- Tax update for Аdvisors

Содержание

- 2. Agenda 2010 tax changes Top 10 Tax Filing Tips (2009 returns) TFSA update U.S estate tax

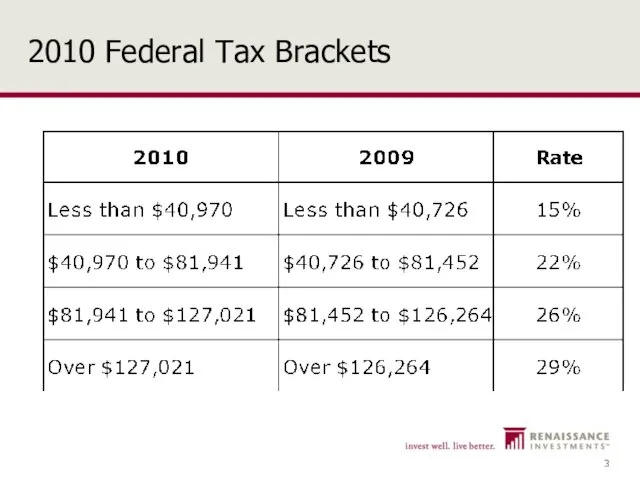

- 3. 2010 Federal Tax Brackets

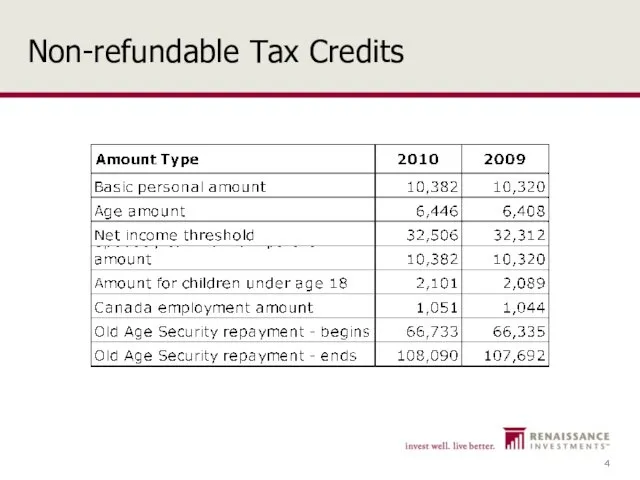

- 4. Non-refundable Tax Credits

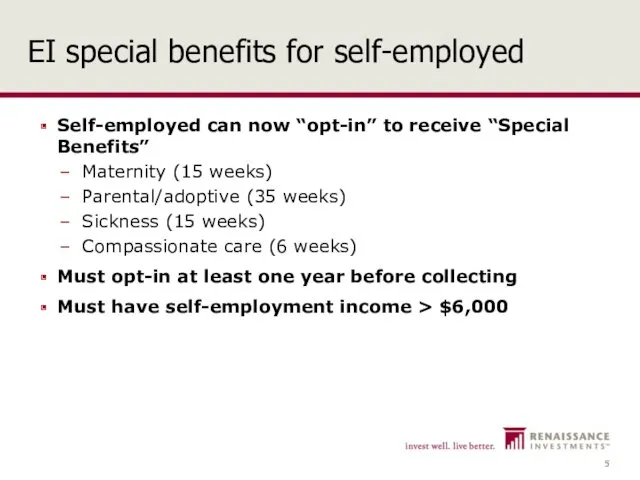

- 5. EI special benefits for self-employed Self-employed can now “opt-in” to receive “Special Benefits” Maternity (15 weeks)

- 6. Interest deductibility update “Borrowed for the purpose of earning income” Stocks that don’t pay any/sufficient dividends?

