- International financial reporting standards

Содержание

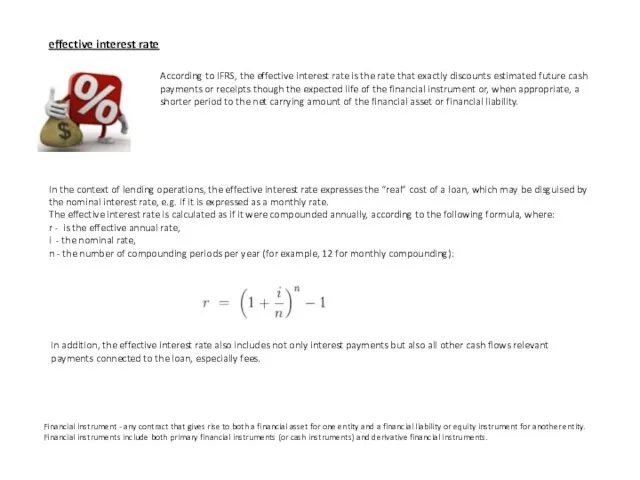

- 2. effective interest rate According to IFRS, the effective interest rate is the rate that exactly discounts

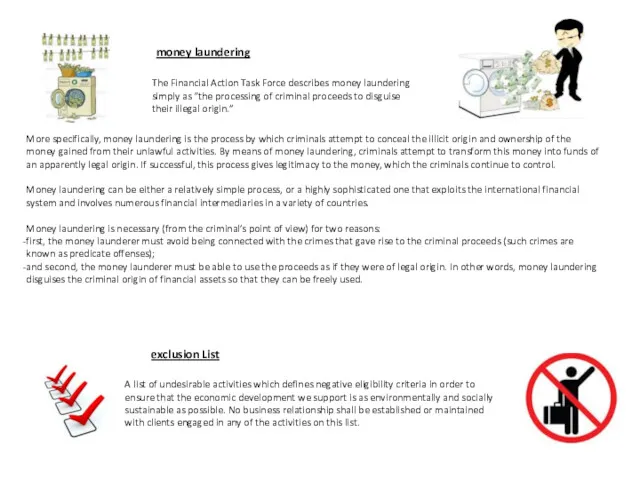

- 3. The Financial Action Task Force describes money laundering simply as “the processing of criminal proceeds to

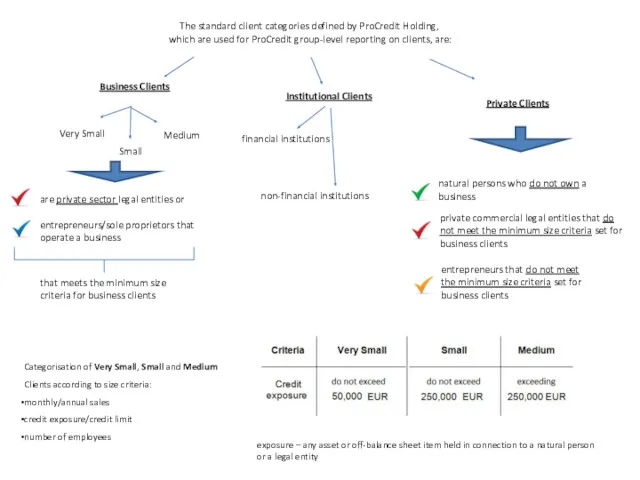

- 4. The standard client categories defined by ProCredit Holding, which are used for ProCredit group-level reporting on

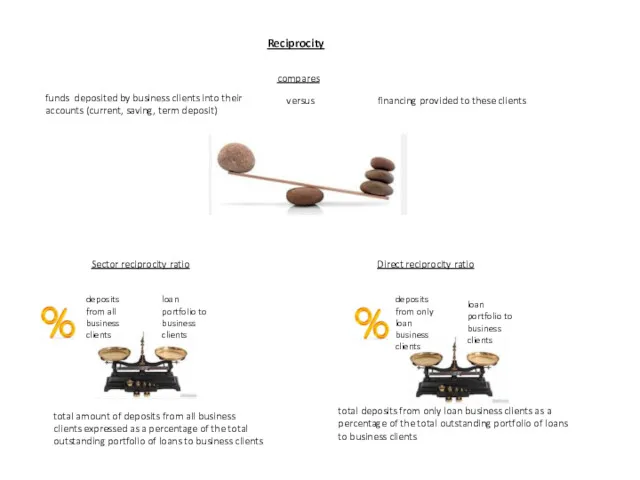

- 5. Reciprocity compares funds deposited by business clients into their accounts (current, saving, term deposit) versus financing

