- Valuing bonds. (Lecture 6)

Содержание

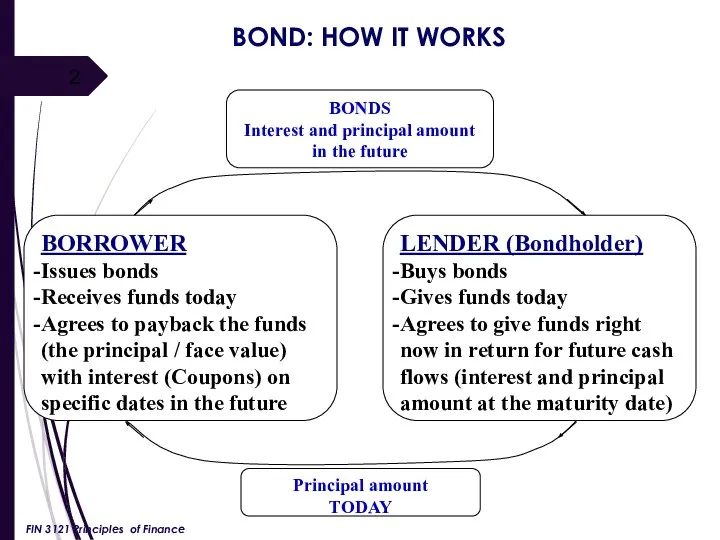

- 2. BOND: HOW IT WORKS FIN 3121 Principles of Finance

- 3. BONDS are debt instruments Two features that set bonds apart from equity investments: The promised cash

- 4. Classification of bonds based on an issuer: Government bonds Corporate bonds Financial institutions bonds FIN 3121

- 5. Classification of bonds based on the currency and origin Bond (conventional one) is issued in a

- 6. Conventional or Straight bonds have a fixed coupon (usually paid on an semi-annual basis) and maturity

- 7. Zero-coupon bonds do not have interest payments, are sold at a significant discount from their eventual

- 8. Perpetual Bond (consol) is a bond in which the issuer does not repay the principal. Rather,

- 9. Callable bonds: the issuer has the right, but not the obligation, to buy back the bonds

- 10. Puttable bonds (put bond, putable or retractable bond) are bonds with an embedded put option. The

- 11. High-yield bonds are those that are rated to be “below investment grade” by credit rating agencies

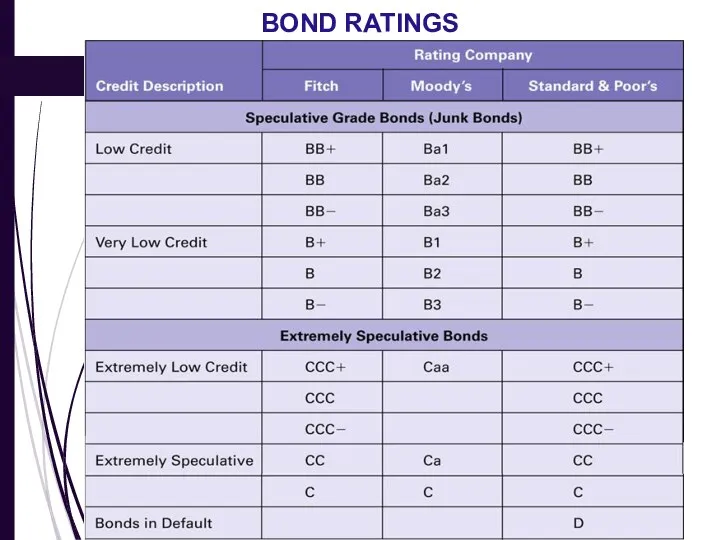

- 12. BOND RATINGS Ratings are produced by Moody’s, Standard and Poor’s, and Fitch Range from AAA (top-rated)

- 13. BOND RATINGS

- 14. BOND RATINGS

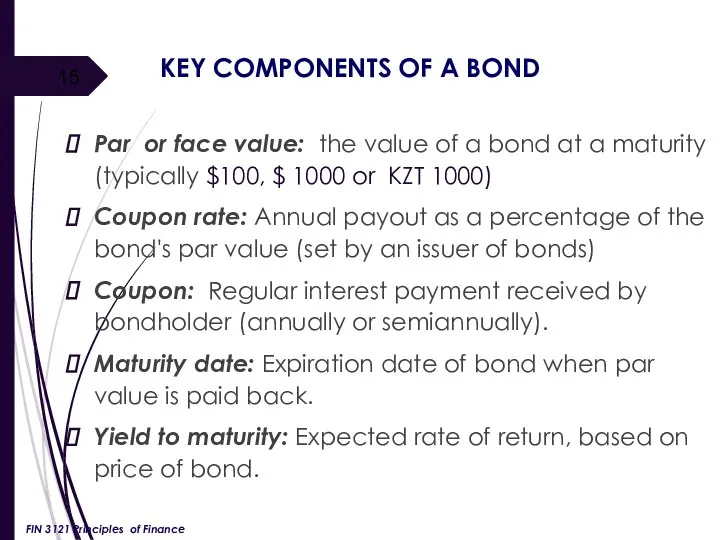

- 15. KEY COMPONENTS OF A BOND Par or face value: the value of a bond at a

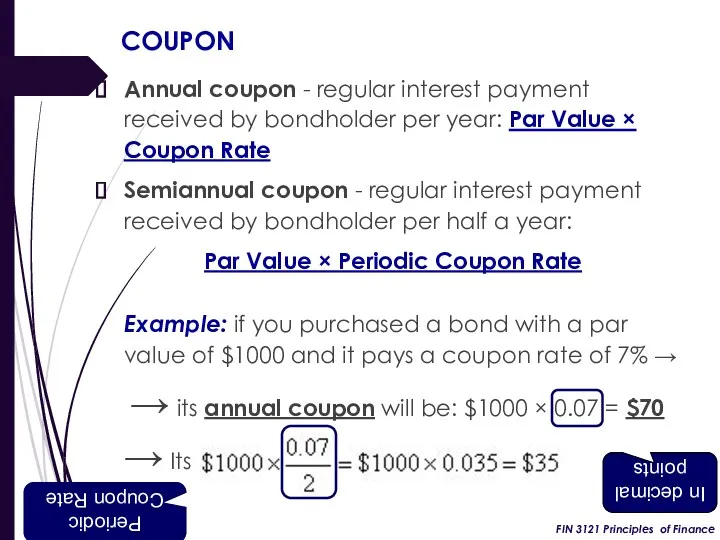

- 16. COUPON Annual coupon - regular interest payment received by bondholder per year: Par Value × Coupon

