- Financial planning: the ties that bind

Содержание

- 2. Learning Objectives Explain why personal financial planning is so important. Describe the five basic steps of

- 3. Why Personal Financial Planning? Need a financial plan because it’s easier to spend than to save.

- 4. Here’s What You Can Accomplish Manage the unplanned Accumulate wealth for special expenses Save for retirement

- 5. The Personal Financial Planning Process Financial planning is an ongoing process – it changes as your

- 6. Personal Financial Planning Process Step 1: Evaluate Your Financial Health Examine your current financial situation. How

- 7. Personal Financial Planning Process Step 2: Define Your Financial Goals Define your goals: Accumulate wealth for

- 8. Personal Financial Planning Process Flexibility Plan for life changes and the unexpected. Liquidity Immediate use of

- 9. Personal Financial Planning Process Step 4: Implement Your Plan Carefully and thoughtfully develop a financial plan,

- 10. Personal Financial Planning Process Step 5: Review Your Progress, Reevaluate, and Revise Your Plan Review progress

- 11. Establishing Your Financial Goals Financial Goals Cover 3 Time Horizons Short-term -- within 1 year Intermediate-term

- 12. Short–Term Goals Accumulate Emergency Funds Equaling 3 Months’ Living Expenses Pay Off Bills and Credit Cards

- 13. Intermediate-Term Goals Save for Older Child’s College Save for a Down Payment or a Major Home

- 14. Long-Term Goals Save for Younger Child’s College Purchase Retirement Home Create a Retirement Fund to Maintain

- 15. Stage 1 The Early Years—A Time of Wealth Accumulation Prior to age 54: Purchase a home

- 16. Stage 2 Approaching Retirement—The Golden Years Transition years between ages 55-64. Retirement goals are the center

- 17. Stage 3 The Retirement Years After age 65, live off savings Retirement age depends on savings.

- 18. Thinking About Your Career Choosing a Major and a Career Getting a Job Making it a

- 19. Being Successful in Your Career Have a marketable skill, be well educated, and keep up with

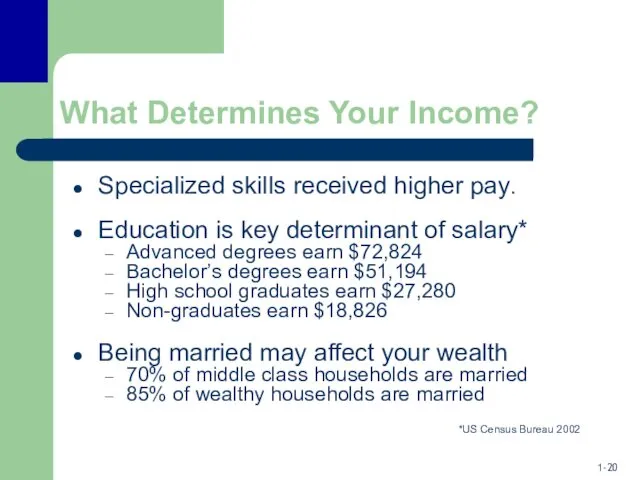

- 20. What Determines Your Income? Specialized skills received higher pay. Education is key determinant of salary* Advanced

- 21. Fifteen Principles of Personal Finance These principles form the foundation of personal finance. They will provide

- 22. Principle 1: The Risk–Return Trade-Off Savings allow for more future purchases. Borrowers pay for using your

- 23. Principle 2: The Time Value of Money Money has a time value. Money received today is

- 24. Principle 3: Diversification Reduces Risk “Don’t put all your eggs in one basket.” To diversify, place

- 25. Principle 4: All Risk Is Not Equal Some risk cannot be diversified away. If stocks move

- 26. Principle 5: The Curse of Competitive Investment Markets In efficient markets, information is instantly reflected in

- 27. Principle 6: Taxes Affect Personal Finance Decisions Taxes influence the realized return of investments. Maximize after-tax

- 28. Principle 7: Stuff Happens, or the Importance of Liquidity Have funds available for the unexpected. Without

- 29. Principle 8: Nothing Happens Without a Plan People spend money without thinking, but you can’t save

- 30. Principle 9: The Best Protection Is Knowledge Take responsibility for your financial affairs: Protect yourself from

- 31. Principle 10: Protect Yourself Against Major Catastrophes Have the right insurance before a tragedy occurs. Know

- 32. Principle 11: The Time Dimension of Investing Take more risk on long-term investments. Large-company stock prices

- 33. Principle 12: The Agency Problem—Beware of the Sales Pitch The agency problem - those who act

- 34. Principle 13: Pay Yourself First For most people, savings are residual. Spend what you like, save

- 35. Principle 14: Money Isn’t Everything Extend financial plans to achieve future goals. See more than just

- 37. Скачать презентацию

Learning Objectives

Explain why personal financial planning is so important.