- 6. Business continuity (BC) The bank’s ability to strategically and tactically plan for and respond to business

- 7. 24/7 Zone (= self-service area) The 24/7 Zone is a part of each Service Point where

- 8. regulatory capital adequacy ratio A regulatory capital adequacy ratio is a measure of a bank’s or

- 9. cost/income ratio Measure of cost efficiency which sets operating expenses in relation to operating income before

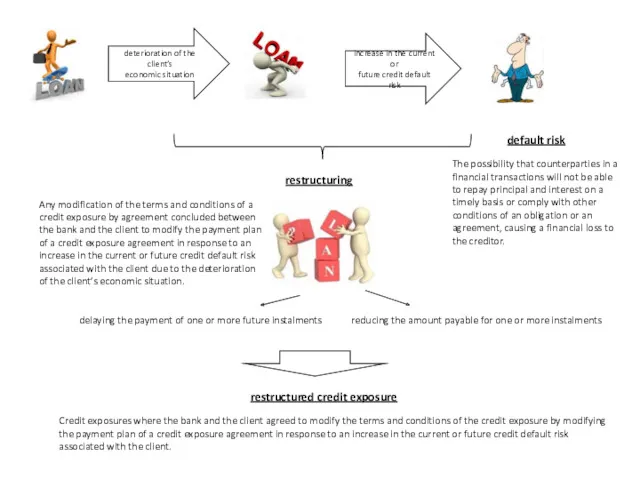

- 10. default risk The possibility that counterparties in a financial transactions will not be able to repay

- 11. refinancing Disbursement of a new loan that serves fully or partially to repay one or more

- 12. Impairment loss The bank obtains information indicating that the value of the credit exposure may have

- 13. Allowance for impairment losses on loans and advances to customers Loan loss provisions set aside in

- 14. coverage ratio total allowance for impairment / volume of PAR 30 (or PAR 90)/ portfolio at

- 15. Credit limit the maximum overall credit exposure the bank decides to have towards a certain client

- 16. Letter of credit An irrevocable (cannot be cancelled) undertaking on the part of the issuing bank

- 17. Letter of guarantee / Bank guarantee The difference between letters of credit and letters of guarantee:

- 18. Credit risk Refers to the danger that the other party to a credit transaction (the counterparty)

- 19. Document Hierarchy & Organisation group strategies outline general principles and development plans that underpin the ProCredit

- 20. Green finance (Green credit products) all financing activities for investments in: Energy efficiency (EE) investments Renewable

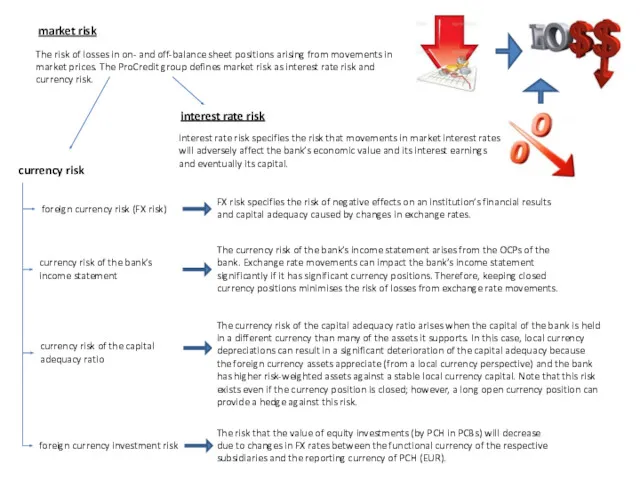

- 21. currency risk foreign currency risk (FX risk) FX risk specifies the risk of negative effects on

- 22. Currency position A currency position is determined by comparing all assets and liabilities in each currency,

- 23. translation reserve The translation reserve is the group-level currency exchange reserve on capital. It consists of

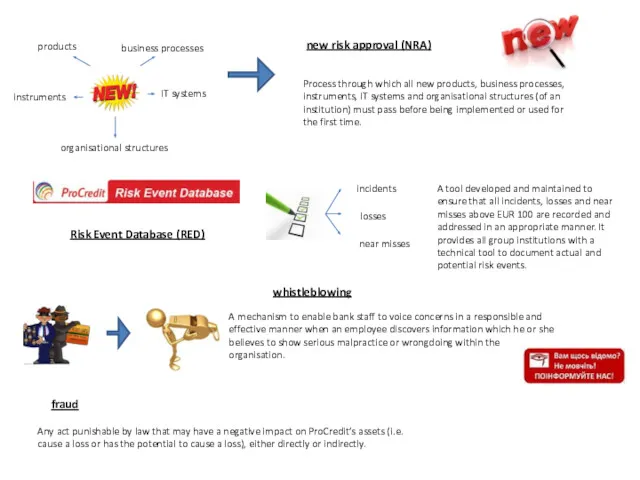

- 24. new risk approval (NRA) products business processes instruments IT systems organisational structures Process through which all

