- The theory of exchange rate determination

Содержание

- 2. Outline Defining Exchange Rate Measuring Exchange Rate Movements Appreciation/Depreciation of a currency Exchange Rate Equilibrium Factors

- 3. Key words and concepts Exchange rate Depreciation Appreciation Balance of payments Devaluation Revaluation Asset Capital mobility

- 4. What does it mean EXCHANGE RATE? Nominal exchange rate Spot rate Forward rate Bilateral exchange rate

- 5. Meaning of Nominal Exchange Rate Nominal exchange rate is the relative price of the currency of

- 6. Measuring Changes in Exchange Rates A decline in a local currency’s value is referred to as

- 7. Appreciation/Depreciation Percentage change in value of Foreign Currency New Value of one $ in terms of

- 8. Exchange Rates and Relative Prices Import and export demands are influenced by relative prices. Appreciation of

- 9. Nominal Exchange Rate Bilateral exchange rate is the rate at which you can swap the money

- 10. The importance of exchange rate Price unification of goods produced in different countries - they enable

- 11. The Foreign Exchange Market Exchange rates are determined in the foreign exchange market. The market in

- 12. The foreign exchange market is the mechanism by which participants: transfer purchasing power across countries; obtain

- 13. Spot Rates and Forward Rates Spot exchange rates Apply to exchange currencies “on the spot” Forward

- 14. Exchange Rate Equilibrium Forces of Demand and Supply Demand for foreign currency negatively related to the

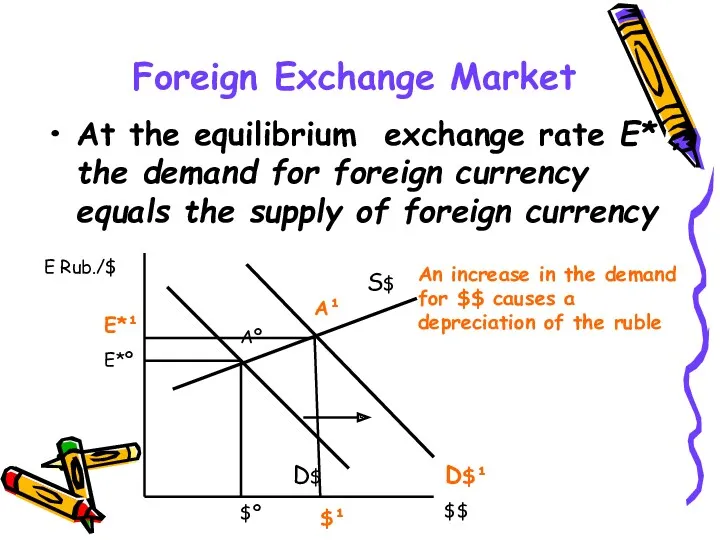

- 15. Foreign Exchange Market At the equilibrium exchange rate Е* , the demand for foreign currency equals

- 16. Exchange rate regimes Floating exchange rates – the CB allows the currency to depreciate until the

- 17. Real Exchange Rate The real exchange rate (RER) is the relative price of the goods of

- 18. Real Exchange Rate E – nominal exchange rate Р* /P – ratio of price levels Real

- 19. Real Exchange Rate Tradables/Nontradables E – nominal exchange rate РT* - prices of tradables in foreign

- 20. Real Exchange Rate E - nominal exchange rate W* - unit labor costs abroad (in foreign

- 21. Real Exchange Rate Internal terms of trade E - nominal exchange rate РIM* - prices of

- 22. Why the RER matters Real variable RER determines the allocation of resources Impact on the competitiveness

- 23. Current Account Theories

- 24. Purchasing Power Parity The law of one price - the same good can not sell for

- 25. PPP Model as Special Case PPP model is a special case of the real exchange rate

- 26. PPP Model as Special Case Real exchange rate equation captures reality at any point in time

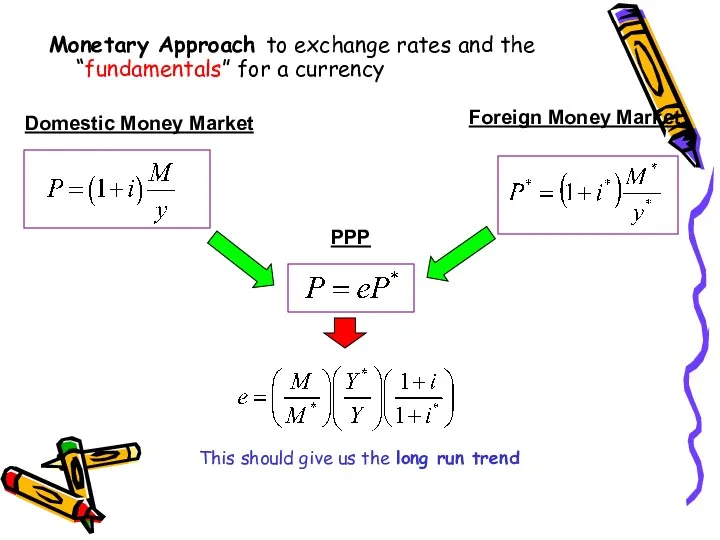

- 27. Exchange Rates in the LR PPP holds Relative prices are constant. Therefore, the real exchange rate

- 28. Monetary Approach to exchange rates and the “fundamentals” for a currency Domestic Money Market PPP Foreign

- 29. Exchange Rates in the SR Commodity prices are fixed (PPP fails) UIP and Currency markets determine

