- The Cost of Capital

Содержание

- 2. Learning Objectives 1. Understand the different kinds of financing available to a company: debt financing, equity

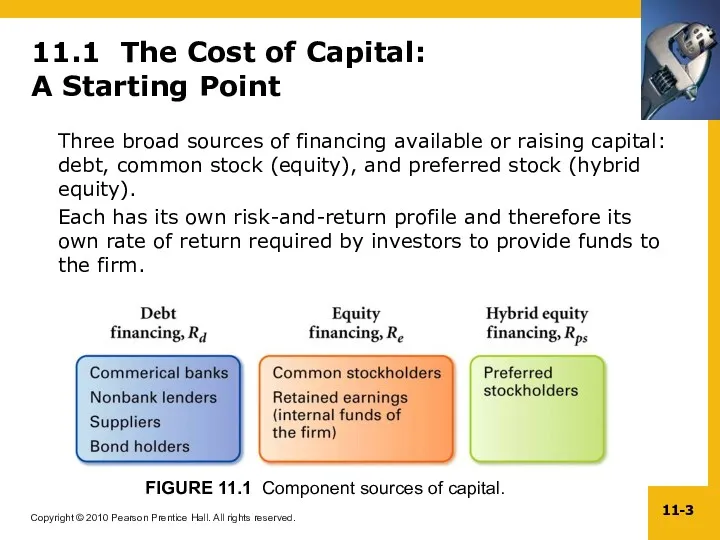

- 3. 11.1 The Cost of Capital: A Starting Point Three broad sources of financing available or raising

- 4. 11.1 The Cost of Capital: A Starting Point The weighted average cost of capital (WACC) is

- 5. 11.1 The Cost of Capital: A Starting Point (continued) Example 1: Measuring the Weighted Average Cost

- 6. 11.1 The Cost of Capital: A Starting Point (continued) Solution Jim’s weighted average cost of borrowing

- 7. 11.2 Components of the Weighted Average Cost of Capital To determine a firm’s WACC we need

- 8. 11.2 (A) Debt Component The cost of debt (Rd) is the rate that firms have to

- 9. 11.2 (A) Debt Component (continued) YTM on outstanding bonds indicates what investors require for lending the

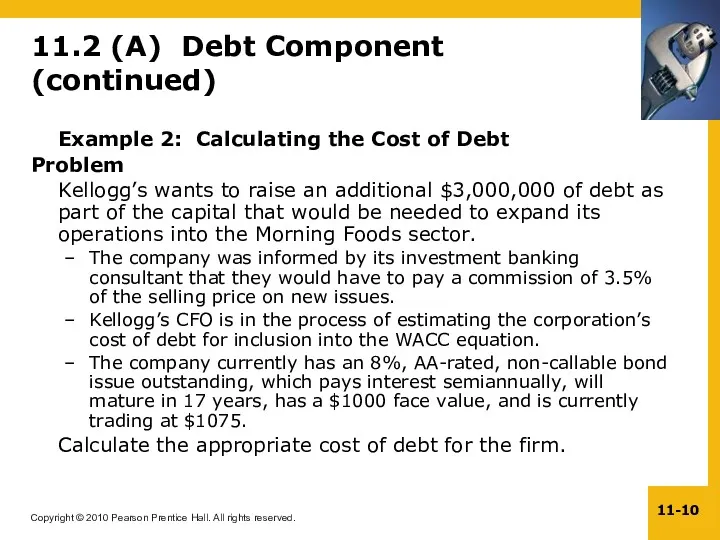

- 10. 11.2 (A) Debt Component (continued) Example 2: Calculating the Cost of Debt Problem Kellogg’s wants to

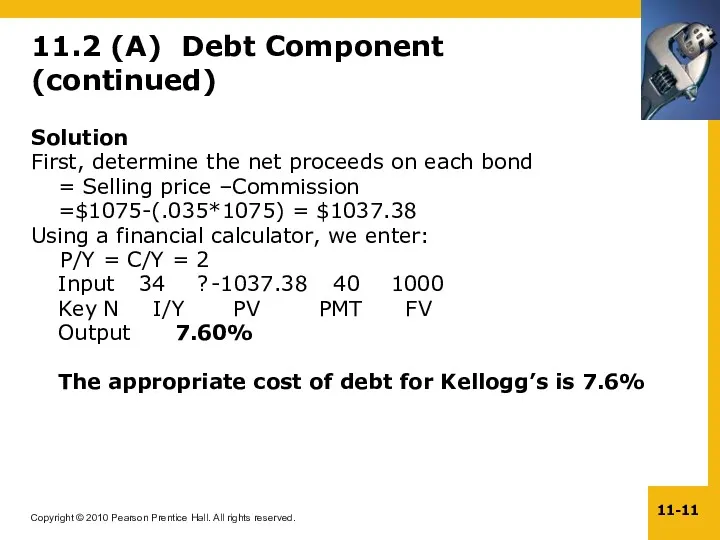

- 11. 11.2 (A) Debt Component (continued) Solution First, determine the net proceeds on each bond = Selling

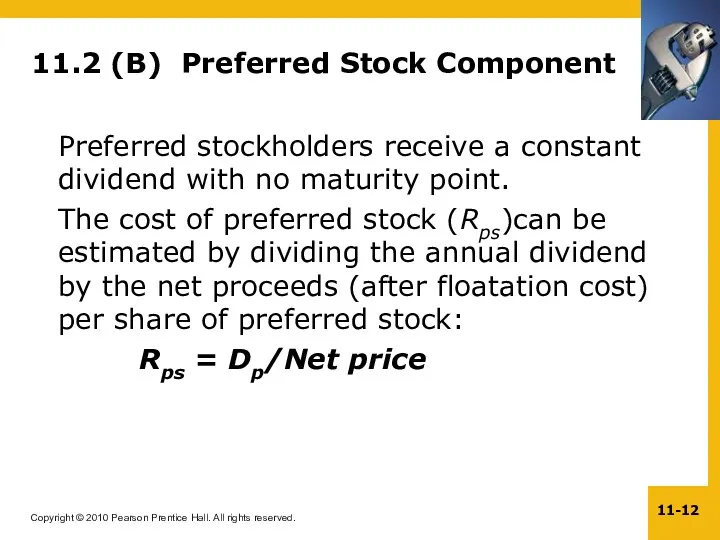

- 12. 11.2 (B) Preferred Stock Component Preferred stockholders receive a constant dividend with no maturity point. The

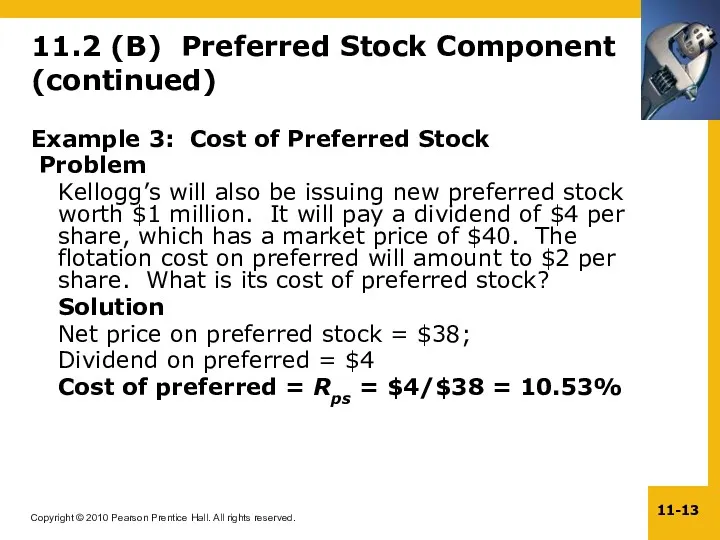

- 13. 11.2 (B) Preferred Stock Component (continued) Example 3: Cost of Preferred Stock Problem Kellogg’s will also

- 14. 11.2 (C) Equity Component The cost of equity (Re)is essentially the rate of return that investors

- 15. 11.2 (C) Equity Component (continued) The Security Market Line Approach calculates the cost of equity as

- 16. 11.2 (C) Equity Component (continued) Example 4: Calculating Cost of Equity with the SML Equation Problem

- 17. 11.2 (C) Equity Component (continued) The Dividend Growth Approach to Re: The Gordon Model, introduced in