- 25. funding Funding instruments are usually financial instruments with an initial maturity of one year or more,

- 26. Management Board Human Resources committee annual staff conversation the group of managers appointed by of the

- 27. salary structure a set of salary ranges that are defined for all key positions in the

- 28. ProCredit outlets Embedded service point is in the same building as a Service Centre or a

- 29. floor manager A client adviser who is on duty in each 24/7 Zone, ready to actively

- 30. Public information - information that is intended for disclosure and distribution to the public disclosure refers

- 31. Audit report a written report on the outcome of an audit, that contains all findings and

- 32. Risk assessments an analysis on an annual basis of the operational and fraud risks inherent to

- 33. Operational risk the risk of loss resulting from inadequate or failed: internal processes from people and

- 35. Скачать презентацию

effective interest rate

According to IFRS, the effective interest rate is the

effective interest rate

According to IFRS, the effective interest rate is the

The Financial Action Task Force describes money laundering simply as “the

The Financial Action Task Force describes money laundering simply as “the

The standard client categories defined by ProCredit Holding,

which are used

The standard client categories defined by ProCredit Holding,

which are used

Reciprocity

compares

funds deposited by business clients into their accounts (current, saving, term

Reciprocity

compares

funds deposited by business clients into their accounts (current, saving, term

Business continuity (BC)

The bank’s ability to strategically and tactically plan for

Business continuity (BC)

