- Calculation of costs for production

Содержание

- 2. Plan Introduction I. Cost calculation II. costing production III. cost effectiveness assessment Conclusion LIterature

- 3. Introduction By way of inclusion in the cost of all costs are divided into direct and

- 4. Enterprise costs Enterprise coxts straight lines invoices can be attributed to a specific product costs while

- 5. Process-based costing is one of the methods for calculating costs in management accounting, cost accounting and

- 6. Manufacturers direct costs raw materials fuel and energy semi-finished products and components salary OPP social contributions

- 7. overheаd manufacturing managerial general business trading

- 8. Definition of indirect costs

- 9. types of cost shop floor Factory full production full commercial

- 10. cost of goods sold and services rendered ( 2017-2018) 1square (trillion kzt) electricity, gas supply 0.35-0.39

- 11. Conclusion Initially, a list of all operations in certain departments of the enterprise, which are performed

- 12. Literature Handbook of economist-mechanical engineer Izd.2 (1977) - [c.177, c.178, c.202] Handbook of economist engineering company

- 14. Скачать презентацию

Plan

Introduction

I. Cost calculation

II. costing production

III. cost effectiveness assessment

Conclusion

LIterature

Plan

Introduction

I. Cost calculation

II. costing production

III. cost effectiveness assessment

Conclusion

LIterature

Introduction

By way of inclusion in the cost of all costs are

Introduction

By way of inclusion in the cost of all costs are

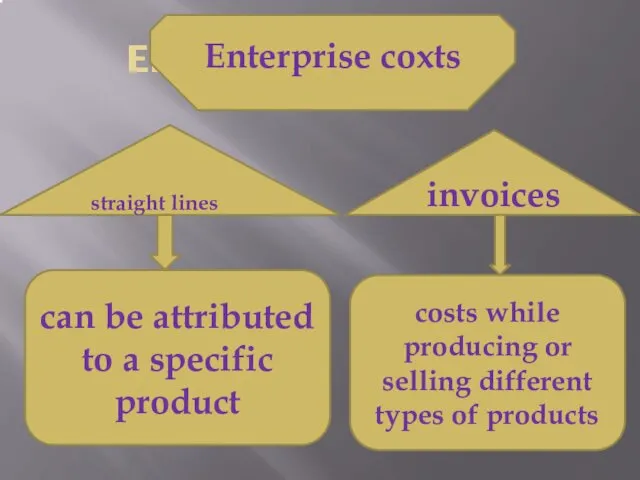

Enterprise costs

Enterprise coxts

straight lines

invoices

can be attributed to a specific product

costs

Enterprise costs

Enterprise coxts

straight lines

invoices

can be attributed to a specific product

costs

Process-based costing is one of the methods for calculating costs in

Process-based costing is one of the methods for calculating costs in

Manufacturers direct costs

raw materials

fuel and energy

semi-finished products and components

salary OPP

social contributions

Manufacturers direct costs

raw materials

fuel and energy

semi-finished products and components

salary OPP

social contributions

overheаd

manufacturing

managerial

general business

trading

overheаd

manufacturing

managerial

general business

trading

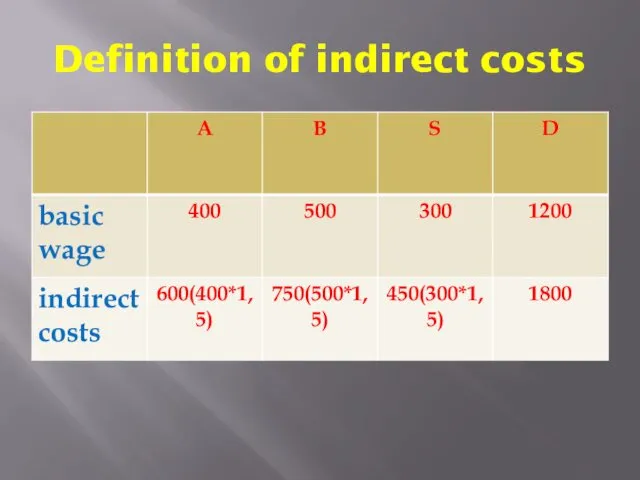

Definition of indirect costs

Definition of indirect costs

types of cost

shop floor

Factory

full production

full commercial

types of cost

shop floor

Factory

full production

full commercial

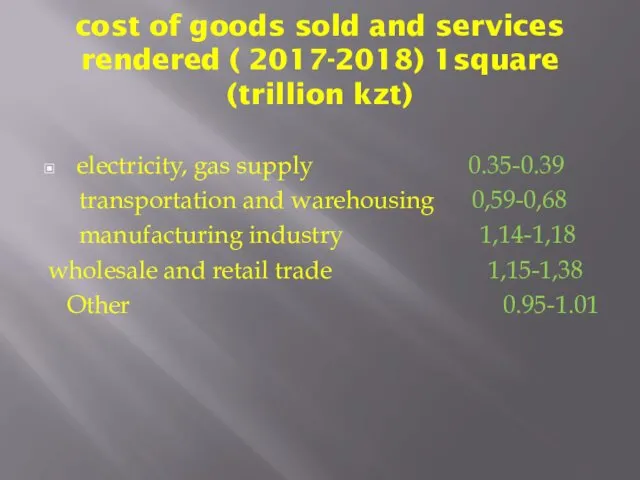