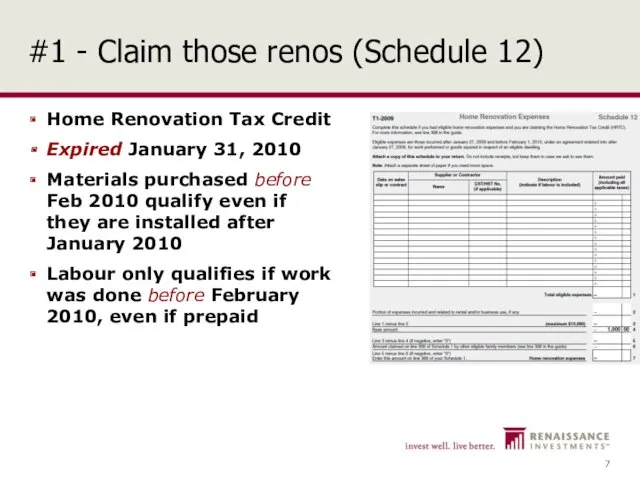

- 7. #1 - Claim those renos (Schedule 12) Home Renovation Tax Credit Expired January 31, 2010 Materials

- 8. #2 – Split that pension (Form T1032) Pension income? Before age 65? Regular monthly pension from

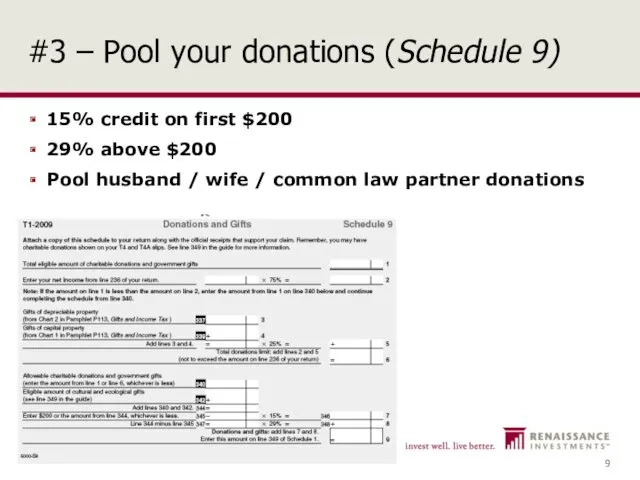

- 9. #3 – Pool your donations (Schedule 9) 15% credit on first $200 29% above $200 Pool

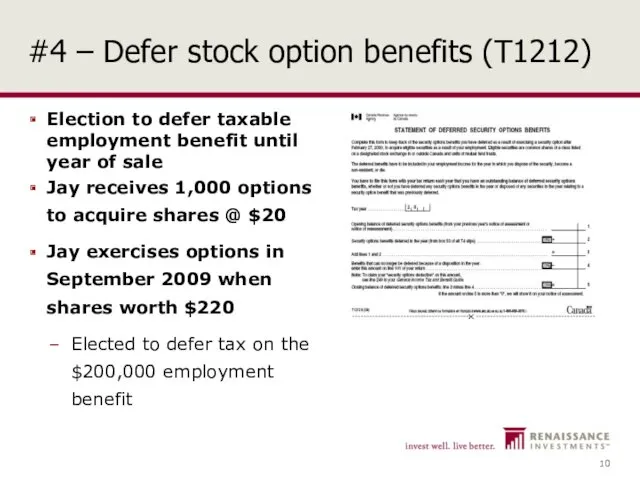

- 10. #4 – Defer stock option benefits (T1212) Election to defer taxable employment benefit until year of

- 11. Relief for underwater stock options Share crashes – now worth $10/share or $10,000 Jay sells Gets

- 12. Relief for underwater stock options BUDGET 2010: New rule – special tax equal to proceeds of

- 13. Elimination of deferral & remittance requirement Effective for exercises after March 4, 2010 – 4 pm

- 14. #5 – Write off the kids! Child amount - $2,089/child Non-refundable credit (federal – 15%) Children’s

- 15. #6 – Report offshore stash (T1135) Foreign income verification statement More than $100,000 (CDN) Funds in

- 16. #7 – Claim legal fees Loss of employment in 2009 Legal fees paid to: Collect /

- 17. #8 – File on time April 30 / June 15 5% of amount owing + 1%/month

- 18. #9 – Report all your income Missing receipt? File on time and estimate missing item Penalty

- 19. #10 - Avoid that refund Reduce tax at source Reduce OAS clawback at source

- 20. Plan NOT to Get a Refund! the euphoria of getting a tax refund that lasts only

