- Financial market fragility

Содержание

- 2. Chart A.8 Advanced economy sovereign bond yields have increased markedly Source: Thomson Reuters Datastream. (a) Yields

- 3. Chart A.9 The causes of changes in nominal government bond yields differs across economies Sources: Bloomberg

- 4. Chart A.10 Term premia in government bond markets are low Sources: Bloomberg, Federal Reserve Bank of

- 5. Chart A.11 Yields on sterling corporate bonds are low by historical standards Sources: Bank of America

- 7. Скачать презентацию

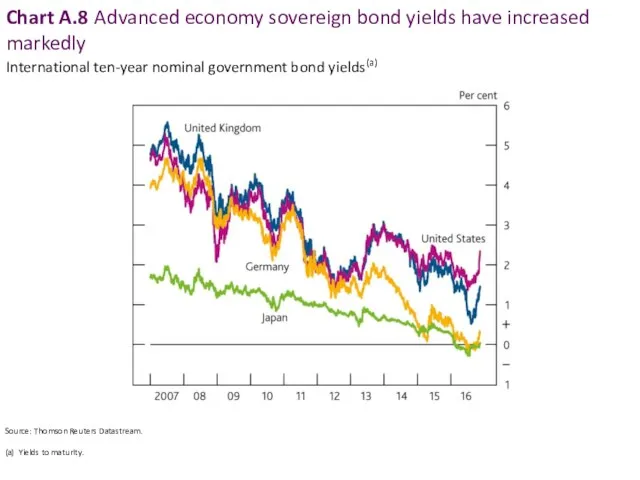

Chart A.8 Advanced economy sovereign bond yields have increased markedly

Source: Thomson

Chart A.8 Advanced economy sovereign bond yields have increased markedly

Source: Thomson

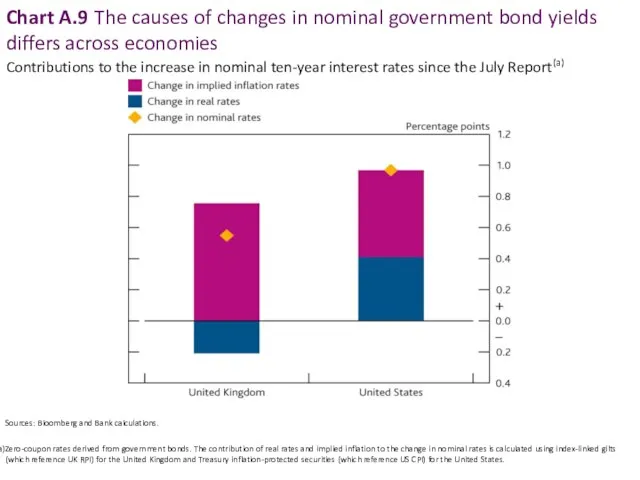

Chart A.9 The causes of changes in nominal government bond yields

Chart A.9 The causes of changes in nominal government bond yields

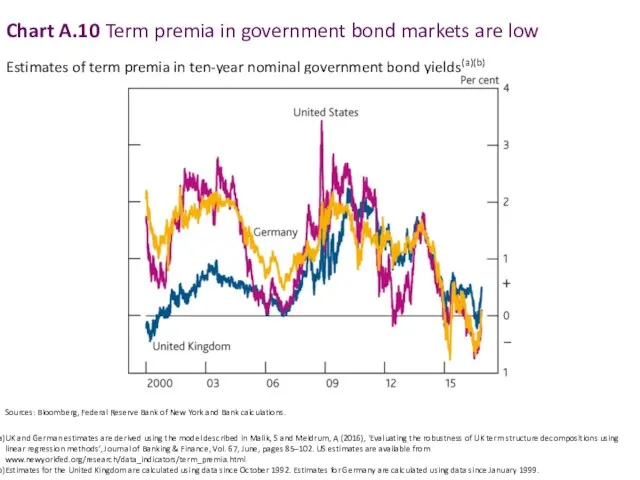

Chart A.10 Term premia in government bond markets are low

Sources: Bloomberg,

Chart A.10 Term premia in government bond markets are low

Sources: Bloomberg,

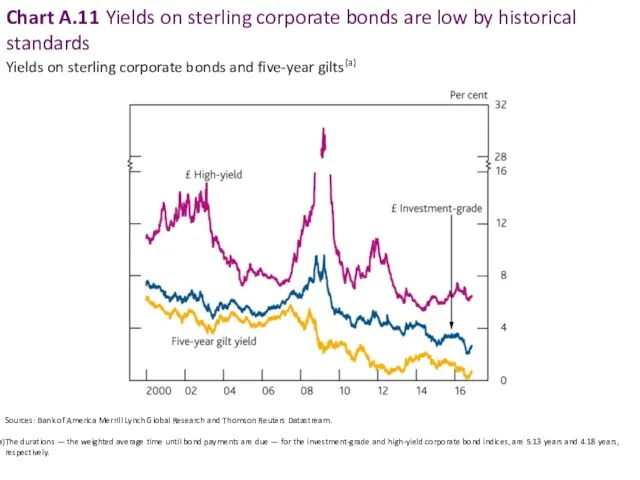

Chart A.11 Yields on sterling corporate bonds are low by historical

Chart A.11 Yields on sterling corporate bonds are low by historical

ОСАГО. Порядок работы в рамках Мобильного приёма документов

ОСАГО. Порядок работы в рамках Мобильного приёма документов Бизнес-ангелы

Бизнес-ангелы Тема: Податок на доходи фізичних осіб в україні (пдфо)

Тема: Податок на доходи фізичних осіб в україні (пдфо) Қазақстан Республикасында лотерея. Лотереяны өткізу тәсіліне қарай екі түрі бар

Қазақстан Республикасында лотерея. Лотереяны өткізу тәсіліне қарай екі түрі бар Правовое регулирование банковской деятельности. Лекция 1

Правовое регулирование банковской деятельности. Лекция 1 Совершенствование системы потребительского кредитования в Калининградском отделении Сбербанка России

Совершенствование системы потребительского кредитования в Калининградском отделении Сбербанка России Учет амортизации основных средств

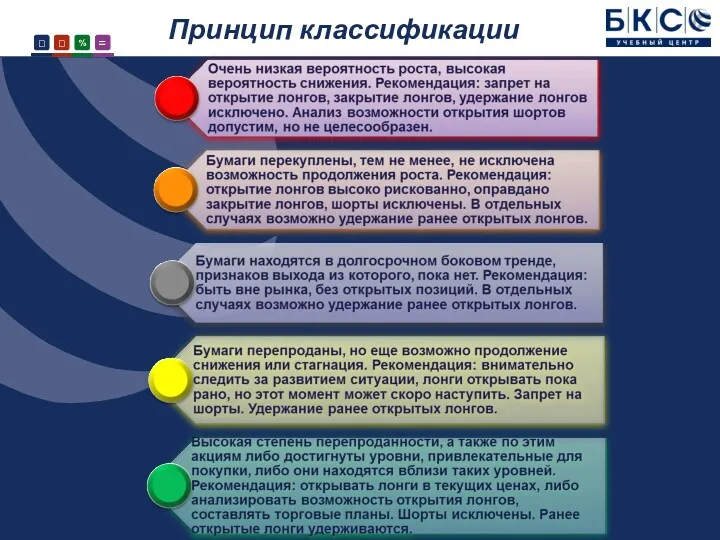