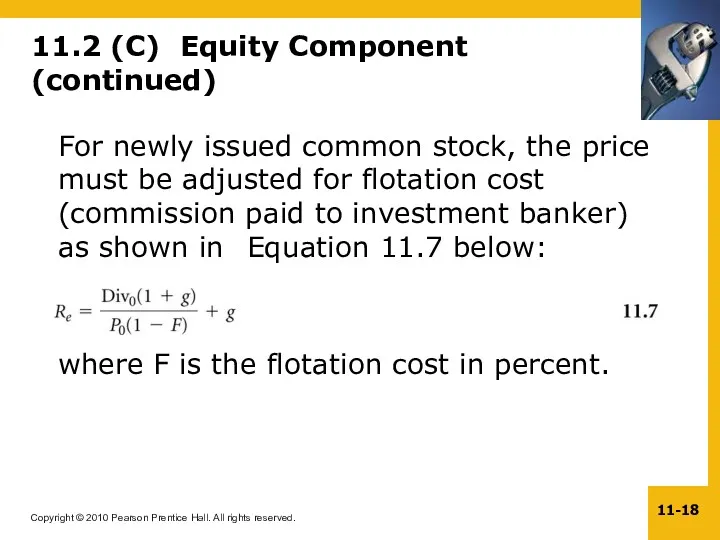

- 18. 11.2 (C) Equity Component (continued) For newly issued common stock, the price must be adjusted for

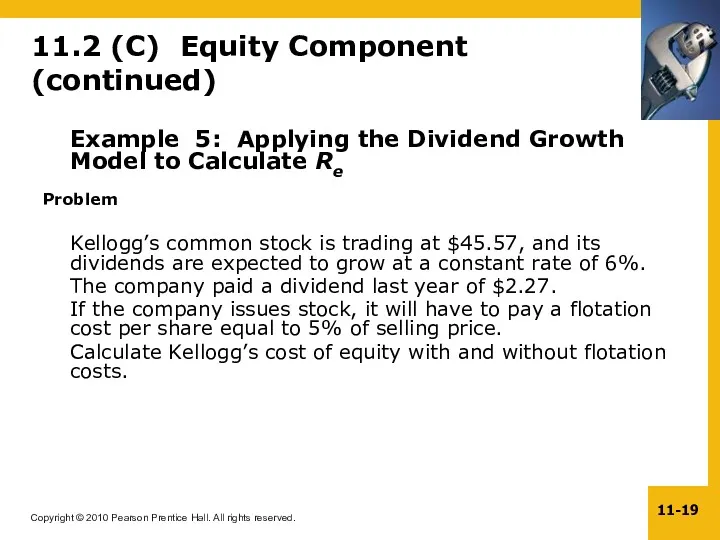

- 19. 11.2 (C) Equity Component (continued) Example 5: Applying the Dividend Growth Model to Calculate Re Problem

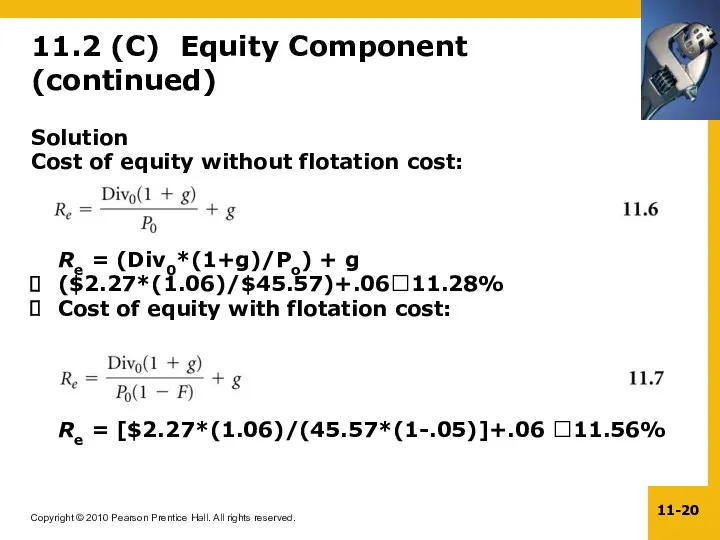

- 20. 11.2 (C) Equity Component (continued) Solution Cost of equity without flotation cost: Re = (Div0*(1+g)/Po) +

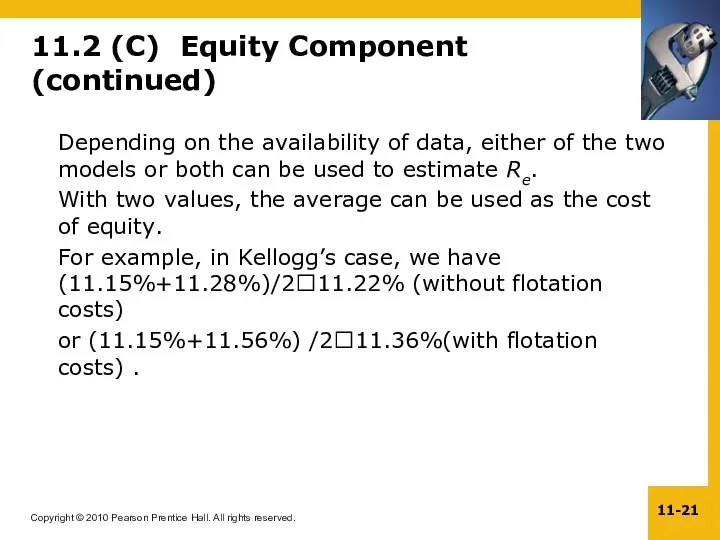

- 21. 11.2 (C) Equity Component (continued) Depending on the availability of data, either of the two models

- 22. 11.2 (D) Retained Earnings Retained earnings do have a cost, i.e., the opportunity cost for the

- 23. 11.2 (E) The Debt Component and Taxes Since interest expenses are tax-deductible, the cost of debt

- 24. 11.3 Weighting the Components: Book Value or Market Value? To calculate the WACC of a firm,

- 25. 11.3 (A) Book Value Book value weights can be determined by taking the balance sheet values

- 26. 11.3 (B) Market Value Market value weights are determined by taking the current market prices of

- 27. 11.3 (B) Market Value (continued) Example 6: Calculating Capital Component Weights Problem Kellogg’s CFO is in

- 28. 11.3 (B) Market Value (continued) Solution Calculate the total book value and total market value of

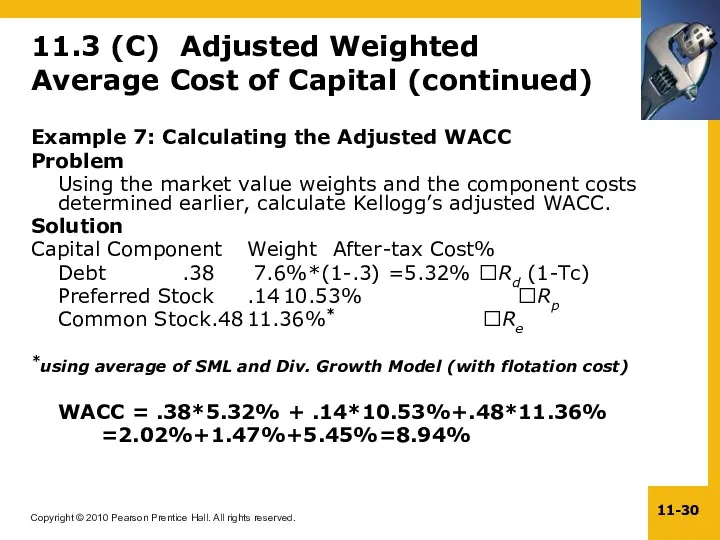

- 29. 11.3 (C) Adjusted Weighted Average Cost of Capital Equation 11.9 can be used to combine all

- 30. 11.3 (C) Adjusted Weighted Average Cost of Capital (continued) Example 7: Calculating the Adjusted WACC Problem

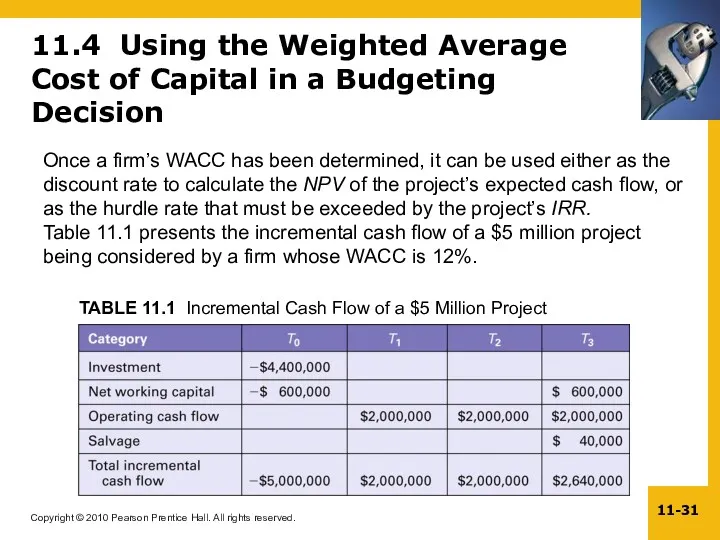

- 31. 11.4 Using the Weighted Average Cost of Capital in a Budgeting Decision Once a firm’s WACC