- 30. Asset Market Theories

- 31. The demand for a foreign currency bank deposit is influenced by the same considerations that influence

- 32. Risk and Liquidity Savers care about two main characteristics of an asset other than its return:

- 33. Return, Risk, and Liquidity in the Foreign Exchange Market The demand for foreign currency assets depends

- 34. Interest Rates Market participants need two pieces of information in order to compare returns on different

- 35. Exchange Rates and Asset Returns The returns on deposits traded in the foreign exchange market depend

- 36. A Simple Rule The dollar rate of return on euro deposits is approximately the euro interest

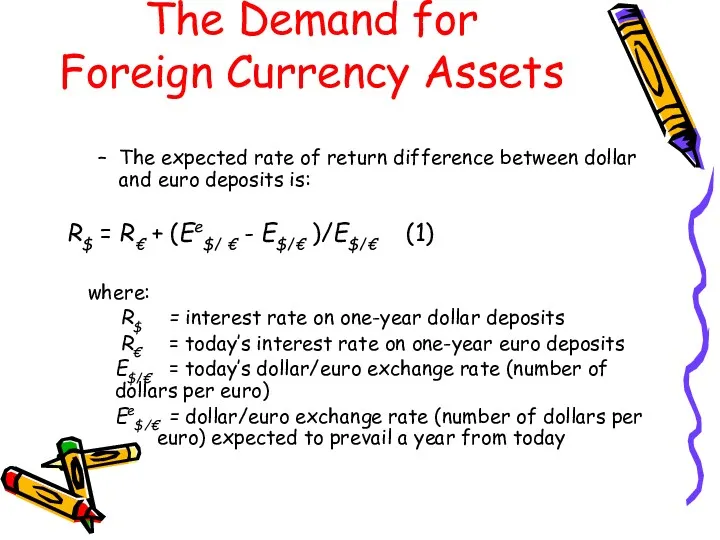

- 37. The expected rate of return difference between dollar and euro deposits is: R$ = R€ +

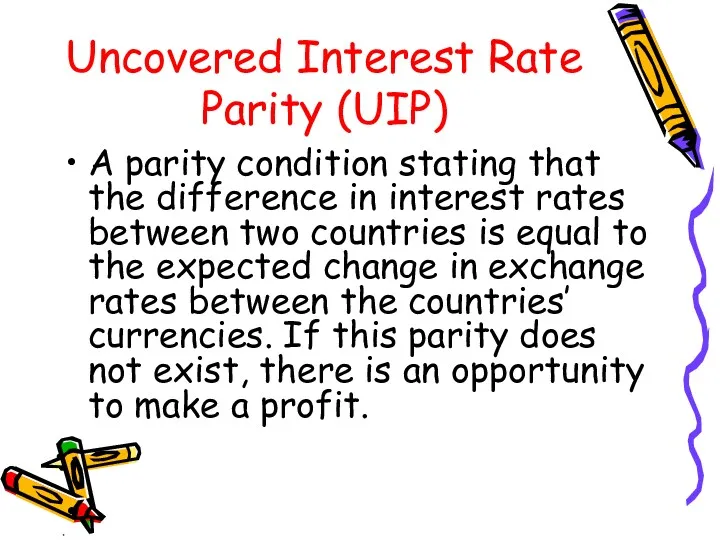

- 38. Uncovered Interest Rate Parity (UIP) A parity condition stating that the difference in interest rates between

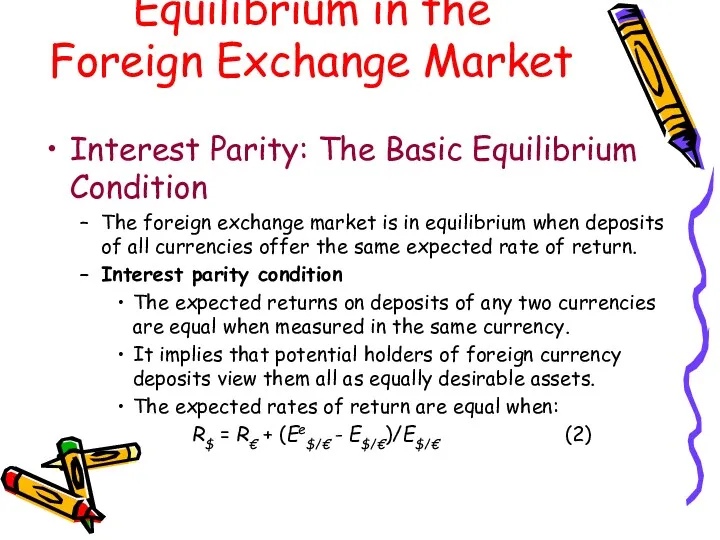

- 39. Equilibrium in the Foreign Exchange Market Interest Parity: The Basic Equilibrium Condition The foreign exchange market

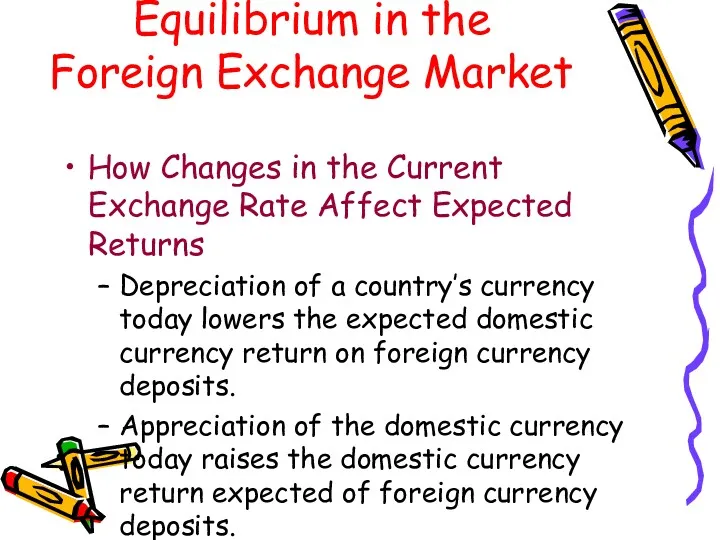

- 40. How Changes in the Current Exchange Rate Affect Expected Returns Depreciation of a country’s currency today

