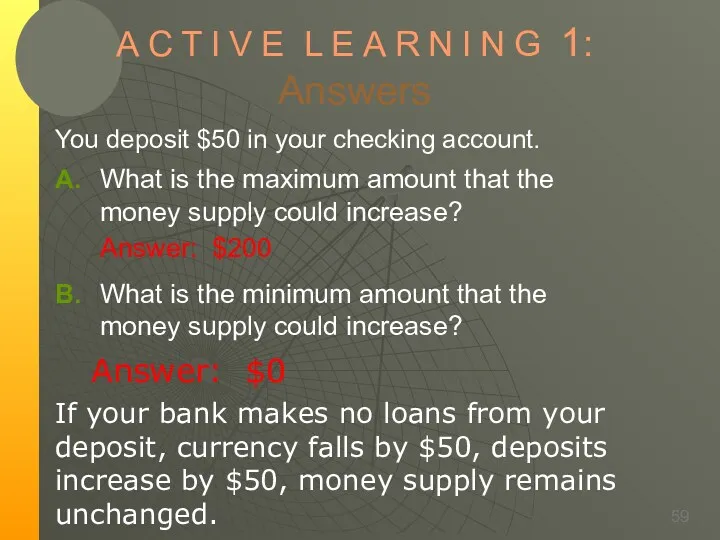

- 57. A C T I V E L E A R N I N G 1: Exercise

- 58. A C T I V E L E A R N I N G 1: Answers

- 59. A C T I V E L E A R N I N G 1: Answers

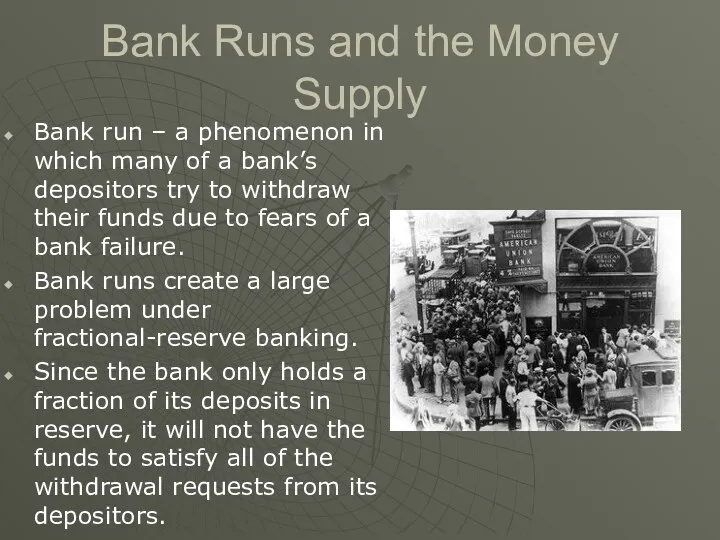

- 60. Bank Runs and the Money Supply Bank run – a phenomenon in which many of a

- 61. Bank Regulation Today depositors are guaranteed through the Federal Depository Insurance Corporation (FDIC). Deposit Insurance –

- 62. Bank Regulation Capital Requirement: regulators require that the owners of banks hold substantially more assets than

- 63. The Federal Reserve System Federal Reserve (Fed) – the central bank of the United States Central

- 64. The Fed’s Organization Not part of the U.S. government, but not a private institution either. Strange

- 65. The Federal Reserve System

- 66. The Federal Open Market Committee The Federal Open Market Committee (FOMC) consists of the 7 members

- 67. The Federal Open Market Committee The primary way in which the Fed increases or decreases the

- 68. Open-Market Operations

- 69. Glass-Steagall Act of 1933 Glass-Steagall Act of 1933 – separated banks into two catergories commercial banks

- 70. Savings and Loan Crisis of the 1980s Savings and loan (thrift) – type of deposit-taking bank,

- 71. Financial Crisis of 2008 Declining asset prices from 2000 to 2002 and the economy going into

- 72. Financial Crisis of 2008 Subprime lending explodes by loan originators, which then sell these loans as

- 73. Financial Crisis of 2008 Housing prices start to fall in 2006 The people with subprime mortgages

- 74. Financial Crisis of 2008 Vicious cycle of deleveraging – takes place when asset sales to cover

- 75. Functions of the Fed One function performed by the Fed is the regulation of banks to

- 76. Functions of the Fed The second function of the Fed is to control the quantity of

- 77. The Federal Reserve System: The U.S. Central Bank (cont’d) Functions of the Fed Supplies the economy

- 78. The Way Fed Policy is Currently Implemented At present the Fed announces an interest rate target

- 79. The Way Fed Policy is Currently Implemented Conversely, if the Fed wants to decrease “the” rate

- 80. The Way Fed Policy is Currently Implemented In reality, “the” interest rates that are relevant to

- 81. The Way Fed Policy is Currently Implemented Federal Funds Rate The interest rate that depository institutions

- 82. The Way Fed Policy is Currently Implemented Discount Rate The interest rate that the Federal Reserve

- 83. The Way Fed Policy is Currently Implemented The interest rate on reserves In October 2008, Congress

- 84. The Market for Bank Reserves and the Federal Funds Rate, Panel (a)

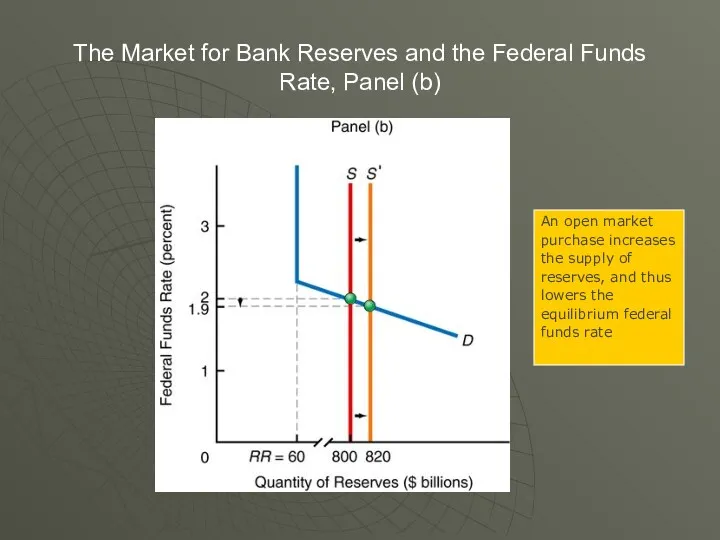

- 85. The Market for Bank Reserves and the Federal Funds Rate, Panel (b) An open market purchase

- 86. Theory of Liquidity Preference Theory of liquidity preference – Keynes’s theory that the interest rate adjusts

- 87. Money Demand Money demand curve – shows the relationship between the quantity of money demanded and

- 88. Three Main Motives behind the Demand for Money Transactions Motive Speculative Motive Precautionary Motive

- 89. Transactions Motive Money demand can be transactions demand for money, money needed for transactions Depend on

- 90. Speculative Motive People choose to hold cash because they want to be prepared for cash-based investment

- 91. Precautionary Motive Describes people’s inclination to hold onto money for unexpected cash expenses, such as medical

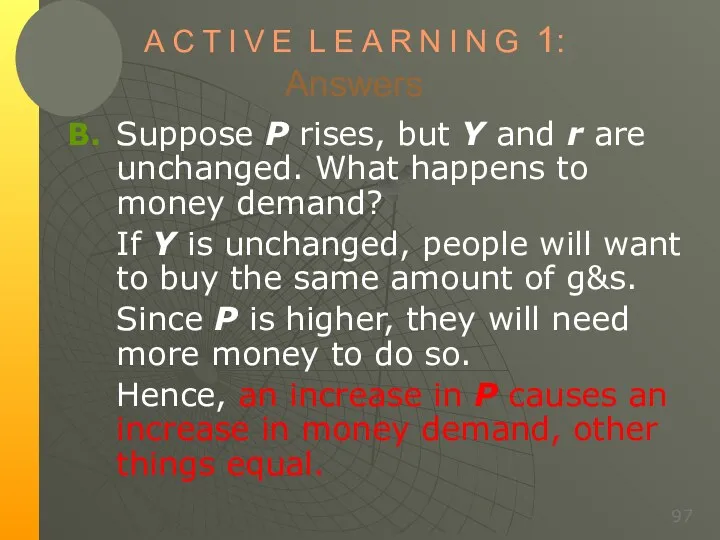

- 92. Money Demand Suppose real income (Y) rises. Other things equal, what happens to money demand? If

- 93. The Downward Slope of the Aggregate-Demand Curve When the price level increases, the quantity of money

- 94. Shifts of the Money Demand Curve Changes in the Aggregate Price Level Price level rises, MD

- 95. A C T I V E L E A R N I N G 1: The

- 96. A C T I V E L E A R N I N G 1: Answers

- 97. A C T I V E L E A R N I N G 1: Answers

- 98. Money Supply The money supply in the economy is controlled by the Federal Reserve. The Fed

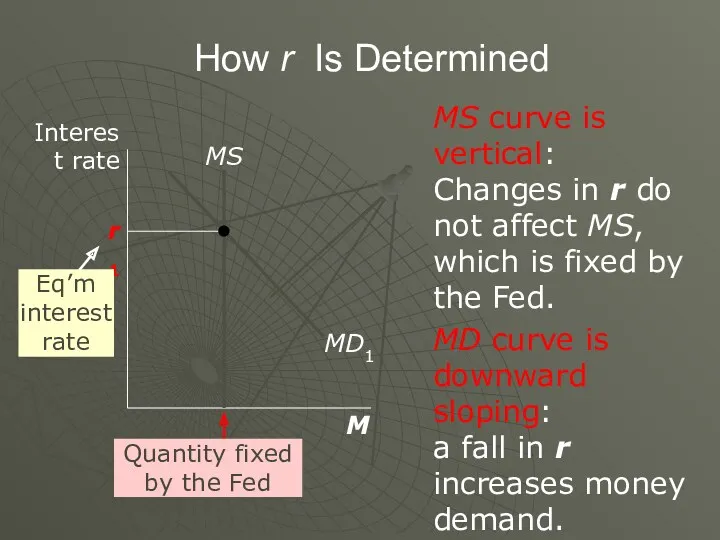

- 99. How r Is Determined MS curve is vertical: Changes in r do not affect MS, which

- 100. Equilibrium in the Money Market The interest rate adjusts to bring money demand and money supply

- 101. How the Interest-Rate Effect Works P2 A fall in P reduces money demand, which lowers r.