The bank’s ability to strategically and tactically plan for

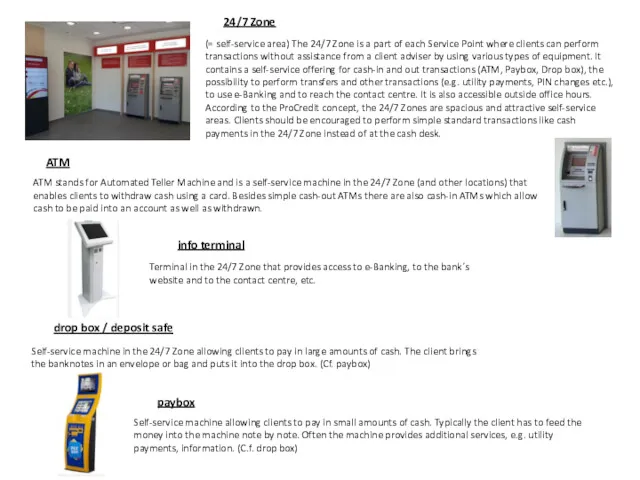

24/7 Zone

(= self-service area) The 24/7 Zone is a part of

24/7 Zone

(= self-service area) The 24/7 Zone is a part of

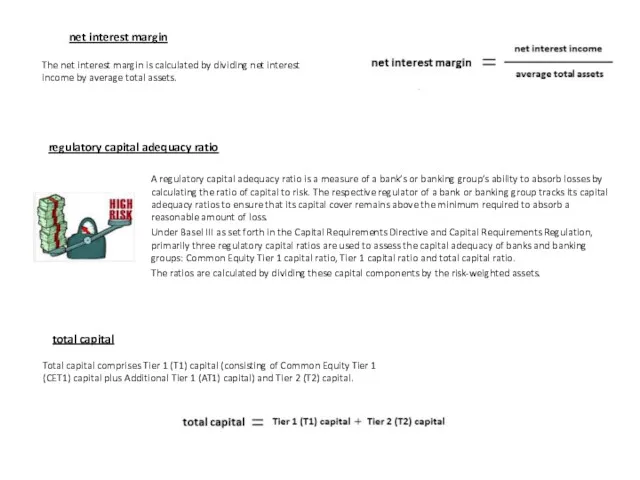

regulatory capital adequacy ratio

A regulatory capital adequacy ratio is a measure

regulatory capital adequacy ratio

A regulatory capital adequacy ratio is a measure

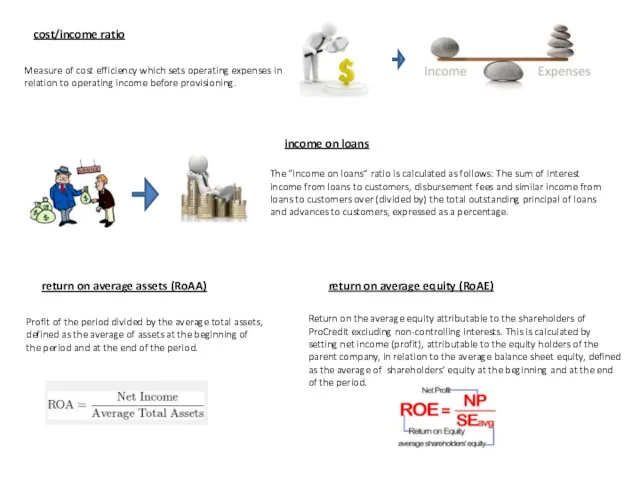

cost/income ratio

Measure of cost efficiency which sets operating expenses in relation

cost/income ratio

Measure of cost efficiency which sets operating expenses in relation

default risk

The possibility that counterparties in a financial transactions will not

default risk

The possibility that counterparties in a financial transactions will not

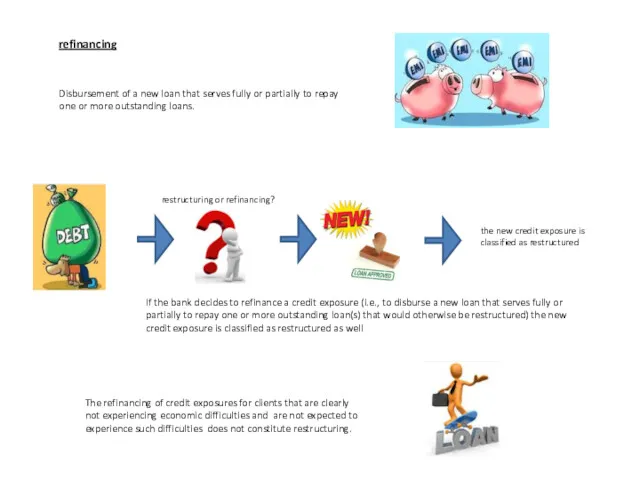

refinancing

Disbursement of a new loan that serves fully or partially to

refinancing

Disbursement of a new loan that serves fully or partially to

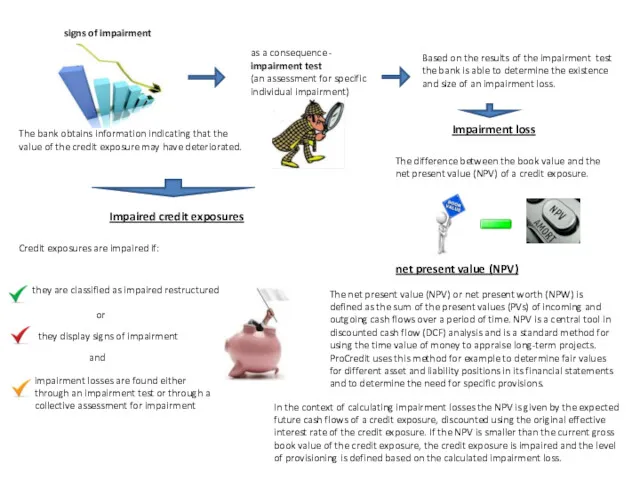

Impairment loss

The bank obtains information indicating that the value of the

Impairment loss