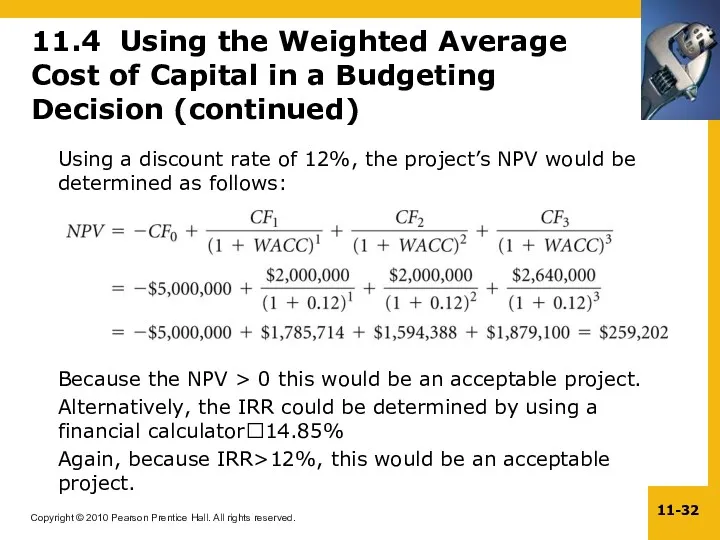

- 32. 11.4 Using the Weighted Average Cost of Capital in a Budgeting Decision (continued) Using a discount

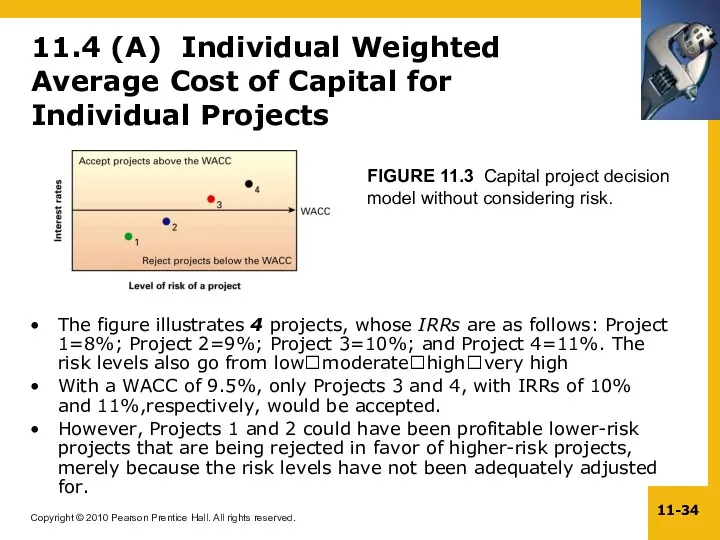

- 33. 11.4 (A) Individual Weighted Average Cost of Capital for Individual Projects Using the WACC for evaluating

- 34. The figure illustrates 4 projects, whose IRRs are as follows: Project 1=8%; Project 2=9%; Project 3=10%;

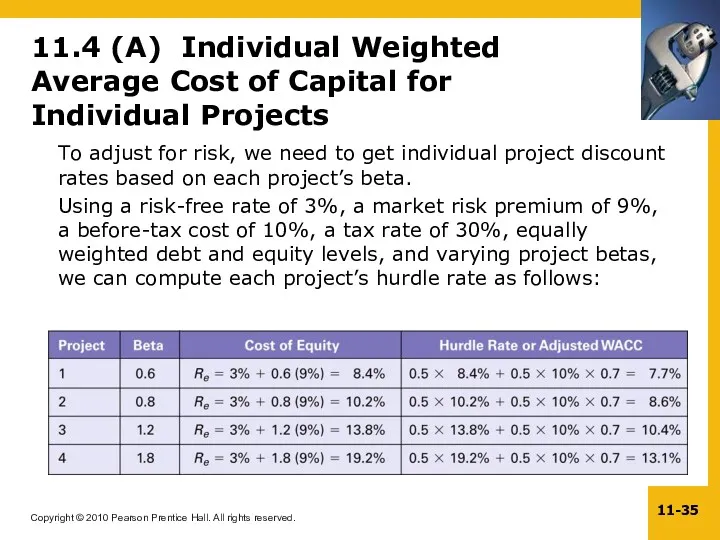

- 35. To adjust for risk, we need to get individual project discount rates based on each project’s

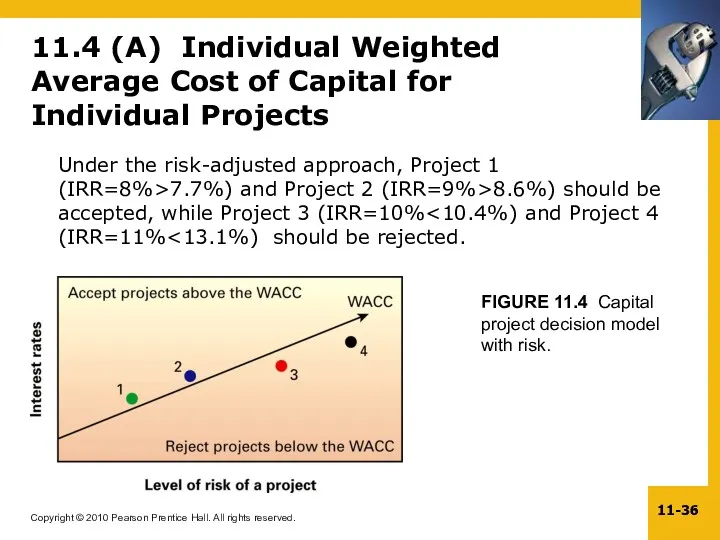

- 36. Under the risk-adjusted approach, Project 1 (IRR=8%>7.7%) and Project 2 (IRR=9%>8.6%) should be accepted, while Project

- 37. 11.5 Selecting Appropriate Betas for Projects It is important to adjust the discount rate used when

- 38. 11.6 Constraints on Borrowing and Selecting Projects for the Portfolio Capital constraints prevent firms from funding

- 39. 11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued) Example 8: Selecting Projects with

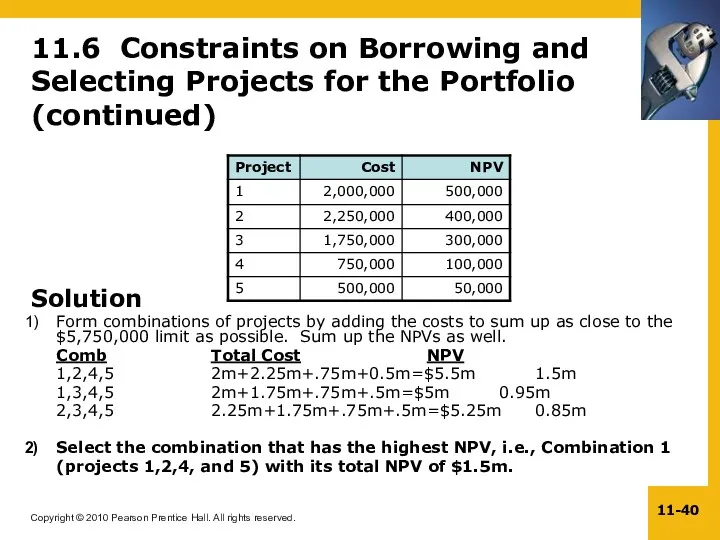

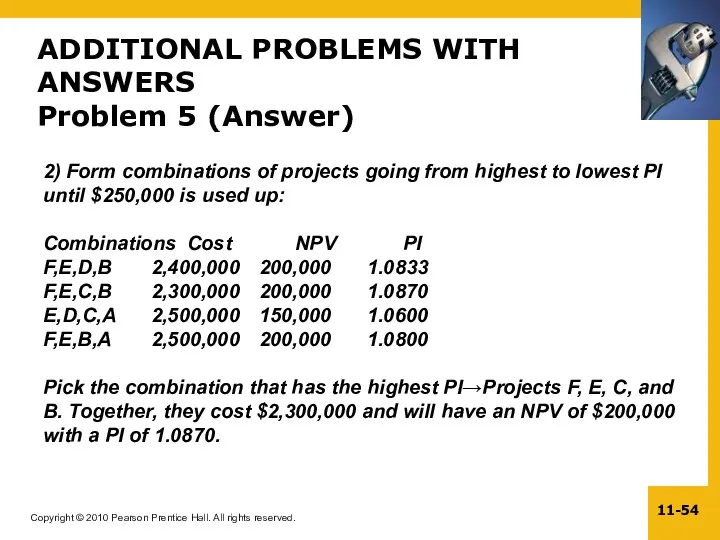

- 40. 11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued) Solution Form combinations of projects