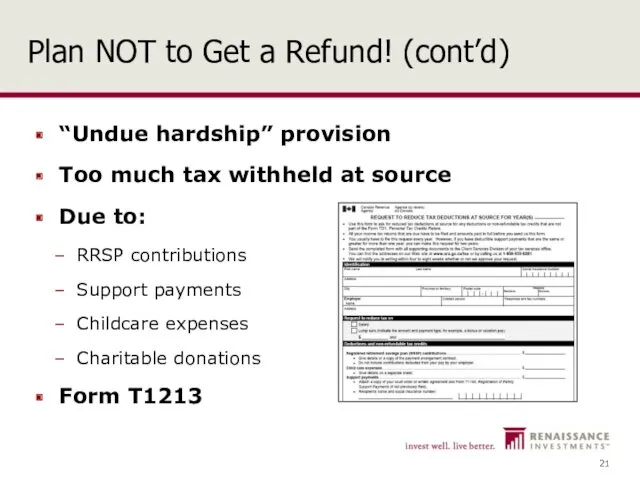

- 21. Plan NOT to Get a Refund! (cont’d) “Undue hardship” provision Too much tax withheld at source

- 22. Capital gain in 2009 – OAS Client will pay back all 2009 OAS because large capital

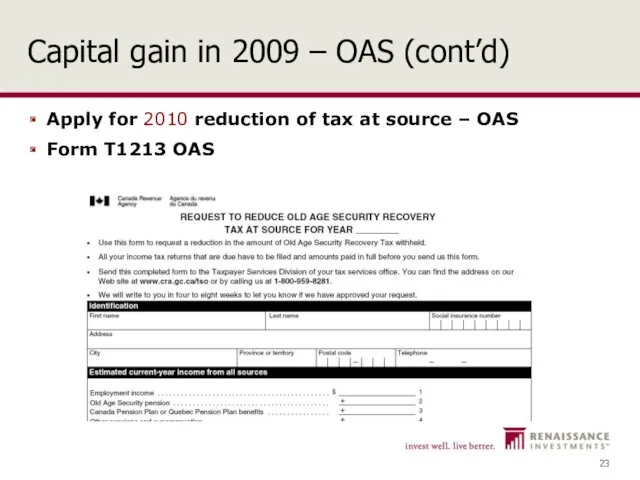

- 23. Capital gain in 2009 – OAS (cont’d) Apply for 2010 reduction of tax at source –

- 24. Miscellaneous tax update TFSA update State of US estate tax Cases of interest

- 25. TFSA carry-forward room $10,000 opportunity $20,000 opportunity (spouses/partners) No attribution

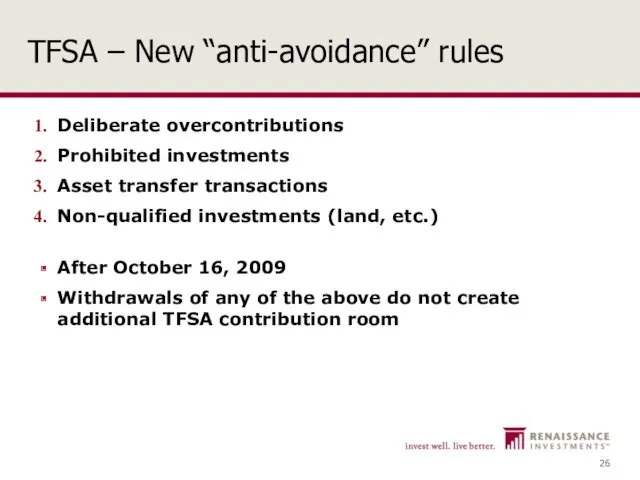

- 26. TFSA – New “anti-avoidance” rules Deliberate overcontributions Prohibited investments Asset transfer transactions Non-qualified investments (land, etc.)