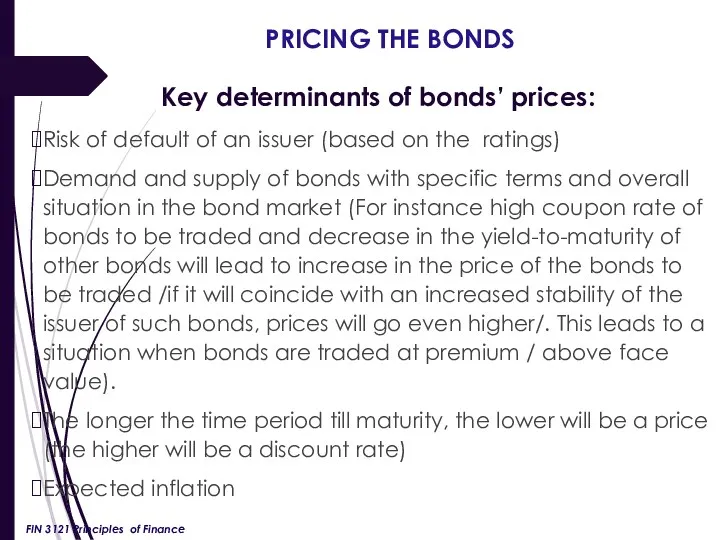

- 17. PRICING THE BONDS Key determinants of bonds’ prices: Risk of default of an issuer (based on

- 18. VALUING BONDS Value of the bond can be estimated by using present value techniques, i.e., discounting

- 19. VALUING BONDS FIN 3121 Principles of Finance

- 20. VALUING BONDS Example Calculate the price of a 20-year, 8% coupon (paid annually) corporate bond (par

- 21. VALUING BONDS Solution Present value of coupons: Present Value of par value: Price of bond =

- 22. VALUING BONDS Solution: Using a financial calculator Input: N i% PV PMT FV Key: 20 10

- 23. SEMIANNUAL BONDS Most bonds pay coupons on a semiannual basis. For valuing such bonds, the values

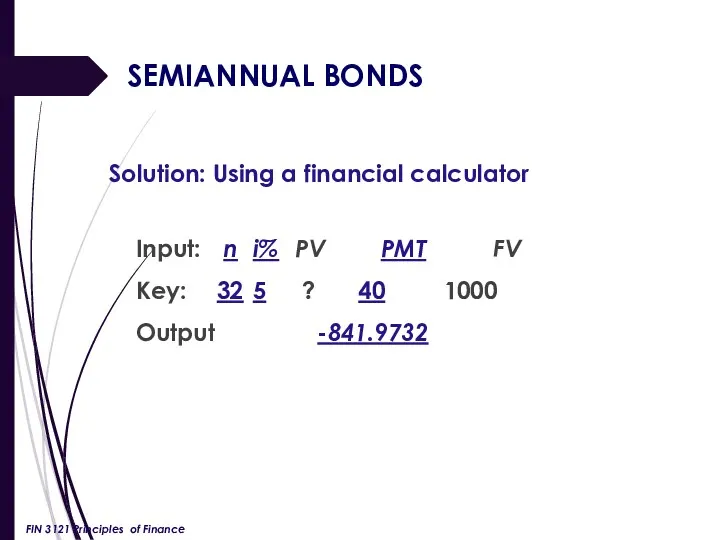

- 24. SEMIANNUAL BONDS Example Four years ago, the XYZ Corporation issued an 8% coupon (paid semiannually), 20-year,

- 25. SEMIANNUAL BONDS Solution FIN 3121 Principles of Finance

- 26. SEMIANNUAL BONDS Solution: Using a financial calculator Input: n i% PV PMT FV Key: 32 5

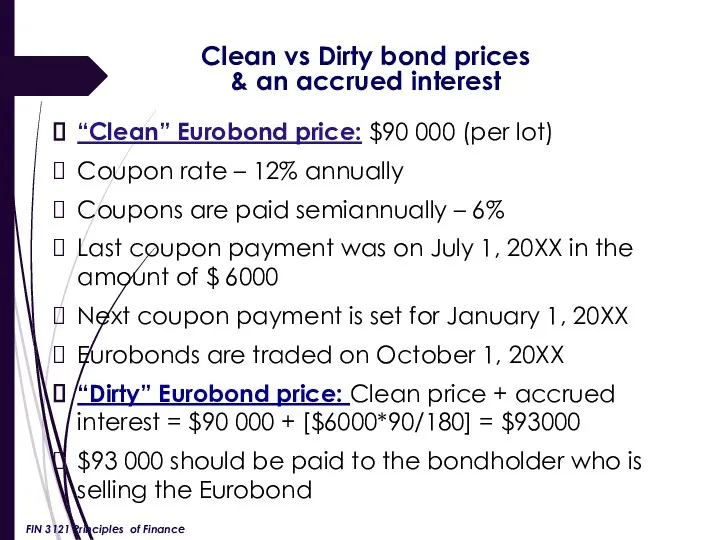

- 27. Because many of the bonds traded in the secondary market are often traded in between coupon

- 28. “Clean” Eurobond price: $90 000 (per lot) Coupon rate – 12% annually Coupons are paid semiannually

