- Bookkeping

Содержание

- 2. PLAN Introduction Methods of bookkeeping Double-entry bookkeeping Day books and ledgers Balancing the books Сonclusion

- 3. INTRODUCTION Bookkeeping is the recording of financial transactions Transactions include: Purchases; Sales; Receipts; Payments by an

- 4. METHODS OF BOOKKEEPING 1.Single entry system only income and expense accounts 2.Double-entry system requires posting (recording)

- 5. BOOKKEEPER is a person who records the day-to-day financial transactions of a business

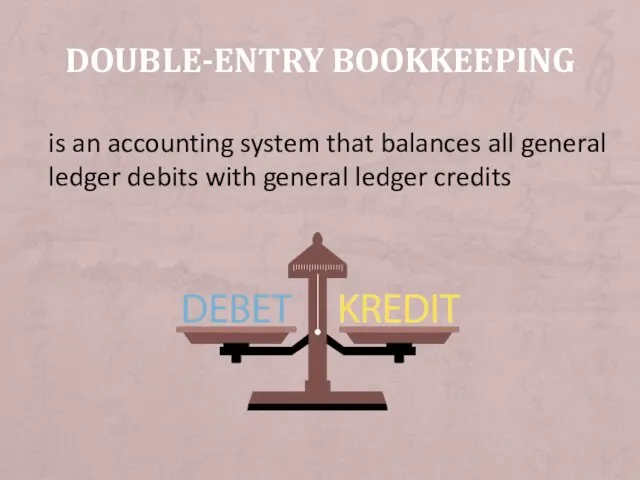

- 6. is an accounting system that balances all general ledger debits with general ledger credits DOUBLE-ENTRY BOOKKEEPING

- 7. Luca Pacioli invented the double-entry bookkeeping

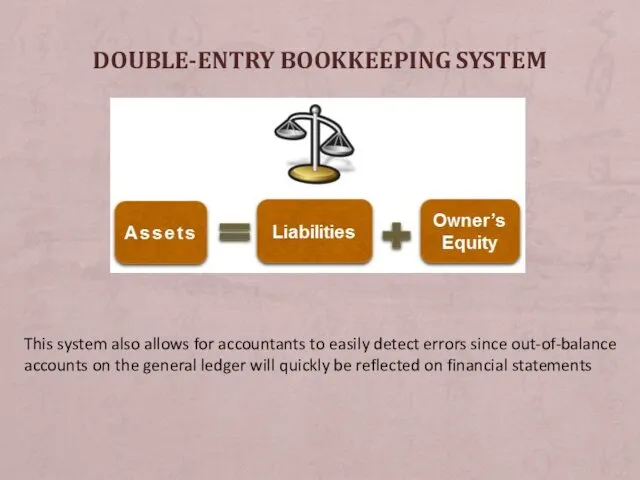

- 8. DOUBLE-ENTRY BOOKKEEPING SYSTEM This system also allows for accountants to easily detect errors since out-of-balance accounts

- 9. double-entry bookkeeping distorts the company’s cash account in the general ledger account because transactions are recorded

- 11. Скачать презентацию

PLAN

Introduction

Methods of bookkeeping

Double-entry bookkeeping

Day books and ledgers

Balancing the books

Сonclusion

PLAN

Introduction

Methods of bookkeeping

Double-entry bookkeeping

Day books and ledgers

Balancing the books

Сonclusion

INTRODUCTION

Bookkeeping is the recording of financial transactions

Transactions include:

Purchases;

Sales;

Receipts;

Payments by an individual

INTRODUCTION

Bookkeeping is the recording of financial transactions

Transactions include:

Purchases;

Sales;

Receipts;

Payments by an individual

METHODS OF BOOKKEEPING

1.Single entry system

only income and expense accounts

2.Double-entry system

requires posting

METHODS OF BOOKKEEPING

1.Single entry system

only income and expense accounts

2.Double-entry system

requires posting

BOOKKEEPER

is a person who records the day-to-day financial transactions of a

BOOKKEEPER

is a person who records the day-to-day financial transactions of a

is an accounting system that balances all general ledger debits with

is an accounting system that balances all general ledger debits with

Luca Pacioli invented the double-entry bookkeeping

Luca Pacioli invented the double-entry bookkeeping

DOUBLE-ENTRY BOOKKEEPING SYSTEM

This system also allows for accountants to easily detect

DOUBLE-ENTRY BOOKKEEPING SYSTEM

This system also allows for accountants to easily detect

double-entry bookkeeping distorts the company’s cash account in the general ledger

double-entry bookkeeping distorts the company’s cash account in the general ledger

Программа смешанного страхования жизни Гармония

Программа смешанного страхования жизни Гармония Подготовка документов для расчета стимулирующей надбавки для работников из числа профессорско-преподавательского состава

Подготовка документов для расчета стимулирующей надбавки для работников из числа профессорско-преподавательского состава Оборотные средства предприятия

Оборотные средства предприятия Методы расчета ставки капитализации

Методы расчета ставки капитализации Податок на додану вартість

Податок на додану вартість Центральний банк і грошово-кредитна політика. Правовий статус і функції НБУ

Центральний банк і грошово-кредитна політика. Правовий статус і функції НБУ Tengri bank

Tengri bank Финансовая грамотность

Финансовая грамотность Урок-игра по финансовой грамотости

Урок-игра по финансовой грамотости Формы и системы оплаты труда

Формы и системы оплаты труда Учет затрат на производство

Учет затрат на производство Идеи М.В. Попова. Банков нет.