- 102. Monetary Policy and Aggregate Demand To achieve macroeconomic goals, the Fed can use monetary policy to

- 103. Changes in the Money Supply Example: The Fed buys government bonds in open-market operations. This will

- 104. The Role of Interest-Rate Targets in Fed Policy In recent years, the Fed has conducted policy

- 105. The Effects of Reducing the Money Supply The Fed can raise r by reducing the money

- 106. A C T I V E L E A R N I N G 2: Exercise

- 107. A C T I V E L E A R N I N G 2: Answers

- 108. A C T I V E L E A R N I N G 2: Answers

- 109. A C T I V E L E A R N I N G 2: Answers

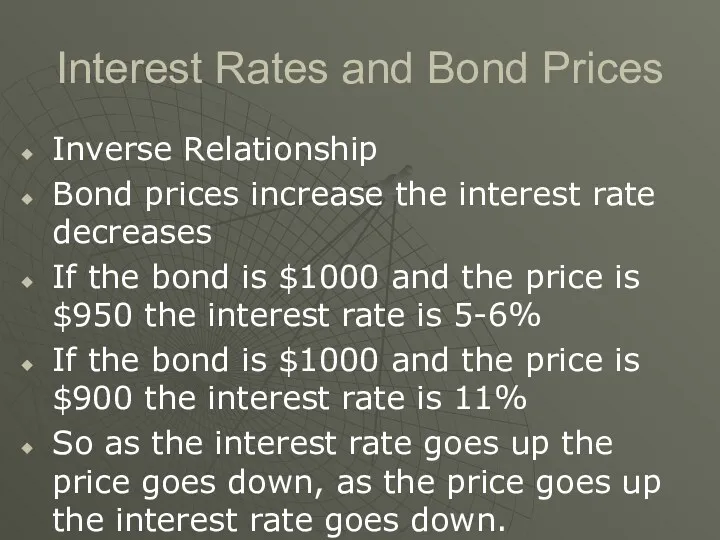

- 110. Interest Rates and Bond Prices Inverse Relationship Bond prices increase the interest rate decreases If the

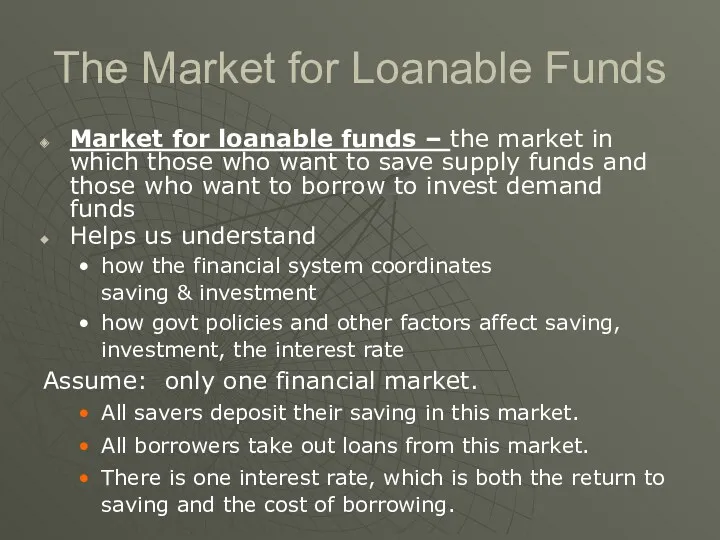

- 111. The Market for Loanable Funds Market for loanable funds – the market in which those who

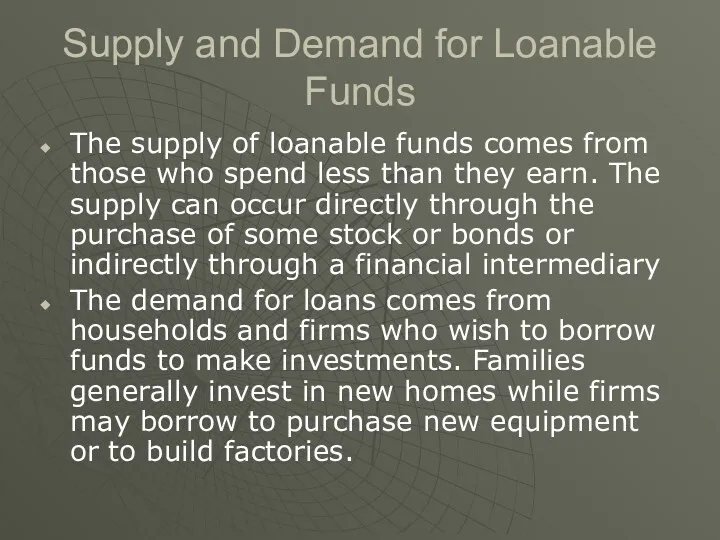

- 112. Supply and Demand for Loanable Funds The supply of loanable funds comes from those who spend

- 113. The Slope of the Supply Curve An increase in the interest rate makes saving more attractive,

- 114. The Slope of the Demand Curve A fall in the interest rate reduces the cost of

- 115. Supply and Demand for Loanable Funds The price of a loan is the interest rate All

- 116. Supply and Demand for Loanable Funds At the equilibrium, the quantity of funds demanded is equal

- 117. Equilibrium The interest rate adjusts to equate supply and demand. The eq’m quantity of L.F. equals

- 118. Shifts of the Demand for Loanable Funds Changes in Perceived Business Opportunities If business believes they

- 119. The Crowding-Out Effect The crowding out effect works in the opposite direction. Crowding out effect –

- 120. The Crowding-Out Effect The higher interest rate raises the cost of borrowing and the return to

- 121. Shifts of the Supply of Loanable Funds Changes in private savings behavior Save less supply shifts

- 122. Policy 1: Saving Incentives Savings rates in the United States are relatively low when compared with

- 123. Policy 1: Saving Incentives Interest Rate Loanable Funds ($billions) D1 Tax incentives for saving increase the

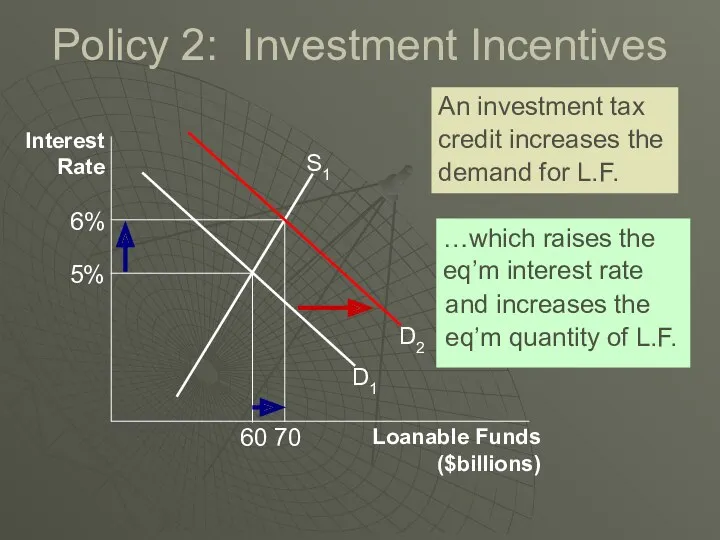

- 124. Policy 2: Investment Incentive Suppose instead that the government passed a new law lowering taxes for

- 125. Policy 2: Investment Incentives Interest Rate Loanable Funds ($billions) D1 An investment tax credit increases the

- 126. A C T I V E L E A R N I N G 2: Exercise

- 127. A C T I V E L E A R N I N G 2: Answers

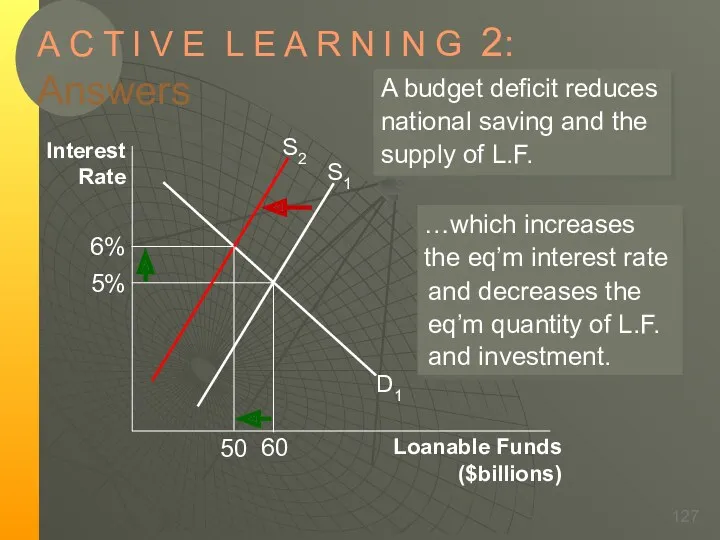

- 128. Policy 3: Government Budget Deficits and Surpluses A budget deficit occurs if the government spends more

- 129. Policy 3: Govt Budget Deficits Interest Rate Loanable Funds ($billions) D1 A budget deficit reduces national

- 130. Policy 3: Government Budget Deficits and Surpluses When the interest rate rises, the quantity of funds

- 131. The U.S. Government Debt The government finances deficits by borrowing (selling government bonds). Persistent deficits lead

- 132. The Fisher Effect Real interest rate is equal to the nominal interest rate minus inflation rate.

- 133. The Fisher Effect Fisher Effect – the one-for-one adjustment of the nominal interest rate to the

- 134. Interest Rates in the Long Run and the Short Run It may appear we have two

- 135. Interest Rates in the Long Run and the Short Run In the long run, the economy’s

- 136. Reconciling the Two Interest Rate Models: The Interest Rate in the Short Run

- 138. Скачать презентацию

Saving, Investment, and the Financial System

Savings-investment spending identity: savings and investment

Saving, Investment, and the Financial System

Savings-investment spending identity: savings and investment

Important Identities (cont.)

To isolate investment, we can subtract C and G

Important Identities (cont.)

To isolate investment, we can subtract C and G

Important Identities (cont.)

Substitute saving (S) into our identity gives us: S=I

This

Important Identities (cont.)

Substitute saving (S) into our identity gives us: S=I

This

Important Identities (cont.)

We can add taxes (T) and subtract taxes (T)

S

Important Identities (cont.)

We can add taxes (T) and subtract taxes (T)

S

Important Identities (cont.)

The fact that S=I means that for the economy

Important Identities (cont.)

The fact that S=I means that for the economy

Open Economy: Savings and Investments

Savings of people in one country can

Open Economy: Savings and Investments

Savings of people in one country can

The Meaning of Saving and Investment

In macroeconomics, investment refers to the

The Meaning of Saving and Investment

In macroeconomics, investment refers to the

The Meaning of Saving and Investment

Private saving is the income remaining

The Meaning of Saving and Investment

Private saving is the income remaining

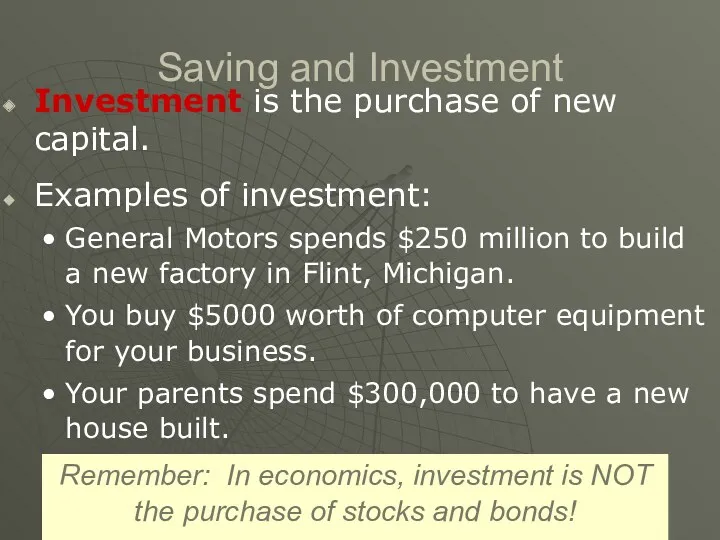

Saving and Investment

Investment is the purchase of new capital.

