- Cash Flow and financial planning

Содержание

- 2. Learning Goals Understand tax depreciation procedures and the effect of depreciation on the firm’s cash flows.

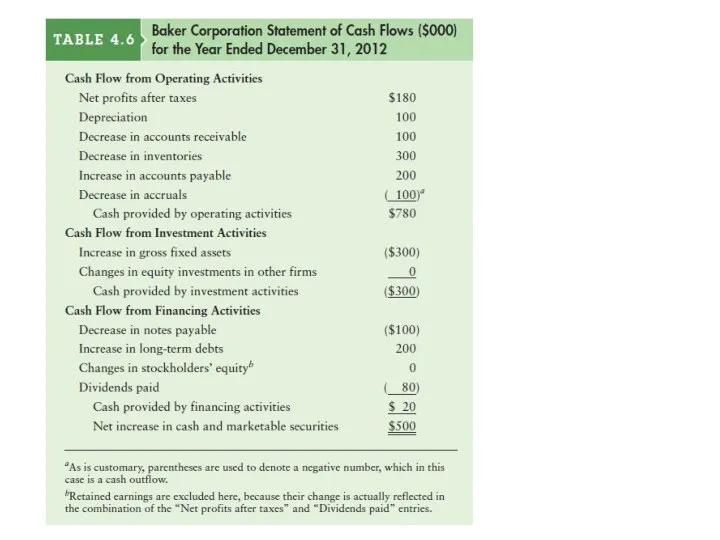

- 3. Analyzing the Firm’s Cash Flow depreciation A portion of the costs of fixed assets charged against

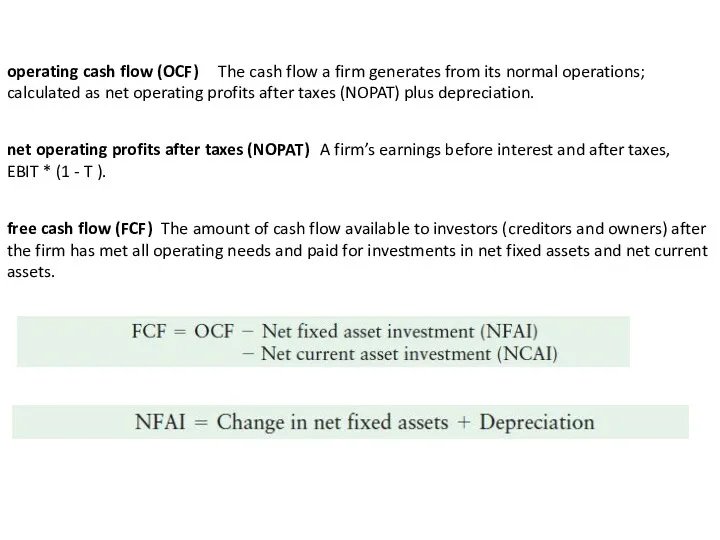

- 5. operating cash flow (OCF) The cash flow a firm generates from its normal operations; calculated as

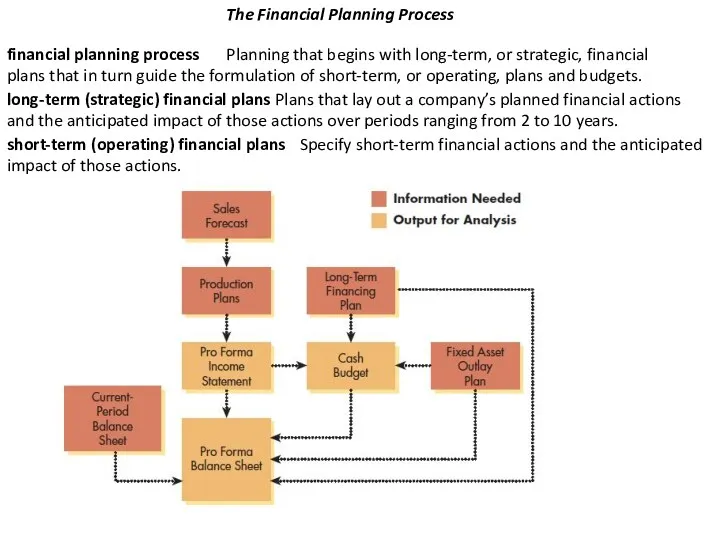

- 6. The Financial Planning Process financial planning process Planning that begins with long-term, or strategic, financial plans