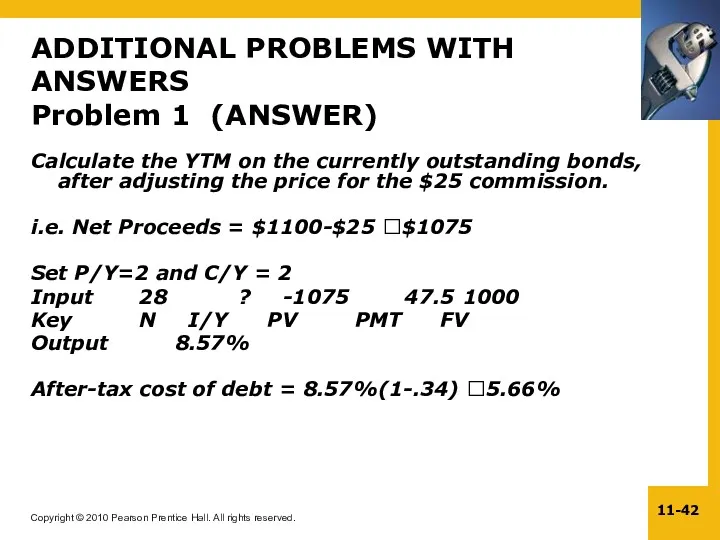

- 41. ADDITIONAL PROBLEMS WITH ANSWERS Problem 1 Cost of debt for a firm You have been assigned

- 42. ADDITIONAL PROBLEMS WITH ANSWERS Problem 1 (ANSWER) Calculate the YTM on the currently outstanding bonds, after

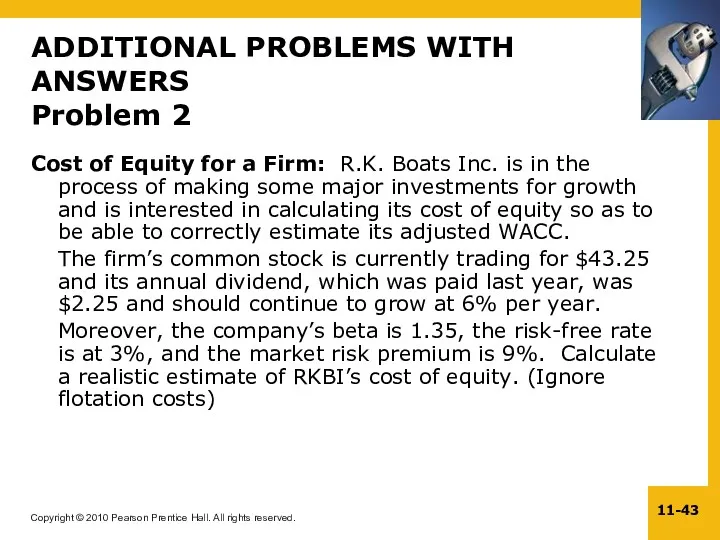

- 43. ADDITIONAL PROBLEMS WITH ANSWERS Problem 2 Cost of Equity for a Firm: R.K. Boats Inc. is

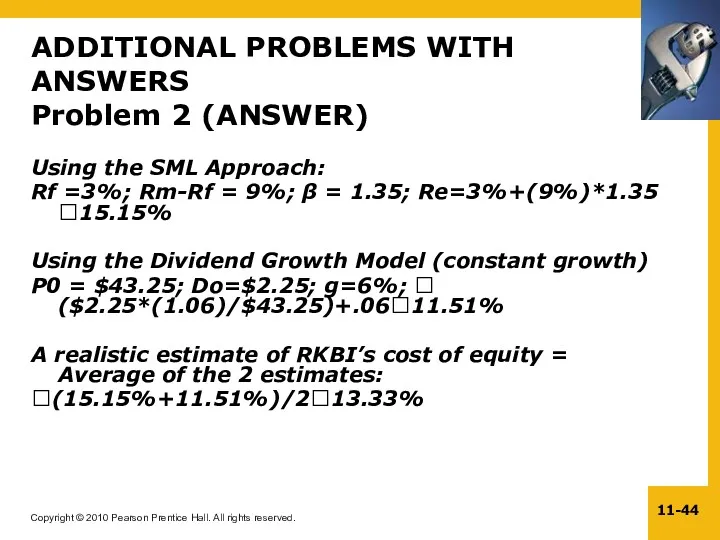

- 44. ADDITIONAL PROBLEMS WITH ANSWERS Problem 2 (ANSWER) Using the SML Approach: Rf =3%; Rm-Rf = 9%;

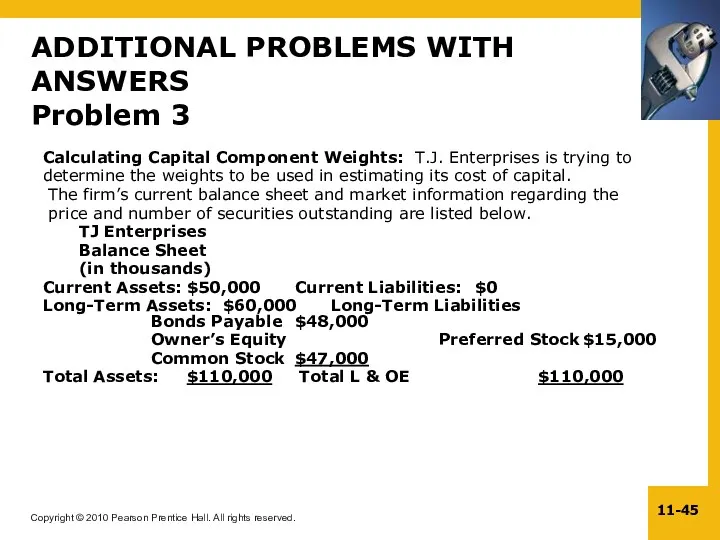

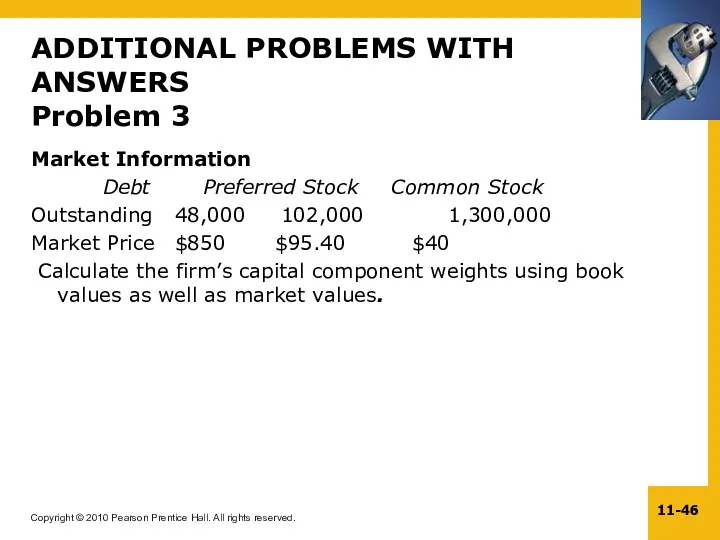

- 45. ADDITIONAL PROBLEMS WITH ANSWERS Problem 3 Calculating Capital Component Weights: T.J. Enterprises is trying to determine

- 46. ADDITIONAL PROBLEMS WITH ANSWERS Problem 3 Market Information Debt Preferred Stock Common Stock Outstanding 48,000 102,000

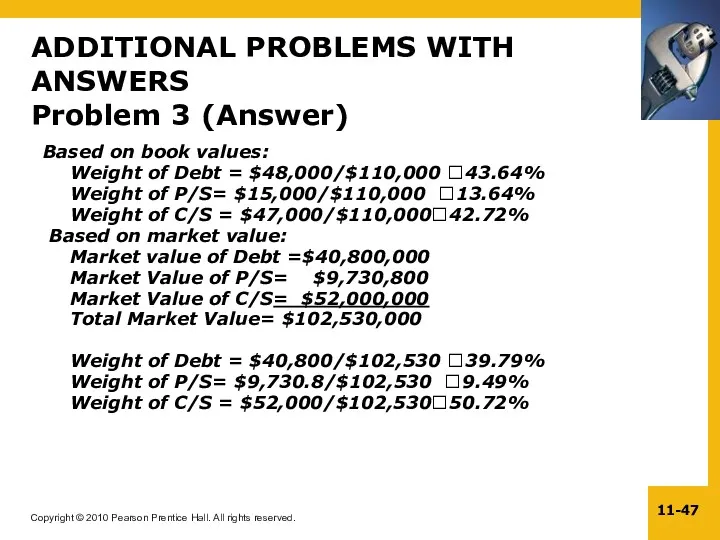

- 47. Based on book values: Weight of Debt = $48,000/$110,000 ?43.64% Weight of P/S= $15,000/$110,000 ?13.64% Weight

- 48. Computing WACC New Ideas Inc. currently has 30,000 of its 9% semiannual coupon bonds outstanding (par

- 49. 1) Determine the component costs Cost of Debt: P=1340; F=2%; Net proceeds=P(1-F) Net proceeds = $1340*(1-.02)=$1273