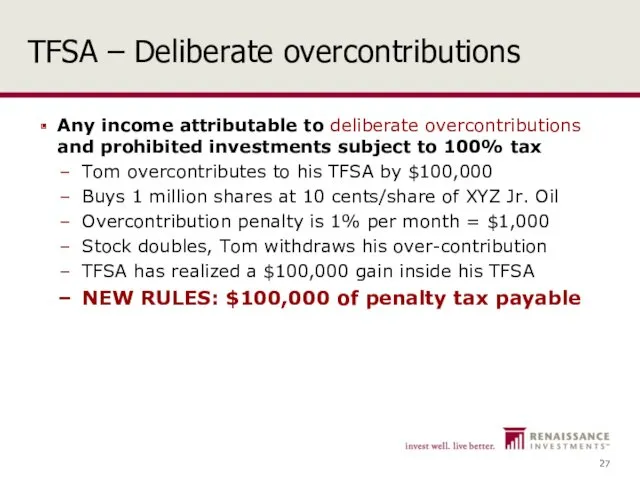

- 27. TFSA – Deliberate overcontributions Any income attributable to deliberate overcontributions and prohibited investments subject to 100%

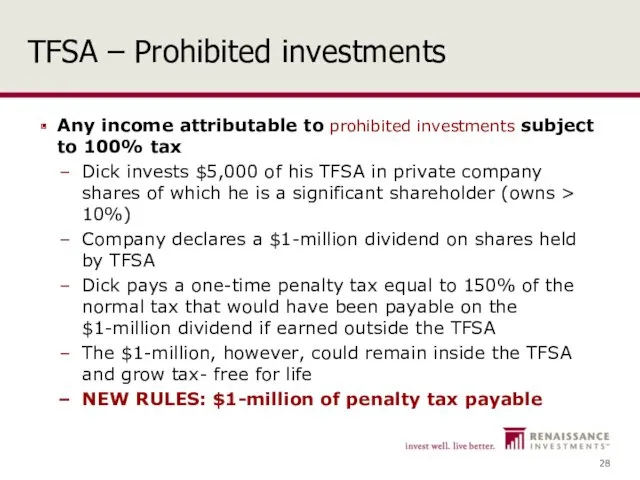

- 28. TFSA – Prohibited investments Any income attributable to prohibited investments subject to 100% tax Dick invests

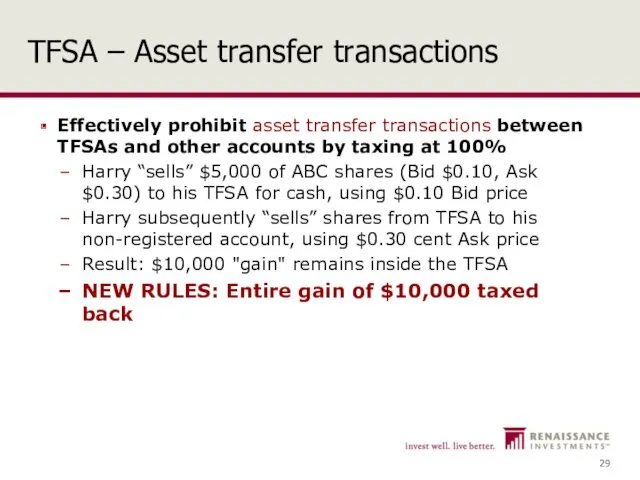

- 29. TFSA – Asset transfer transactions Effectively prohibit asset transfer transactions between TFSAs and other accounts by

- 30. U.S. Estate Tax Update Assume non-resident, non-U.S. citizen (“ALIEN”) U.S. situs property: U.S. real estate U.S.