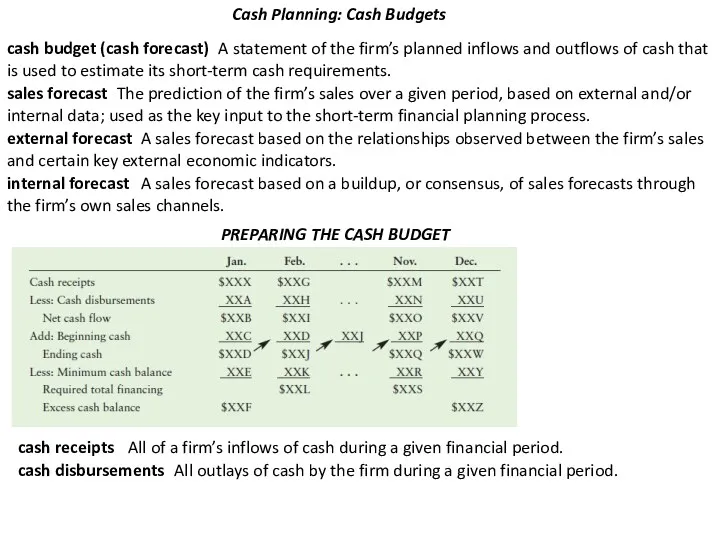

- 7. Cash Planning: Cash Budgets cash budget (cash forecast) A statement of the firm’s planned inflows and

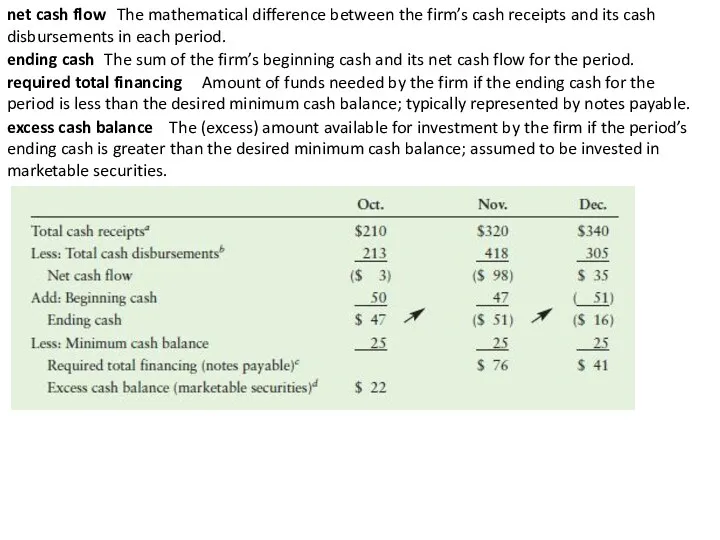

- 8. net cash flow The mathematical difference between the firm’s cash receipts and its cash disbursements in

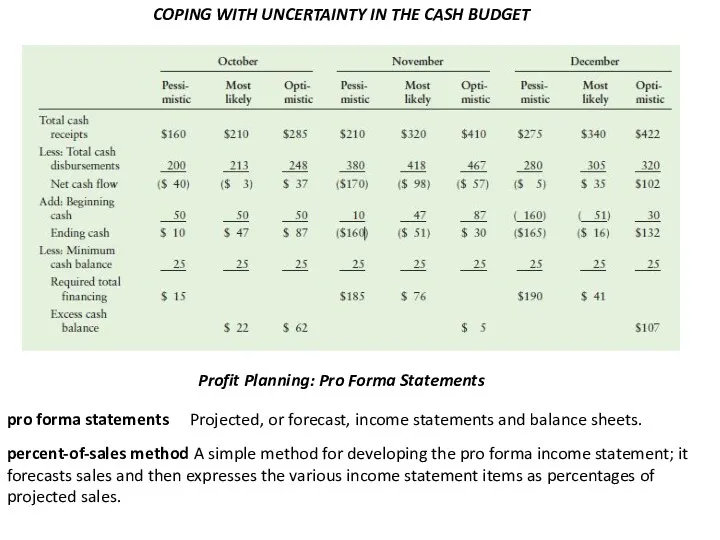

- 9. COPING WITH UNCERTAINTY IN THE CASH BUDGET Profit Planning: Pro Forma Statements pro forma statements Projected,

- 10. judgmental approach A simplified approach for preparing the pro forma balance sheet under which the firm