Examples of

Saving and Investment

Investment is the purchase of new capital.

Examples of

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

Financial System

Financial System – the group of institutions in the economy

Financial System

Financial System – the group of institutions in the economy

Three Tasks of a Financial System

3 Problems facing borrowers and lenders:

Three Tasks of a Financial System

3 Problems facing borrowers and lenders:

Three Tasks of a Financial System

2) Reducing Risk

Financial risk – uncertainty

Three Tasks of a Financial System

2) Reducing Risk

Financial risk – uncertainty

Risk Aversion

Most people are risk averse – they dislike uncertainty.

Example:

Risk Aversion

Most people are risk averse – they dislike uncertainty.

Example:

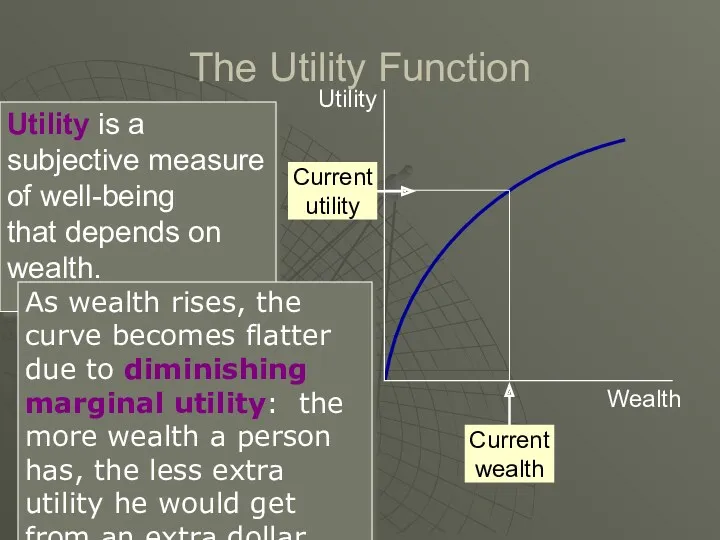

The Utility Function

Utility is a subjective measure of well-being

that depends

The Utility Function

Utility is a subjective measure of well-being that depends

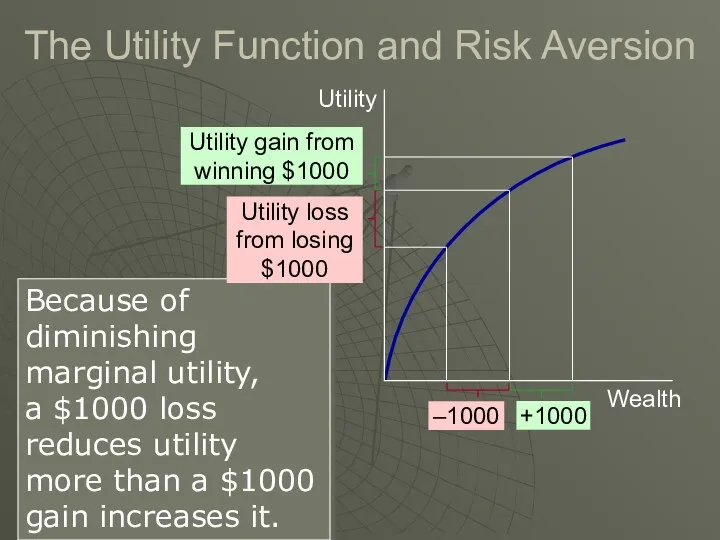

The Utility Function and Risk Aversion

Because of diminishing marginal utility,

a

The Utility Function and Risk Aversion

Because of diminishing marginal utility, a

Three Tasks of a Financial System

3) Providing Liquidity

Liquid asset is an

Three Tasks of a Financial System

3) Providing Liquidity

Liquid asset is an

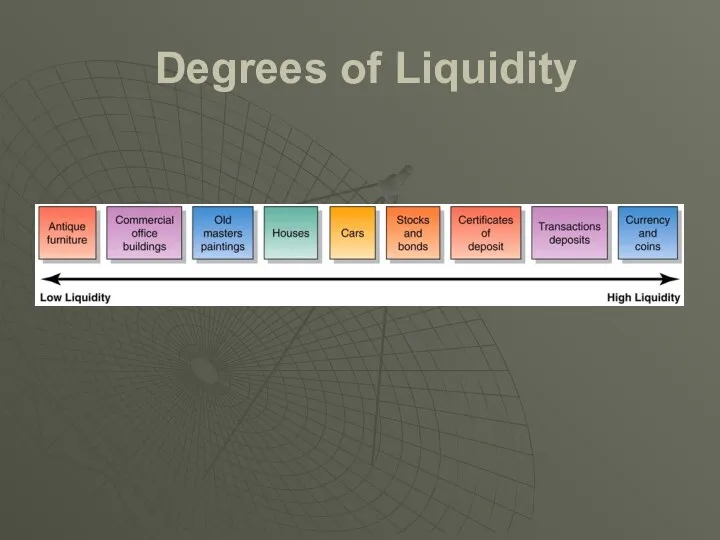

Degrees of Liquidity

Degrees of Liquidity

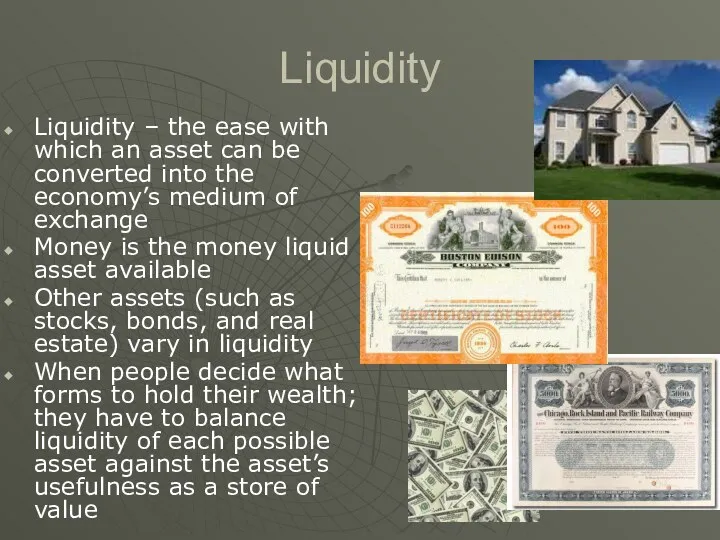

Liquidity

Liquidity – the ease with which an asset can be converted

Liquidity

Liquidity – the ease with which an asset can be converted

Financial markets

The Bond Market

Bond – a certificate of indebtedness

A bond identifies

Financial markets

The Bond Market

Bond – a certificate of indebtedness

A bond identifies

Characteristics of a Bond

One characteristic that determines a bond’s value is

Characteristics of a Bond

One characteristic that determines a bond’s value is

Financial Markets

Stock Market

Stock – a claim to partial ownership in a

Financial Markets

Stock Market

Stock – a claim to partial ownership in a

Financial Assets

Stock

Bond

Loan – a lending agreement between an individual lender and

Financial Assets

Stock

Bond

Loan – a lending agreement between an individual lender and

Financial Intermediaries

Banks

The primary role of banks is to take in deposits

Financial Intermediaries

Banks

The primary role of banks is to take in deposits

Financial Intermediaries

Mutual funds – an institution that sells shares to the

Financial Intermediaries

Mutual funds – an institution that sells shares to the

Financial Intermediaries

Pension fund: a type of mutual fund that holds assets

Financial Intermediaries

Pension fund: a type of mutual fund that holds assets

Definition and Measurement of Money

Money: the set of assets in an

Definition and Measurement of Money

Money: the set of assets in an

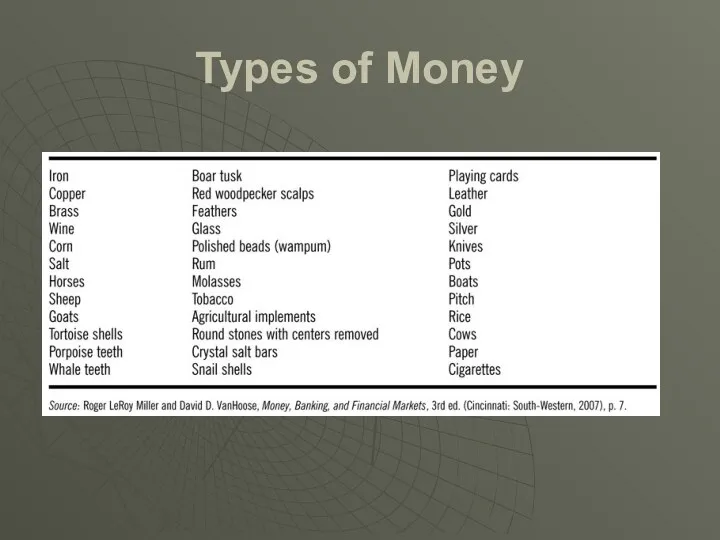

Types of Money

Types of Money

The Functions of Money

Medium of exchange – an item that buyers

The Functions of Money

Medium of exchange – an item that buyers

Kinds of Money

Commodity money:

takes the form of a commodity with

Kinds of Money

Commodity money: takes the form of a commodity with

Money is the U.S. Economy

The quantity of money circulating in the

Money is the U.S. Economy

The quantity of money circulating in the

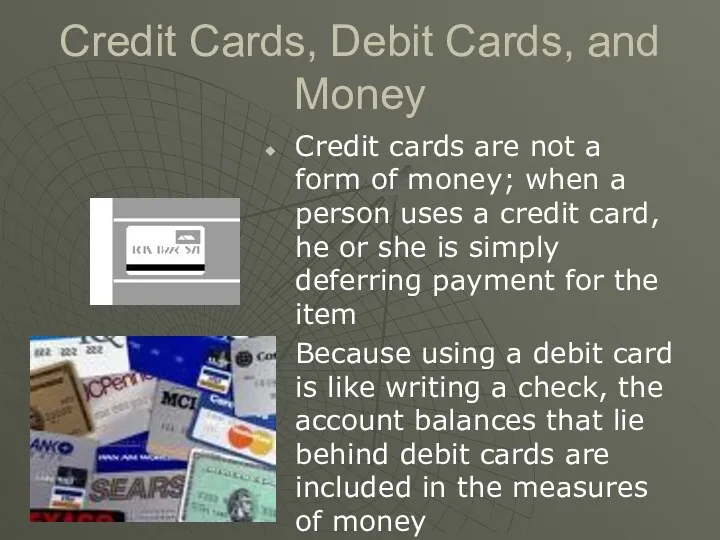

Credit Cards, Debit Cards, and Money

Credit cards are not a form

Credit Cards, Debit Cards, and Money

Credit cards are not a form

Measures of the U.S. Money Supply

M1: currency, demand deposits,

traveler’s checks,

Measures of the U.S. Money Supply

M1: currency, demand deposits, traveler’s checks,

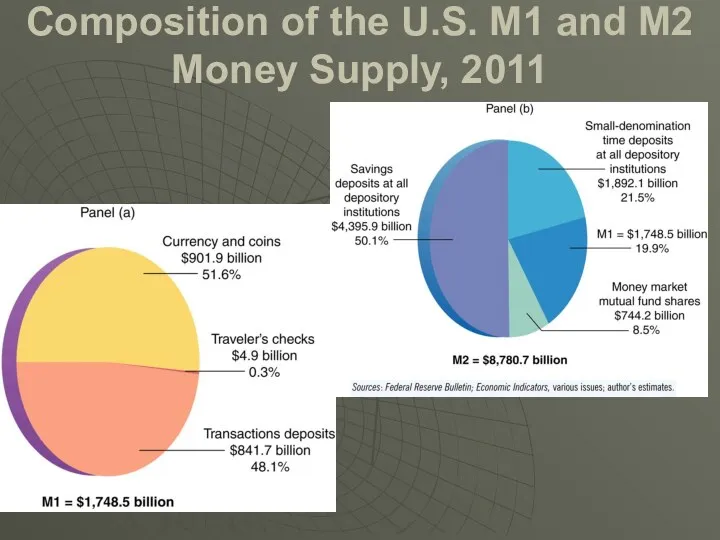

Composition of the U.S. M1 and M2 Money Supply, 2011

Composition of the U.S. M1 and M2 Money Supply, 2011

Financial markets coordinate saving and investment

Financial decisions involve two elements –

Financial markets coordinate saving and investment

Financial decisions involve two elements –

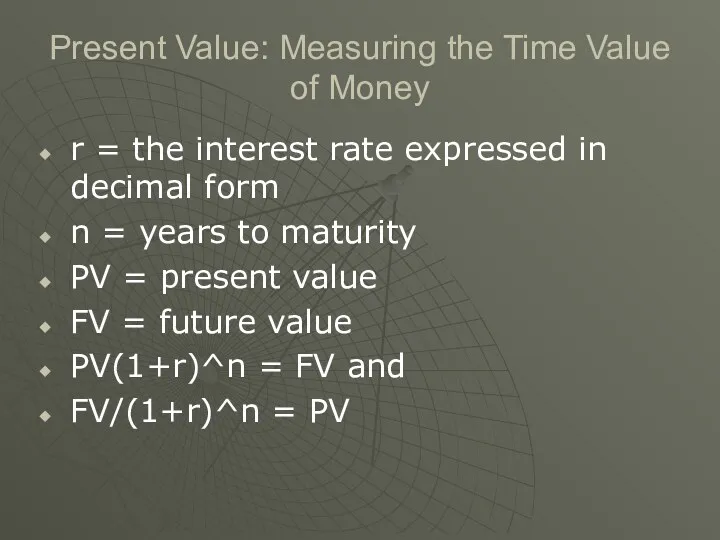

Present Value: Measuring the Time Value of Money

The present value of

Present Value: Measuring the Time Value of Money

The present value of

Present Value: Measuring the Time Value of Money

r = the interest

Present Value: Measuring the Time Value of Money

r = the interest

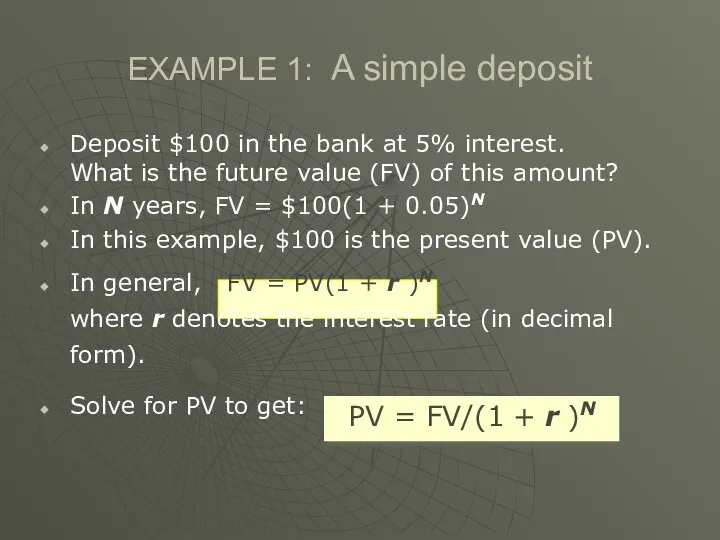

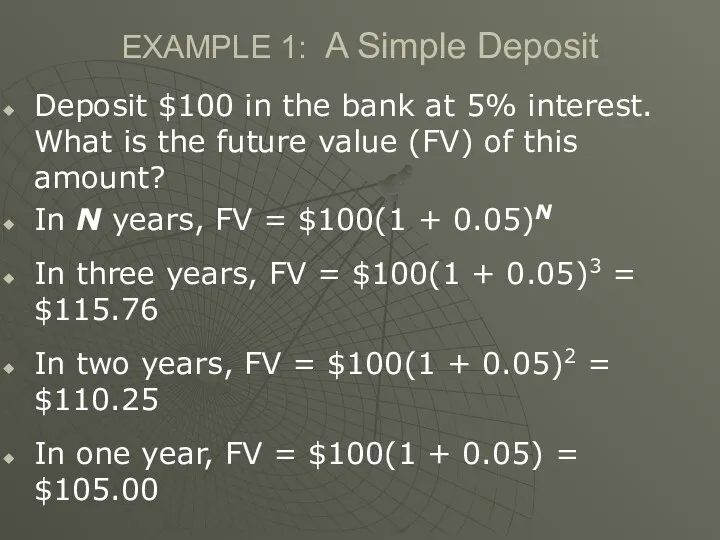

EXAMPLE 1: A simple deposit

Deposit $100 in the bank at 5%

EXAMPLE 1: A simple deposit

Deposit $100 in the bank at 5%

EXAMPLE 1: A Simple Deposit

Deposit $100 in the bank at 5%

EXAMPLE 1: A Simple Deposit

Deposit $100 in the bank at 5%

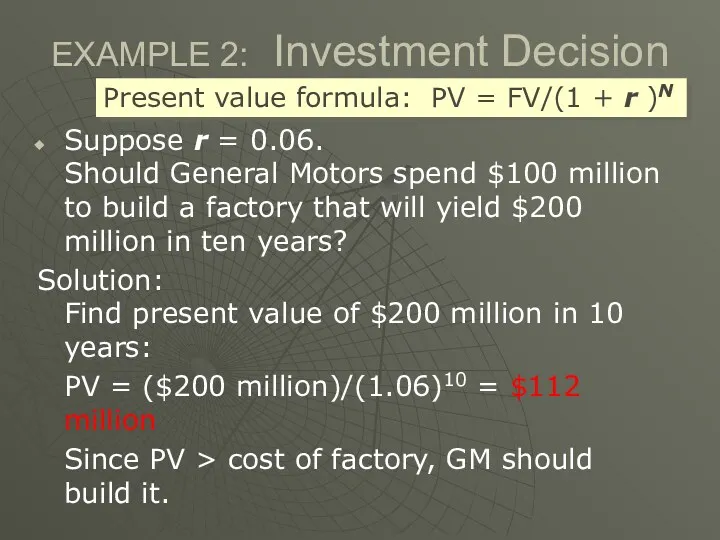

EXAMPLE 2: Investment Decision

Suppose r = 0.06.

Should General Motors spend

EXAMPLE 2: Investment Decision

Suppose r = 0.06. Should General Motors spend

EXAMPLE 2: Investment Decision

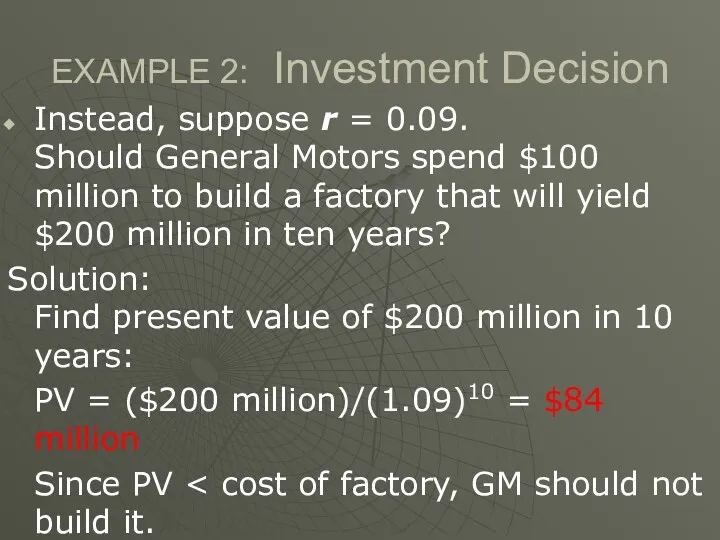

Instead, suppose r = 0.09.

Should General Motors

EXAMPLE 2: Investment Decision

Instead, suppose r = 0.09. Should General Motors

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

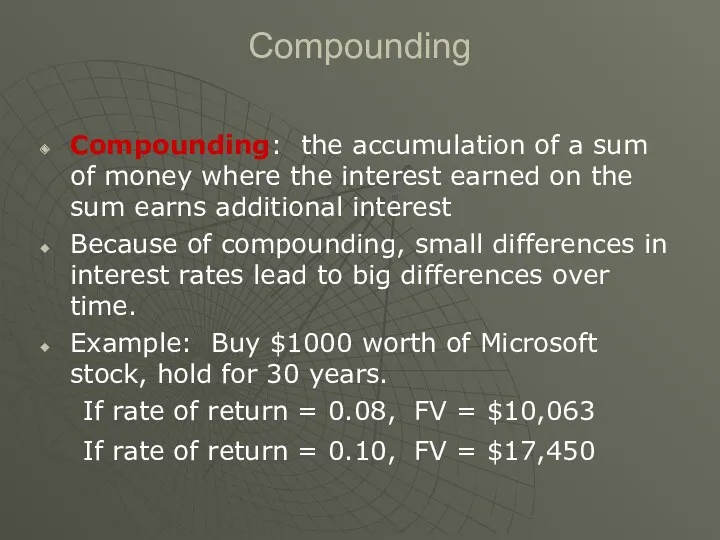

Compounding

Compounding: the accumulation of a sum of money where the interest

Compounding

Compounding: the accumulation of a sum of money where the interest

The Rule of 70

The Rule of 70:

If a variable grows

The Rule of 70

The Rule of 70: If a variable grows

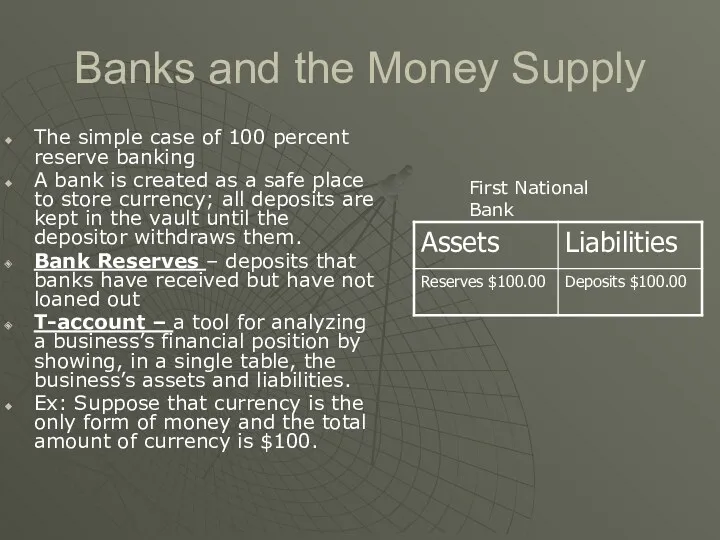

Banks and the Money Supply

The simple case of 100 percent reserve

Banks and the Money Supply

The simple case of 100 percent reserve

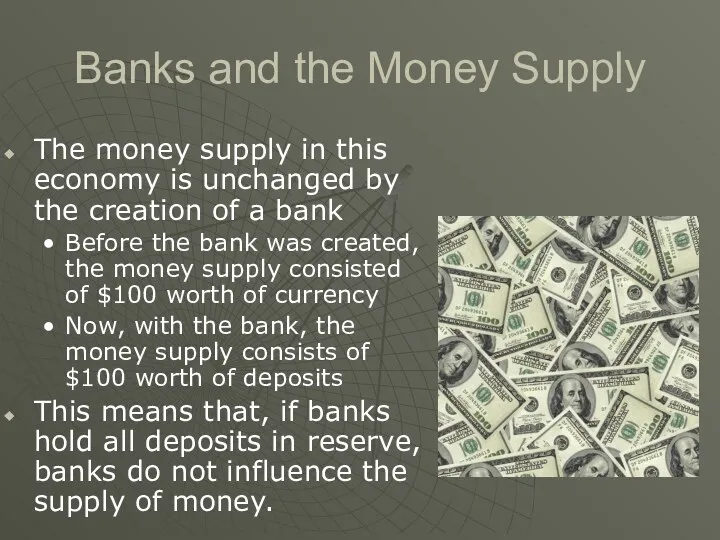

Banks and the Money Supply

The money supply in this economy is

Banks and the Money Supply

The money supply in this economy is

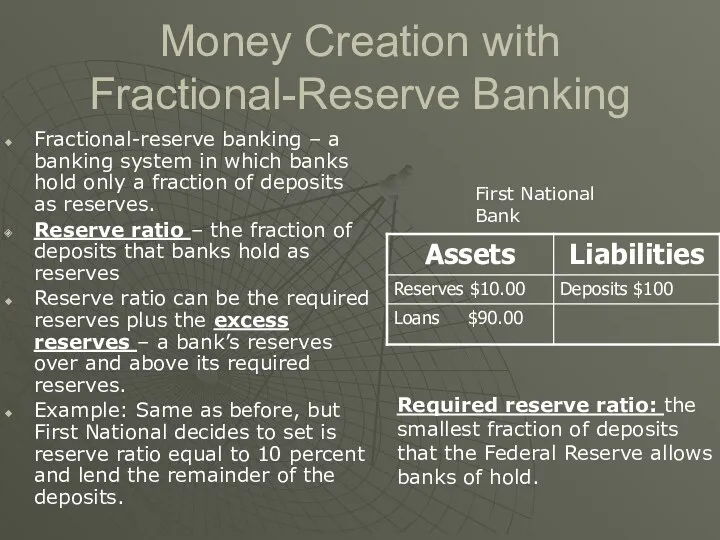

Money Creation with Fractional-Reserve Banking

Fractional-reserve banking – a banking system in

Money Creation with Fractional-Reserve Banking

Fractional-reserve banking – a banking system in

Money Creation with Fractional-Reserve Banking

When the bank makes these loans, the

Money Creation with Fractional-Reserve Banking

When the bank makes these loans, the

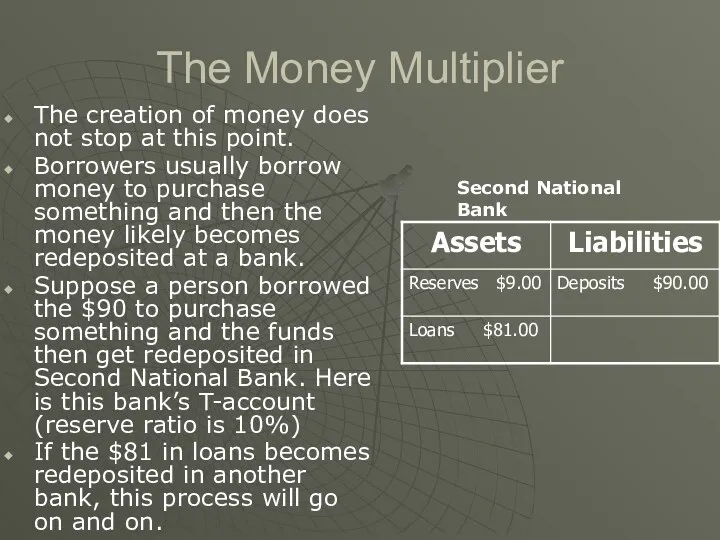

The Money Multiplier

The creation of money does not stop at this

The Money Multiplier

The creation of money does not stop at this

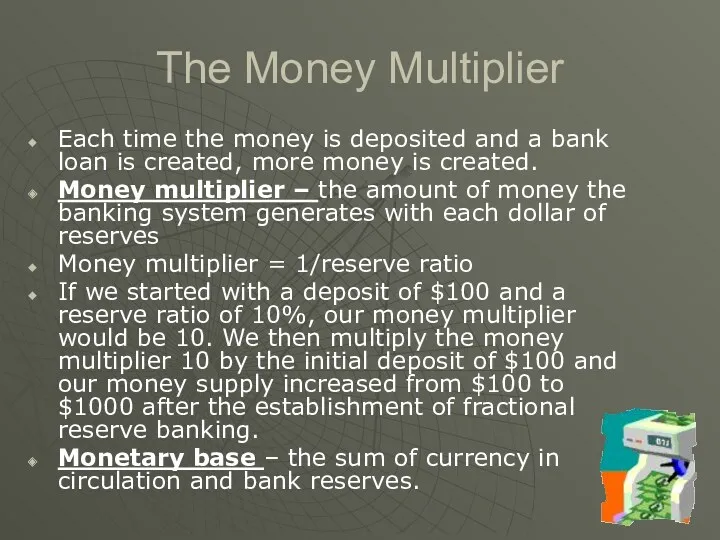

The Money Multiplier

Each time the money is deposited and a bank

The Money Multiplier

Each time the money is deposited and a bank

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

Bank Runs and the Money Supply

Bank run – a phenomenon in

Bank Runs and the Money Supply

Bank run – a phenomenon in

Bank Regulation

Today depositors are guaranteed through the Federal Depository Insurance Corporation

Bank Regulation

Today depositors are guaranteed through the Federal Depository Insurance Corporation

