- International financial reporting standards. Balance sheet

Содержание

- 2. Minority the portion of a subsidiary corporation's stock that is not owned by the parent corporation.

- 3. Balance Sheet. Fixed assets Investment Property Intangible assets Financial assets Investment using the equity method Inventories

- 4. Fixed assets a long-term tangible piece of property that a firm owns and uses in the

- 5. Investment property (IAS 40) Investment property is property (land or a building or part of a

- 6. Intangible assets (IAS 38) non-monetary assets which are without physical substance and identifiable (either being separable

- 7. Financial assets (IAS 39, IFRS 9) A financial asset is a tangible liquid asset that derives

- 8. Investment using the equity method http://www.investopedia.com/terms/e/equitymethod.asp?ad=dirN&qo=investopediaSiteSearch&qsrc=0&o=40186

- 9. Inventories (IAS 2) Inventories include: assets held for sale in the ordinary course of business (finished

- 10. Accounts receivable Accounts receivable refers to the outstanding invoices a company has or the money the

- 11. Cash and cash equivalents (IAS 7) Cash and cash equivalents refer to the line item on

- 12. Deferred and current tax assets Deferred tax asset is an accounting term that refers to a

- 13. Deferred and current tax liabilities A deferred tax liability is an account on a company's balance

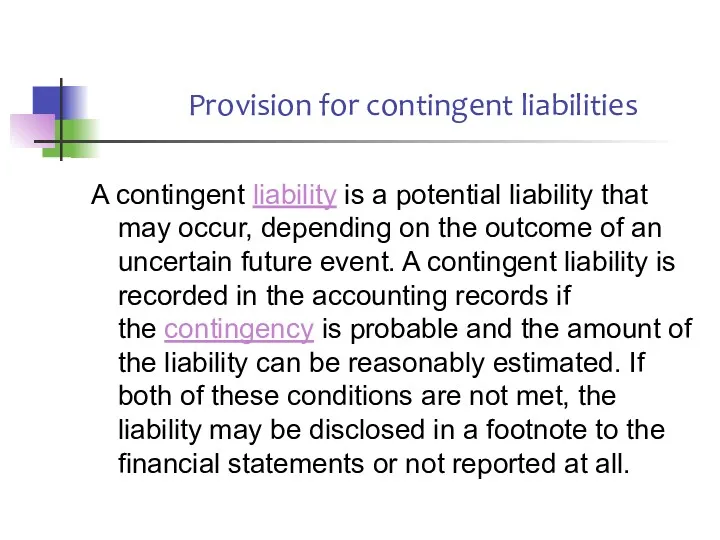

- 14. Provision for contingent liabilities A contingent liability is a potential liability that may occur, depending on

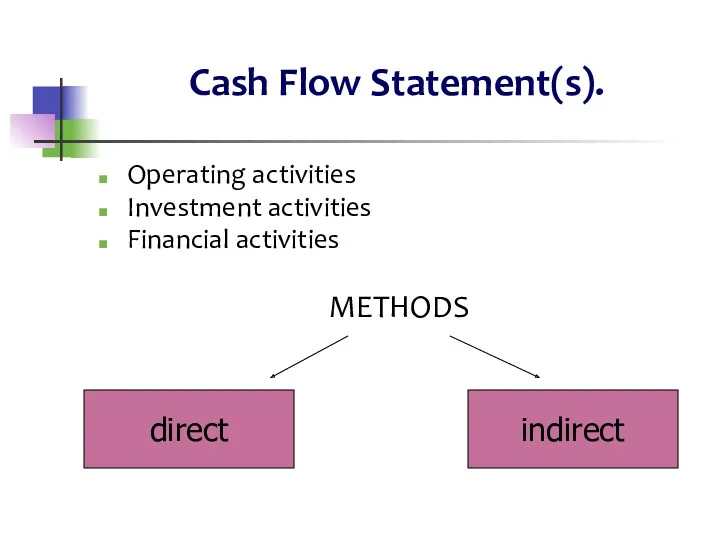

- 15. Cash Flow Statement(s). Operating activities Investment activities Financial activities METHODS direct indirect