Describe the five

Learning Objectives

Explain why personal financial planning is so important.

Describe the five

Why Personal Financial Planning?

Need a financial plan because it’s easier to

Why Personal Financial Planning?

Need a financial plan because it’s easier to

Here’s What You Can Accomplish

Manage the unplanned

Accumulate wealth for

Here’s What You Can Accomplish

Manage the unplanned

Accumulate wealth for

The Personal Financial Planning Process

Financial planning is an ongoing process –

The Personal Financial Planning Process

Financial planning is an ongoing process –

Personal Financial Planning Process

Step 1: Evaluate Your Financial Health

Examine your current

Personal Financial Planning Process

Step 1: Evaluate Your Financial Health

Examine your current

Personal Financial Planning Process

Step 2: Define Your Financial Goals

Define your goals:

Accumulate

Personal Financial Planning Process

Step 2: Define Your Financial Goals

Define your goals:

Accumulate

Personal Financial Planning Process

Flexibility

Plan for life changes and the unexpected.

Liquidity

Immediate use

Personal Financial Planning Process

Flexibility

Plan for life changes and the unexpected.

Liquidity

Immediate use

Personal Financial Planning Process

Step 4: Implement Your Plan

Carefully and thoughtfully develop

Personal Financial Planning Process

Step 4: Implement Your Plan

Carefully and thoughtfully develop

Personal Financial Planning Process

Step 5: Review Your Progress, Reevaluate, and Revise

Personal Financial Planning Process

Step 5: Review Your Progress, Reevaluate, and Revise

Establishing Your Financial Goals

Financial Goals Cover 3 Time Horizons

Short-term -- within

Establishing Your Financial Goals

Financial Goals Cover 3 Time Horizons

Short-term -- within

Short–Term Goals

Accumulate Emergency Funds Equaling 3 Months’ Living Expenses

Pay Off Bills

Short–Term Goals

Accumulate Emergency Funds Equaling 3 Months’ Living Expenses

Pay Off Bills

Intermediate-Term Goals

Save for Older Child’s College

Save for a Down Payment

Intermediate-Term Goals

Save for Older Child’s College

Save for a Down Payment

Long-Term Goals

Save for Younger Child’s College

Purchase Retirement Home

Create a Retirement Fund

Long-Term Goals

Save for Younger Child’s College

Purchase Retirement Home

Create a Retirement Fund

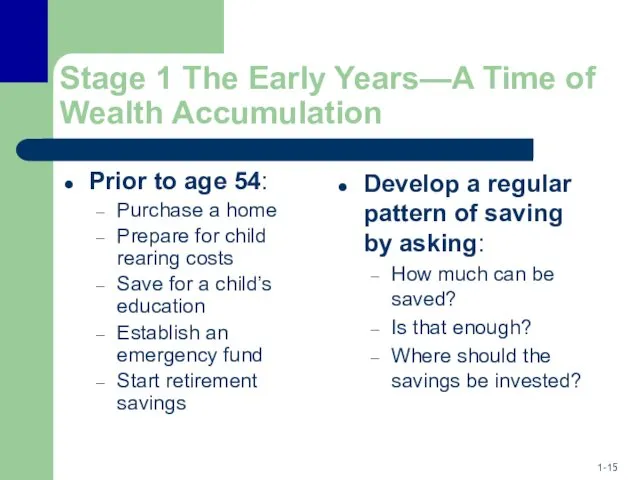

Stage 1 The Early Years—A Time of Wealth Accumulation

Prior to age

Stage 1 The Early Years—A Time of Wealth Accumulation

Prior to age

Stage 2 Approaching Retirement—The Golden Years

Transition years between ages 55-64.

Retirement

Stage 2 Approaching Retirement—The Golden Years

Transition years between ages 55-64.