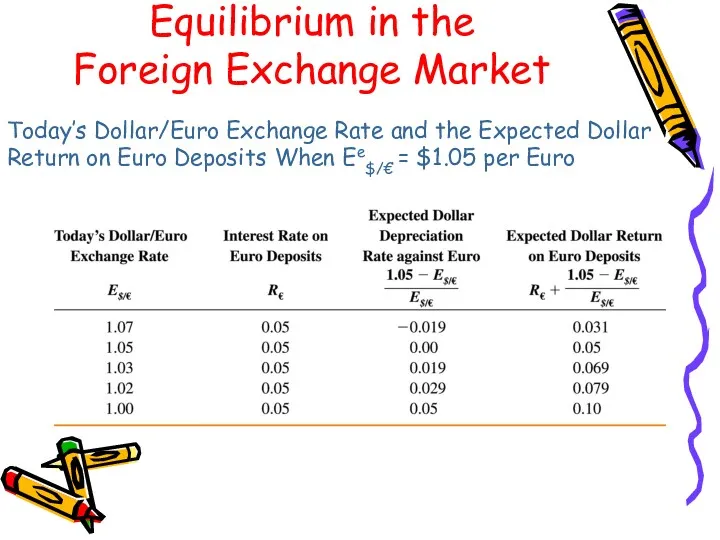

- 41. Today’s Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro Deposits When Ee$/€ = $1.05

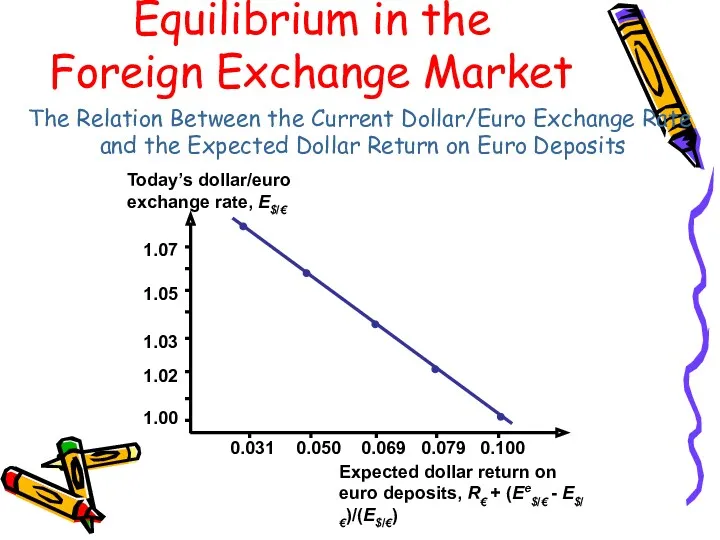

- 42. The Relation Between the Current Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro Deposits

- 43. The Equilibrium Exchange Rate Exchange rates always adjust to maintain interest parity. Assume that the dollar

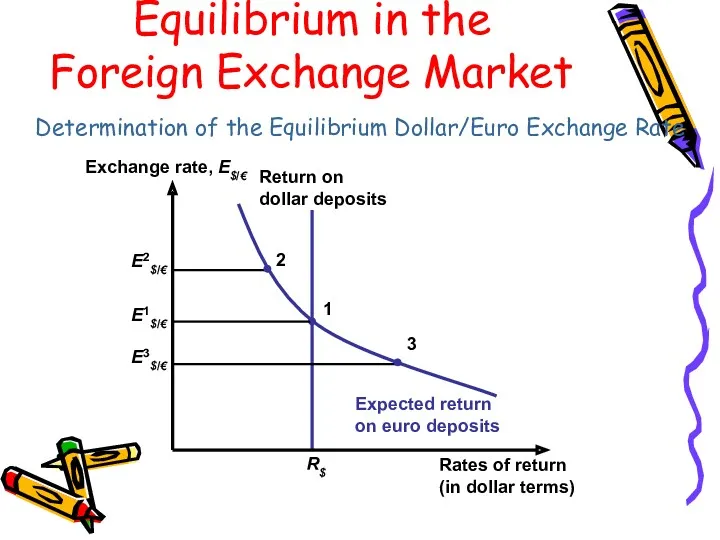

- 44. Determination of the Equilibrium Dollar/Euro Exchange Rate Equilibrium in the Foreign Exchange Market

- 45. The Effect of Changing Interest Rates on the Current Exchange Rate An increase in the interest

