- Working capital and Cash management

Содержание

- 2. Management of Working Capital The owners of any company make two major investments of capital in

- 3. Working Capital Working Capital may be defined as the necessary investment in stock and cash to

- 4. Working Capital Working Capital – the difference between current assets and current liabilities of the company.

- 5. Current Assets Current assets consist of cash, marketable securities, notes receivable, credit card receivables, accounts receivable,

- 6. Current Liabilities Current liabilities consist of accounts payable, accrued expenses (wages and salaries payable, interest payable,

- 7. Hotels and restaurants should minimize the amount of working capital needed to operate the business. Any

- 8. The amount of working capital your business needs to operate is a function of several factors:

- 9. How to get it low? • Offer a discount on cash sales • Turn your inventories

- 10. Working Capital analysis Working capital analysis evaluates changes to working capital over an operating period for

- 11. Working Capital analysis Working capital analysis evaluates changes to working capital over an operating period for

- 12. Management of Working Capital From the point of view of the impact on the working capital,

- 13. Inflows – Sources of Working Capital The following are the major inflows or sources that will

- 14. Inflows – Sources of Working Capital The following are the major inflows or sources that will

- 15. Inflows – Sources of Working Capital The following are the major inflows or sources that will

- 16. Inflows – Sources of Working Capital The following are the major inflows or sources that will

- 17. Inflows – Sources of Working Capital The following are the major inflows or sources that will

- 18. Outflows – Uses of Working Capital The following are the major outflows or uses that will

- 19. Outflows – Uses of Working Capital The following are the major outflows or uses that will

- 20. Outflows – Uses of Working Capital The following are the major outflows or uses that will

- 21. Outflows – Uses of Working Capital The following are the major outflows or uses that will

- 22. Transactions which have no effect on working capital: The purchase of fixed assets financed by a

- 23. Management must control the amount of cash tied up in working capital. The amount of working

- 24. Working Capital Cycle is the length of time a business has to wait between expending its

- 25. Controlling the key items Stock: regular stock-taking, reviewing the system of stock receipt and quality of

- 26. Cash is the one asset that is convertible into any other type of asset. It is

- 27. Whether or not the hotel takes in enough cash in a day to cover all these

- 28. Ratio analysis using the Statement of Cash Flows

- 29. Ratio analysis using the CFS The cash flow from operating activities to current liabilities ratio is

- 30. Ratio analysis using the CFS The cash flow from operating activities to total liabilities ratio considers

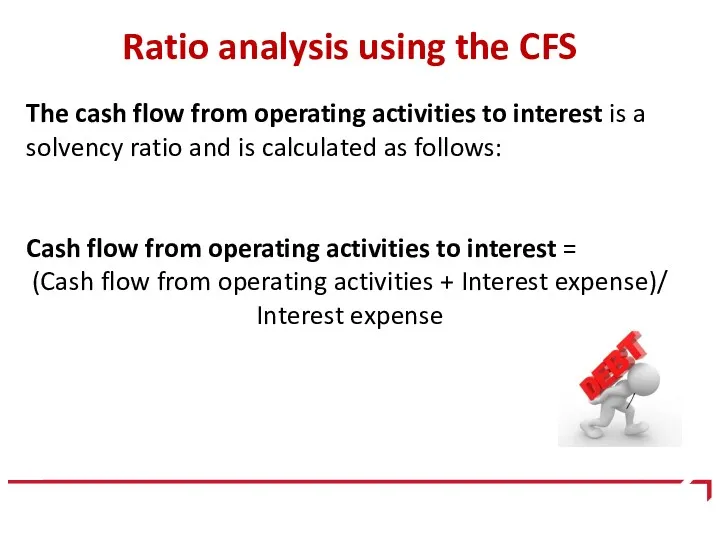

- 31. Ratio analysis using the CFS The cash flow from operating activities to interest is a solvency

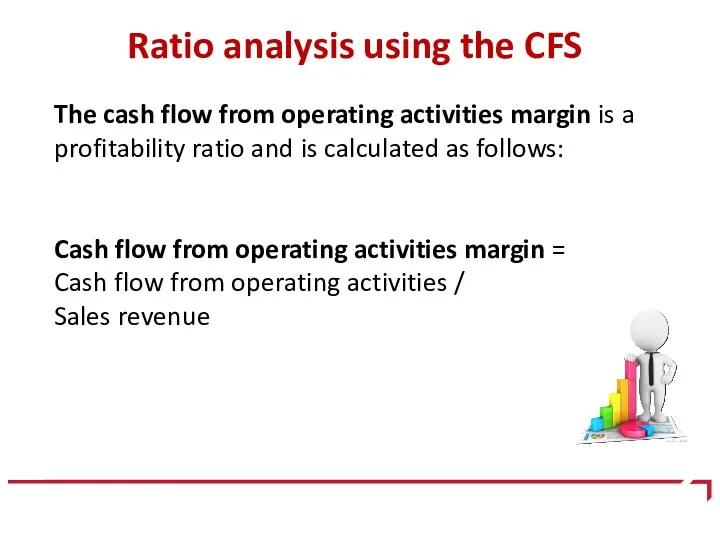

- 32. Ratio analysis using the CFS The cash flow from operating activities margin is a profitability ratio