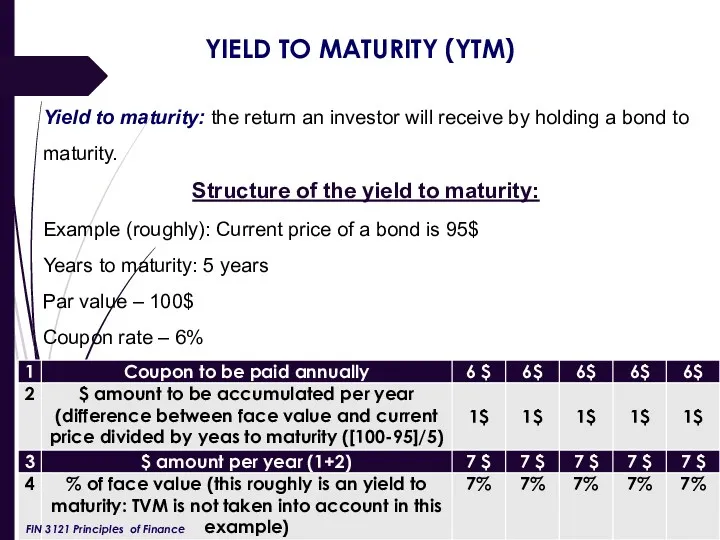

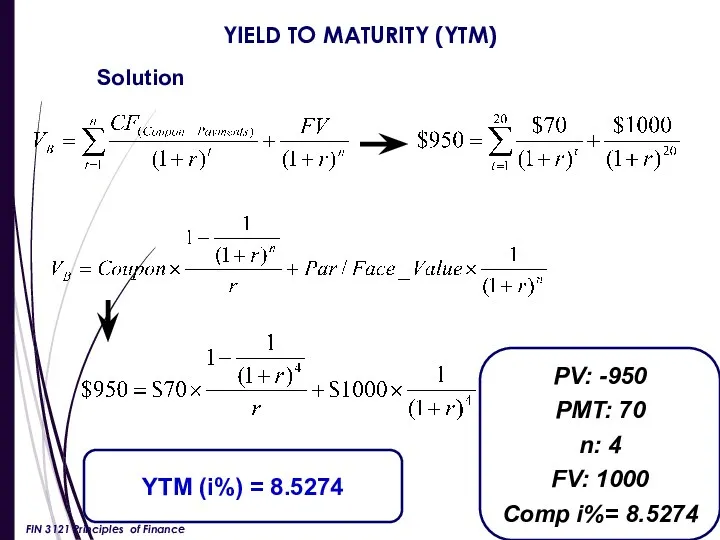

- 29. YIELD TO MATURITY (YTM) Yield to maturity: the return an investor will receive by holding a

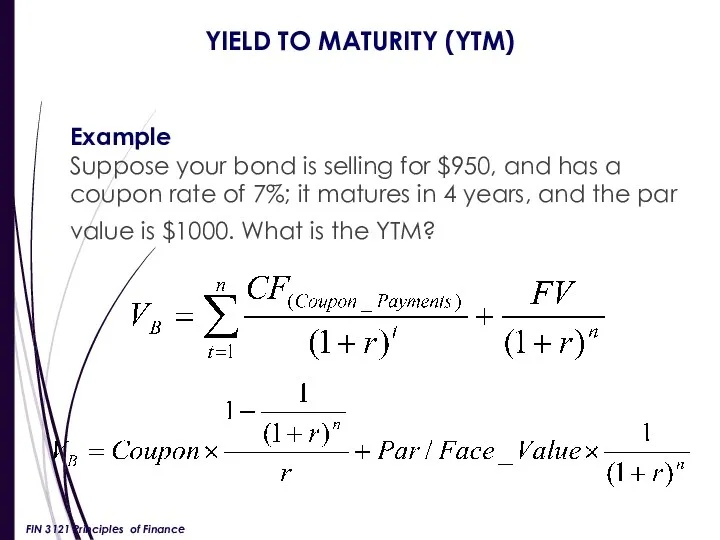

- 30. YIELD TO MATURITY (YTM) Example Suppose your bond is selling for $950, and has a coupon

- 31. YIELD TO MATURITY (YTM) PV: -950 PMT: 70 n: 4 FV: 1000 Comp i%= 8.5274 Solution

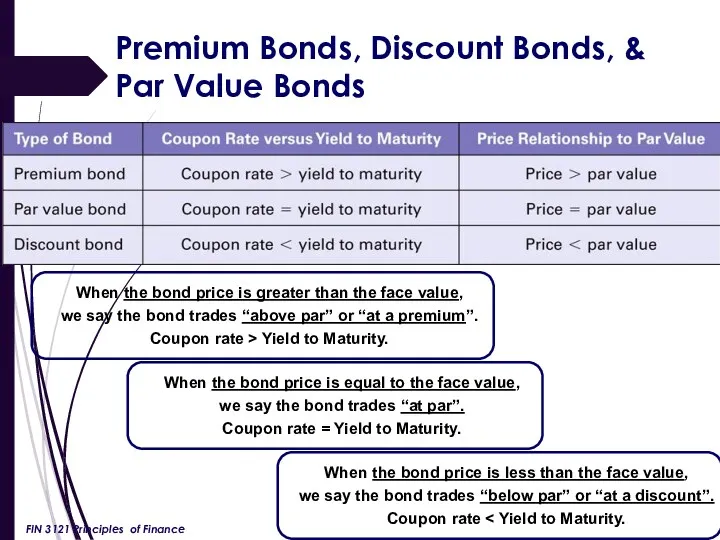

- 32. Premium Bonds, Discount Bonds, & Par Value Bonds DISCOUNT A bond is selling at a discount

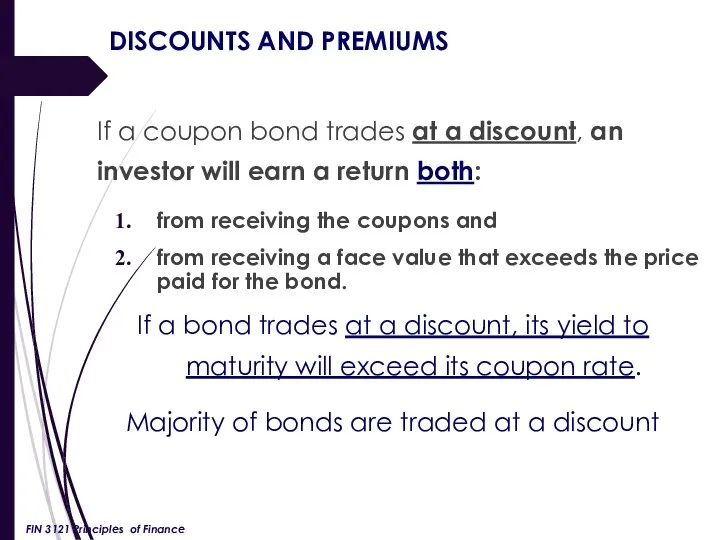

- 33. DISCOUNTS AND PREMIUMS If a coupon bond trades at a discount, an investor will earn a