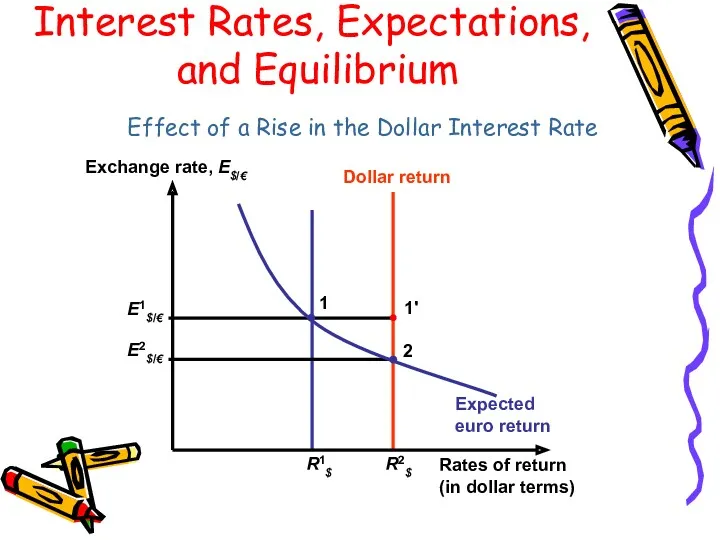

- 46. Effect of a Rise in the Dollar Interest Rate Interest Rates, Expectations, and Equilibrium

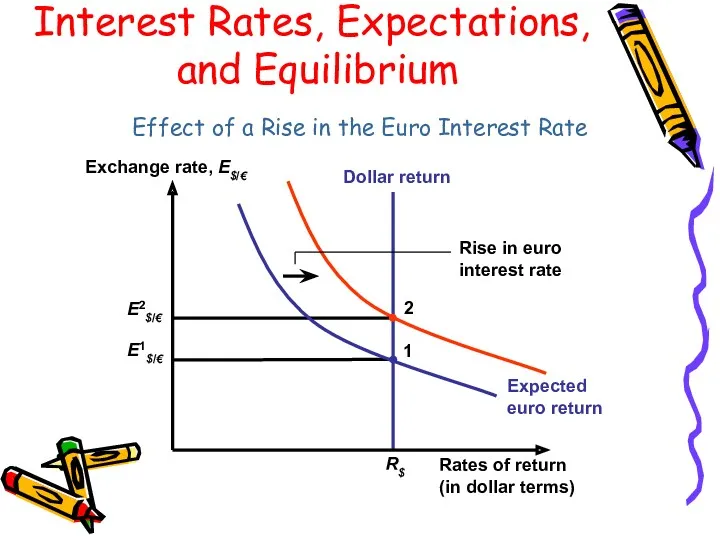

- 47. Effect of a Rise in the Euro Interest Rate Interest Rates, Expectations, and Equilibrium

- 48. The Effect of Changing Expectations on the Current Exchange Rate A rise in the expected future

- 49. Factors that influence the Exchange Rate Expectations of the Market Political Events Relative Inflation Rates Relative

- 50. Outcomes Models of exchange rate determination based on macroeconomic fundamentals have not had much success in

- 52. Скачать презентацию

Outline

Defining Exchange Rate

Measuring Exchange Rate Movements

Appreciation/Depreciation of a currency

Exchange Rate Equilibrium

Factors

Outline

Defining Exchange Rate

Measuring Exchange Rate Movements

Appreciation/Depreciation of a currency

Exchange Rate Equilibrium

Factors

Key words and concepts

Exchange rate

Depreciation

Appreciation

Balance of payments

Devaluation

Revaluation

Asset

Capital mobility

Volatility

Foreign exchange market

Determinants

Key words and concepts

Exchange rate

Depreciation

Appreciation

Balance of payments

Devaluation

Revaluation

Asset

Capital mobility

Volatility

Foreign exchange market

Determinants

What does it mean EXCHANGE RATE?

Nominal exchange rate

Spot rate

Forward rate

Bilateral exchange

What does it mean EXCHANGE RATE?