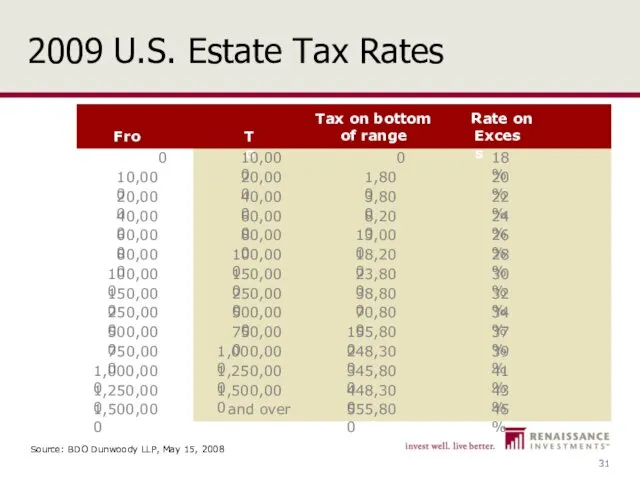

- 31. 2009 U.S. Estate Tax Rates Source: BDO Dunwoody LLP, May 15, 2008

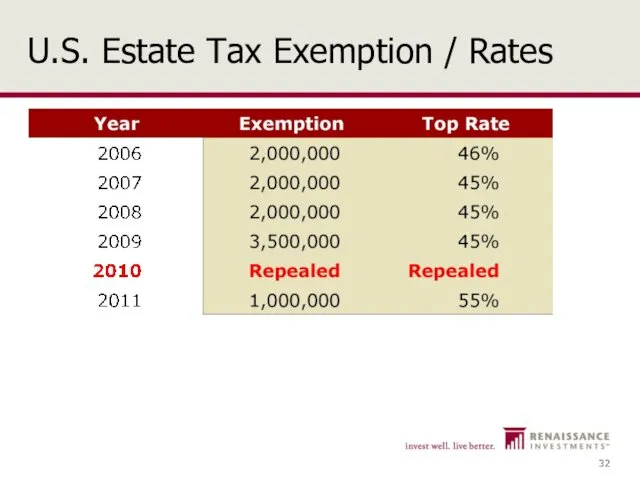

- 32. U.S. Estate Tax Exemption / Rates

- 33. Where are we now? December 2009 – U.S. House of Representatives approved Bill to extend 45%

- 34. Where are we now?

- 35. Garron Family Trust (2009) Barbados trusts $450 million capital gain Residency of trusts IT 447 “Residence

- 36. Marechaux (2009) Leveraged donation tax shelter Produces "return on donation of up to 62.4%” Supported by

- 37. Innovative Installation Inc. (2009) Innovative borrowed $220,000 from RBC “Key person” life insurance purchased on founder’s

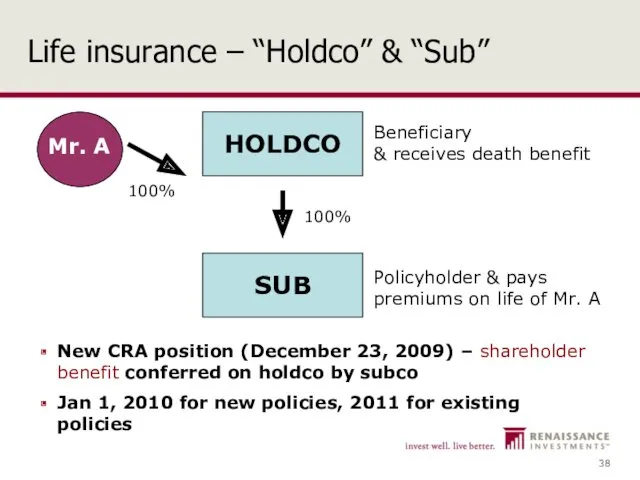

- 38. Life insurance – “Holdco” & “Sub” New CRA position (December 23, 2009) – shareholder benefit conferred

- 39. Bilodeau (2009) Financial advisor purchased two $1 million UL policies Life insurance commissions ($43,000) on advisor’s

- 40. Li (2009) Financial advisor deducted various employment expenses: Salary to assistant/husband ($14,000) Form T2200 inconsistencies Commissions

- 41. Rupprecht (2009) Financial advisor deducted: Costco membership fees Clothing ($8,400 in “suitable clothing”) RRSP penalties for

- 42. Renaissance Funds – Advisor site

- 43. Thank You This material was prepared for investment professionals only and is not for public distribution.