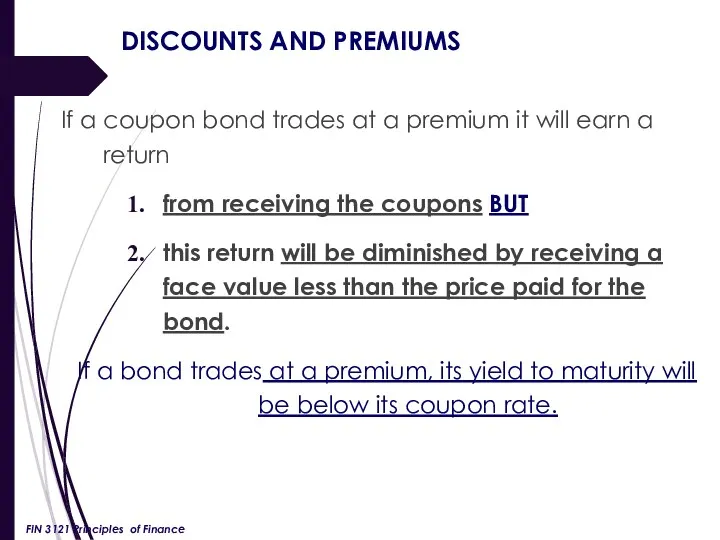

- 34. DISCOUNTS AND PREMIUMS If a coupon bond trades at a premium it will earn a return

- 35. Premium Bonds, Discount Bonds, & Par Value Bonds When the bond price is greater than the

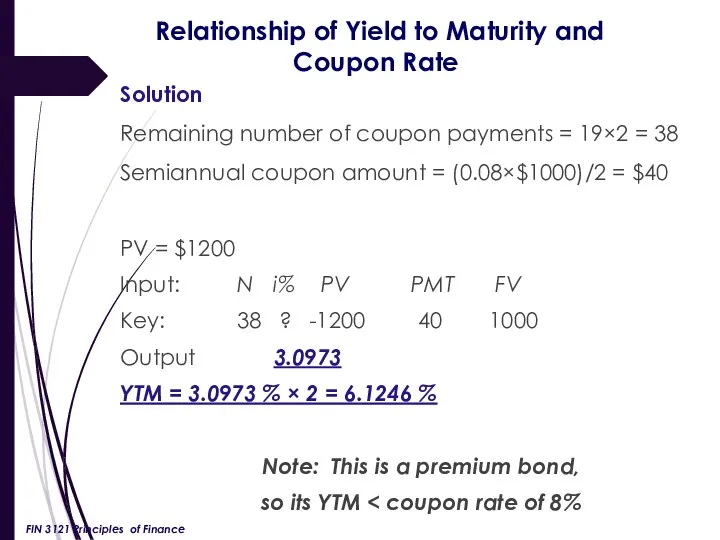

- 36. Relationship of Yield to Maturity and Coupon Rate Example Last year, the ABC Corporation had issued

- 37. Relationship of Yield to Maturity and Coupon Rate Solution Remaining number of coupon payments = 19×2

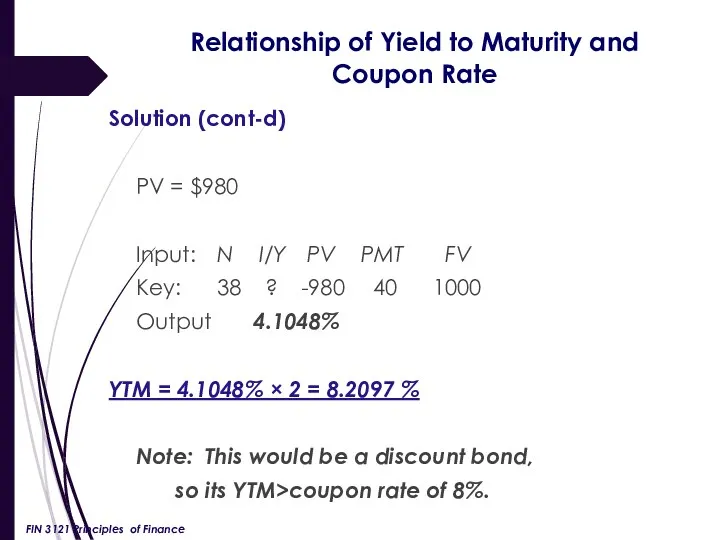

- 38. Relationship of Yield to Maturity and Coupon Rate Solution (cont-d) PV = $980 Input: N I/Y