The bank obtains information indicating that the value of the

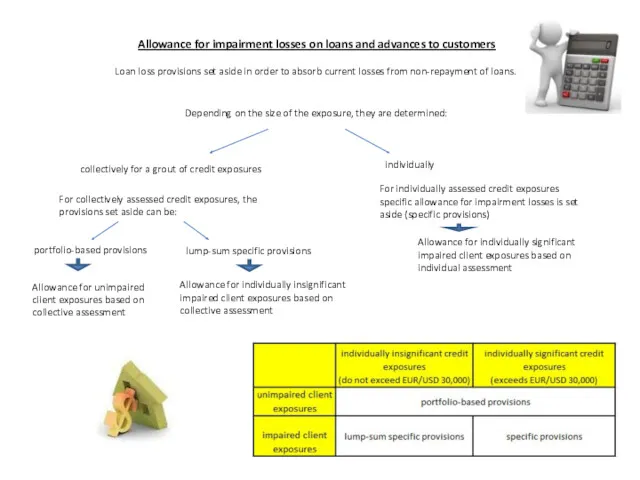

Allowance for impairment losses on loans and advances to customers

Loan

Allowance for impairment losses on loans and advances to customers

Loan

coverage ratio

total allowance for impairment / volume of PAR 30

coverage ratio

total allowance for impairment / volume of PAR 30

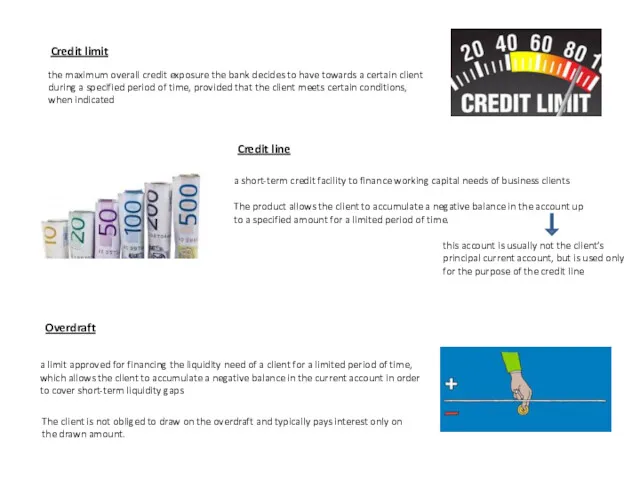

Credit limit

the maximum overall credit exposure the bank decides to have

Credit limit

the maximum overall credit exposure the bank decides to have

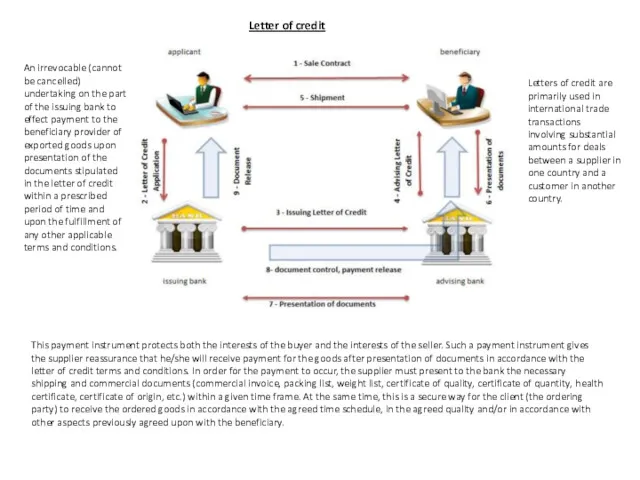

Letter of credit

An irrevocable (cannot be cancelled) undertaking on the part

Letter of credit

An irrevocable (cannot be cancelled) undertaking on the part

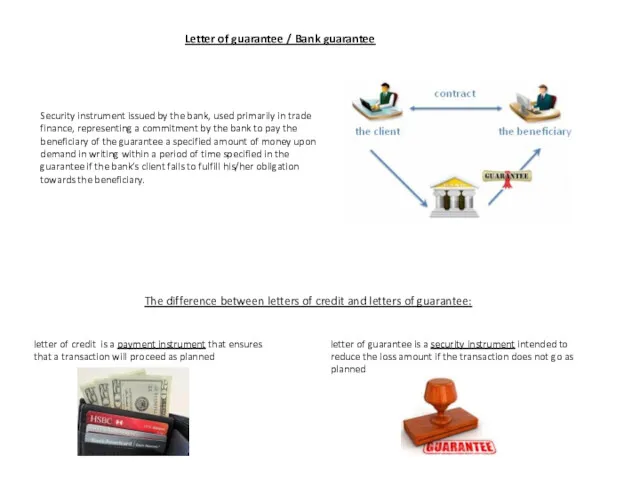

Letter of guarantee / Bank guarantee

The difference between letters of credit

Letter of guarantee / Bank guarantee

The difference between letters of credit

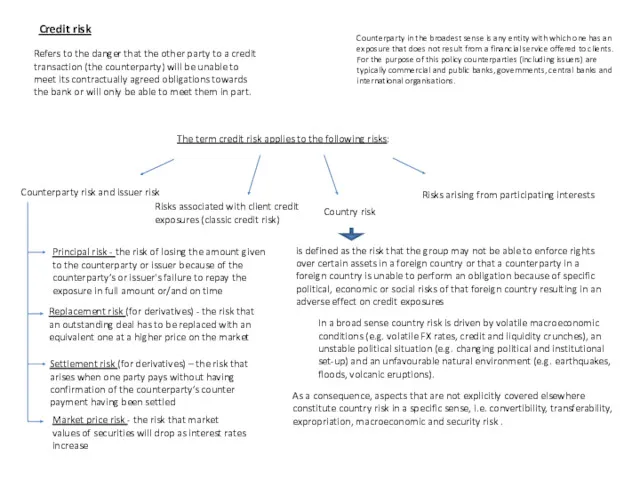

Credit risk

Refers to the danger that the other party to

Credit risk

Refers to the danger that the other party to

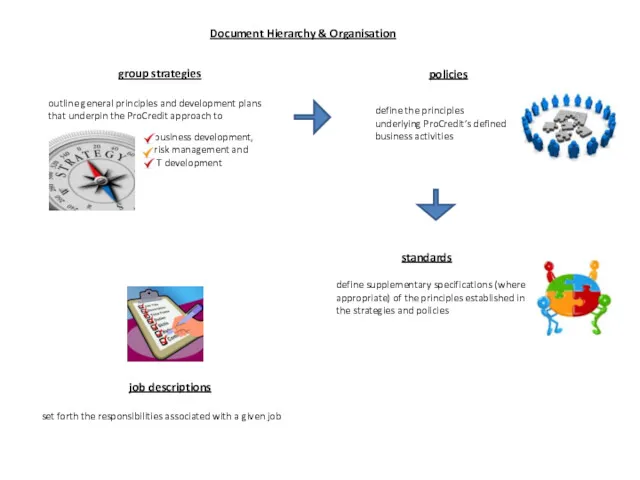