Nominal exchange rate

Spot rate

Forward rate

Bilateral exchange

Meaning of Nominal Exchange Rate

Nominal exchange rate is the relative price

Meaning of Nominal Exchange Rate

Nominal exchange rate is the relative price

Measuring Changes in Exchange Rates

A decline in a local currency’s value

Measuring Changes in Exchange Rates

A decline in a local currency’s value

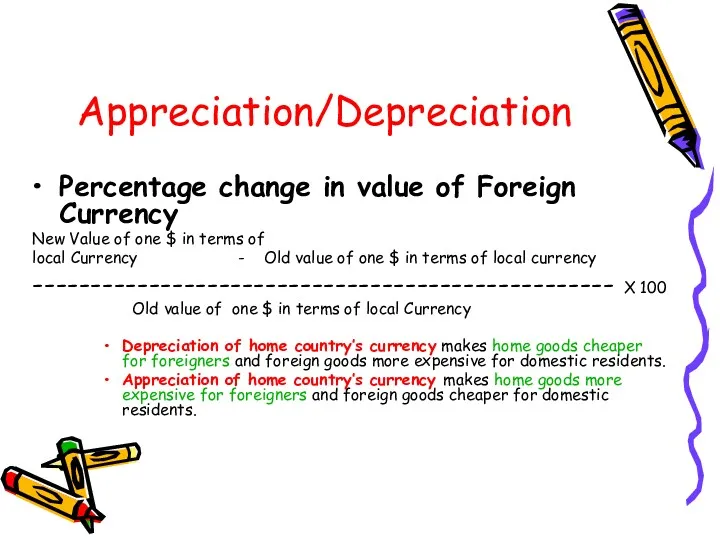

Appreciation/Depreciation

Percentage change in value of Foreign Currency

New Value of one $

Appreciation/Depreciation

Percentage change in value of Foreign Currency

New Value of one $

Exchange Rates and Relative Prices

Import and export demands are influenced by

Exchange Rates and Relative Prices

Import and export demands are influenced by

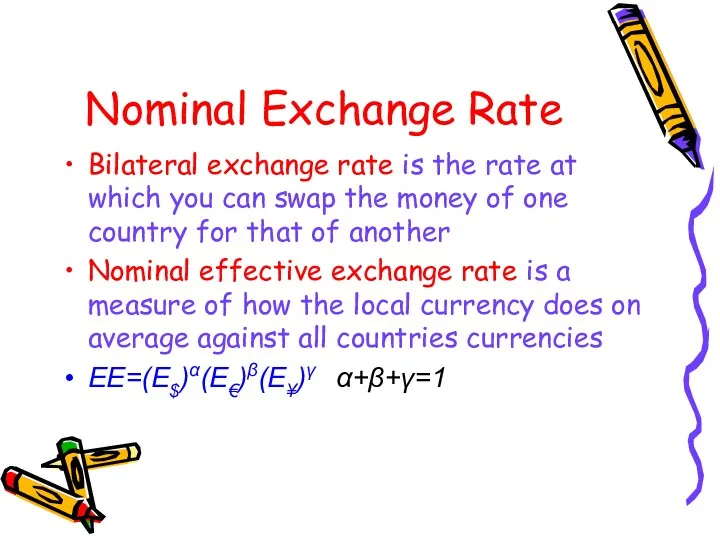

Nominal Exchange Rate

Bilateral exchange rate is the rate at which you

Nominal Exchange Rate

Bilateral exchange rate is the rate at which you

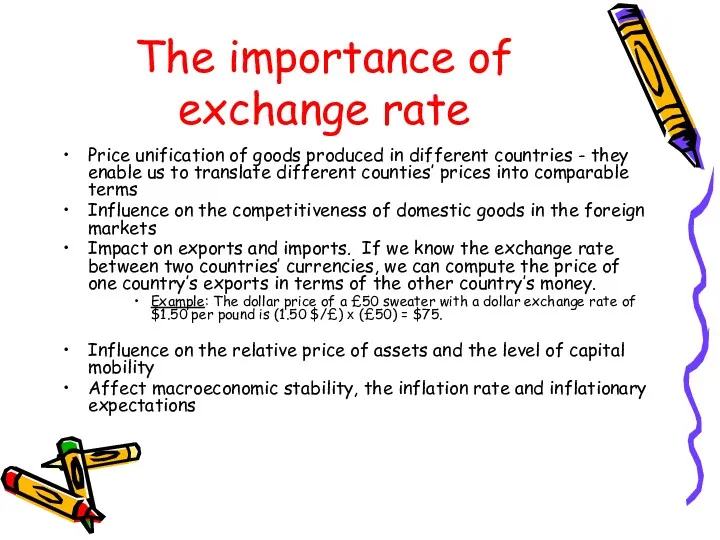

The importance of exchange rate

Price unification of goods produced in different

The importance of exchange rate

Price unification of goods produced in different

The Foreign Exchange Market

Exchange rates are determined in the foreign exchange

The Foreign Exchange Market

Exchange rates are determined in the foreign exchange

The foreign exchange market is the mechanism by which participants:

transfer purchasing

The foreign exchange market is the mechanism by which participants:

transfer purchasing

Spot Rates and Forward Rates

Spot exchange rates

Apply to exchange currencies “on

Spot Rates and Forward Rates

Spot exchange rates

Apply to exchange currencies “on

Exchange Rate Equilibrium

Forces of Demand and Supply

Demand for foreign currency negatively

Exchange Rate Equilibrium

Forces of Demand and Supply

Demand for foreign currency negatively

Foreign Exchange Market

At the equilibrium exchange rate Е* , the demand

Foreign Exchange Market

At the equilibrium exchange rate Е* , the demand

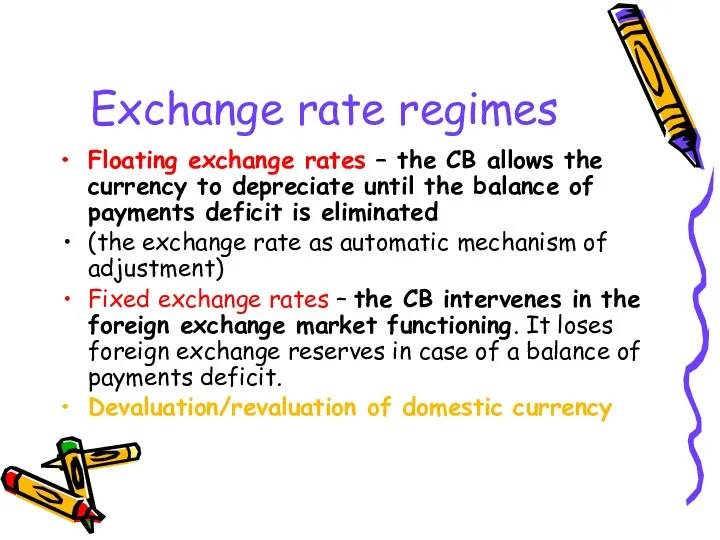

Exchange rate regimes

Floating exchange rates – the CB allows the currency

Exchange rate regimes

Floating exchange rates – the CB allows the currency

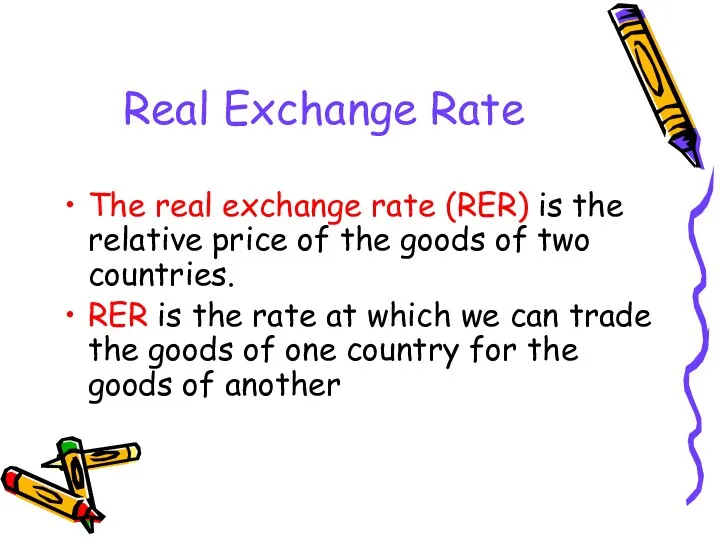

Real Exchange Rate

The real exchange rate (RER) is the relative price

Real Exchange Rate

The real exchange rate (RER) is the relative price

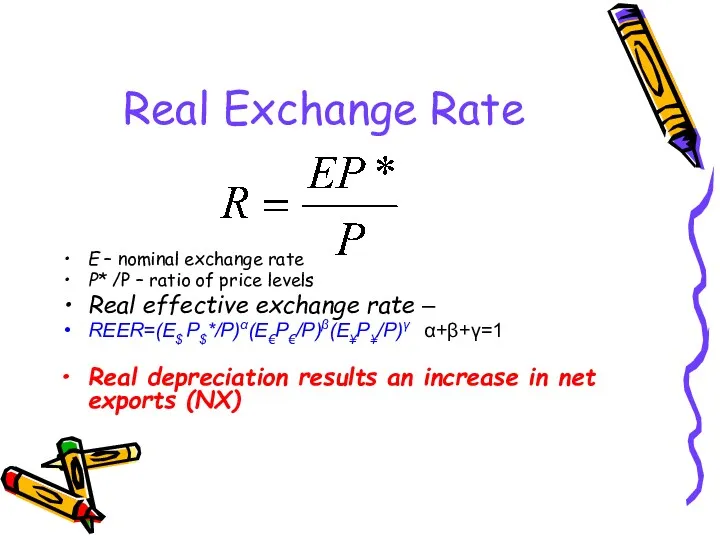

Real Exchange Rate

E – nominal exchange rate

Р* /P – ratio

Real Exchange Rate

E – nominal exchange rate

Р* /P – ratio

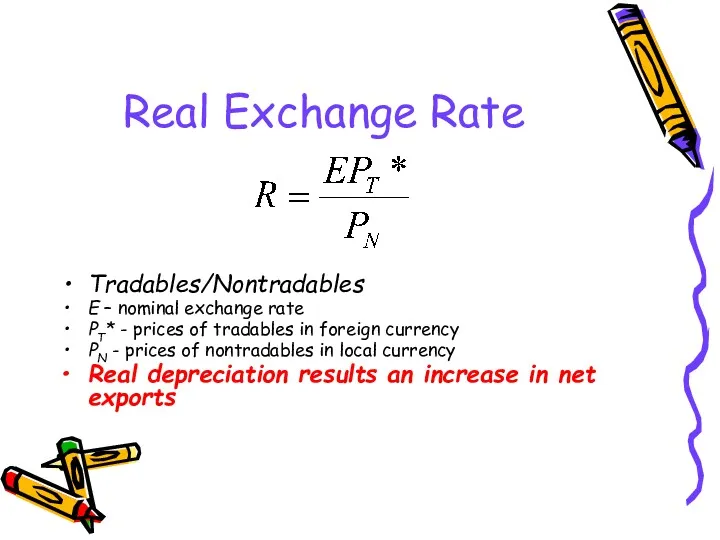

Real Exchange Rate

Tradables/Nontradables

E – nominal exchange rate

РT* - prices of tradables

Real Exchange Rate

Tradables/Nontradables

E – nominal exchange rate

РT* - prices of tradables

Real Exchange Rate

E - nominal exchange rate

W* - unit labor costs

Real Exchange Rate

E - nominal exchange rate

W* - unit labor costs

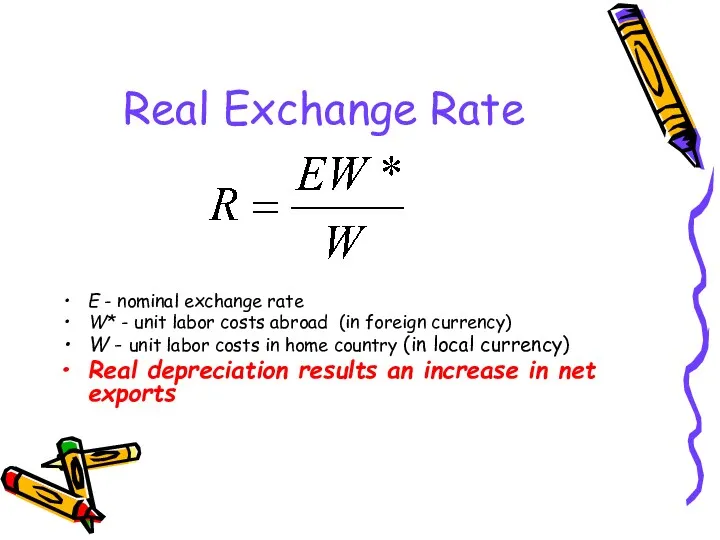

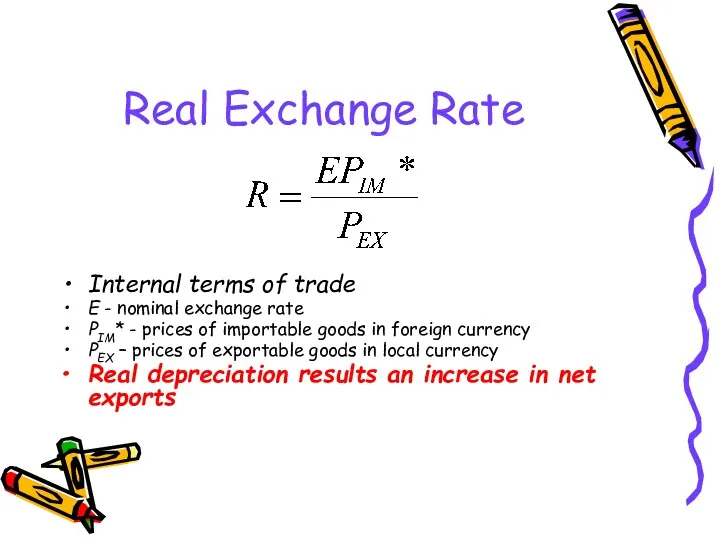

Real Exchange Rate

Internal terms of trade

E - nominal exchange rate

РIM* -

Real Exchange Rate

Internal terms of trade

E - nominal exchange rate

РIM* -

Why the RER matters

Real variable

RER determines the allocation of resources

Impact

Why the RER matters

Real variable

RER determines the allocation of resources

Impact

Current Account Theories

Current Account Theories

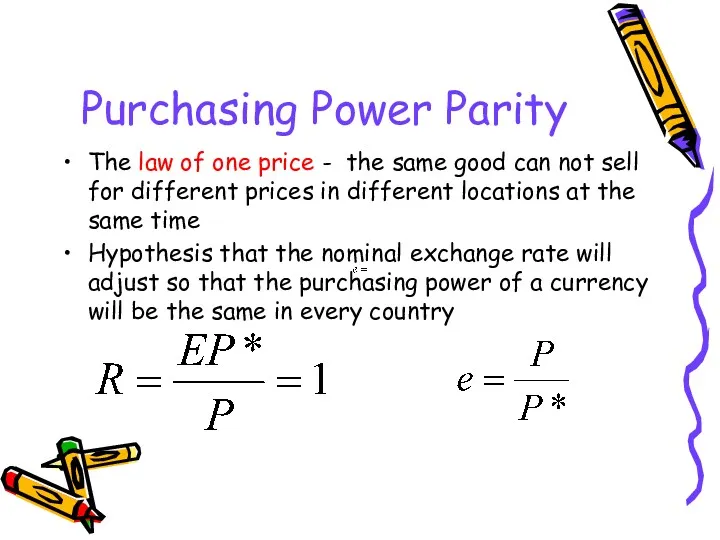

Purchasing Power Parity

The law of one price - the same good

Purchasing Power Parity

The law of one price - the same good

PPP Model as Special Case

PPP model is a special case of

PPP Model as Special Case

PPP model is a special case of

PPP Model as Special Case

Real exchange rate equation captures reality at

PPP Model as Special Case

Real exchange rate equation captures reality at

Exchange Rates in the LR

PPP holds

