- Principles of Business Finance. Lecture 2: Financial Statements

Содержание

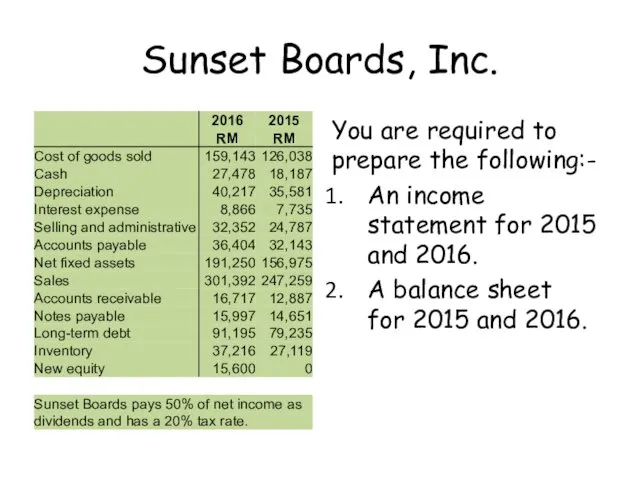

- 2. Sunset Boards, Inc. You are required to prepare the following:- An income statement for 2015 and

- 3. Learning Outcomes By the end of this lecture, you should be able to:- know the balance

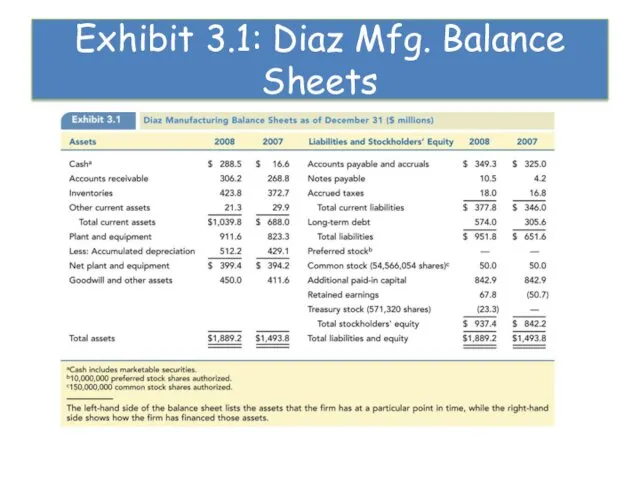

- 4. Exhibit 3.1: Diaz Mfg. Balance Sheets

- 5. The Balance Sheet Reports the firm’s financial position at a particular point in time. Assets: Liabilities:

- 6. The Balance Sheet Current assets and liabilities Net working capital Accounting for inventory Long term assets

- 7. Market Value Vs. Book Value Values shown on the b/s for the firm’s assets are book

- 8. A More Informative Balance Sheet Assets Liabilities Stockholders’ equity

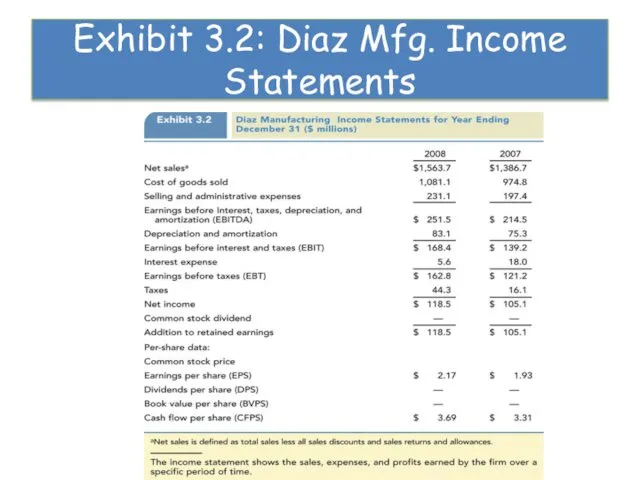

- 9. The Income Statement & The Statement of Retained Earnings I/S shows how profitable a firm is

- 10. Exhibit 3.2: Diaz Mfg. Income Statements

- 11. Expense Categories Depreciation expense Amortization expense Extraordinary items

- 12. The Statement of Retained Earnings Two events that affect the retained earnings account balance:- Firm reports

- 13. Cash Flows Goal of financial management is to maximize the value of stockholders’ shares which means

- 14. The Statement of Cash Flows The detail of all the cash flows that have taken place

- 15. Sources and Uses of Cash Shows the firm’s cash inflows and cash outflows for a period