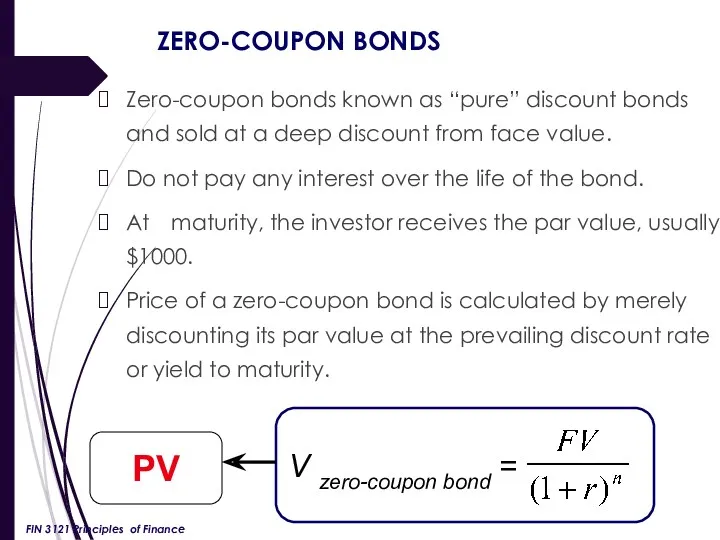

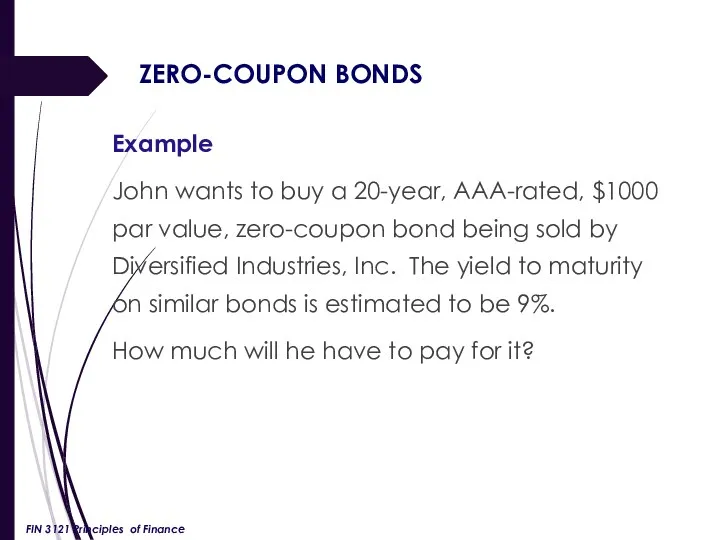

- 39. ZERO-COUPON BONDS Zero-coupon bonds known as “pure” discount bonds and sold at a deep discount from

- 40. ZERO-COUPON BONDS Example John wants to buy a 20-year, AAA-rated, $1000 par value, zero-coupon bond being

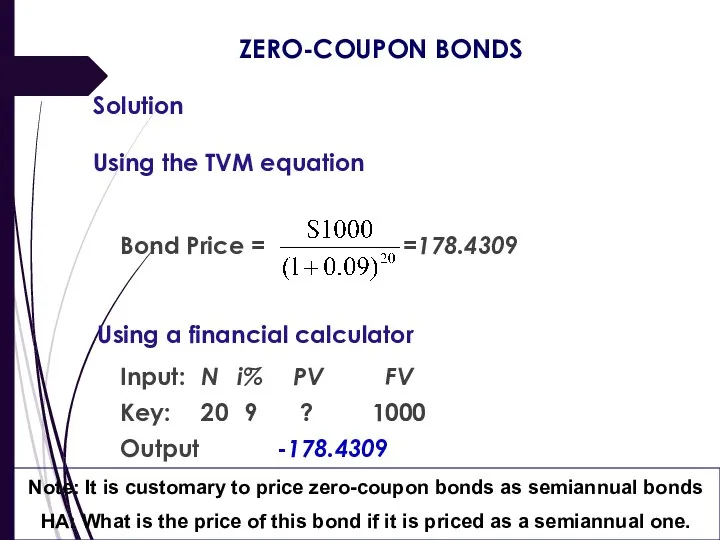

- 41. ZERO-COUPON BONDS Solution Using the TVM equation Bond Price = =178.4309 Using a financial calculator Input:

- 43. Скачать презентацию

BOND: HOW IT WORKS

FIN 3121 Principles of Finance

BOND: HOW IT WORKS

FIN 3121 Principles of Finance

BONDS are debt instruments

Two features that set bonds apart from equity

BONDS are debt instruments

Two features that set bonds apart from equity

Classification of bonds based on an issuer:

Government bonds

Corporate bonds

Financial institutions bonds

Classification of bonds based on an issuer:

Government bonds

Corporate bonds

Financial institutions bonds

Classification of bonds based on the currency and origin

Bond (conventional one)

Classification of bonds based on the currency and origin

Bond (conventional one)

Conventional or Straight bonds have a fixed coupon (usually paid on an

Conventional or Straight bonds have a fixed coupon (usually paid on an

Zero-coupon bonds do not have interest payments, are sold at a significant discount

Zero-coupon bonds do not have interest payments, are sold at a significant discount

Perpetual Bond (consol) is a bond in which the issuer does not

Perpetual Bond (consol) is a bond in which the issuer does not

Callable bonds: the issuer has the right, but not the obligation,

Callable bonds: the issuer has the right, but not the obligation,

Puttable bonds (put bond, putable or retractable bond) are bonds with an embedded put

Puttable bonds (put bond, putable or retractable bond) are bonds with an embedded put

High-yield bonds are those that are rated to be “below investment grade”

High-yield bonds are those that are rated to be “below investment grade”

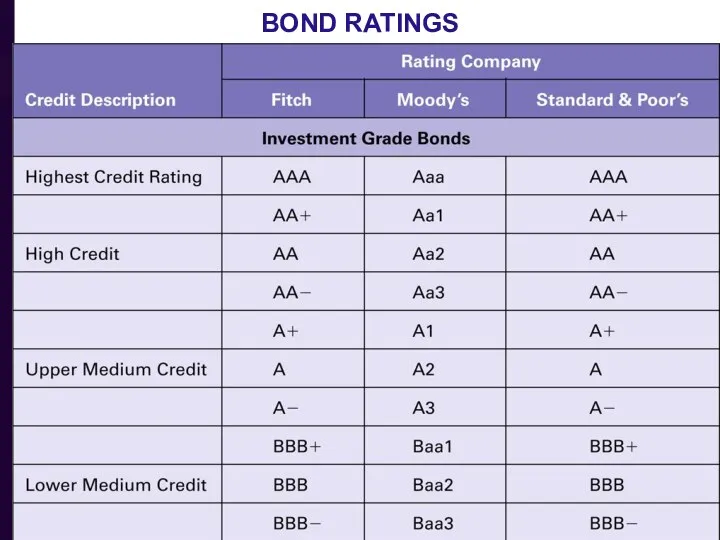

BOND RATINGS

Ratings are produced by Moody’s, Standard and Poor’s, and Fitch

BOND RATINGS

Ratings are produced by Moody’s, Standard and Poor’s, and Fitch

BOND RATINGS

BOND RATINGS

BOND RATINGS

BOND RATINGS

KEY COMPONENTS OF A BOND

Par or face value: the value of

KEY COMPONENTS OF A BOND

Par or face value: the value of

COUPON

Annual coupon - regular interest payment received by bondholder per year:

COUPON

Annual coupon - regular interest payment received by bondholder per year:

PRICING THE BONDS

Key determinants of bonds’ prices:

Risk of default of an

PRICING THE BONDS

Key determinants of bonds’ prices:

Risk of default of an

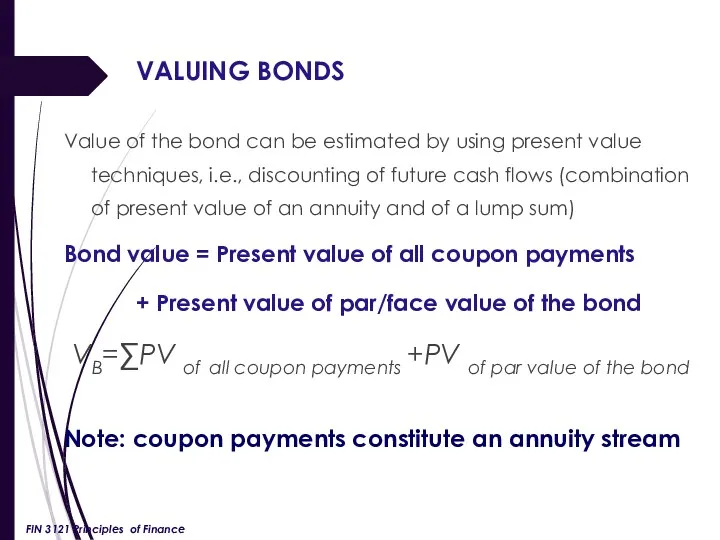

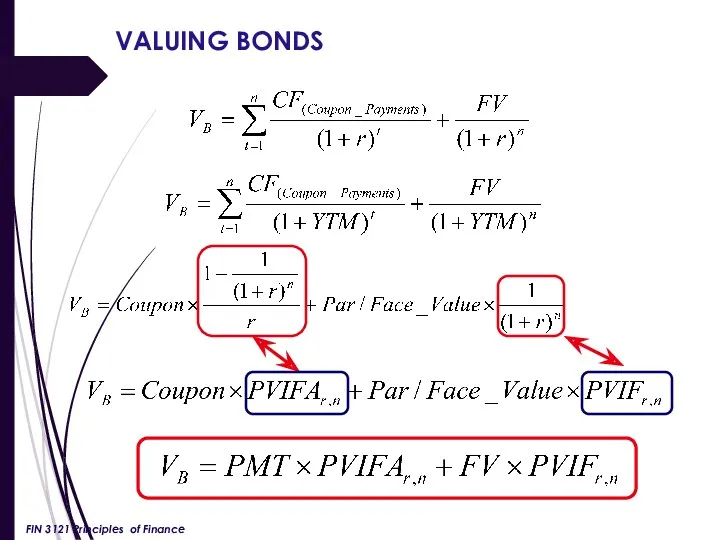

VALUING BONDS

Value of the bond can be estimated by using present

VALUING BONDS

Value of the bond can be estimated by using present

VALUING BONDS

FIN 3121 Principles of Finance

VALUING BONDS

FIN 3121 Principles of Finance

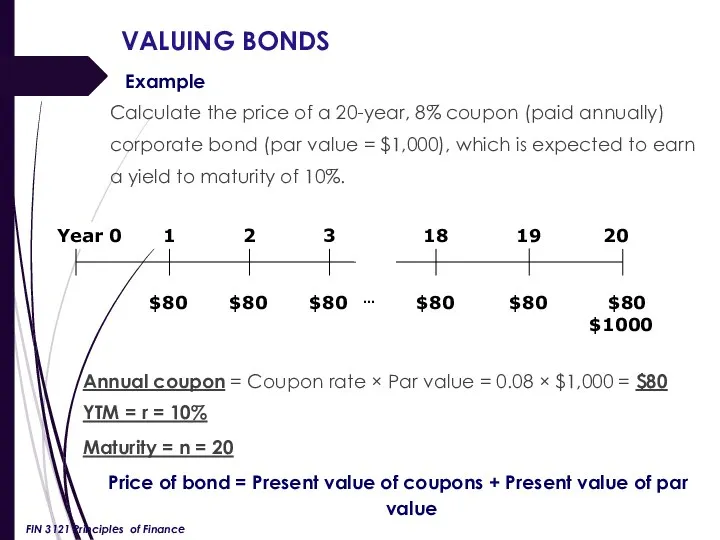

VALUING BONDS

Example

Calculate the price of a 20-year, 8% coupon (paid

VALUING BONDS

Example

Calculate the price of a 20-year, 8% coupon (paid

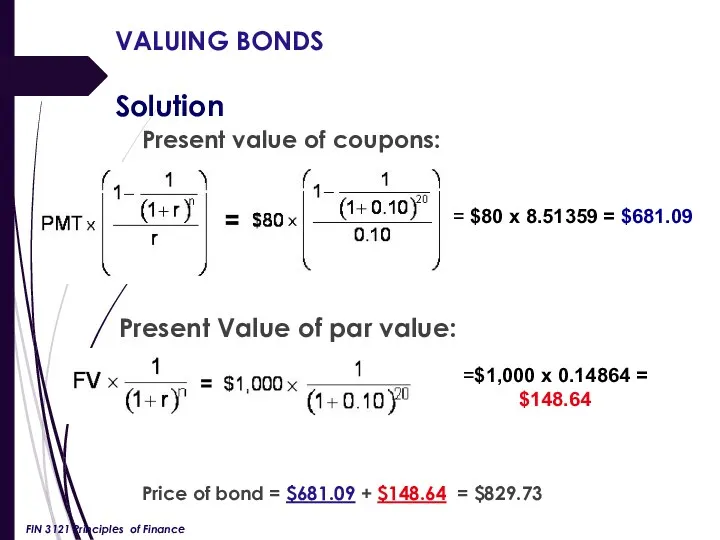

VALUING BONDS

Solution

Present value of coupons:

Present Value of par value:

Price

VALUING BONDS

Solution

Present value of coupons:

Present Value of par value:

Price

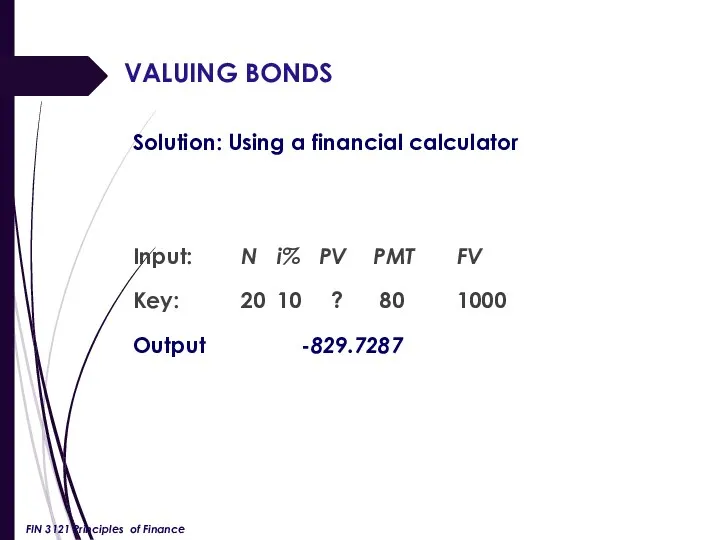

VALUING BONDS

Solution: Using a financial calculator

Input: N i% PV PMT FV

Key: 20 10 ? 80

VALUING BONDS

Solution: Using a financial calculator

Input: N i% PV PMT FV

Key: 20 10 ? 80

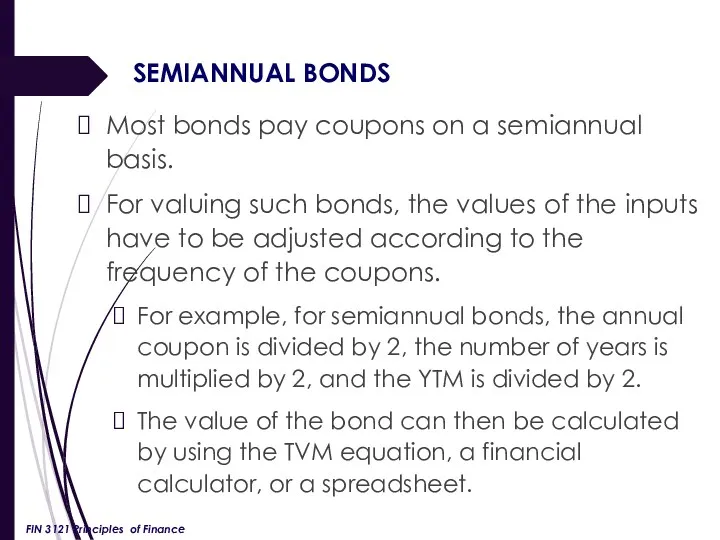

SEMIANNUAL BONDS

Most bonds pay coupons on a semiannual basis.

For valuing such

SEMIANNUAL BONDS

Most bonds pay coupons on a semiannual basis.

For valuing such

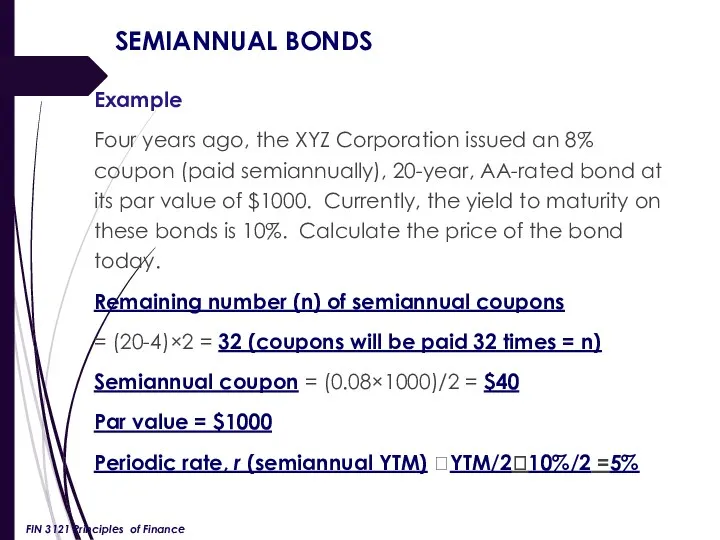

SEMIANNUAL BONDS

Example

Four years ago, the XYZ Corporation issued an 8% coupon

SEMIANNUAL BONDS

Example

Four years ago, the XYZ Corporation issued an 8% coupon

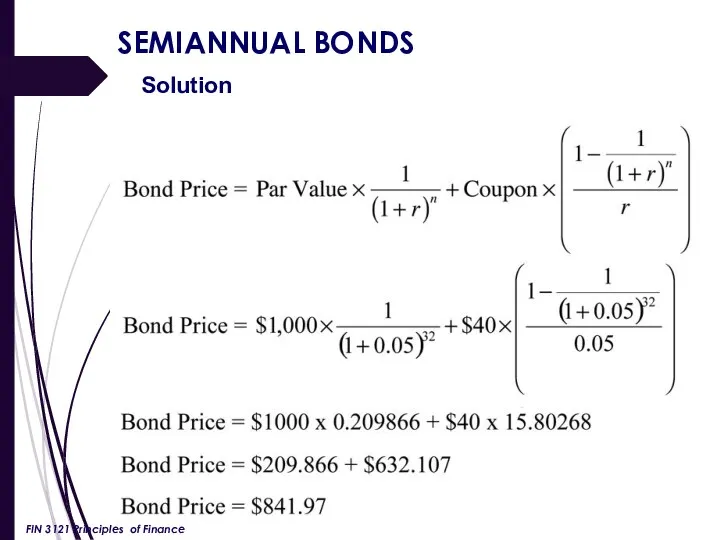

SEMIANNUAL BONDS

Solution

FIN 3121 Principles of Finance

SEMIANNUAL BONDS

Solution

FIN 3121 Principles of Finance

SEMIANNUAL BONDS

Solution: Using a financial calculator

Input: n i% PV PMT FV

Key: 32 5

SEMIANNUAL BONDS

Solution: Using a financial calculator

Input: n i% PV PMT FV

Key: 32 5

Because many of the bonds traded in the secondary market are often

Because many of the bonds traded in the secondary market are often

“Clean” Eurobond price: $90 000 (per lot)