Bank Regulation

Capital Requirement: regulators require that the owners of banks hold

Bank Regulation

Capital Requirement: regulators require that the owners of banks hold

The Federal Reserve System

Federal Reserve (Fed) – the central bank of

The Federal Reserve System

Federal Reserve (Fed) – the central bank of

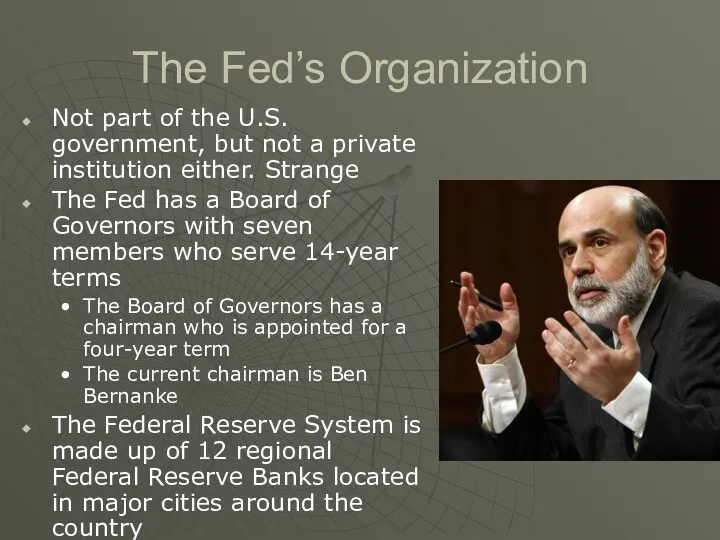

The Fed’s Organization

Not part of the U.S. government, but not a

The Fed’s Organization

Not part of the U.S. government, but not a

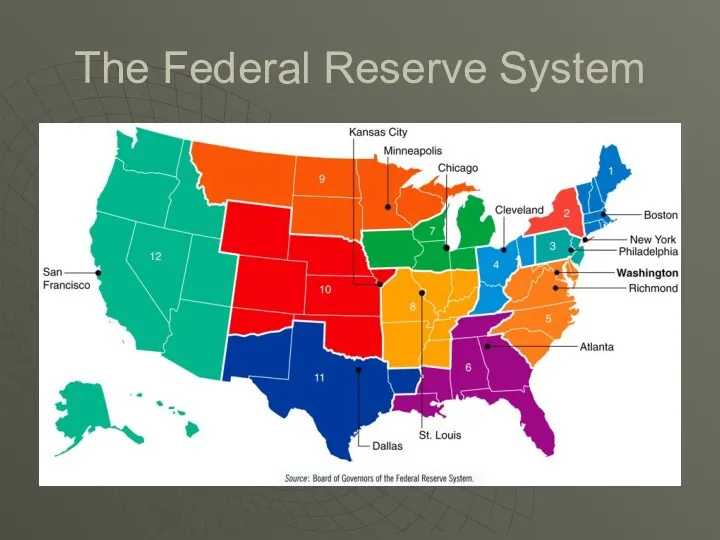

The Federal Reserve System

The Federal Reserve System

The Federal Open Market Committee

The Federal Open Market Committee (FOMC) consists

The Federal Open Market Committee

The Federal Open Market Committee (FOMC) consists

The Federal Open Market Committee

The primary way in which the Fed

The Federal Open Market Committee

The primary way in which the Fed

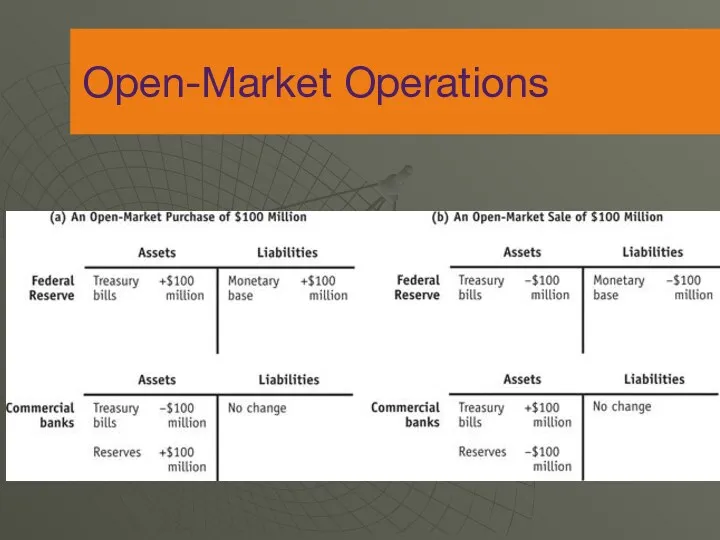

Open-Market Operations

Open-Market Operations

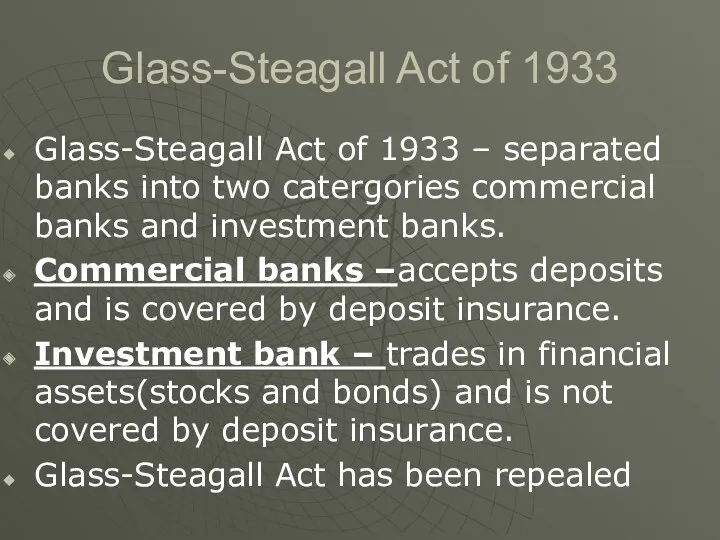

Glass-Steagall Act of 1933

Glass-Steagall Act of 1933 – separated banks into

Glass-Steagall Act of 1933

Glass-Steagall Act of 1933 – separated banks into

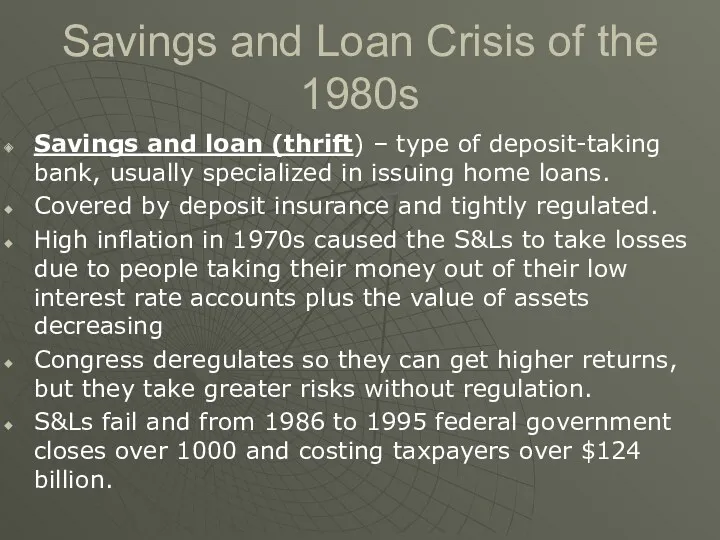

Savings and Loan Crisis of the 1980s

Savings and loan (thrift) –

Savings and Loan Crisis of the 1980s

Savings and loan (thrift) –

Financial Crisis of 2008

Declining asset prices from 2000 to 2002 and

Financial Crisis of 2008

Declining asset prices from 2000 to 2002 and

Financial Crisis of 2008

Subprime lending explodes by loan originators, which then

Financial Crisis of 2008

Subprime lending explodes by loan originators, which then

Financial Crisis of 2008

Housing prices start to fall in 2006

The people

Financial Crisis of 2008

Housing prices start to fall in 2006

The people

Financial Crisis of 2008

Vicious cycle of deleveraging – takes place when

Financial Crisis of 2008

Vicious cycle of deleveraging – takes place when

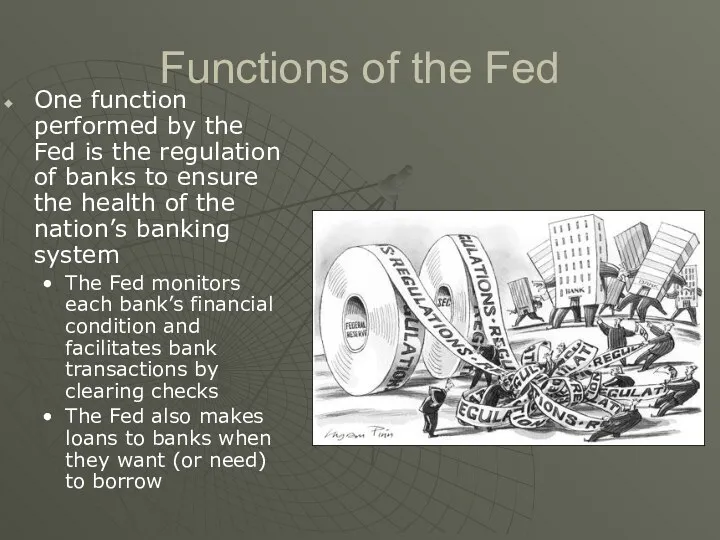

Functions of the Fed

One function performed by the Fed is the

Functions of the Fed

One function performed by the Fed is the

Functions of the Fed

The second function of the Fed is to

Functions of the Fed

The second function of the Fed is to

The Federal Reserve System: The U.S. Central Bank (cont’d)

Functions of the

The Federal Reserve System: The U.S. Central Bank (cont’d)