Document Hierarchy & Organisation

group strategies

outline general principles and development plans

Document Hierarchy & Organisation

group strategies

outline general principles and development plans

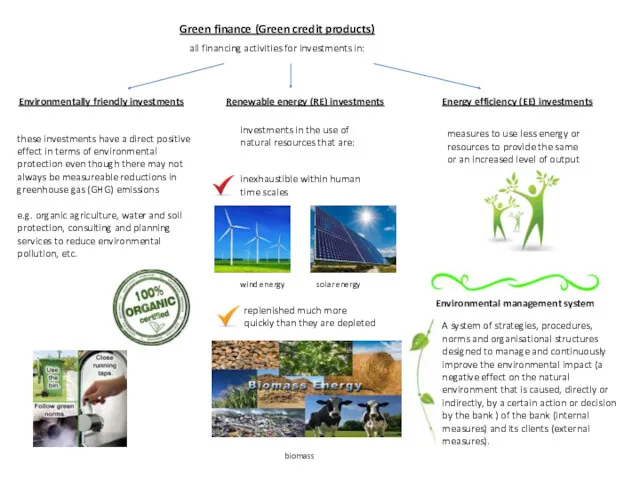

Green finance (Green credit products)

all financing activities for investments in:

Energy efficiency

Green finance (Green credit products)

all financing activities for investments in:

Energy efficiency

currency risk

foreign currency risk (FX risk)

FX risk specifies the risk of

currency risk

foreign currency risk (FX risk)

FX risk specifies the risk of

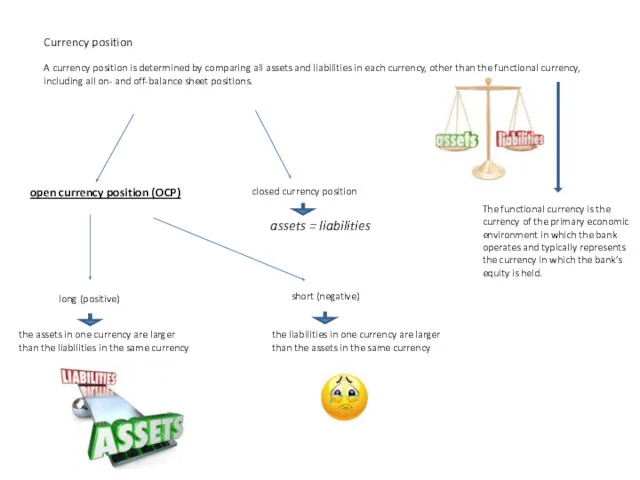

Currency position

A currency position is determined by comparing all assets and

Currency position

A currency position is determined by comparing all assets and

translation reserve

The translation reserve is the group-level currency exchange reserve

translation reserve

The translation reserve is the group-level currency exchange reserve

new risk approval (NRA)

products

business processes

instruments

IT systems

organisational structures

Process through which all

new risk approval (NRA)