- 12. Скачать презентацию

Learning Goals

Understand tax depreciation procedures and the effect of depreciation on

Learning Goals

Understand tax depreciation procedures and the effect of depreciation on

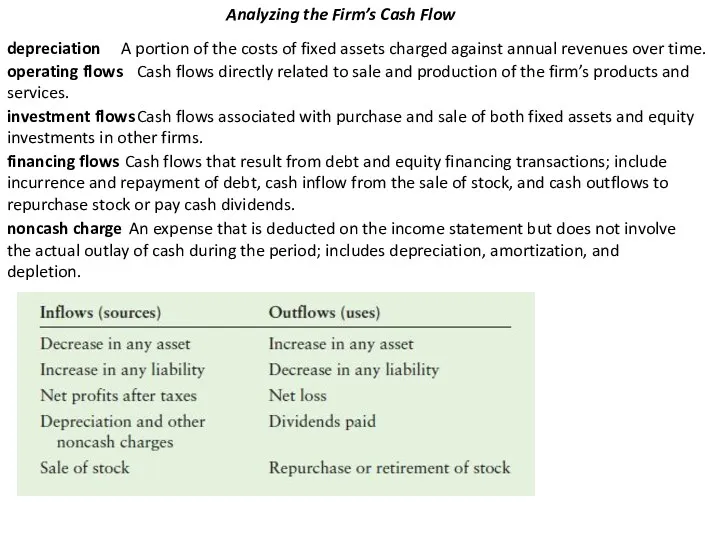

Analyzing the Firm’s Cash Flow

depreciation

A portion of the costs of

Analyzing the Firm’s Cash Flow

depreciation

A portion of the costs of

operating cash flow (OCF)

The cash flow a firm generates from

operating cash flow (OCF)

The cash flow a firm generates from

The Financial Planning Process

financial planning process

Planning that begins with long-term,

The Financial Planning Process

financial planning process

Planning that begins with long-term,

Cash Planning: Cash Budgets

cash budget (cash forecast)

A statement of the

Cash Planning: Cash Budgets

cash budget (cash forecast)

A statement of the

net cash flow

The mathematical difference between the firm’s cash receipts

net cash flow

The mathematical difference between the firm’s cash receipts

COPING WITH UNCERTAINTY IN THE CASH BUDGET

Profit Planning: Pro Forma Statements

pro

COPING WITH UNCERTAINTY IN THE CASH BUDGET

Profit Planning: Pro Forma Statements

pro

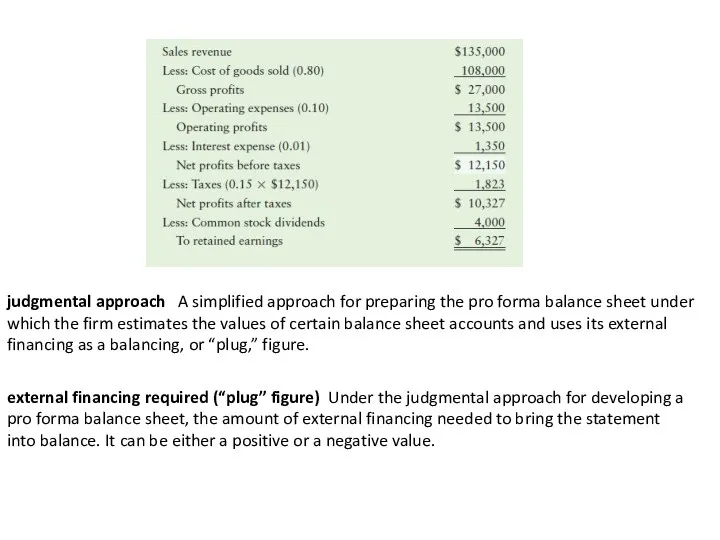

judgmental approach

A simplified approach for preparing the pro forma balance

judgmental approach

A simplified approach for preparing the pro forma balance

Заработная плата, гарантии, компенсации

Заработная плата, гарантии, компенсации LifePay

LifePay Оценка объектов интеллектуальной собственности

Оценка объектов интеллектуальной собственности Налогообложение субъектов малого предпринимательства

Налогообложение субъектов малого предпринимательства Филиалдардың дебиторлық берешек есебі

Филиалдардың дебиторлық берешек есебі О городском бюджете на 2019 год и плановый период 2020 и 2021 годов (с изменениями)