- 45. Скачать презентацию

Agenda

2010 tax changes

Top 10 Tax Filing Tips (2009 returns)

TFSA update

U.S estate

Agenda

2010 tax changes

Top 10 Tax Filing Tips (2009 returns)

TFSA update

U.S estate

2010 Federal Tax Brackets

2010 Federal Tax Brackets

Non-refundable Tax Credits

Non-refundable Tax Credits

EI special benefits for self-employed

Self-employed can now “opt-in” to receive “Special

EI special benefits for self-employed

Self-employed can now “opt-in” to receive “Special

Interest deductibility update

“Borrowed for the purpose of earning income”

Stocks that don’t

Interest deductibility update

“Borrowed for the purpose of earning income”

Stocks that don’t

#1 - Claim those renos (Schedule 12)

Home Renovation Tax Credit

Expired January

#1 - Claim those renos (Schedule 12)

Home Renovation Tax Credit

Expired January

#2 – Split that pension (Form T1032)

Pension income?

Before age 65?

Regular monthly

#2 – Split that pension (Form T1032)

Pension income?

Before age 65?

Regular monthly

#3 – Pool your donations (Schedule 9)

15% credit on first $200

29%

#3 – Pool your donations (Schedule 9)

15% credit on first $200

29%

#4 – Defer stock option benefits (T1212)

Election to defer taxable employment

#4 – Defer stock option benefits (T1212)

Election to defer taxable employment

Relief for underwater stock options

Share crashes – now worth $10/share or

Relief for underwater stock options

Share crashes – now worth $10/share or

Relief for underwater stock options

BUDGET 2010: New rule – special tax

Relief for underwater stock options

BUDGET 2010: New rule – special tax

Elimination of deferral & remittance requirement

Effective for exercises after March 4,

Elimination of deferral & remittance requirement

Effective for exercises after March 4,

#5 – Write off the kids!

Child amount - $2,089/child

Non-refundable credit (federal

#5 – Write off the kids!

Child amount - $2,089/child

Non-refundable credit (federal

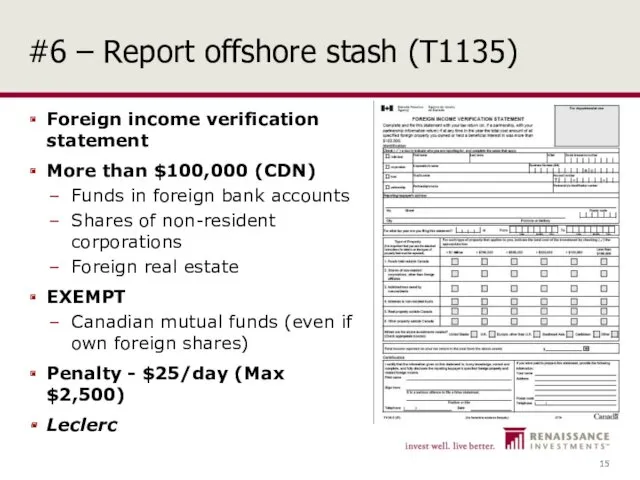

#6 – Report offshore stash (T1135)

Foreign income verification statement

More than $100,000

#6 – Report offshore stash (T1135)

Foreign income verification statement

More than $100,000

#7 – Claim legal fees

Loss of employment in 2009

Legal fees paid

#7 – Claim legal fees

Loss of employment in 2009

Legal fees paid

#8 – File on time

April 30 / June 15

5% of

#8 – File on time

April 30 / June 15

5% of

#9 – Report all your income

Missing receipt?

File on time and estimate

#9 – Report all your income

Missing receipt?

File on time and estimate

#10 - Avoid that refund

Reduce tax at source

Reduce OAS clawback at

#10 - Avoid that refund

Reduce tax at source

Reduce OAS clawback at

Plan NOT to Get a Refund!

the euphoria of getting a tax

Plan NOT to Get a Refund!

the euphoria of getting a tax

Plan NOT to Get a Refund! (cont’d)

“Undue hardship” provision

Too

Plan NOT to Get a Refund! (cont’d)

“Undue hardship” provision

Too

Capital gain in 2009 – OAS

Client will pay back all 2009

Capital gain in 2009 – OAS

Client will pay back all 2009

Capital gain in 2009 – OAS (cont’d)

Apply for 2010 reduction of

Capital gain in 2009 – OAS (cont’d)