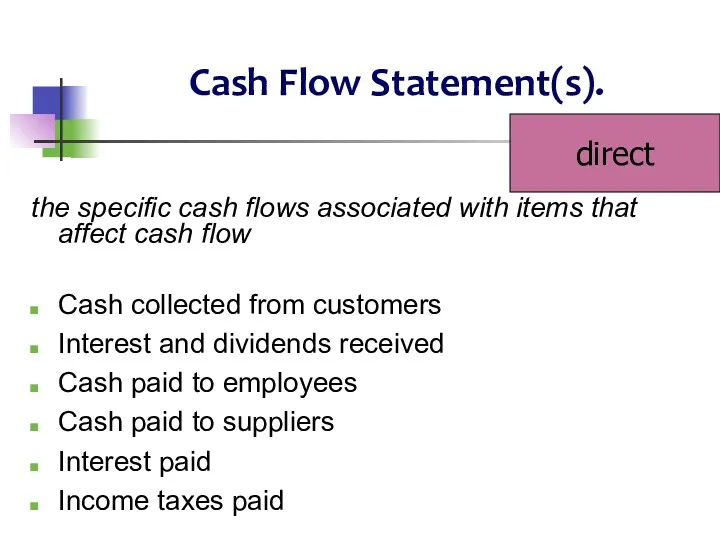

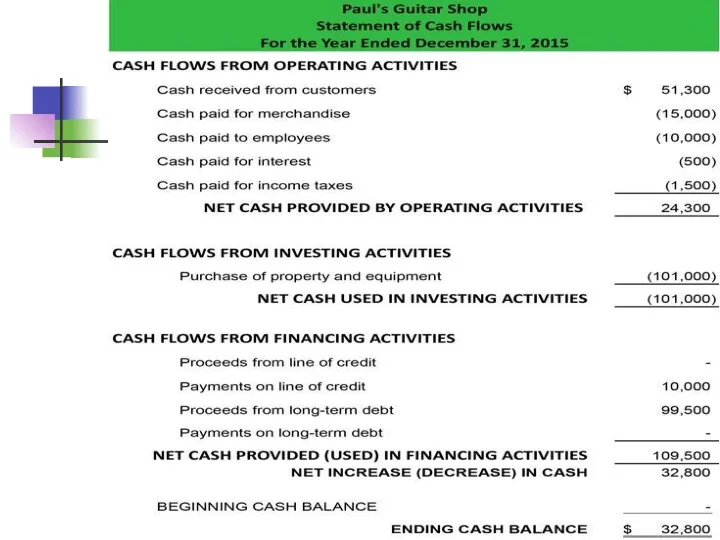

- 16. Cash Flow Statement(s). the specific cash flows associated with items that affect cash flow Cash collected

- 18. Cash Flow Statement(s). the sources and uses of cash by a business the presentation of this

- 20. Statement of Changes in Own Equity. Basic approach Profit / loss for the period Profit /

- 22. Скачать презентацию

Minority

the portion of a subsidiary corporation's stock that is not owned

Minority

the portion of a subsidiary corporation's stock that is not owned

Balance Sheet.

Fixed assets

Investment Property

Intangible assets

Financial assets

Investment using the equity method

Inventories

Disposal assets

Balance Sheet.

Fixed assets

Investment Property

Intangible assets

Financial assets

Investment using the equity method

Inventories

Disposal assets

Fixed assets

a long-term tangible piece of property that a firm owns

Fixed assets

a long-term tangible piece of property that a firm owns

Investment property (IAS 40)

Investment property is property (land or a building or

Investment property (IAS 40)

Investment property is property (land or a building or

Intangible assets (IAS 38)

non-monetary assets which are without physical substance and

Intangible assets (IAS 38)

non-monetary assets which are without physical substance and

Financial assets (IAS 39, IFRS 9)

A financial asset is a tangible liquid

Financial assets (IAS 39, IFRS 9)

A financial asset is a tangible liquid

Investment using the equity method

http://www.investopedia.com/terms/e/equitymethod.asp?ad=dirN&qo=investopediaSiteSearch&qsrc=0&o=40186

Investment using the equity method

http://www.investopedia.com/terms/e/equitymethod.asp?ad=dirN&qo=investopediaSiteSearch&qsrc=0&o=40186

Inventories (IAS 2)

Inventories include:

assets held for sale in the ordinary

Inventories (IAS 2)

Inventories include:

assets held for sale in the ordinary

Accounts receivable

Accounts receivable refers to the outstanding invoices a company

Accounts receivable

Accounts receivable refers to the outstanding invoices a company

Cash and cash equivalents (IAS 7)

Cash and cash equivalents refer to the line

Cash and cash equivalents (IAS 7)

Cash and cash equivalents refer to the line

Deferred and current tax assets

Deferred tax asset is an accounting term

Deferred and current tax assets

Deferred tax asset is an accounting term

Deferred and current tax liabilities

A deferred tax liability is an account

Deferred and current tax liabilities

A deferred tax liability is an account

Provision for contingent liabilities

A contingent liability is a potential liability that may occur,

Provision for contingent liabilities

A contingent liability is a potential liability that may occur,

Cash Flow Statement(s).