Relative prices are constant. Therefore,

Exchange Rates in the LR

PPP holds

Relative prices are constant. Therefore,

Monetary Approach to exchange rates and the “fundamentals” for a currency

Domestic

Monetary Approach to exchange rates and the “fundamentals” for a currency

Domestic

Exchange Rates in the SR

Commodity prices are fixed (PPP fails)

UIP and

Exchange Rates in the SR

Commodity prices are fixed (PPP fails)

UIP and

Asset Market Theories

Asset Market Theories

The demand for a foreign currency bank deposit is influenced by

The demand for a foreign currency bank deposit is influenced by

Risk and Liquidity

Savers care about two main characteristics of an asset

Risk and Liquidity

Savers care about two main characteristics of an asset

Return, Risk, and Liquidity in the Foreign Exchange Market

The demand for

Return, Risk, and Liquidity in the Foreign Exchange Market

The demand for

Interest Rates

Market participants need two pieces of information in order to

Interest Rates

Market participants need two pieces of information in order to

Exchange Rates and Asset Returns

The returns on deposits traded in the

Exchange Rates and Asset Returns

The returns on deposits traded in the

A Simple Rule

The dollar rate of return on euro deposits is

A Simple Rule

The dollar rate of return on euro deposits is

The expected rate of return difference between dollar and euro deposits

The expected rate of return difference between dollar and euro deposits

Uncovered Interest Rate Parity (UIP)

A parity condition stating that the difference

Uncovered Interest Rate Parity (UIP)

A parity condition stating that the difference

Equilibrium in the

Foreign Exchange Market

Interest Parity: The Basic Equilibrium Condition

The

Equilibrium in the

Foreign Exchange Market

Interest Parity: The Basic Equilibrium Condition

The

How Changes in the Current Exchange Rate Affect Expected Returns

Depreciation of

How Changes in the Current Exchange Rate Affect Expected Returns

Depreciation of

Today’s Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro

Today’s Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro

The Relation Between the Current Dollar/Euro Exchange Rate

and the Expected

The Relation Between the Current Dollar/Euro Exchange Rate

and the Expected

The Equilibrium Exchange Rate

Exchange rates always adjust to maintain interest parity.