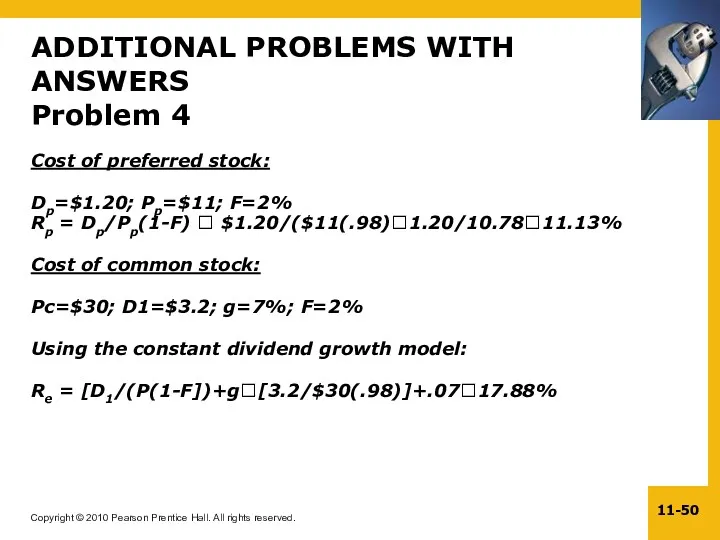

- 50. Cost of preferred stock: Dp=$1.20; Pp=$11; F=2% Rp = Dp/Pp(1-F) ? $1.20/($11(.98)?1.20/10.78?11.13% Cost of common stock:

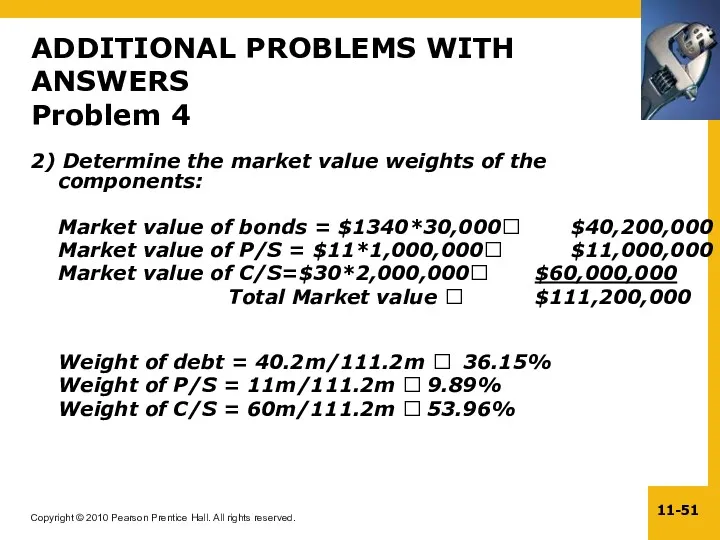

- 51. 2) Determine the market value weights of the components: Market value of bonds = $1340*30,000? $40,200,000

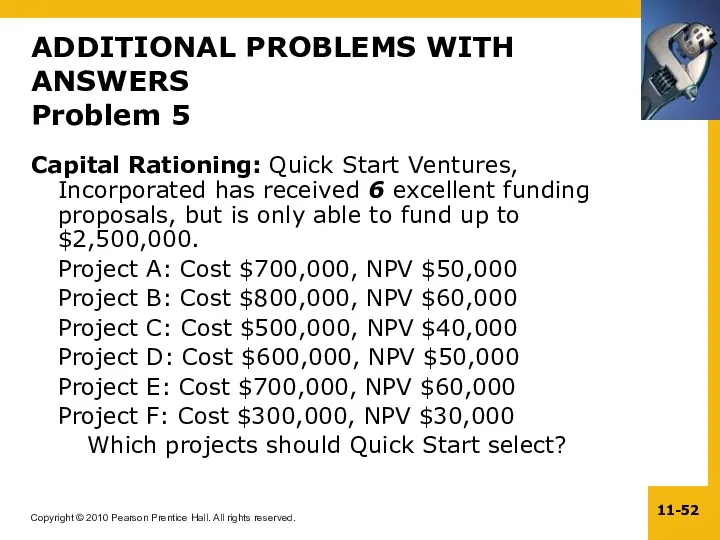

- 52. ADDITIONAL PROBLEMS WITH ANSWERS Problem 5 Capital Rationing: Quick Start Ventures, Incorporated has received 6 excellent

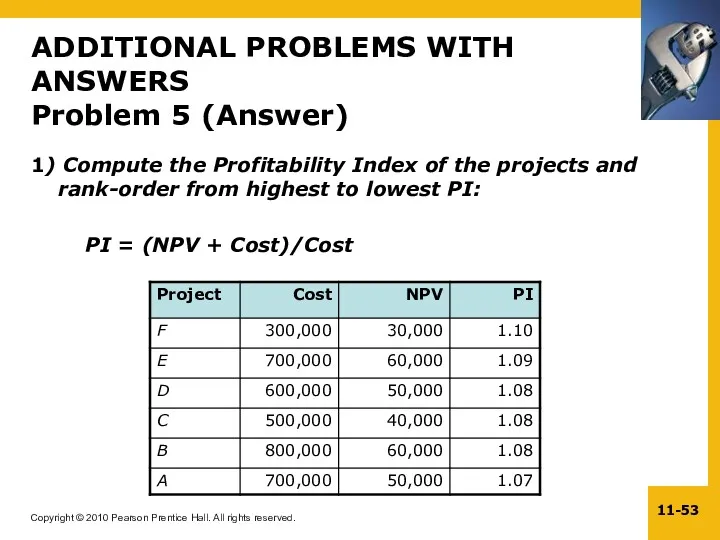

- 53. 1) Compute the Profitability Index of the projects and rank-order from highest to lowest PI: PI

- 54. ADDITIONAL PROBLEMS WITH ANSWERS Problem 5 (Answer) 2) Form combinations of projects going from highest to

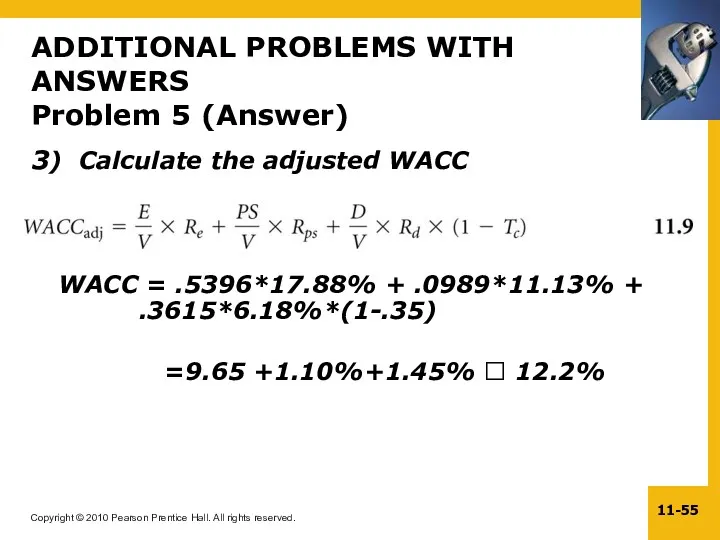

- 55. ADDITIONAL PROBLEMS WITH ANSWERS Problem 5 (Answer) 3) Calculate the adjusted WACC WACC = .5396*17.88% +

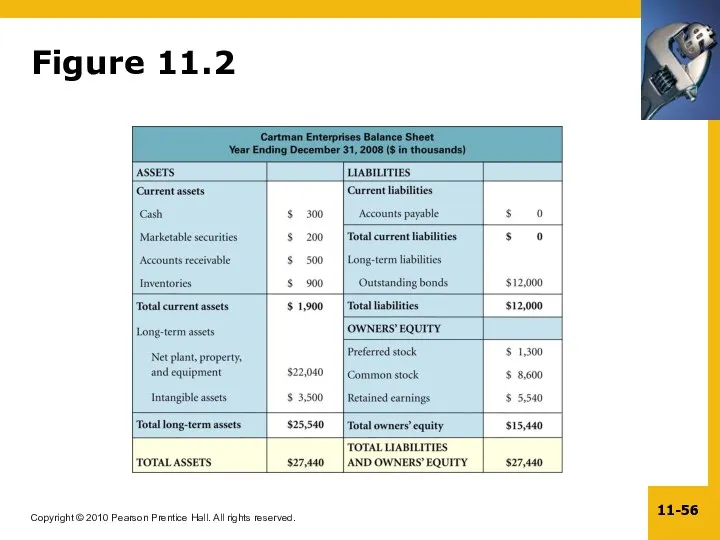

- 56. Figure 11.2

- 58. Скачать презентацию

Learning Objectives

1. Understand the different kinds of financing available to a company:

Learning Objectives

1. Understand the different kinds of financing available to a company:

11.1 The Cost of Capital:

A Starting Point

Three broad sources of

11.1 The Cost of Capital:

A Starting Point

Three broad sources of

11.1 The Cost of Capital: A Starting Point

The weighted average cost

11.1 The Cost of Capital: A Starting Point

The weighted average cost

11.1 The Cost of Capital: A Starting Point (continued)

Example 1:

11.1 The Cost of Capital: A Starting Point (continued)

Example 1:

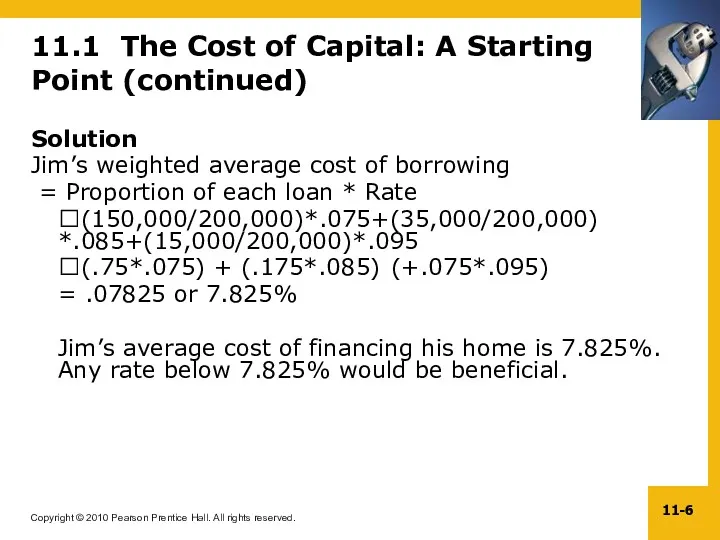

11.1 The Cost of Capital: A Starting Point (continued)

Solution

Jim’s weighted average

11.1 The Cost of Capital: A Starting Point (continued)

Solution

Jim’s weighted average

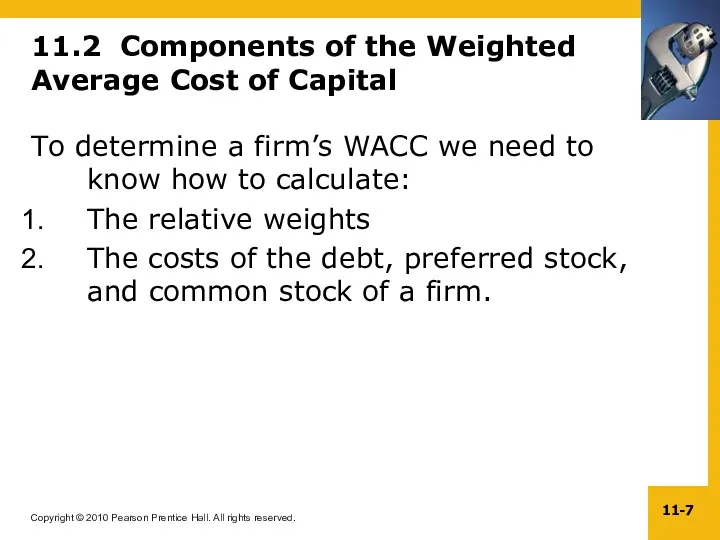

11.2 Components of the Weighted Average Cost of Capital

To determine a

11.2 Components of the Weighted Average Cost of Capital

To determine a

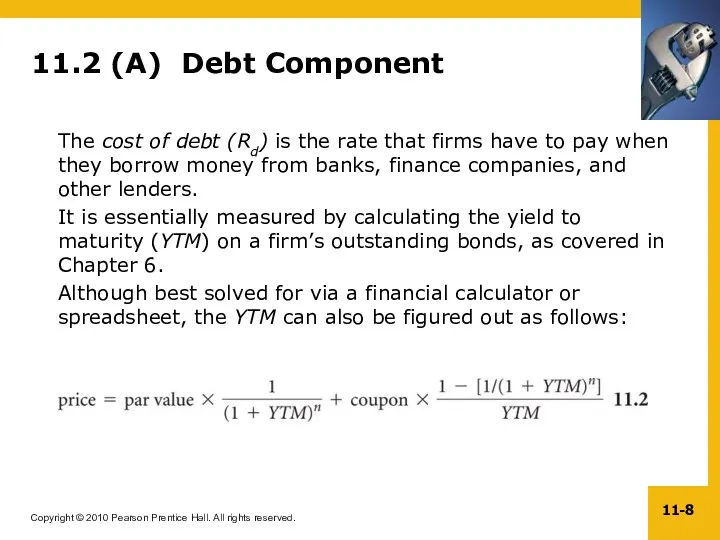

11.2 (A) Debt Component

The cost of debt (Rd) is the rate

11.2 (A) Debt Component

The cost of debt (Rd) is the rate

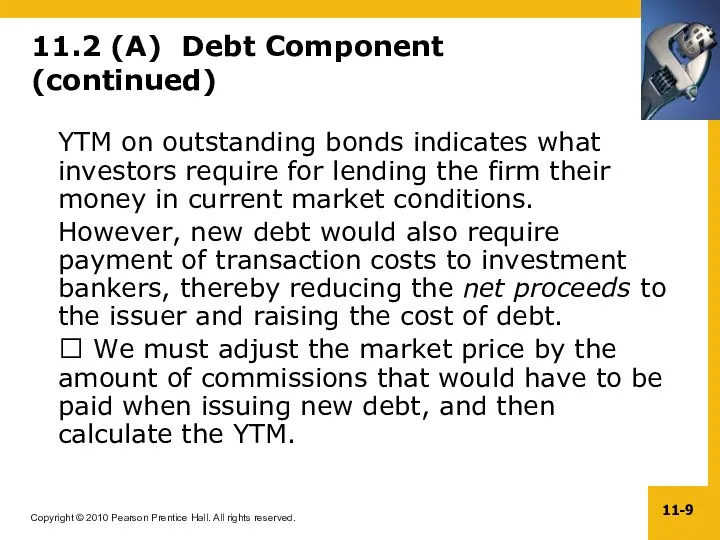

11.2 (A) Debt Component (continued)

YTM on outstanding bonds indicates what investors

11.2 (A) Debt Component (continued)

YTM on outstanding bonds indicates what investors

11.2 (A) Debt Component (continued)

Example 2: Calculating the Cost of Debt

Problem

Kellogg’s

11.2 (A) Debt Component (continued)

Example 2: Calculating the Cost of Debt

Problem

Kellogg’s

11.2 (A) Debt Component (continued)

Solution

First, determine the net proceeds on each

11.2 (A) Debt Component (continued)

Solution

First, determine the net proceeds on each

11.2 (B) Preferred Stock Component

Preferred stockholders receive a constant dividend with

11.2 (B) Preferred Stock Component

Preferred stockholders receive a constant dividend with

11.2 (B) Preferred Stock Component (continued)

Example 3: Cost of Preferred Stock

Problem

Kellogg’s

11.2 (B) Preferred Stock Component (continued)

Example 3: Cost of Preferred Stock

Problem

Kellogg’s

11.2 (C) Equity Component

The cost of equity (Re)is essentially the rate

11.2 (C) Equity Component

The cost of equity (Re)is essentially the rate

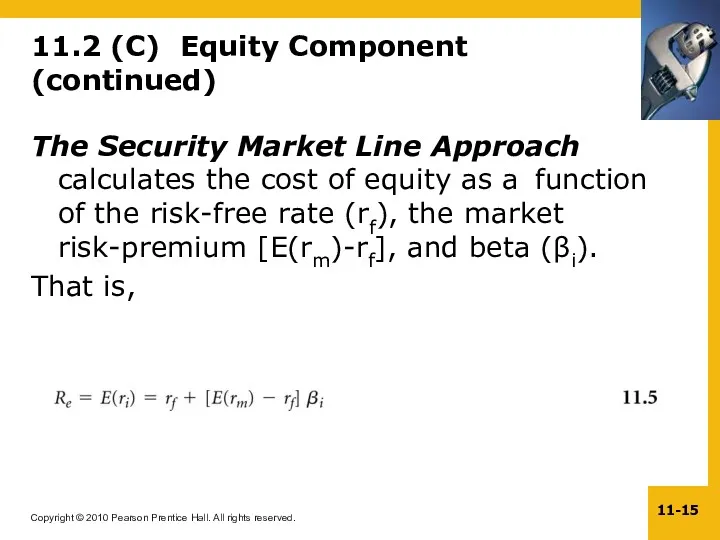

11.2 (C) Equity Component (continued)

The Security Market Line Approach calculates the

11.2 (C) Equity Component (continued)