Operating activities

Investment activities

Financial activities

METHODS

direct

indirect

Cash Flow Statement(s).

Operating activities

Investment activities

Financial activities

METHODS

direct

indirect

Cash Flow Statement(s).

the specific cash flows associated with items that affect

Cash Flow Statement(s).

the specific cash flows associated with items that affect

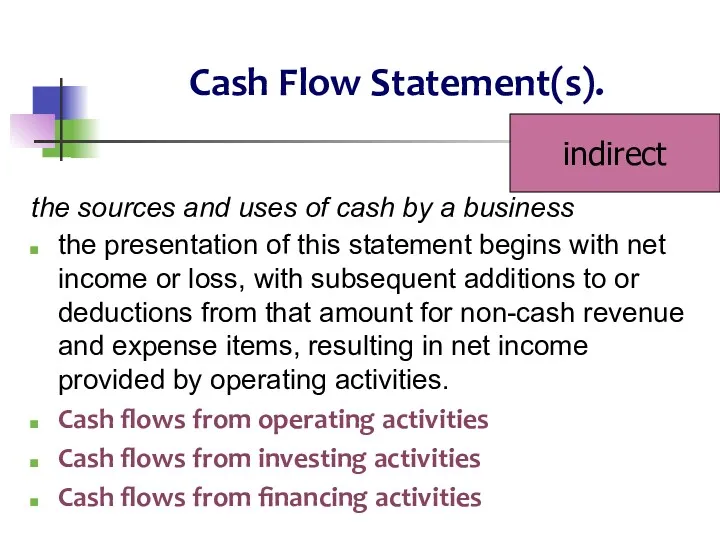

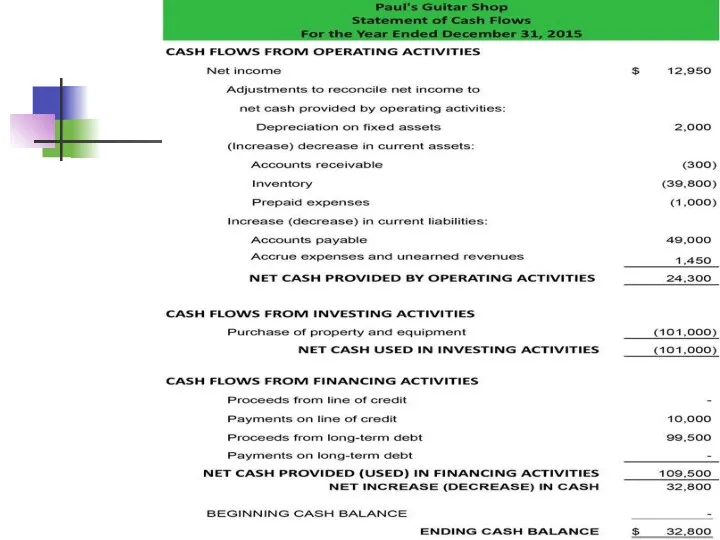

Cash Flow Statement(s).

the sources and uses of cash by a business

the

Cash Flow Statement(s).

the sources and uses of cash by a business

the

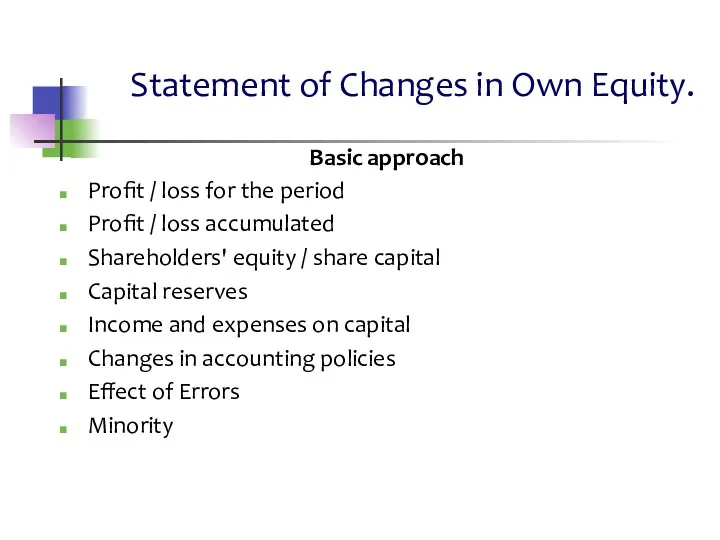

Statement of Changes in Own Equity.