products

business processes

instruments

IT systems

organisational structures

Process through which all

funding

Funding instruments are usually financial instruments with an initial maturity

funding

Funding instruments are usually financial instruments with an initial maturity

Management Board

Human Resources committee

annual staff conversation

the group of managers

appointed by of

Management Board

Human Resources committee

annual staff conversation

the group of managers

appointed by of

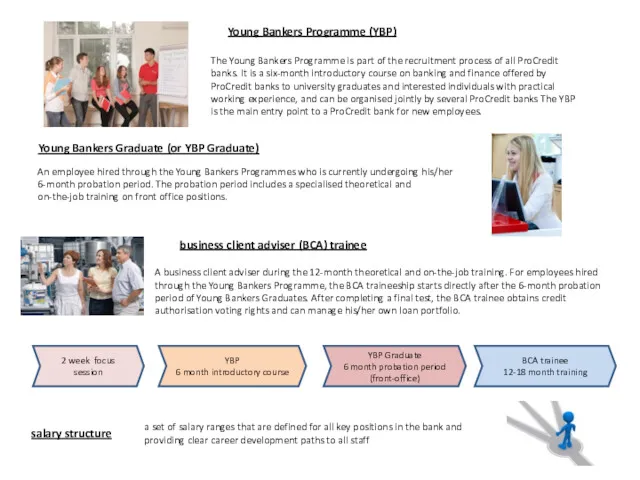

salary structure

a set of salary ranges that are defined for all

salary structure

a set of salary ranges that are defined for all

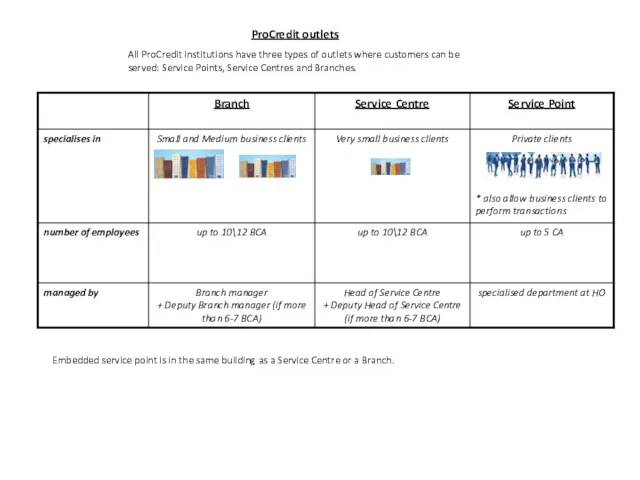

ProCredit outlets

Embedded service point is in the same building as a

ProCredit outlets

Embedded service point is in the same building as a

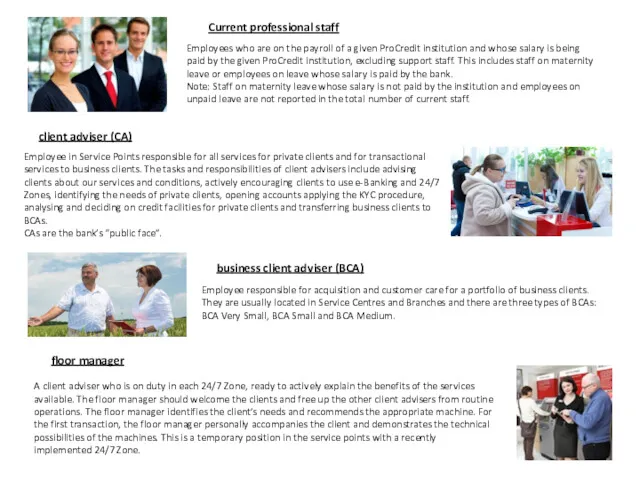

floor manager

A client adviser who is on duty in each 24/7

floor manager

A client adviser who is on duty in each 24/7

Public information

- information that is intended for disclosure and distribution to

Public information

- information that is intended for disclosure and distribution to

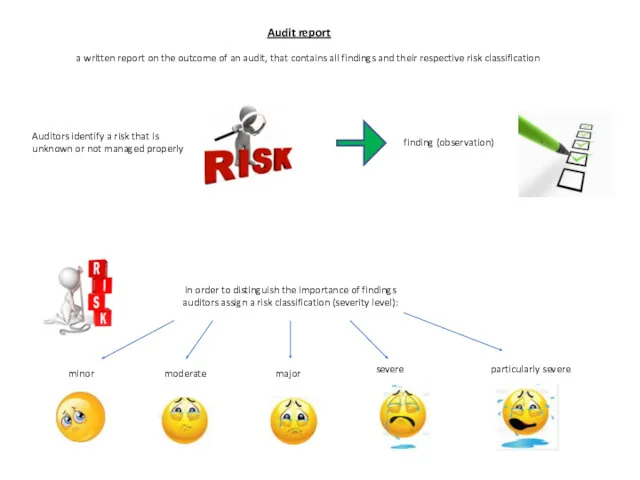

Audit report

a written report on the outcome of an audit, that

Audit report

a written report on the outcome of an audit, that

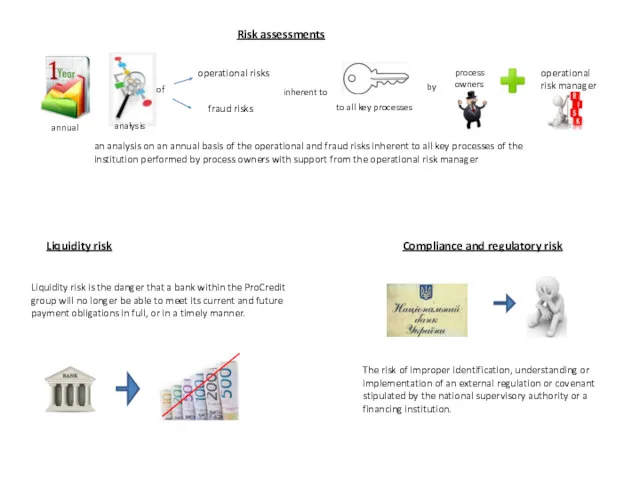

Risk assessments

an analysis on an annual basis of the operational

Risk assessments

an analysis on an annual basis of the operational

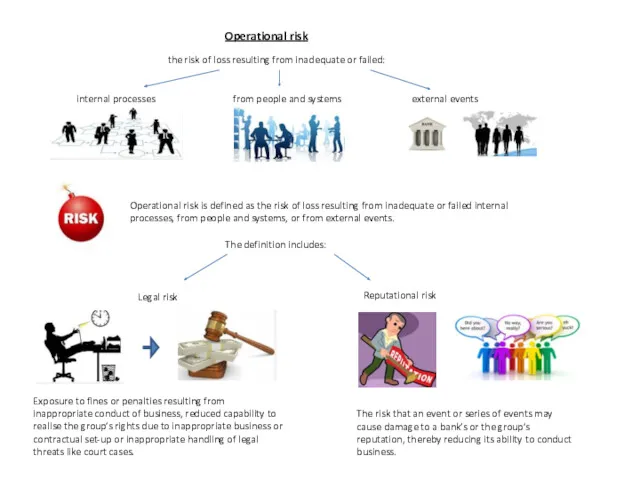

Operational risk

the risk of loss resulting from inadequate or failed:

internal processes

from

Operational risk

the risk of loss resulting from inadequate or failed:

internal processes

from

Фінансовий аналіз діяльності комерційних банків

Фінансовий аналіз діяльності комерційних банків Государственная программа о социальной защите и содействии занятости населения на 2016 – 2020 годы

Государственная программа о социальной защите и содействии занятости населения на 2016 – 2020 годы Преимущества зарплатной карты ВТБ. Для работников РЖД

Преимущества зарплатной карты ВТБ. Для работников РЖД Анализ состояния и эффективности использования основных средств, на примере ООО Камапроминвест