Идеи М.В. Попова. Банков нет. Понятие временной нетрудоспособности. Виды пособий по временной нетрудоспособности

Понятие временной нетрудоспособности. Виды пособий по временной нетрудоспособности Сущность и функции финансов, их роль в системе денежных отношений

Сущность и функции финансов, их роль в системе денежных отношений Налог на доходы физических лиц (НДФЛ)

Налог на доходы физических лиц (НДФЛ) МодульКасса. Торговый эквайринг

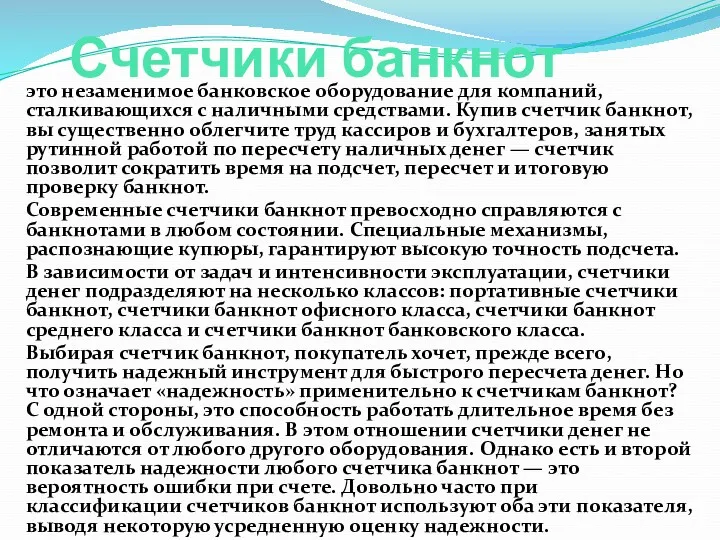

МодульКасса. Торговый эквайринг Счетчики банкнот, пневмопочта

Счетчики банкнот, пневмопочта Страховые формальности. Страхование в туризме. Виды страховых программ

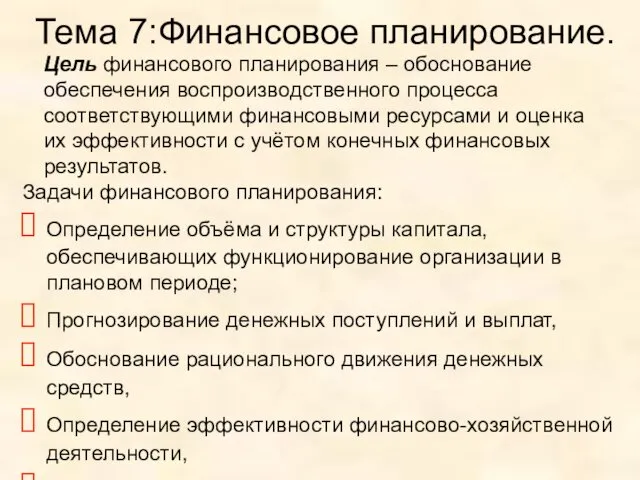

Страховые формальности. Страхование в туризме. Виды страховых программ Финансовое планирование

Финансовое планирование Первые шаги к финансовому успеху подростка. Повышение осознанности и ответственности в финансовых вопросах

Первые шаги к финансовому успеху подростка. Повышение осознанности и ответственности в финансовых вопросах Организация и способы ведения налогового учета на предприятии ООО ПКФ Монтажник

Организация и способы ведения налогового учета на предприятии ООО ПКФ Монтажник Банки. Банковская система