Functions of the

The Way Fed Policy is Currently Implemented

At present the Fed announces

The Way Fed Policy is Currently Implemented

At present the Fed announces

The Way Fed Policy is Currently Implemented

Conversely, if the Fed wants

The Way Fed Policy is Currently Implemented

Conversely, if the Fed wants

The Way Fed Policy is Currently Implemented

In reality, “the” interest rates

The Way Fed Policy is Currently Implemented

In reality, “the” interest rates

The Way Fed Policy is Currently Implemented

Federal Funds Rate

The interest

The Way Fed Policy is Currently Implemented

Federal Funds Rate

The interest

The Way Fed Policy is Currently Implemented

Discount Rate

The interest rate

The Way Fed Policy is Currently Implemented

Discount Rate

The interest rate

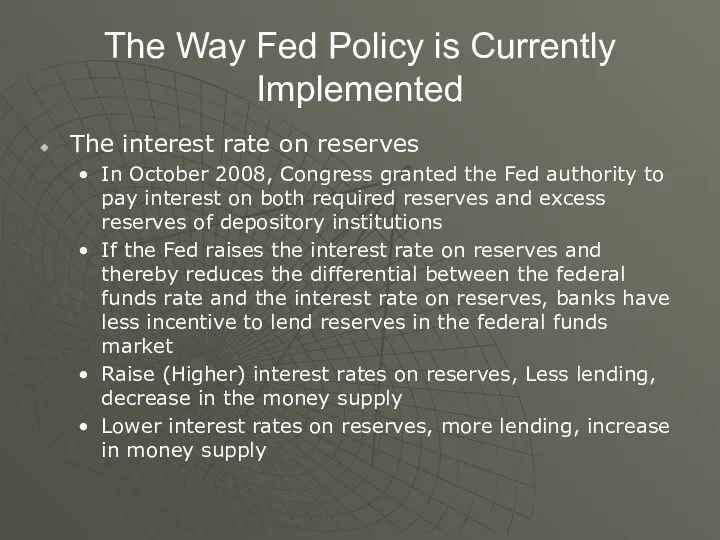

The Way Fed Policy is Currently Implemented

The interest rate on

The Way Fed Policy is Currently Implemented

The interest rate on

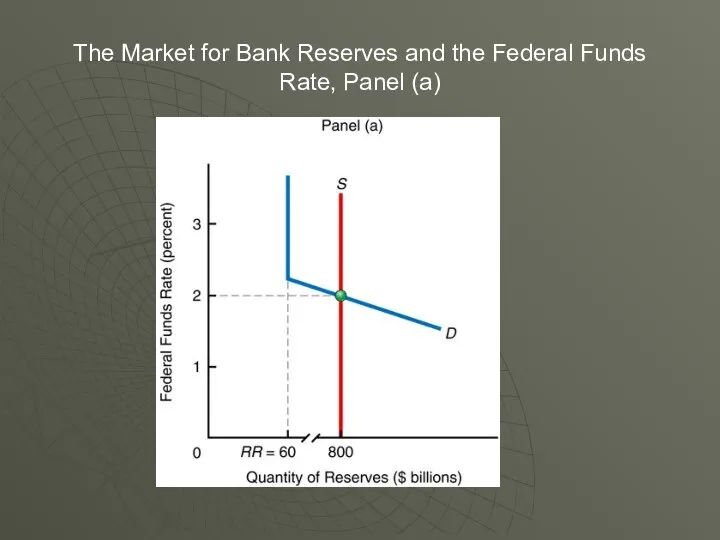

The Market for Bank Reserves and the Federal Funds Rate, Panel

The Market for Bank Reserves and the Federal Funds Rate, Panel

The Market for Bank Reserves and the Federal Funds Rate, Panel

The Market for Bank Reserves and the Federal Funds Rate, Panel

Theory of Liquidity Preference

Theory of liquidity preference – Keynes’s theory that

Theory of Liquidity Preference

Theory of liquidity preference – Keynes’s theory that

Money Demand

Money demand curve – shows the relationship between the quantity

Money Demand

Money demand curve – shows the relationship between the quantity

Three Main Motives behind the Demand for Money

Transactions Motive

Speculative Motive

Precautionary Motive

Three Main Motives behind the Demand for Money

Transactions Motive

Speculative Motive

Precautionary Motive

Transactions Motive

Money demand can be transactions demand for money, money needed

Transactions Motive

Money demand can be transactions demand for money, money needed

Speculative Motive

People choose to hold cash because they want to be

Speculative Motive

People choose to hold cash because they want to be

Precautionary Motive

Describes people’s inclination to hold onto money for unexpected cash

Precautionary Motive

Describes people’s inclination to hold onto money for unexpected cash

Money Demand

Suppose real income (Y) rises. Other things equal, what happens

Money Demand

Suppose real income (Y) rises. Other things equal, what happens

The Downward Slope of the Aggregate-Demand Curve

When the price level increases,

The Downward Slope of the Aggregate-Demand Curve

When the price level increases,

Shifts of the Money Demand Curve

Changes in the Aggregate Price Level

Price

Shifts of the Money Demand Curve

Changes in the Aggregate Price Level

Price

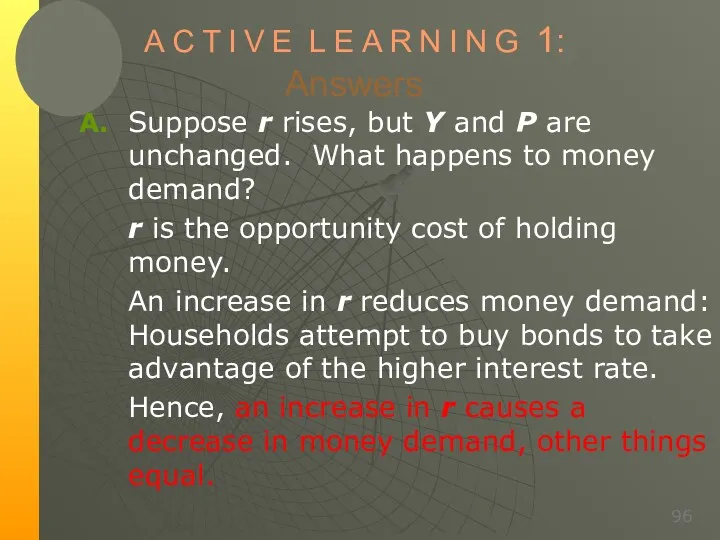

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

Money Supply

The money supply in the economy is controlled by the

Money Supply

The money supply in the economy is controlled by the

How r Is Determined

MS curve is vertical: Changes in r do

How r Is Determined

MS curve is vertical: Changes in r do

Equilibrium in the Money Market

The interest rate adjusts to bring money

Equilibrium in the Money Market

The interest rate adjusts to bring money

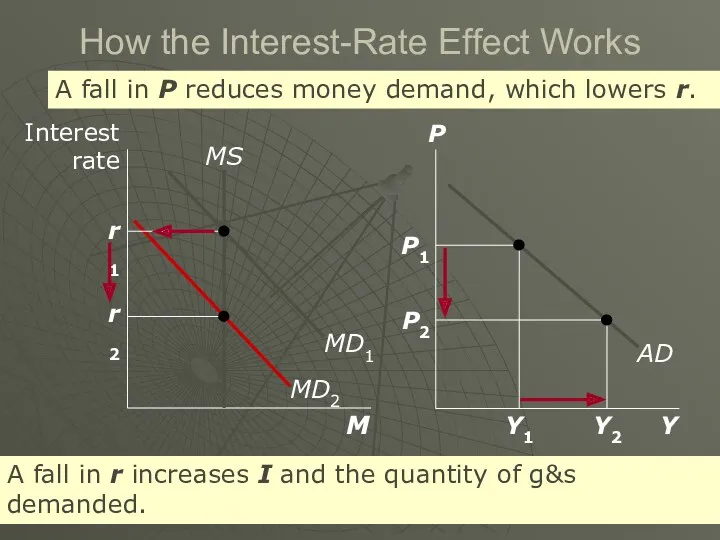

How the Interest-Rate Effect Works

P2

A fall in P reduces money demand,

How the Interest-Rate Effect Works

P2

A fall in P reduces money demand,

Monetary Policy and

Aggregate Demand

To achieve macroeconomic goals, the Fed can

Monetary Policy and

Aggregate Demand

To achieve macroeconomic goals, the Fed can

Changes in the Money Supply

Example: The Fed buys government bonds in

Changes in the Money Supply

Example: The Fed buys government bonds in

The Role of Interest-Rate Targets in Fed Policy

In recent years, the

The Role of Interest-Rate Targets in Fed Policy

In recent years, the

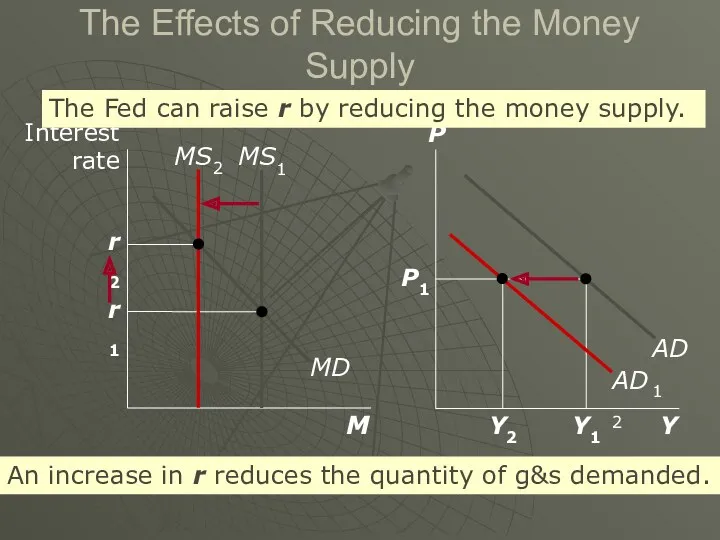

The Effects of Reducing the Money Supply

The Fed can raise r

The Effects of Reducing the Money Supply

The Fed can raise r

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

Interest Rates and Bond Prices

Inverse Relationship

Bond prices increase the interest rate

Interest Rates and Bond Prices

Inverse Relationship

Bond prices increase the interest rate

The Market for Loanable Funds

Market for loanable funds – the market

The Market for Loanable Funds

Market for loanable funds – the market

Supply and Demand for Loanable Funds

The supply of loanable funds comes

Supply and Demand for Loanable Funds

The supply of loanable funds comes

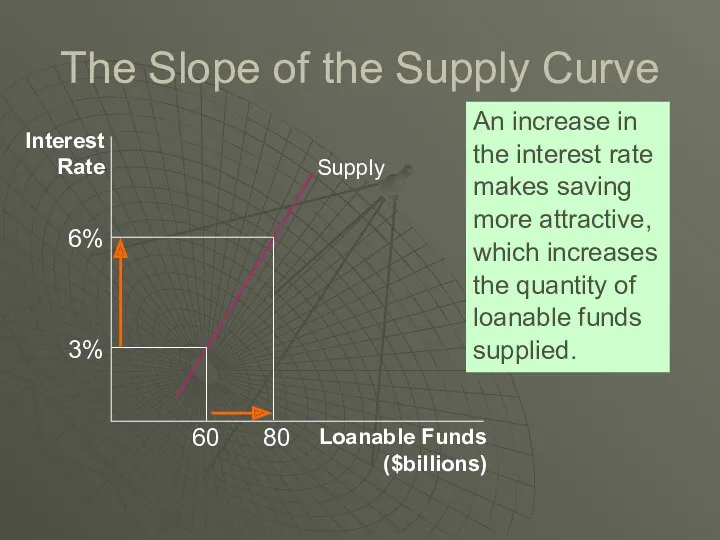

The Slope of the Supply Curve

An increase in the interest rate

The Slope of the Supply Curve

An increase in the interest rate

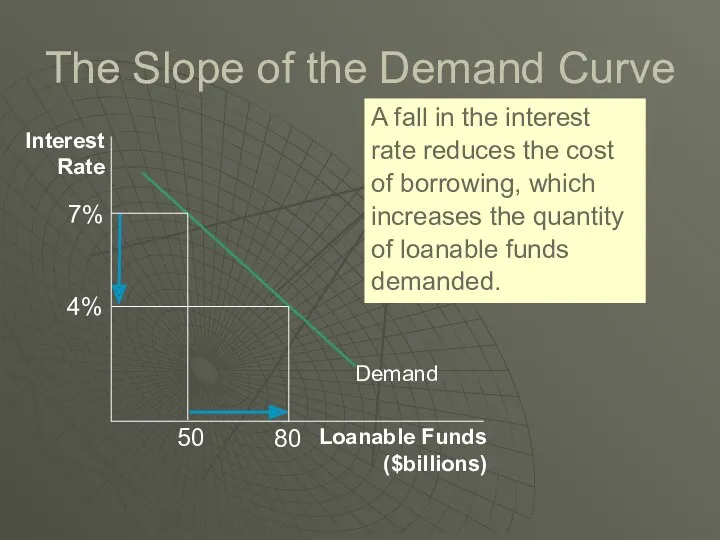

The Slope of the Demand Curve

A fall in the interest rate

The Slope of the Demand Curve

A fall in the interest rate

Supply and Demand for Loanable Funds

The price of a loan is

Supply and Demand for Loanable Funds

The price of a loan is

Supply and Demand for Loanable Funds

At the equilibrium, the quantity of

Supply and Demand for Loanable Funds

At the equilibrium, the quantity of

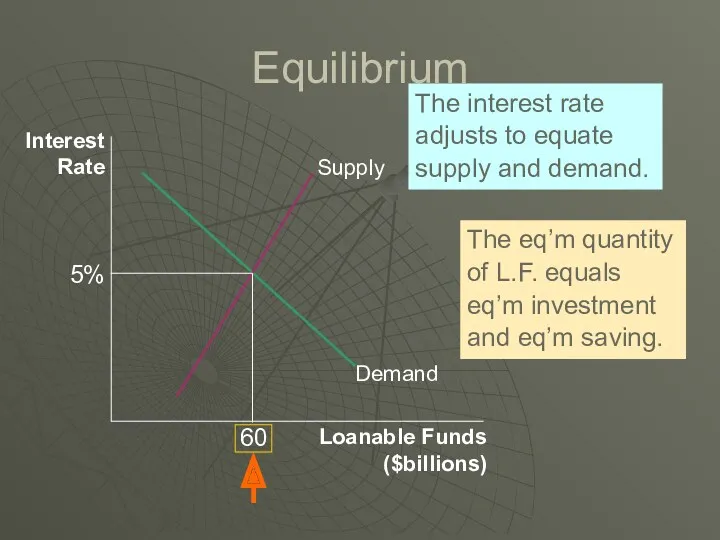

Equilibrium

The interest rate adjusts to equate supply and demand.

The eq’m

Equilibrium

The interest rate adjusts to equate supply and demand.

The eq’m

Shifts of the Demand for Loanable Funds

Changes in Perceived Business Opportunities

If

Shifts of the Demand for Loanable Funds

Changes in Perceived Business Opportunities

If

The Crowding-Out Effect

The crowding out effect works in the opposite direction.

Crowding

The Crowding-Out Effect

The crowding out effect works in the opposite direction.

Crowding

The Crowding-Out Effect

The higher interest rate raises the cost of borrowing

The Crowding-Out Effect

The higher interest rate raises the cost of borrowing

Shifts of the Supply of Loanable Funds

Changes in private savings behavior

Save

Shifts of the Supply of Loanable Funds

Changes in private savings behavior

Save

Policy 1: Saving Incentives

Savings rates in the United States are relatively

Policy 1: Saving Incentives

Savings rates in the United States are relatively

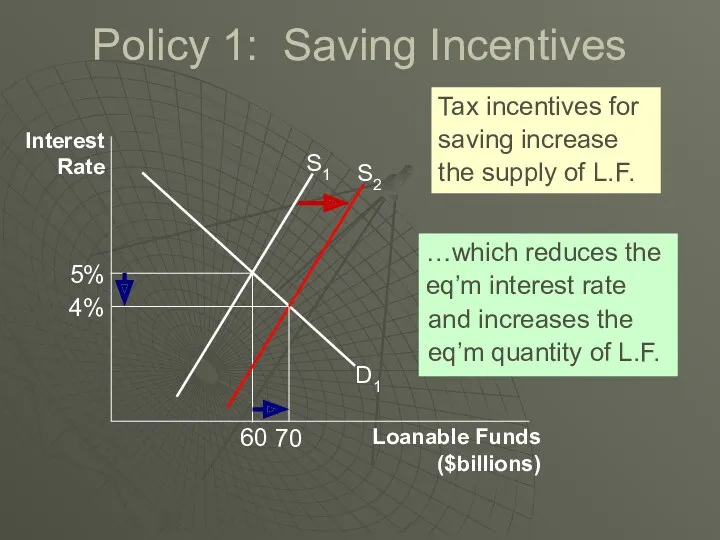

Policy 1: Saving Incentives

Interest

Rate

Loanable Funds ($billions)

D1

Tax incentives for saving increase the

Policy 1: Saving Incentives

Interest

Rate

Loanable Funds ($billions)