The Security Market Line Approach calculates the

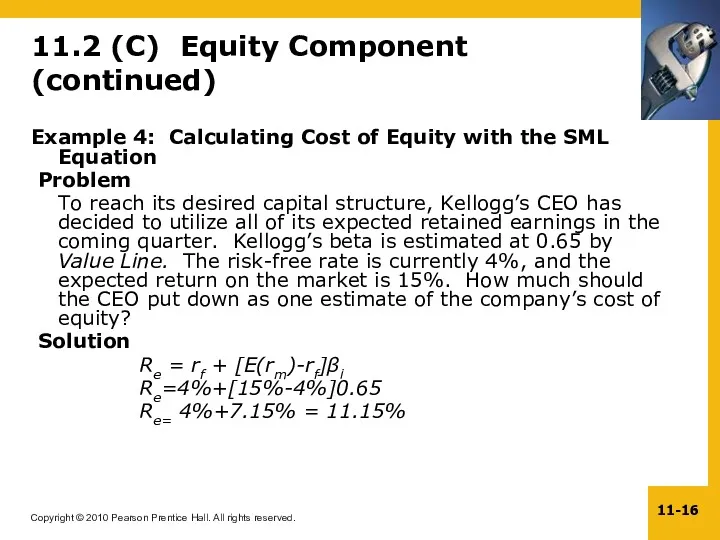

11.2 (C) Equity Component (continued)

Example 4: Calculating Cost of Equity with

11.2 (C) Equity Component (continued)

Example 4: Calculating Cost of Equity with

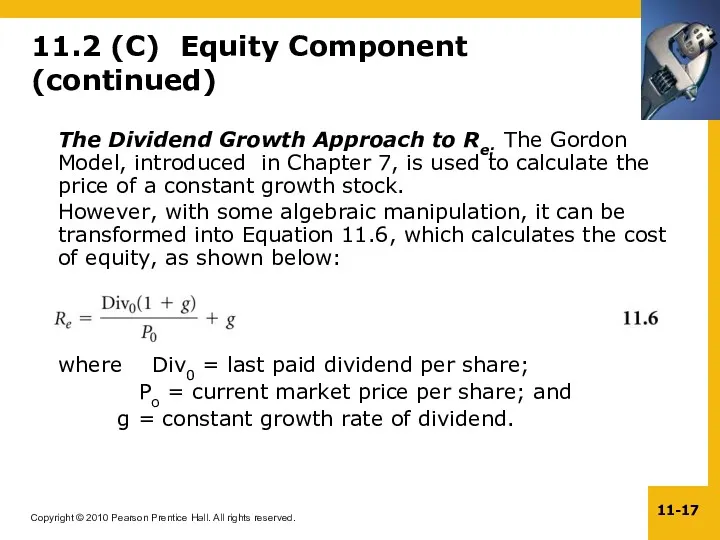

11.2 (C) Equity Component (continued)

The Dividend Growth Approach to Re: The

11.2 (C) Equity Component (continued)

The Dividend Growth Approach to Re: The

11.2 (C) Equity Component (continued)

For newly issued common stock, the price

11.2 (C) Equity Component (continued)

For newly issued common stock, the price

11.2 (C) Equity Component (continued)

Example 5: Applying the Dividend Growth Model

11.2 (C) Equity Component (continued)

Example 5: Applying the Dividend Growth Model

11.2 (C) Equity Component (continued)

Solution

Cost of equity without flotation cost:

Re =

11.2 (C) Equity Component (continued)

Solution

Cost of equity without flotation cost:

Re =

11.2 (C) Equity Component (continued)

Depending on the availability of data, either

11.2 (C) Equity Component (continued)

Depending on the availability of data, either

11.2 (D) Retained Earnings

Retained earnings do have a cost, i.e., the

11.2 (D) Retained Earnings

Retained earnings do have a cost, i.e., the

11.2 (E) The Debt Component and Taxes

Since interest expenses are tax-deductible,

11.2 (E) The Debt Component and Taxes

Since interest expenses are tax-deductible,

11.3 Weighting the Components: Book Value or Market Value?

To calculate the

11.3 Weighting the Components: Book Value or Market Value?

To calculate the

11.3 (A) Book Value

Book value weights can be determined by taking

11.3 (A) Book Value

Book value weights can be determined by taking

11.3 (B) Market Value

Market value weights are determined by taking the

11.3 (B) Market Value

Market value weights are determined by taking the

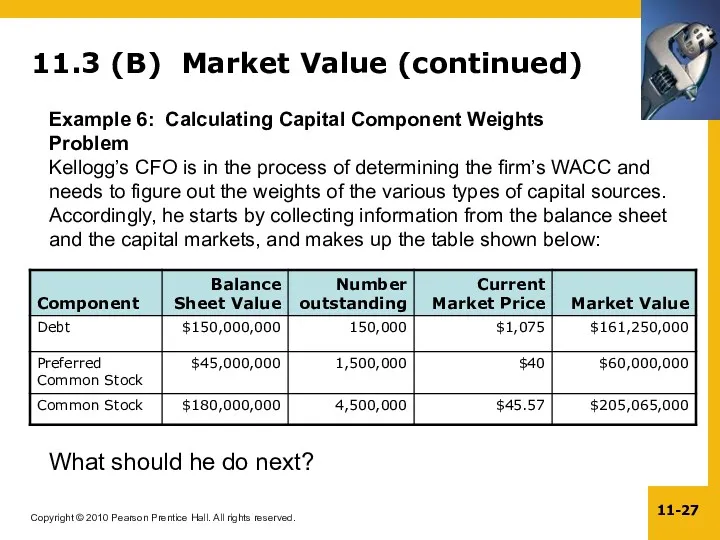

11.3 (B) Market Value (continued)

Example 6: Calculating Capital Component Weights

Problem

Kellogg’s CFO

11.3 (B) Market Value (continued)

Example 6: Calculating Capital Component Weights

Problem

Kellogg’s CFO

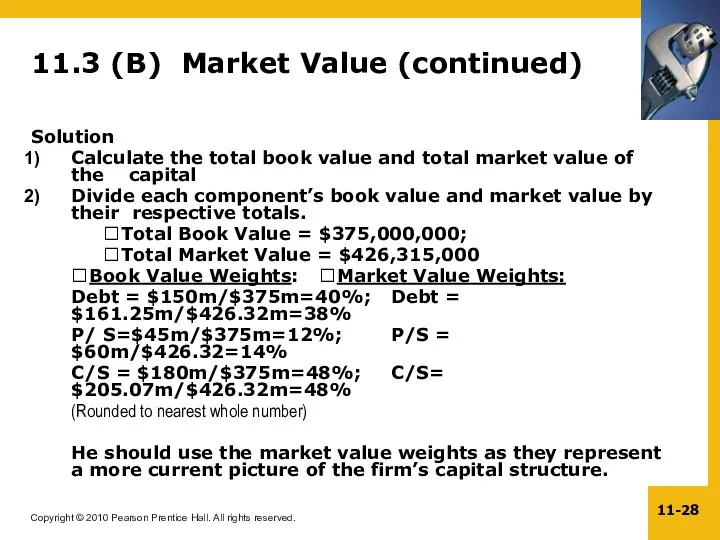

11.3 (B) Market Value (continued)

Solution

Calculate the total book value and total

11.3 (B) Market Value (continued)

Solution

Calculate the total book value and total

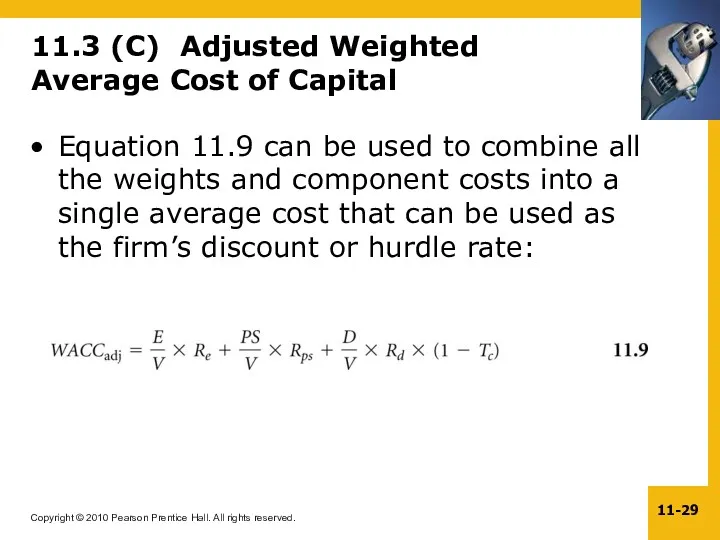

11.3 (C) Adjusted Weighted Average Cost of Capital

Equation 11.9 can be

11.3 (C) Adjusted Weighted Average Cost of Capital

Equation 11.9 can be

11.3 (C) Adjusted Weighted Average Cost of Capital (continued)

Example 7: Calculating

11.3 (C) Adjusted Weighted Average Cost of Capital (continued)