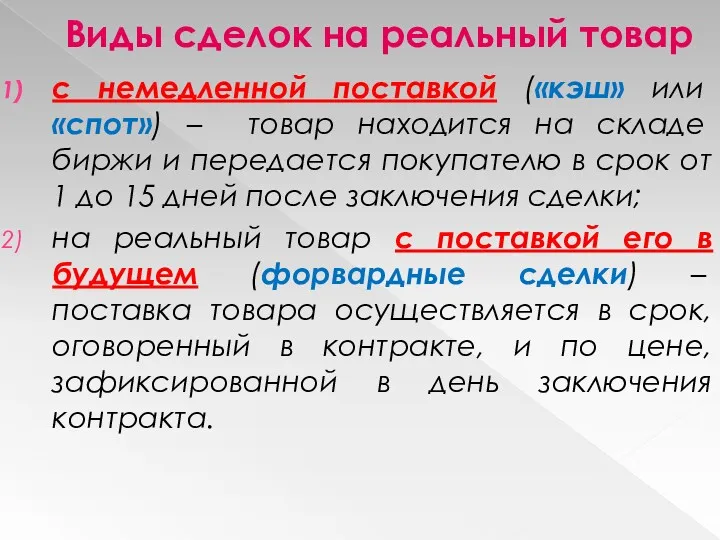

О городском бюджете на 2019 год и плановый период 2020 и 2021 годов (с изменениями) Виды сделок на реальный товар

Виды сделок на реальный товар Оценка ювелирных изделий из золота. Стандарты работы с клиентами ломбарда. Лекция №2

Оценка ювелирных изделий из золота. Стандарты работы с клиентами ломбарда. Лекция №2 Поняття банківської таємниці. (Тема 9)

Поняття банківської таємниці. (Тема 9) Базовые и производные ценные бумаги

Базовые и производные ценные бумаги Управление инвестициями. (Тема 3)

Управление инвестициями. (Тема 3) Бухгалтерский баланс

Бухгалтерский баланс Оценка земли в составе застроенных и незастроенных земельных участков

Оценка земли в составе застроенных и незастроенных земельных участков Отказ в выдаче кредита. Решение задачи 6.12

Отказ в выдаче кредита. Решение задачи 6.12 Бухгалтерский учет и аудит расчетов с поставщиками и подрядчиками на примере ООО ОП Статус-2

Бухгалтерский учет и аудит расчетов с поставщиками и подрядчиками на примере ООО ОП Статус-2 Издержки производства

Издержки производства Налоги

Налоги Понятие инвестиций и эффективности

Понятие инвестиций и эффективности Фінанси підприємств. Оцінка фінансового стану підприємства. (Тема 9)

Фінанси підприємств. Оцінка фінансового стану підприємства. (Тема 9) Основы управления финансовыми рисками в организациях

Основы управления финансовыми рисками в организациях Деньги и денежно-кредитная политика государства

Деньги и денежно-кредитная политика государства Кредитная система и ее организация. (Лекция 9)

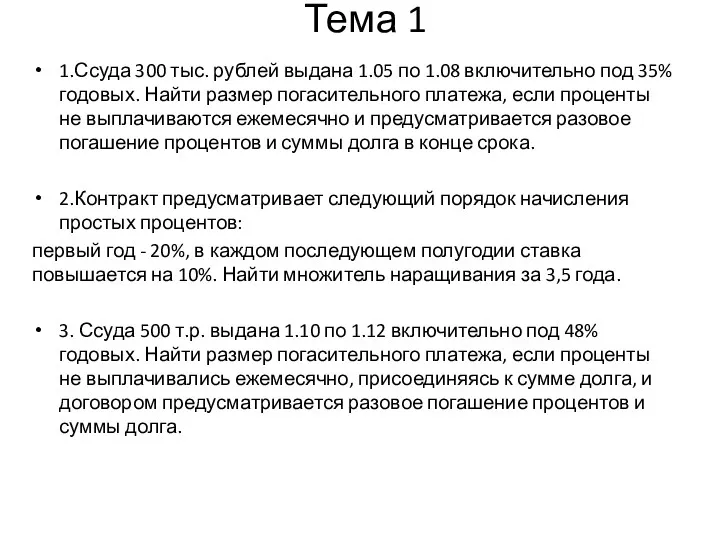

Кредитная система и ее организация. (Лекция 9) Финансы. Задачи. Тема 1

Финансы. Задачи. Тема 1 Преимущества почты в предоставлении услуги Электронные переводы

Преимущества почты в предоставлении услуги Электронные переводы Ипотечное Кредитование. ПАО Московский Кредитный Банк

Ипотечное Кредитование. ПАО Московский Кредитный Банк Курсовая работа на тему прибыли

Курсовая работа на тему прибыли Субсидиарная ответственность

Субсидиарная ответственность Введение в банковское дело

Введение в банковское дело