Basic approach

Profit / loss for the

Statement of Changes in Own Equity.

Basic approach

Profit / loss for the

Налог на доходы физических лиц

Налог на доходы физических лиц Античне страхування

Античне страхування Кроссворд по финансовой грамотности дошкольников 5-7 лет

Кроссворд по финансовой грамотности дошкольников 5-7 лет Судебные споры, банкротство и субсидиарная ответственность в финансовом секторе

Судебные споры, банкротство и субсидиарная ответственность в финансовом секторе Денежные фонды и резервы организации

Денежные фонды и резервы организации Структура и содержание внешнеторгового контракта

Структура и содержание внешнеторгового контракта Страхование в банковском секторе. Проблемы и меры по усовершенствованию

Страхование в банковском секторе. Проблемы и меры по усовершенствованию Оплата труда

Оплата труда Таможенные платежи в ЕАЭС: общая характеристика и назначение

Таможенные платежи в ЕАЭС: общая характеристика и назначение Fortebank

Fortebank Зарплатный проект Росбанка

Зарплатный проект Росбанка Налоговый контроль

Налоговый контроль Аудит достоверности строк финансовой отчетности организации

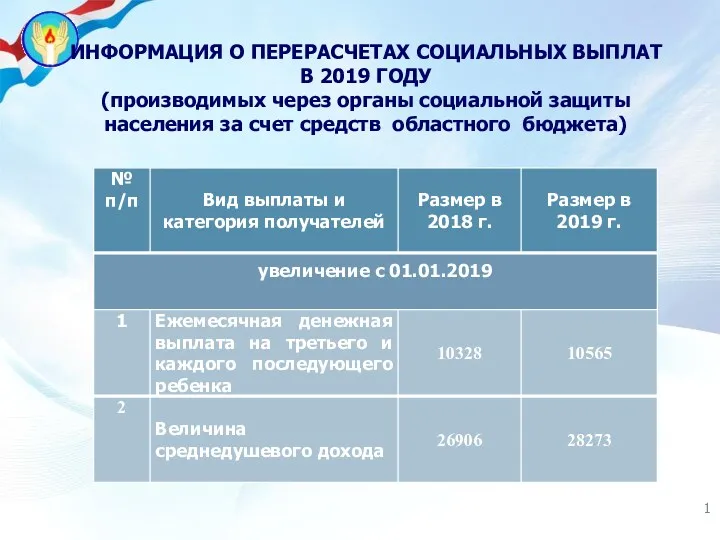

Аудит достоверности строк финансовой отчетности организации Информация о перерасчетах социальных выплат (через органы социальной защиты населения за счет средств областного бюджета)

Информация о перерасчетах социальных выплат (через органы социальной защиты населения за счет средств областного бюджета) Кредит - жизнь в долг или способ удовлетворения потребностей

Кредит - жизнь в долг или способ удовлетворения потребностей Основные принципы кадровой и социальной работы ПАО НК Роснефть

Основные принципы кадровой и социальной работы ПАО НК Роснефть Организация документооборота и внутреннего контроля в бухгалтерском учете коммерческого банка

Организация документооборота и внутреннего контроля в бухгалтерском учете коммерческого банка The world of money

The world of money Понятие налоговой системы и ее элементы

Понятие налоговой системы и ее элементы Аудит учета матариально-производственных запасов и готовой продукции

Аудит учета матариально-производственных запасов и готовой продукции Экономическая сущность и природа налогов

Экономическая сущность и природа налогов НДФЛ-2016. Внесение изменения в статью 218 части второй Налогового кодекса РФ

НДФЛ-2016. Внесение изменения в статью 218 части второй Налогового кодекса РФ Фінанси домогосподарств

Фінанси домогосподарств Қаржы нарығы және делдалдары

Қаржы нарығы және делдалдары Заработная плата и факторы, влияющие на ее размер

Заработная плата и факторы, влияющие на ее размер Организация финансов коммерческих организаций в современных условиях

Организация финансов коммерческих организаций в современных условиях Учёт денежных средств

Учёт денежных средств Price Equilibrium 11.2a

Price Equilibrium 11.2a