- 16. Let’s try this… Increase of CA Increase of CL Increase of FA Decrease of FA Increase

- 17. Sources and Uses of Cash Working capital Fixed assets Long term liabilities and equity Dividends

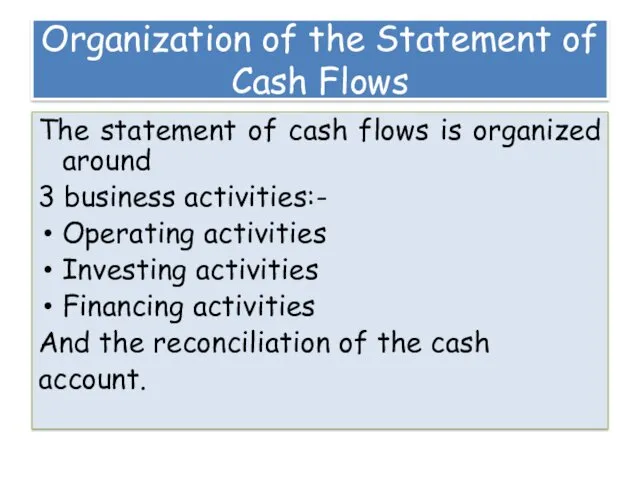

- 18. Organization of the Statement of Cash Flows The statement of cash flows is organized around 3

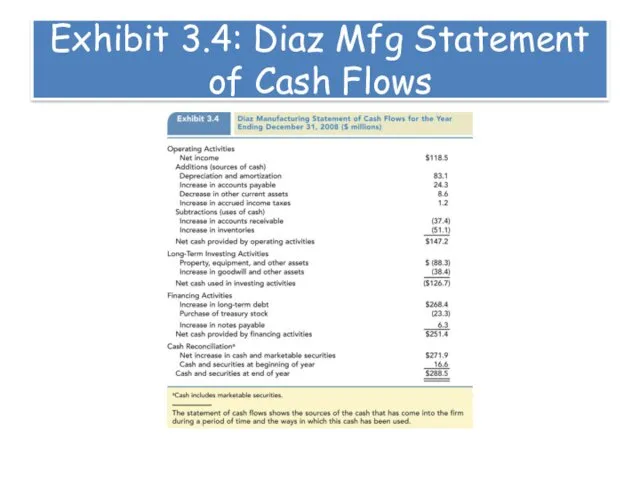

- 19. Exhibit 3.4: Diaz Mfg Statement of Cash Flows

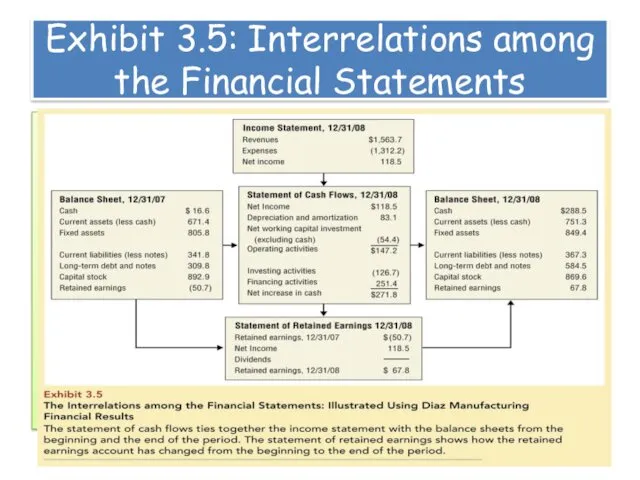

- 20. Exhibit 3.5: Interrelations among the Financial Statements

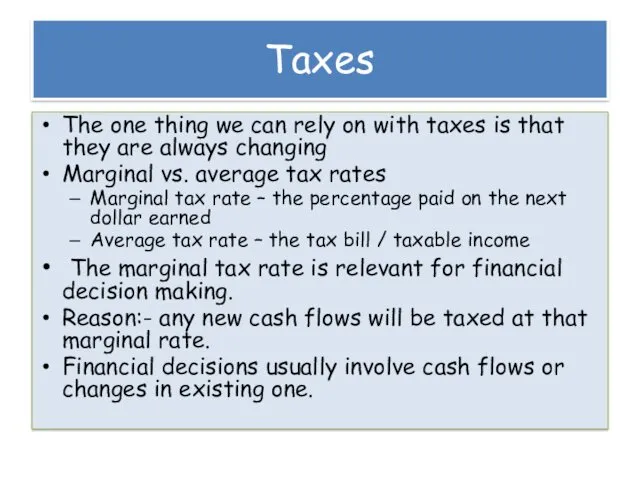

- 21. Taxes The one thing we can rely on with taxes is that they are always changing