Example 7: Calculating

11.4 Using the Weighted Average Cost of Capital in a Budgeting

11.4 Using the Weighted Average Cost of Capital in a Budgeting

11.4 Using the Weighted Average Cost of Capital in a Budgeting

11.4 Using the Weighted Average Cost of Capital in a Budgeting

11.4 (A) Individual Weighted Average Cost of Capital for Individual Projects

Using

11.4 (A) Individual Weighted Average Cost of Capital for Individual Projects

Using

The figure illustrates 4 projects, whose IRRs are as follows: Project

The figure illustrates 4 projects, whose IRRs are as follows: Project

To adjust for risk, we need to get individual project discount

To adjust for risk, we need to get individual project discount

Under the risk-adjusted approach, Project 1 (IRR=8%>7.7%) and Project 2 (IRR=9%>8.6%)

Under the risk-adjusted approach, Project 1 (IRR=8%>7.7%) and Project 2 (IRR=9%>8.6%)

11.5 Selecting Appropriate Betas for Projects

It is important to adjust the

11.5 Selecting Appropriate Betas for Projects

It is important to adjust the

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio

Capital constraints

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio

Capital constraints

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued)

Example

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued)

Example

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued)

Solution

Form

11.6 Constraints on Borrowing and Selecting Projects for the Portfolio (continued)

Solution

Form

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 1

Cost of debt for a firm You

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 1

Cost of debt for a firm You

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 1 (ANSWER)

Calculate the YTM on the currently

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 1 (ANSWER)

Calculate the YTM on the currently

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 2

Cost of Equity for a Firm: R.K.

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 2

Cost of Equity for a Firm: R.K.

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 2 (ANSWER)

Using the SML Approach:

Rf =3%; Rm-Rf

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 2 (ANSWER)

Using the SML Approach:

Rf =3%; Rm-Rf

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 3

Calculating Capital Component Weights: T.J. Enterprises is

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 3

Calculating Capital Component Weights: T.J. Enterprises is

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 3

Market Information

Debt Preferred Stock Common Stock

Outstanding 48,000 102,000

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 3

Market Information

Debt Preferred Stock Common Stock

Outstanding 48,000 102,000

Based on book values:

Weight of Debt = $48,000/$110,000 ?43.64%

Weight of P/S=

Based on book values:

Weight of Debt = $48,000/$110,000 ?43.64%

Weight of P/S=

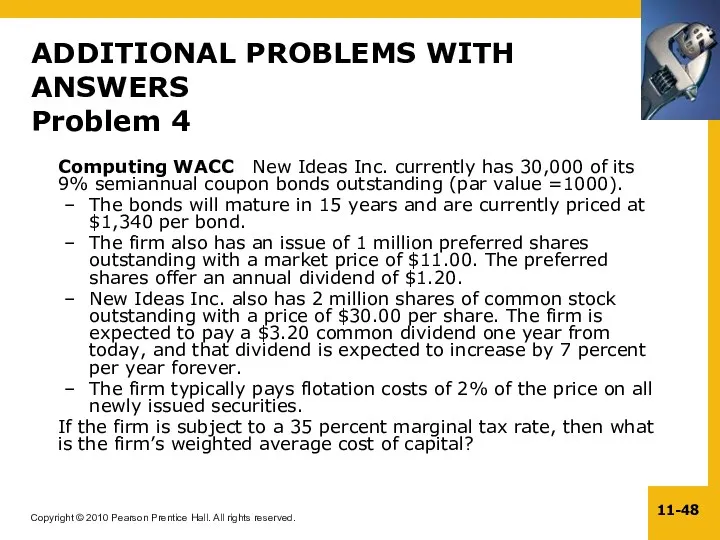

Computing WACC New Ideas Inc. currently has 30,000 of its 9%

Computing WACC New Ideas Inc. currently has 30,000 of its 9%

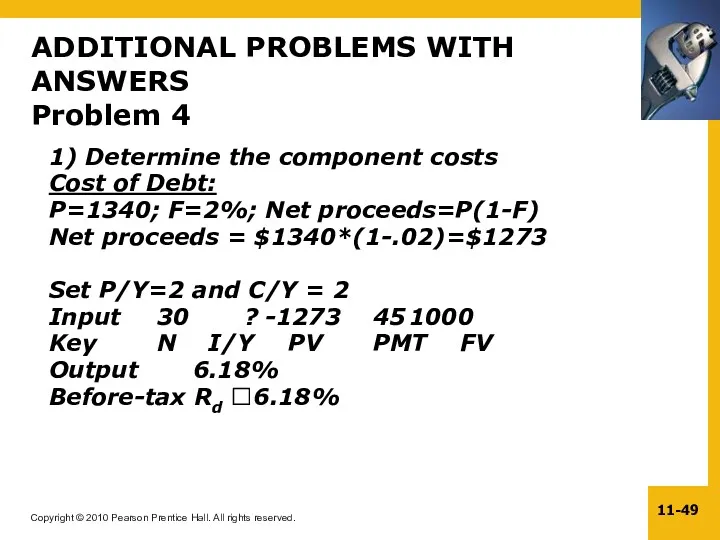

1) Determine the component costs

Cost of Debt:

P=1340; F=2%; Net proceeds=P(1-F)

Net proceeds

1) Determine the component costs

Cost of Debt:

P=1340; F=2%; Net proceeds=P(1-F)

Net proceeds

Cost of preferred stock:

Dp=$1.20; Pp=$11; F=2%

Rp = Dp/Pp(1-F) ? $1.20/($11(.98)?1.20/10.78?11.13%

Cost of

Cost of preferred stock:

Dp=$1.20; Pp=$11; F=2%

Rp = Dp/Pp(1-F) ? $1.20/($11(.98)?1.20/10.78?11.13%

Cost of

2) Determine the market value weights of the components:

Market value of

2) Determine the market value weights of the components:

Market value of

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5

Capital Rationing: Quick Start Ventures, Incorporated has

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5

Capital Rationing: Quick Start Ventures, Incorporated has

1) Compute the Profitability Index of the projects and rank-order from

1) Compute the Profitability Index of the projects and rank-order from

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5 (Answer)

2) Form combinations of projects going

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5 (Answer)

2) Form combinations of projects going

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5 (Answer)

3) Calculate the adjusted WACC

WACC =

ADDITIONAL PROBLEMS WITH ANSWERS

Problem 5 (Answer)

3) Calculate the adjusted WACC

WACC =

Figure 11.2

Figure 11.2

Управление инвестиционными проектами. (Тема 7)

Управление инвестиционными проектами. (Тема 7) Управлiння ресурсною базою банку

Управлiння ресурсною базою банку Мировые банковские системы

Мировые банковские системы Налоговая система РФ. Фискальная политика

Налоговая система РФ. Фискальная политика Аналіз фінансових результатів діяльності підприємства

Аналіз фінансових результатів діяльності підприємства Болонский процесс и гарантия качества высшего образования

Болонский процесс и гарантия качества высшего образования Планирование затрат на производство НПЗ

Планирование затрат на производство НПЗ Аудит учредительных документов и учетной политики организации

Аудит учредительных документов и учетной политики организации Порядок бухгалтерского учета операций в иностранной валюте

Порядок бухгалтерского учета операций в иностранной валюте Защита покупки. Группа АльфаСтрахование

Защита покупки. Группа АльфаСтрахование Объем рынка

Объем рынка Учет затрат и готовой продукции

Учет затрат и готовой продукции Платежная система России: проблемы и перспективы развития

Платежная система России: проблемы и перспективы развития Дисциплина Сметное дело. Введение в дисциплину

Дисциплина Сметное дело. Введение в дисциплину Почта России ЕАС ОПС

Почта России ЕАС ОПС Страховая компания Ренессанс Жизнь

Страховая компания Ренессанс Жизнь Участники рынка ценных бумаг. (Тема 2)

Участники рынка ценных бумаг. (Тема 2) Управление региональными финансовыми ресурсами

Управление региональными финансовыми ресурсами Ценообразование и цены на продукцию АПК

Ценообразование и цены на продукцию АПК Финансовые активы

Финансовые активы Понятие и цели финансового планирования

Понятие и цели финансового планирования Обзор изменений законодательства, федеральные стандарты бухгалтерского учета для организаций государственного сектора

Обзор изменений законодательства, федеральные стандарты бухгалтерского учета для организаций государственного сектора Семинар для клиентов малого и микро бизнеса приуроченный презентации нового продукта ЭВОТОР – СМАРТ-КАССА

Семинар для клиентов малого и микро бизнеса приуроченный презентации нового продукта ЭВОТОР – СМАРТ-КАССА Финансовый контроль, формы и методы его проведения. Виды финансового контроля

Финансовый контроль, формы и методы его проведения. Виды финансового контроля Государственная пенсия по инвалидности

Государственная пенсия по инвалидности Государственные или муниципальные преференции

Государственные или муниципальные преференции Процесс кредитования экономических субъектов

Процесс кредитования экономических субъектов Система персонифицированного финансирования дополнительного образования в Ачитском городском округе

Система персонифицированного финансирования дополнительного образования в Ачитском городском округе