Анализ состояния и эффективности использования основных средств, на примере ООО Камапроминвест 05

05 Планирование и калькулирование затрат

Планирование и калькулирование затрат Финансовый результат деятельности предприятия

Финансовый результат деятельности предприятия Денежные единицы стран мира

Денежные единицы стран мира Бухгалтерский учет и аудит расчетов с поставщиками и подрядчиками на примере ООО ОП Статус-2

Бухгалтерский учет и аудит расчетов с поставщиками и подрядчиками на примере ООО ОП Статус-2 Бухгалтерский баланс

Бухгалтерский баланс Platinum Bank. Банк и банковские продукты

Platinum Bank. Банк и банковские продукты Программы регионального финансирования субъектов малого и среднего предпринимательства

Программы регионального финансирования субъектов малого и среднего предпринимательства Инвестиционная деятельность. Факторы стоимости. Лекция 5 (1)

Инвестиционная деятельность. Факторы стоимости. Лекция 5 (1) Банківська система

Банківська система Моделі аналізу беззбитковості діяльності. Тема 3

Моделі аналізу беззбитковості діяльності. Тема 3 Бюджетная система Китая, Франции и Великобритании

Бюджетная система Китая, Франции и Великобритании Программа поддержки начинающих фермеров в Республике Мордовия

Программа поддержки начинающих фермеров в Республике Мордовия Предложение по накопительному страхованию жизни

Предложение по накопительному страхованию жизни Кәсіпорында еңбекті ұйымдастыру және еңбек ақы төлеу

Кәсіпорында еңбекті ұйымдастыру және еңбек ақы төлеу Инвестициялық нарық

Инвестициялық нарық Фундаментальный анализ финансовых рынков

Фундаментальный анализ финансовых рынков Региональные финансы зарубежных стран

Региональные финансы зарубежных стран Особенности формирования национальной валютной системы Китая

Особенности формирования национальной валютной системы Китая Оценка эффективности инвестиционных проектов

Оценка эффективности инвестиционных проектов Базельские соглашения и регулирование банковских рисков

Базельские соглашения и регулирование банковских рисков Семей қаласының банктері

Семей қаласының банктері Министерство финансов Российской Федерации

Министерство финансов Российской Федерации Семейный бюджет. Доходы и расходы

Семейный бюджет. Доходы и расходы