Assume

The Equilibrium Exchange Rate

Exchange rates always adjust to maintain interest parity.

Assume

Determination of the Equilibrium Dollar/Euro Exchange Rate

Equilibrium in the

Foreign Exchange

Determination of the Equilibrium Dollar/Euro Exchange Rate

Equilibrium in the Foreign Exchange

The Effect of Changing Interest Rates on the Current Exchange Rate

An

The Effect of Changing Interest Rates on the Current Exchange Rate

An

Effect of a Rise in the Dollar Interest Rate

Interest Rates,

Effect of a Rise in the Dollar Interest Rate

Interest Rates,

Effect of a Rise in the Euro Interest Rate

Interest Rates, Expectations,

Effect of a Rise in the Euro Interest Rate

Interest Rates, Expectations,

The Effect of Changing Expectations on the Current Exchange Rate

A rise

The Effect of Changing Expectations on the Current Exchange Rate

A rise

Factors that influence the Exchange Rate

Expectations of the Market

Political Events

Relative

Factors that influence the Exchange Rate

Expectations of the Market

Political Events

Relative

Outcomes

Models of exchange rate determination based on

macroeconomic fundamentals have not

Outcomes

Models of exchange rate determination based on

macroeconomic fundamentals have not

Капитан Грантов. Основы грантрайтинга

Капитан Грантов. Основы грантрайтинга Structuring. Transaction Framework

Structuring. Transaction Framework История денег

История денег Организация и совершенствование финансового менеджмента на предприятии

Организация и совершенствование финансового менеджмента на предприятии Bank of England

Bank of England Доходы, расходы и прибыль организации

Доходы, расходы и прибыль организации Ақша қаражаттар қозғалысы

Ақша қаражаттар қозғалысы Порядок работы с должниками ООО ТЭК-Энерго

Порядок работы с должниками ООО ТЭК-Энерго Основы кредитно-денежной политики

Основы кредитно-денежной политики Джерела фінансування інвестицій підприємства

Джерела фінансування інвестицій підприємства Разработка и внедрение электронных документов развитие

Разработка и внедрение электронных документов развитие Федеральный стандарт бухгалтерского учета для организаций государственного сектора События после отчетной даты

Федеральный стандарт бухгалтерского учета для организаций государственного сектора События после отчетной даты Учет денежных средств и расчетов. Кассовые операции. Учет труда и заработной платы в аптечной организации

Учет денежных средств и расчетов. Кассовые операции. Учет труда и заработной платы в аптечной организации Банковские услуги

Банковские услуги Финансовая система (тема 2)

Финансовая система (тема 2) Операції банків з обслуговування платіжного обігу. Безготівкові та готівкові розрахунки. Порядок відкриття рахунків в банках

Операції банків з обслуговування платіжного обігу. Безготівкові та готівкові розрахунки. Порядок відкриття рахунків в банках Bank RBK

Bank RBK Понятие и назначение финансов

Понятие и назначение финансов Стратегии ценообразования банковских услуг

Стратегии ценообразования банковских услуг Новая продуктовая линейка АО Микрофинансовая компания Пермского края при финансовой поддержке Правительства Пермского края

Новая продуктовая линейка АО Микрофинансовая компания Пермского края при финансовой поддержке Правительства Пермского края Объекты учета затрат в системе управленческого учета. (Лекция 3)

Объекты учета затрат в системе управленческого учета. (Лекция 3) Дидактические игры по формированию основ финансовой грамотности у детей старшего дошкольного возраста

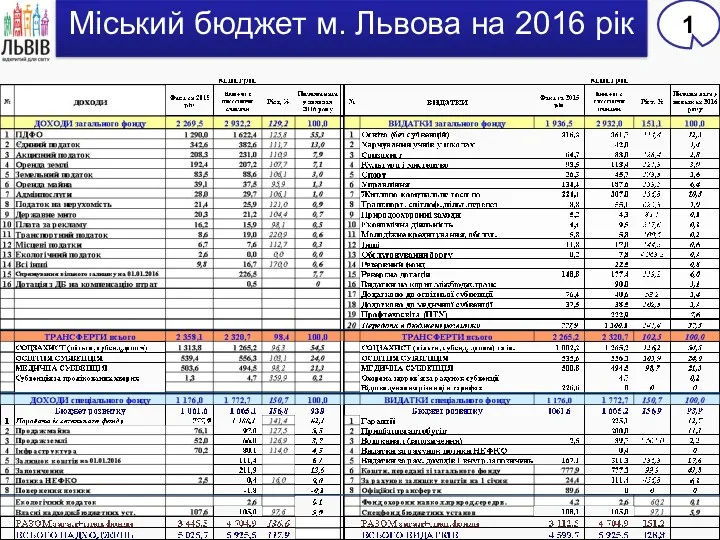

Дидактические игры по формированию основ финансовой грамотности у детей старшего дошкольного возраста Міський бюджет м. Львова на 2016 рік

Міський бюджет м. Львова на 2016 рік Корректировка плана МТО ООО Таргин

Корректировка плана МТО ООО Таргин Надёжность и гарантии. Страховая компания Metlife Alico в Украине

Надёжность и гарантии. Страховая компания Metlife Alico в Украине Формирование бюджетов ОГВ и ОМСУ

Формирование бюджетов ОГВ и ОМСУ Всемирные (международные) экономические отношения

Всемирные (международные) экономические отношения Бухгалтерский баланс

Бухгалтерский баланс