cost of goods sold and services rendered ( 2017-2018) 1square (trillion

cost of goods sold and services rendered ( 2017-2018) 1square (trillion

Conclusion

Initially, a list of all operations in certain departments of the

Conclusion

Initially, a list of all operations in certain departments of the

Literature

Handbook of economist-mechanical engineer Izd.2 (1977) - [c.177, c.178, c.202]

Handbook of

Literature

Handbook of economist-mechanical engineer Izd.2 (1977) - [c.177, c.178, c.202]

Handbook of

Актуальные проблемы налогового контроля в РФ

Актуальные проблемы налогового контроля в РФ Анализ капитальных вложений

Анализ капитальных вложений Банк қызметінің құқықтық негіздері

Банк қызметінің құқықтық негіздері Методика SIGMA

Методика SIGMA Фонд развития промышленности Республики Карелия

Фонд развития промышленности Республики Карелия Бизнес-планирование инновационных проектов

Бизнес-планирование инновационных проектов Лекция 16. Японские свечи

Лекция 16. Японские свечи Доходность и риск финансовой операции

Доходность и риск финансовой операции Денежная система

Денежная система Оценка гудвилла

Оценка гудвилла Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа

Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа Аналіз джерел формування капіталу. Лекція 5

Аналіз джерел формування капіталу. Лекція 5 Управление стоимостью компании

Управление стоимостью компании Вклад Альянса ФМС УрФО в развитие местных сообществ

Вклад Альянса ФМС УрФО в развитие местных сообществ Оборотные средства гостиничного предприятия

Оборотные средства гостиничного предприятия Налог на доходы физических лиц (НДФЛ)

Налог на доходы физических лиц (НДФЛ) Семейный бюджет

Семейный бюджет Концептуальні основи оподаткування

Концептуальні основи оподаткування Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3)

Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3) Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1)

Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1) Activity-Based Costing and Activity-Based Management

Activity-Based Costing and Activity-Based Management Президентские гранты для ННО

Президентские гранты для ННО Салық салу саласындағы мемлекеттік басқару түсінігі,маңызы,міндеттері

Салық салу саласындағы мемлекеттік басқару түсінігі,маңызы,міндеттері Региональная бюджетная система

Региональная бюджетная система Налог на добавленную стоимость

Налог на добавленную стоимость Такафул – исламское страхование

Такафул – исламское страхование ТОО КазМунайГаз-Сервис. Активы компании

ТОО КазМунайГаз-Сервис. Активы компании Фінансові інвестиції

Фінансові інвестиції