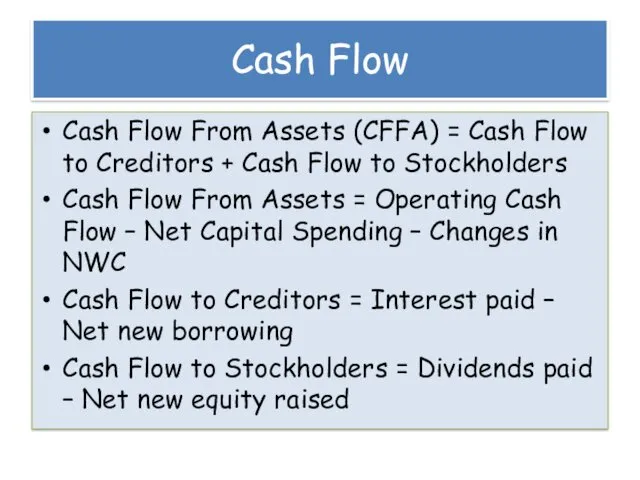

- 22. Cash Flow Cash Flow From Assets (CFFA) = Cash Flow to Creditors + Cash Flow to

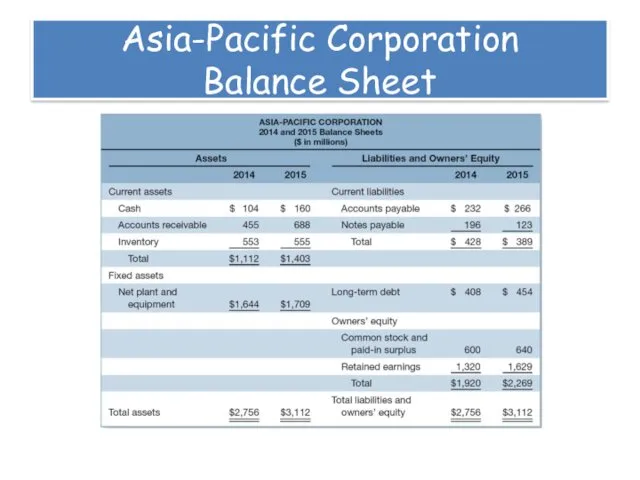

- 23. Asia-Pacific Corporation Balance Sheet

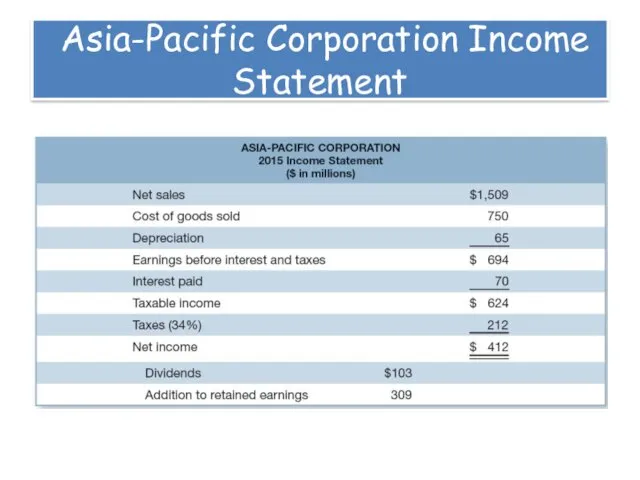

- 24. Asia-Pacific Corporation Income Statement

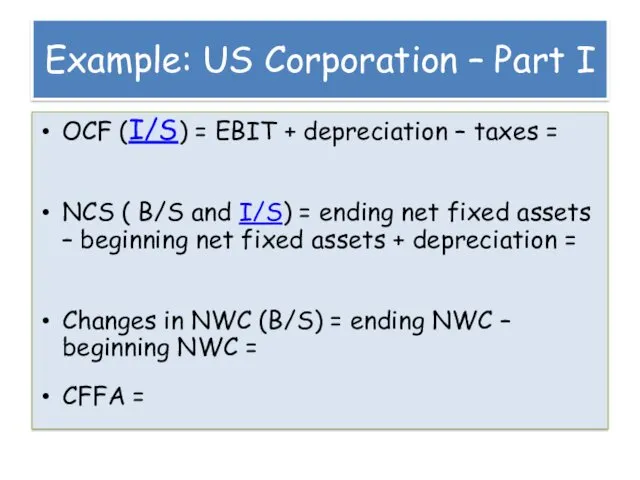

- 25. Example: US Corporation – Part I OCF (I/S) = EBIT + depreciation – taxes = NCS

- 26. Example: US Corporation – Part II CF to Creditors (B/S and I/S) = interest paid –

- 27. Cash Flow Summary - Table 2.6

- 29. Скачать презентацию

Sunset Boards, Inc.