Apply for 2010 reduction of

Miscellaneous tax update

TFSA update

State of US estate tax

Cases of interest

Miscellaneous tax update

TFSA update

State of US estate tax

Cases of interest

TFSA carry-forward room

$10,000 opportunity

$20,000 opportunity (spouses/partners)

No attribution

TFSA carry-forward room

$10,000 opportunity

$20,000 opportunity (spouses/partners)

No attribution

TFSA – New “anti-avoidance” rules

Deliberate overcontributions

Prohibited investments

Asset transfer transactions

Non-qualified investments (land,

TFSA – New “anti-avoidance” rules

Deliberate overcontributions

Prohibited investments

Asset transfer transactions

Non-qualified investments (land,

TFSA – Deliberate overcontributions

Any income attributable to deliberate overcontributions and prohibited

TFSA – Deliberate overcontributions

Any income attributable to deliberate overcontributions and prohibited

TFSA – Prohibited investments

Any income attributable to prohibited investments subject to

TFSA – Prohibited investments

Any income attributable to prohibited investments subject to

TFSA – Asset transfer transactions

Effectively prohibit asset transfer transactions between TFSAs

TFSA – Asset transfer transactions

Effectively prohibit asset transfer transactions between TFSAs

U.S. Estate Tax Update

Assume non-resident, non-U.S. citizen (“ALIEN”)

U.S. situs property:

U.S. real

U.S. Estate Tax Update

Assume non-resident, non-U.S. citizen (“ALIEN”)

U.S. situs property:

U.S. real

2009 U.S. Estate Tax Rates

Source: BDO Dunwoody LLP, May 15, 2008

2009 U.S. Estate Tax Rates

Source: BDO Dunwoody LLP, May 15, 2008

U.S. Estate Tax Exemption / Rates

U.S. Estate Tax Exemption / Rates

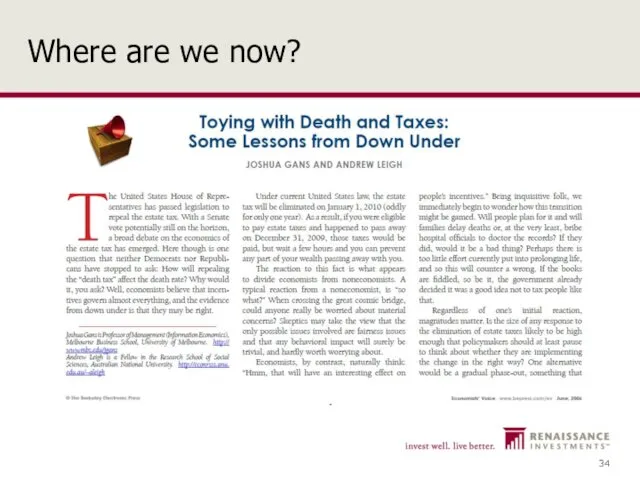

Where are we now?

December 2009 – U.S. House of Representatives approved

Where are we now?

December 2009 – U.S. House of Representatives approved

Where are we now?

Where are we now?

Garron Family Trust (2009)

Barbados trusts

$450 million capital gain

Residency of trusts

IT 447

Garron Family Trust (2009)

Barbados trusts

$450 million capital gain

Residency of trusts

IT 447

Marechaux (2009)

Leveraged donation tax shelter

Produces "return on donation of up to

Marechaux (2009)

Leveraged donation tax shelter

Produces "return on donation of up to

Innovative Installation Inc. (2009)

Innovative borrowed $220,000 from RBC

“Key person” life insurance

Innovative Installation Inc. (2009)

Innovative borrowed $220,000 from RBC

“Key person” life insurance

Life insurance – “Holdco” & “Sub”

New CRA position (December 23, 2009)

Life insurance – “Holdco” & “Sub”

New CRA position (December 23, 2009)

Bilodeau (2009)

Financial advisor purchased two $1 million UL policies

Life insurance commissions

Bilodeau (2009)

Financial advisor purchased two $1 million UL policies

Life insurance commissions

Li (2009)

Financial advisor deducted various employment expenses:

Salary to assistant/husband ($14,000)

Form T2200

Li (2009)

Financial advisor deducted various employment expenses:

Salary to assistant/husband ($14,000)

Form T2200

Rupprecht (2009)