Банки. Банковская система Поддержка промышленности Московской области

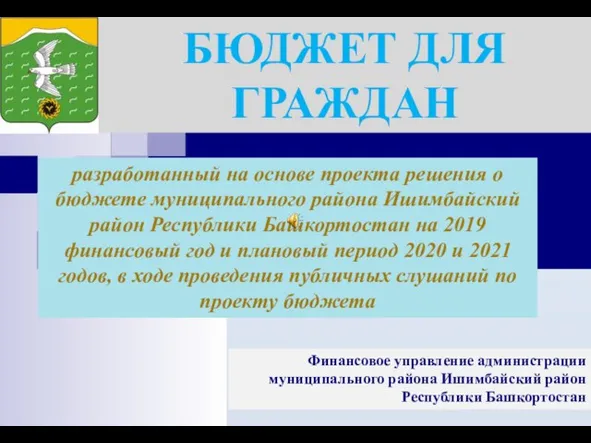

Поддержка промышленности Московской области Бюджет для граждан на 2019-2021гг

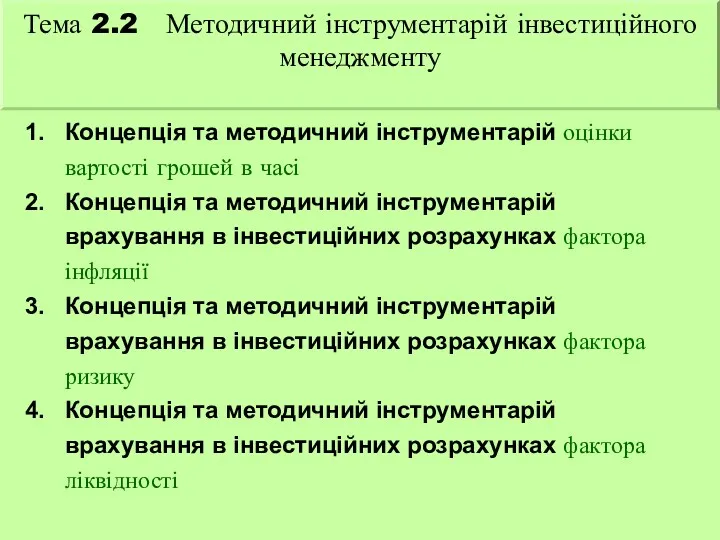

Бюджет для граждан на 2019-2021гг Методичний інструментарій інвестиційного менеджменту. (Тема 2.2)

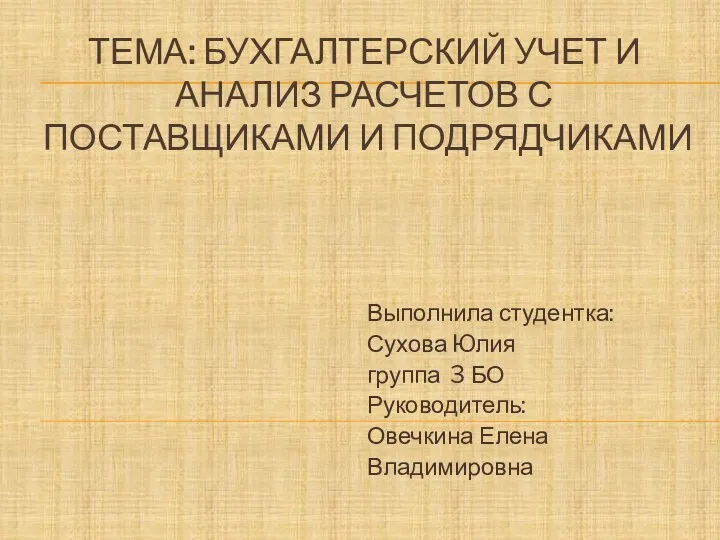

Методичний інструментарій інвестиційного менеджменту. (Тема 2.2) Бухгалтерский учет и анализ расчетов с поставщиками и подрядчиками

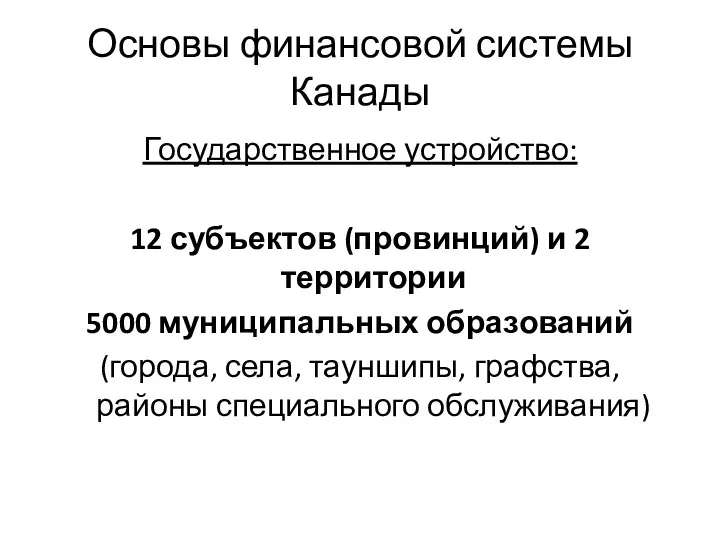

Бухгалтерский учет и анализ расчетов с поставщиками и подрядчиками Основы финансовой системы Канады

Основы финансовой системы Канады Основы бизнес-аналитики. Лекция 5. Цепочки формирования добавленной ценности

Основы бизнес-аналитики. Лекция 5. Цепочки формирования добавленной ценности