You are required to prepare the following:-

An income statement

Sunset Boards, Inc.

You are required to prepare the following:-

An income statement

Learning Outcomes

By the end of this lecture, you should be able

Learning Outcomes

By the end of this lecture, you should be able

Exhibit 3.1: Diaz Mfg. Balance Sheets

Exhibit 3.1: Diaz Mfg. Balance Sheets

The Balance Sheet

Reports the firm’s financial position at a particular point

The Balance Sheet

Reports the firm’s financial position at a particular point

The Balance Sheet

Current assets and liabilities

Net working capital

Accounting for inventory

Long term

The Balance Sheet

Current assets and liabilities

Net working capital

Accounting for inventory

Long term

Market Value Vs. Book Value

Values shown on the b/s for the

Market Value Vs. Book Value

Values shown on the b/s for the

A More Informative Balance Sheet

Assets

Liabilities

Stockholders’ equity

A More Informative Balance Sheet

Assets

Liabilities

Stockholders’ equity

The Income Statement & The Statement of Retained Earnings

I/S shows how

The Income Statement & The Statement of Retained Earnings

I/S shows how

Exhibit 3.2: Diaz Mfg. Income Statements

Exhibit 3.2: Diaz Mfg. Income Statements

Expense Categories

Depreciation expense

Amortization expense

Extraordinary items

Expense Categories

Depreciation expense

Amortization expense

Extraordinary items

The Statement of Retained Earnings

Two events that affect the retained

earnings account

The Statement of Retained Earnings

Two events that affect the retained

earnings account

Cash Flows

Goal of financial management is to maximize the value of

Cash Flows

Goal of financial management is to maximize the value of

The Statement of Cash Flows

The detail of all the cash flows

The Statement of Cash Flows

The detail of all the cash flows

Sources and Uses of Cash

Shows the firm’s cash inflows and cash

Sources and Uses of Cash

Shows the firm’s cash inflows and cash

Let’s try this…

Increase of CA

Increase of CL

Increase of FA

Decrease of FA

Increase

Let’s try this…

Increase of CA

Increase of CL

Increase of FA

Decrease of FA

Increase

Sources and Uses of Cash

Working capital

Fixed assets

Long term liabilities and equity

Dividends

Sources and Uses of Cash

Working capital

Fixed assets

Long term liabilities and equity

Dividends

Organization of the Statement of Cash Flows

The statement of cash flows

Organization of the Statement of Cash Flows

The statement of cash flows

Exhibit 3.4: Diaz Mfg Statement of Cash Flows

Exhibit 3.4: Diaz Mfg Statement of Cash Flows

Exhibit 3.5: Interrelations among the Financial Statements

Exhibit 3.5: Interrelations among the Financial Statements

Taxes

The one thing we can rely on with taxes is that

Taxes

The one thing we can rely on with taxes is that

Cash Flow

Cash Flow From Assets (CFFA) = Cash Flow to Creditors

Cash Flow

Cash Flow From Assets (CFFA) = Cash Flow to Creditors

Asia-Pacific Corporation

Balance Sheet

Asia-Pacific Corporation

Balance Sheet

Asia-Pacific Corporation Income Statement

Asia-Pacific Corporation Income Statement

Example: US Corporation – Part I

OCF (I/S) = EBIT + depreciation

Example: US Corporation – Part I

OCF (I/S) = EBIT + depreciation

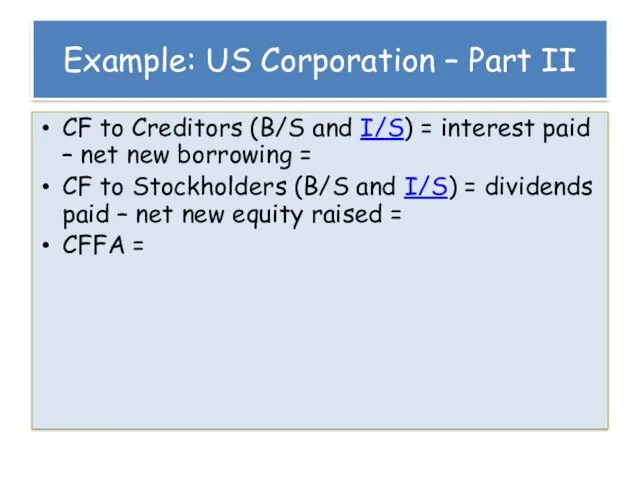

Example: US Corporation – Part II

CF to Creditors (B/S and I/S)