Coupon rate – 12% annually

Coupons

“Clean” Eurobond price: $90 000 (per lot)

Coupon rate – 12% annually

Coupons

YIELD TO MATURITY (YTM)

Yield to maturity: the return an investor will

YIELD TO MATURITY (YTM)

Yield to maturity: the return an investor will

YIELD TO MATURITY (YTM)

Example

Suppose your bond is selling for $950, and

YIELD TO MATURITY (YTM)

Example

Suppose your bond is selling for $950, and

YIELD TO MATURITY (YTM)

PV: -950

PMT: 70

n: 4

FV: 1000

Comp i%= 8.5274

Solution

YTM (i%)

YIELD TO MATURITY (YTM)

PV: -950

PMT: 70

n: 4

FV: 1000

Comp i%= 8.5274

Solution

YTM (i%)

Premium Bonds, Discount Bonds, &

Par Value Bonds

DISCOUNT

A bond is selling

Premium Bonds, Discount Bonds, &

Par Value Bonds

DISCOUNT

A bond is selling

DISCOUNTS AND PREMIUMS

If a coupon bond trades at a discount, an

DISCOUNTS AND PREMIUMS

If a coupon bond trades at a discount, an

DISCOUNTS AND PREMIUMS

If a coupon bond trades at a premium it

DISCOUNTS AND PREMIUMS

If a coupon bond trades at a premium it

Premium Bonds, Discount Bonds, &

Par Value Bonds

When the bond price

Premium Bonds, Discount Bonds, &

Par Value Bonds

When the bond price

Relationship of Yield to Maturity and Coupon Rate

Example

Last

Relationship of Yield to Maturity and Coupon Rate

Example

Last

Relationship of Yield to Maturity and Coupon Rate

Solution

Remaining number

Relationship of Yield to Maturity and Coupon Rate

Solution

Remaining number

Relationship of Yield to Maturity and

Coupon Rate

Solution (cont-d)

PV

Relationship of Yield to Maturity and

Coupon Rate

Solution (cont-d)

PV

ZERO-COUPON BONDS

Zero-coupon bonds known as “pure” discount bonds and sold at

ZERO-COUPON BONDS

Zero-coupon bonds known as “pure” discount bonds and sold at

ZERO-COUPON BONDS

Example

John wants to buy a 20-year, AAA-rated, $1000 par value,

ZERO-COUPON BONDS

Example

John wants to buy a 20-year, AAA-rated, $1000 par value,

ZERO-COUPON BONDS

Solution

Using the TVM equation

Bond Price = =178.4309

Using a financial calculator

ZERO-COUPON BONDS

Solution

Using the TVM equation

Bond Price = =178.4309

Using a financial calculator

Организация и управление бюджетного процесса

Организация и управление бюджетного процесса Мир привилегий МКБ BP CLUB

Мир привилегий МКБ BP CLUB Налог на акциз

Налог на акциз Принципы организации финансов организаций (предприятий)

Принципы организации финансов организаций (предприятий) Види підприємницької діяльності

Види підприємницької діяльності Учебно-методический комплект: основы финансовой грамотности

Учебно-методический комплект: основы финансовой грамотности Понятие, экономическая сущность и функции налогов. Классификация налогов

Понятие, экономическая сущность и функции налогов. Классификация налогов Доходы и расходы организации, формирование финансового результата и его планирование

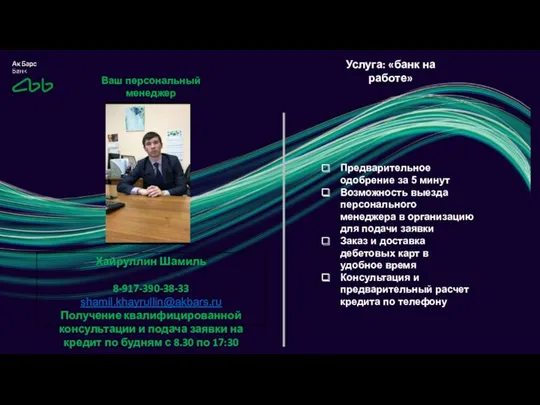

Доходы и расходы организации, формирование финансового результата и его планирование Ак Барс Банк. Услуга: банк на работе

Ак Барс Банк. Услуга: банк на работе Бюджет для граждан

Бюджет для граждан Система налогообложения в виде единого налога на вмененный доход

Система налогообложения в виде единого налога на вмененный доход Platinum Bank. Банк и банковские продукты

Platinum Bank. Банк и банковские продукты Сведения для ведения индивидуального учета и сведения о начисленных страховых взносах на обязательное социальное страхование

Сведения для ведения индивидуального учета и сведения о начисленных страховых взносах на обязательное социальное страхование Семейная экономика

Семейная экономика Аудиторлық тәуекелділік және оның маңызы

Аудиторлық тәуекелділік және оның маңызы Учет труда и заработной платы

Учет труда и заработной платы Государственный долг Украины. Взаимоотношения Украины и МВФ на современном этапе. Технический дефолт Украины

Государственный долг Украины. Взаимоотношения Украины и МВФ на современном этапе. Технический дефолт Украины Налоги и налогообложение. (Темы 1-6)

Налоги и налогообложение. (Темы 1-6) Учет и анализ финансовых результатов в растениеводстве в ОАО Литвяны-Агро

Учет и анализ финансовых результатов в растениеводстве в ОАО Литвяны-Агро Инвестиционный портфель. Точка Роста

Инвестиционный портфель. Точка Роста Финансовые рынки

Финансовые рынки Оборотные средства предприятия

Оборотные средства предприятия Семейный бюджет

Семейный бюджет Финансовые институты. Банковская система

Финансовые институты. Банковская система Возникновение и эволюция денег на Руси

Возникновение и эволюция денег на Руси История становления социального обеспечения в России

История становления социального обеспечения в России Вклад Престиж. Банк Санкт-Петербург

Вклад Престиж. Банк Санкт-Петербург Финансовое состояние корпорации: понятие и методика анализа

Финансовое состояние корпорации: понятие и методика анализа