- 34. Скачать презентацию

Management of Working Capital

The owners of any company make two major

Management of Working Capital

The owners of any company make two major

Working Capital

Working Capital may be defined as the necessary investment in

Working Capital

Working Capital may be defined as the necessary investment in

Working Capital

Working Capital – the difference between current assets and current

Working Capital

Working Capital – the difference between current assets and current

Current Assets

Current assets consist of

cash,

marketable securities,

notes receivable,

credit card

Current Assets

Current assets consist of

cash,

marketable securities,

notes receivable,

credit card

Current Liabilities

Current liabilities consist of

accounts payable,

accrued expenses (wages and

Current Liabilities

Current liabilities consist of

accounts payable,

accrued expenses (wages and

Hotels and restaurants should minimize the amount of working capital needed

Hotels and restaurants should minimize the amount of working capital needed

The amount of working capital your business needs to

operate is a

The amount of working capital your business needs to operate is a

How to get it low?

• Offer a discount on cash sales

•

How to get it low? • Offer a discount on cash sales •

Working Capital analysis

Working capital analysis evaluates changes to working capital over

Working Capital analysis

Working capital analysis evaluates changes to working capital over

Working Capital analysis

Working capital analysis evaluates changes to working capital over

Working Capital analysis

Working capital analysis evaluates changes to working capital over

Management of Working Capital

From the point of view of the impact

Management of Working Capital

From the point of view of the impact

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Inflows – Sources of Working Capital

The following are the major inflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Outflows – Uses of Working Capital

The following are the major outflows

Transactions which have no effect on working capital:

The purchase of fixed

Transactions which have no effect on working capital:

The purchase of fixed

Management must control the amount of cash tied up in working

Management must control the amount of cash tied up in working

Working Capital Cycle is the length of time a business has

Working Capital Cycle is the length of time a business has

Controlling the key items

Stock: regular stock-taking, reviewing the system of stock

Controlling the key items

Stock: regular stock-taking, reviewing the system of stock

Cash is the one asset that is convertible into any other

Cash is the one asset that is convertible into any other

Whether or not the hotel takes in enough cash in a

Whether or not the hotel takes in enough cash in a

Ratio analysis using the Statement of Cash Flows

Ratio analysis using the Statement of Cash Flows

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities to

Ratio analysis using the CFS

The cash flow from operating activities margin

Ratio analysis using the CFS

The cash flow from operating activities margin

Управление обязательствами банка

Управление обязательствами банка Налогообложение предприятий АПК. Налог на прибыль организаций. (Тема 2)

Налогообложение предприятий АПК. Налог на прибыль организаций. (Тема 2) Эффективность рекламной деятельности универсальных магазинов

Эффективность рекламной деятельности универсальных магазинов Тетрадь по обучению участника учебного трека. Хоум Кредит Банк

Тетрадь по обучению участника учебного трека. Хоум Кредит Банк Анализ затрат на производство продукции организации

Анализ затрат на производство продукции организации Банковская система и кредитно-денежная политика. Лекция 4

Банковская система и кредитно-денежная политика. Лекция 4 Особенности налогообложения

Особенности налогообложения Форма и система оплаты труда. Виды заработной платы. Начисление и синтетический учет заработной платы. Лекция №19

Форма и система оплаты труда. Виды заработной платы. Начисление и синтетический учет заработной платы. Лекция №19 Этапы бюджетного процесса

Этапы бюджетного процесса Разработка направлений совершенствования коммерческой деятельности по организации договорной работы

Разработка направлений совершенствования коммерческой деятельности по организации договорной работы Акцизний податок

Акцизний податок Виды обеспечения в связи с несчастными случаями на производстве и профессиональными заболеваниями

Виды обеспечения в связи с несчастными случаями на производстве и профессиональными заболеваниями Управление дебиторской и кредиторской задолженностью организации АО Компания Росинка, г. Липецк

Управление дебиторской и кредиторской задолженностью организации АО Компания Росинка, г. Липецк Сущность и значение бюджета и бюджетной системы Российской Федерации

Сущность и значение бюджета и бюджетной системы Российской Федерации Сравнительный подход к оценке стоимости предприятия

Сравнительный подход к оценке стоимости предприятия Тема 7. Необходимость и сущность кредита

Тема 7. Необходимость и сущность кредита Денежно – кредитная система

Денежно – кредитная система Российские научные фонды. Как получить свой первый грант?

Российские научные фонды. Как получить свой первый грант? Современный государственный бюджет РФ, проблемы формирования и исполнения

Современный государственный бюджет РФ, проблемы формирования и исполнения Сводка и группровка статистических данных

Сводка и группровка статистических данных Особенности финансового планирования ФГКУ ПСЧ МЧС России

Особенности финансового планирования ФГКУ ПСЧ МЧС России Экономическая сущность и природа налогов

Экономическая сущность и природа налогов Финансовые рынки и финансовые институты

Финансовые рынки и финансовые институты КАСКО - добровольное страхование транспортного средства

КАСКО - добровольное страхование транспортного средства Страхование багажа (кросс-продукт к ОСАГО)

Страхование багажа (кросс-продукт к ОСАГО) Перспективы создания международного финансового центра в Москве

Перспективы создания международного финансового центра в Москве Технология бизнес-планирования. Содержание бизнес-плана. (Раздел 2.5)

Технология бизнес-планирования. Содержание бизнес-плана. (Раздел 2.5) Что такое деньги. 3 класс

Что такое деньги. 3 класс