Учет амортизации основных средств Основные рыночные характеристики для отбора акций на долгосрочную перспективу. БКС

Основные рыночные характеристики для отбора акций на долгосрочную перспективу. БКС Направления средств материнского (семейного) капитала на улучшение жилищных условий

Направления средств материнского (семейного) капитала на улучшение жилищных условий Облік валютних операцій (3.1 - 3.3)

Облік валютних операцій (3.1 - 3.3) Анализ институциональной структуры банковской сферы

Анализ институциональной структуры банковской сферы Анализ бухгалтерского баланса

Анализ бухгалтерского баланса Формирование и развитие банковской системы, как объекта государственного управления. (Тема 1)

Формирование и развитие банковской системы, как объекта государственного управления. (Тема 1) Деньги: причины возникновения, формы и функции

Деньги: причины возникновения, формы и функции Финансирование системы образования

Финансирование системы образования Вопросы по продуктам РКО Tinkoff

Вопросы по продуктам РКО Tinkoff Формирование и использование оборотных активов (оборотного капитала) корпорации

Формирование и использование оборотных активов (оборотного капитала) корпорации Ключевые направления деятельности ФНС России по созданию благоприятной налоговой среды

Ключевые направления деятельности ФНС России по созданию благоприятной налоговой среды Управление рисками

Управление рисками Договор страхования

Договор страхования Деньги. Функции и формы денег

Деньги. Функции и формы денег Оценка стоимости контрольных и неконтрольных пакетов акций

Оценка стоимости контрольных и неконтрольных пакетов акций Реализация проекта Финансовая грамотность

Реализация проекта Финансовая грамотность Заработная плата

Заработная плата Аудиторская выборка

Аудиторская выборка Анализ безубыточности

Анализ безубыточности Как легально и выгодно вывести деньги из бизнеса

Как легально и выгодно вывести деньги из бизнеса Денежная система: черты денежных систем в России и в мире, характеристика основных элементов

Денежная система: черты денежных систем в России и в мире, характеристика основных элементов