D1

Tax incentives for saving increase the

Policy 2: Investment Incentive

Suppose instead that the government passed a new

Policy 2: Investment Incentive

Suppose instead that the government passed a new

Policy 2: Investment Incentives

Interest

Rate

Loanable Funds ($billions)

D1

An investment tax credit increases the

Policy 2: Investment Incentives

Interest

Rate

Loanable Funds ($billions)

D1

An investment tax credit increases the

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

A C T I V E L E A R N

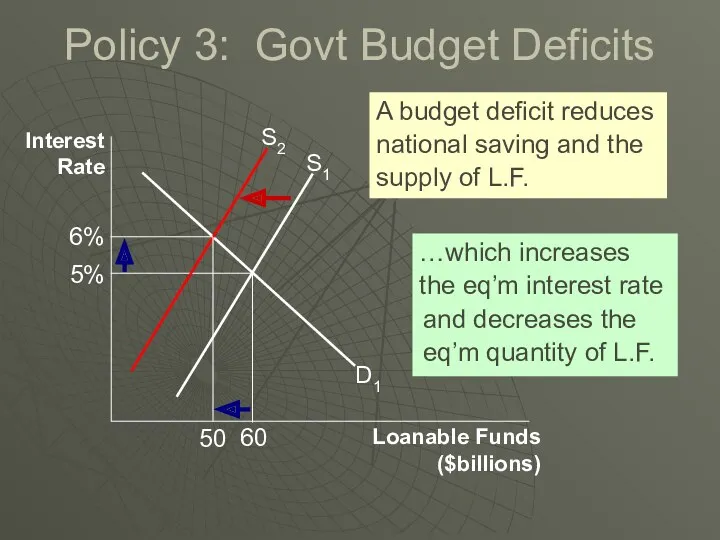

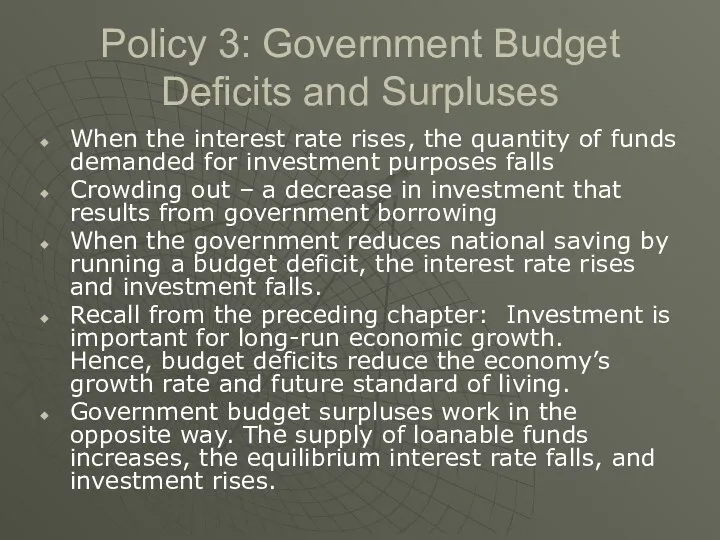

Policy 3: Government Budget Deficits and Surpluses

A budget deficit occurs if

Policy 3: Government Budget Deficits and Surpluses

A budget deficit occurs if

Policy 3: Govt Budget Deficits

Interest

Rate

Loanable Funds ($billions)

D1

A budget deficit reduces national

Policy 3: Govt Budget Deficits

Interest

Rate

Loanable Funds ($billions)

D1

A budget deficit reduces national

Policy 3: Government Budget Deficits and Surpluses

When the interest rate rises,

Policy 3: Government Budget Deficits and Surpluses

When the interest rate rises,

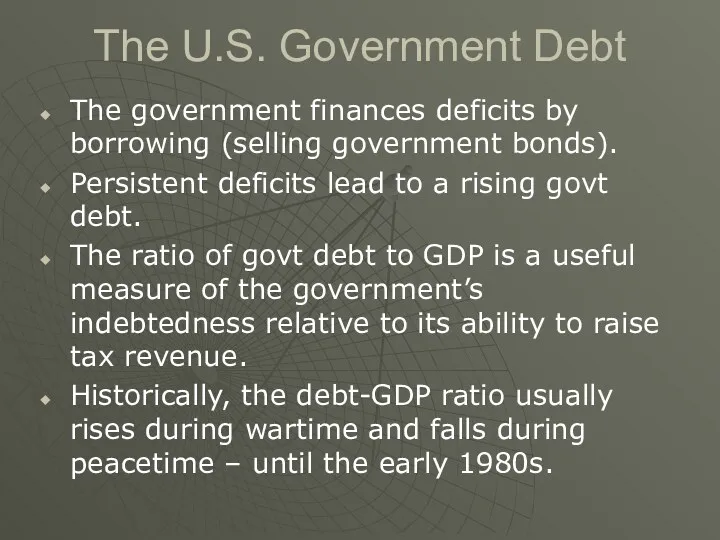

The U.S. Government Debt

The government finances deficits by borrowing (selling government

The U.S. Government Debt

The government finances deficits by borrowing (selling government

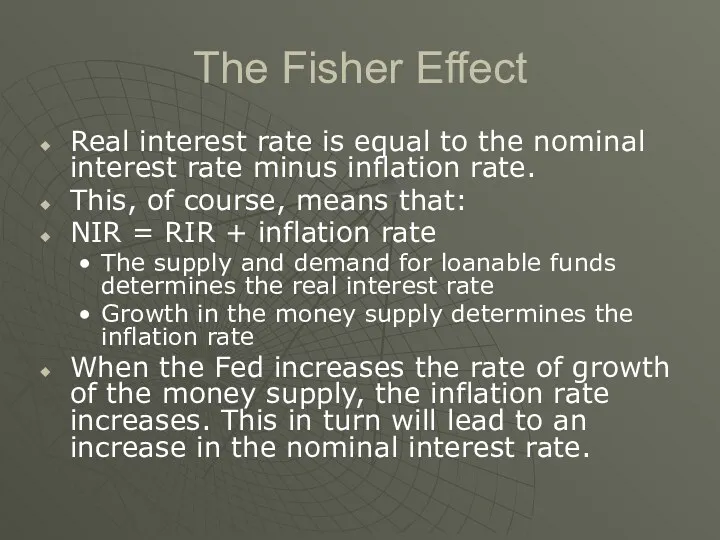

The Fisher Effect

Real interest rate is equal to the nominal interest

The Fisher Effect

Real interest rate is equal to the nominal interest

The Fisher Effect

Fisher Effect – the one-for-one adjustment of the nominal

The Fisher Effect

Fisher Effect – the one-for-one adjustment of the nominal

Interest Rates in the Long Run and the Short Run

It may

Interest Rates in the Long Run and the Short Run

It may

Interest Rates in the Long Run and the Short Run

In the

Interest Rates in the Long Run and the Short Run

In the

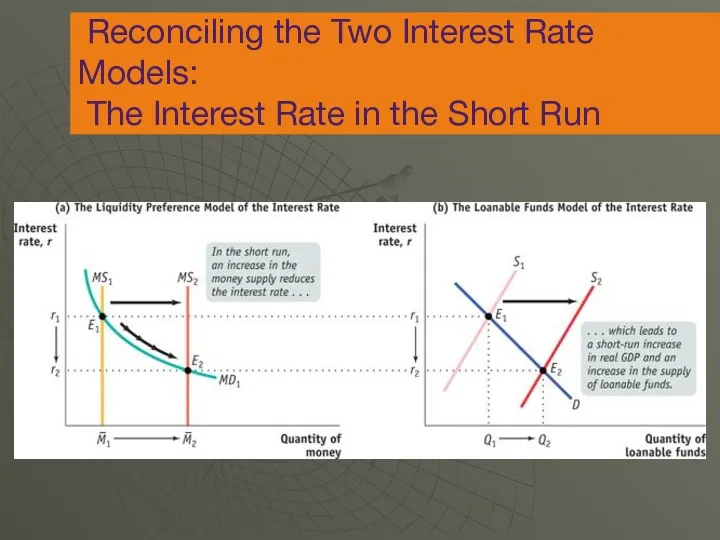

Reconciling the Two Interest Rate Models:

The Interest Rate in

Reconciling the Two Interest Rate Models: The Interest Rate in

Статистика оплаты труда на предприятии

Статистика оплаты труда на предприятии Формирование уставного капитала

Формирование уставного капитала Программы регионального финансирования субъектов малого и среднего предпринимательства

Программы регионального финансирования субъектов малого и среднего предпринимательства Бухгалтерский учет. Тесты-тренажер

Бухгалтерский учет. Тесты-тренажер Фискальный механизм использования водных биологических ресурсов в Российской Федерации

Фискальный механизм использования водных биологических ресурсов в Российской Федерации Структура модели управления недвижимостью и характеристика ее элементов. Принципы принятия инвестиционных решений

Структура модели управления недвижимостью и характеристика ее элементов. Принципы принятия инвестиционных решений Banking system

Banking system Корпоративная форма организации бизнеса и управление корпоративными финансами

Корпоративная форма организации бизнеса и управление корпоративными финансами Уровень лояльности работников к деятельности предприятия, на основании учёта их социальных потребностей

Уровень лояльности работников к деятельности предприятия, на основании учёта их социальных потребностей Реабилитация бизнеса, если финансовые организации отказывают в проведении операции или в заключении договора банковского счета

Реабилитация бизнеса, если финансовые организации отказывают в проведении операции или в заключении договора банковского счета Стратегия и тактика в антикризисном управлении. Тема № 3

Стратегия и тактика в антикризисном управлении. Тема № 3 Организация работы бухгалтерской службы кредитной организации

Организация работы бухгалтерской службы кредитной организации Внедрение персонифицированного финансирования дополнительного образования детей

Внедрение персонифицированного финансирования дополнительного образования детей Неделя финансовой грамотности для детей и молодежи. 10-11 класс

Неделя финансовой грамотности для детей и молодежи. 10-11 класс Центральні банки

Центральні банки МСФО (IFRS) 13. Оценка по справедливой стоимости

МСФО (IFRS) 13. Оценка по справедливой стоимости Сутність та значення фондової біржі

Сутність та значення фондової біржі Применения новых ФСБУ при аудите бухгалтерской отчетности

Применения новых ФСБУ при аудите бухгалтерской отчетности Учет материально-производственных запасов

Учет материально-производственных запасов Учет расходов коммерческого банка на примере ПАО Сбербанк России

Учет расходов коммерческого банка на примере ПАО Сбербанк России Урок финансовой грамотности

Урок финансовой грамотности Инициативное бюджетирование в Республике Башкортостан

Инициативное бюджетирование в Республике Башкортостан Программа по кредитованию дополнительного оборудования и сервисных услуг

Программа по кредитованию дополнительного оборудования и сервисных услуг Обязательное страхование вкладов: проблемы и перспективы( на примере ПАО Росгосстрах Банк)

Обязательное страхование вкладов: проблемы и перспективы( на примере ПАО Росгосстрах Банк) Налог на имущество организаций

Налог на имущество организаций Налог на добавленную стоимость

Налог на добавленную стоимость ВЭД услуги. Сложные вопросы НДС

ВЭД услуги. Сложные вопросы НДС Topic 1. Introduction to Finance

Topic 1. Introduction to Finance