Example: US Corporation – Part II

CF to Creditors (B/S and I/S)

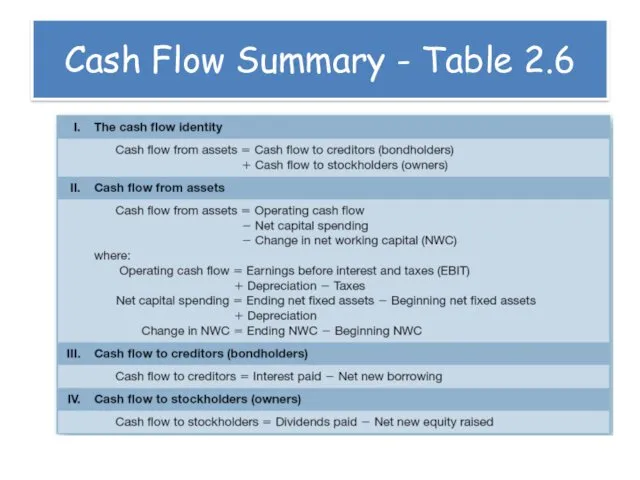

Cash Flow Summary - Table 2.6

Cash Flow Summary - Table 2.6

Менеджмент капитала банка

Менеджмент капитала банка Banking

Banking Газпромбанк (Акционерное общество)

Газпромбанк (Акционерное общество) Этика. Профессиональная этика

Этика. Профессиональная этика Взаимоотношения с инвесторами. Вебинар

Взаимоотношения с инвесторами. Вебинар Финансовый анализ ПАО “КАМАЗ“

Финансовый анализ ПАО “КАМАЗ“ Новые полномочия финансового органа по контролю в сфере закупок, вступающие в силу с 1 января 2017 года

Новые полномочия финансового органа по контролю в сфере закупок, вступающие в силу с 1 января 2017 года Организация бухгалтерского учета на предприятии

Организация бухгалтерского учета на предприятии Концепции финансового менеджмента. (Лекция 2)

Концепции финансового менеджмента. (Лекция 2) Доходы и расходы семейного бюджета

Доходы и расходы семейного бюджета Акционерное общество Первоуральский акционерный коммерческий банк

Акционерное общество Первоуральский акционерный коммерческий банк Задачі. Фінансові інвестиції

Задачі. Фінансові інвестиції Управление государственными и муниципальными закупками в системе образования

Управление государственными и муниципальными закупками в системе образования Управління капіталом підприємства

Управління капіталом підприємства Денежный оборот. Масса и скорость

Денежный оборот. Масса и скорость Налоговые службы Костромской области

Налоговые службы Костромской области Расходы предприятия, себестоимость продукции

Расходы предприятия, себестоимость продукции Финансовый сектор экономики и основы его функционирования

Финансовый сектор экономики и основы его функционирования Учет и анализ расчетов с покупателями и заказчиками

Учет и анализ расчетов с покупателями и заказчиками Государственная поддержка малого бизнеса в России

Государственная поддержка малого бизнеса в России Қысқа мерзімдегі фирманың шығындар

Қысқа мерзімдегі фирманың шығындар Венчурный бизнес. Специфика рискового финансирования

Венчурный бизнес. Специфика рискового финансирования Налоговое право. Налоговые органы. Виды налогов

Налоговое право. Налоговые органы. Виды налогов Эффективные и эквивалентные ставки процентов

Эффективные и эквивалентные ставки процентов Организация финансовой деятельности

Организация финансовой деятельности Учет материально-производственных запасов

Учет материально-производственных запасов Основы бизнес-планирования

Основы бизнес-планирования Направления улучшения использования основных средств предприятия (на примере ООО АГРОФИРА Тысячный, Краснодарский край)

Направления улучшения использования основных средств предприятия (на примере ООО АГРОФИРА Тысячный, Краснодарский край)