Financial advisor deducted:

Costco membership fees

Clothing ($8,400 in “suitable clothing”)

RRSP penalties

Rupprecht (2009)

Financial advisor deducted:

Costco membership fees

Clothing ($8,400 in “suitable clothing”)

RRSP penalties

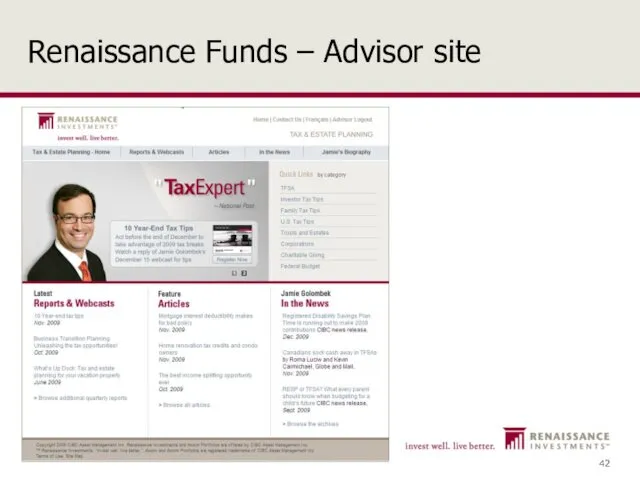

Renaissance Funds – Advisor site

Renaissance Funds – Advisor site

Thank You

This material was prepared for investment professionals only and is

Thank You

This material was prepared for investment professionals only and is

Анализ и оценка эффективности деятельности организации малого бизнеса на примере ООО Газпроминвест

Анализ и оценка эффективности деятельности организации малого бизнеса на примере ООО Газпроминвест Производительность труда и заработная плата

Производительность труда и заработная плата Фонд развития промышленности Республики Башкортостан

Фонд развития промышленности Республики Башкортостан How much for your company?

How much for your company? Рынок Forex

Рынок Forex Государственная социальная помощь на основании социального контракта. Пермский край

Государственная социальная помощь на основании социального контракта. Пермский край Особенности финансов предприятий различных организационно-правовых форм хозяйствования

Особенности финансов предприятий различных организационно-правовых форм хозяйствования Бесконтактный бухгалтер 1С:БухОбслуживание

Бесконтактный бухгалтер 1С:БухОбслуживание Денежно-кредитная политика

Денежно-кредитная политика Учет и анализ денежных средств в ООО НПК Механика Сервис

Учет и анализ денежных средств в ООО НПК Механика Сервис О возможностях стипендиального обеспечения в университете

О возможностях стипендиального обеспечения в университете Региональный рынок банковского потребительского кредитования

Региональный рынок банковского потребительского кредитования Грошові системи

Грошові системи Оплата труда персонала

Оплата труда персонала Основные активные операции коммерческого банка

Основные активные операции коммерческого банка Topic 1. Introduction to Finance

Topic 1. Introduction to Finance Көлік құралдарына салынатын салық

Көлік құралдарына салынатын салық Бухгалтерские информационные системы

Бухгалтерские информационные системы Лизинговые программы для субъектов малого и среднего предпринимательства

Лизинговые программы для субъектов малого и среднего предпринимательства Сутність, будова та функції банківської системи. (Тема 1)

Сутність, будова та функції банківської системи. (Тема 1) ФОП (Фізичні особи-підприємці)

ФОП (Фізичні особи-підприємці) РЕСО ДОМ - страхование индивидуальных строений

РЕСО ДОМ - страхование индивидуальных строений План счетов кредитной организации

План счетов кредитной организации Управление денежными средствами и легко реализуемыми ценными бумагами

Управление денежными средствами и легко реализуемыми ценными бумагами Кредитный продукт Овердрафт. Альфа-Банк

Кредитный продукт Овердрафт. Альфа-Банк Налог на доходы физических лиц

Налог на доходы физических лиц Сущность и функции страхования. Законодательные основы страховой деятельности. Рынок страхования

Сущность и функции страхования. Законодательные основы страховой деятельности. Рынок страхования Методы финансового анализа

Методы финансового анализа