Retirement

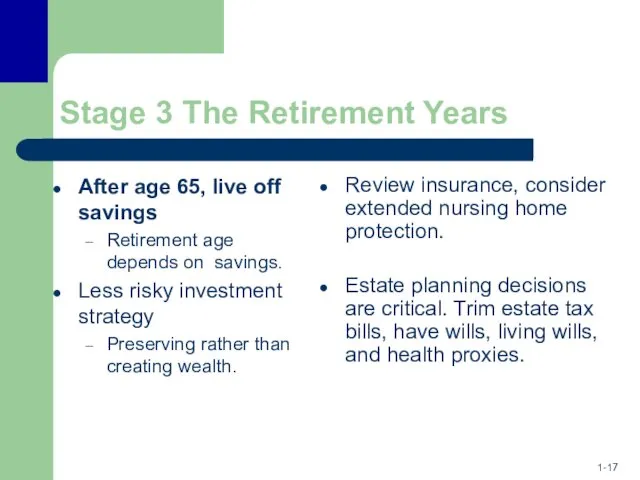

Stage 3 The Retirement Years

After age 65, live off savings

Retirement age

Stage 3 The Retirement Years

After age 65, live off savings

Retirement age

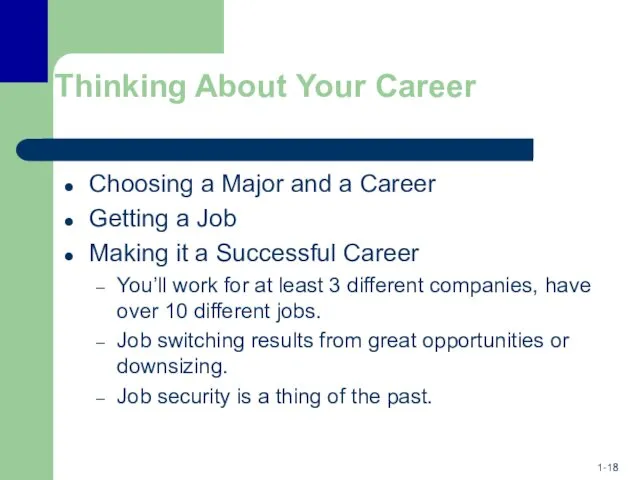

Thinking About Your Career

Choosing a Major and a Career

Getting a Job

Making

Thinking About Your Career

Choosing a Major and a Career

Getting a Job

Making

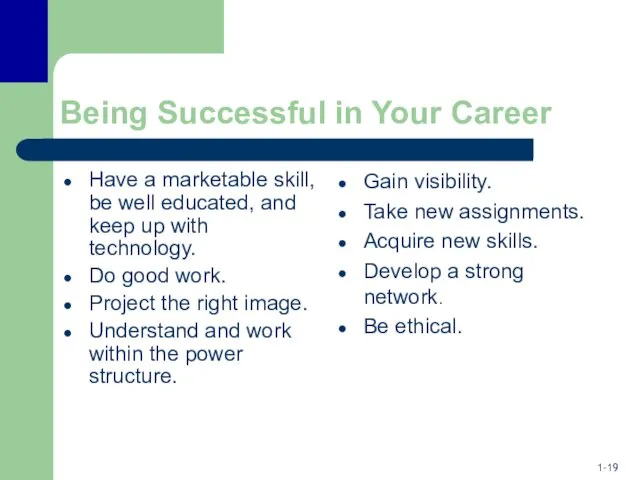

Being Successful in Your Career

Have a marketable skill, be well

Being Successful in Your Career

Have a marketable skill, be well

What Determines Your Income?

Specialized skills received higher pay.

Education is key determinant

What Determines Your Income?

Specialized skills received higher pay.

Education is key determinant

Fifteen Principles of

Personal Finance

These principles form the foundation of personal finance.

They

Fifteen Principles of

Personal Finance

These principles form the foundation of personal finance.

They

Principle 1: The Risk–Return Trade-Off

Savings allow for more future purchases.

Borrowers

Principle 1: The Risk–Return Trade-Off

Savings allow for more future purchases.

Borrowers

Principle 2: The Time

Value of Money

Money has a time value.

Money

Principle 2: The Time

Value of Money

Money has a time value.

Money

Principle 3: Diversification Reduces Risk

“Don’t put all your eggs in one

Principle 3: Diversification Reduces Risk

“Don’t put all your eggs in one

Principle 4: All Risk Is Not Equal

Some risk cannot be

Principle 4: All Risk Is Not Equal

Some risk cannot be

Principle 5: The Curse of Competitive Investment Markets

In efficient markets,

Principle 5: The Curse of Competitive Investment Markets

In efficient markets,

Principle 6: Taxes Affect Personal Finance Decisions

Taxes influence the realized

Principle 6: Taxes Affect Personal Finance Decisions

Taxes influence the realized

Principle 7: Stuff Happens, or the Importance of Liquidity

Have funds available

Principle 7: Stuff Happens, or the Importance of Liquidity

Have funds available

Principle 8: Nothing Happens Without a Plan

People spend money without

Principle 8: Nothing Happens Without a Plan

People spend money without

Principle 9: The Best Protection Is Knowledge

Take responsibility for your financial

Principle 9: The Best Protection Is Knowledge

Take responsibility for your financial

Principle 10: Protect Yourself Against Major Catastrophes

Have the right insurance before

Principle 10: Protect Yourself Against Major Catastrophes

Have the right insurance before

Principle 11: The Time Dimension of Investing

Take more risk on long-term

Principle 11: The Time Dimension of Investing

Take more risk on long-term

Principle 12: The Agency Problem—Beware of the Sales Pitch

The agency problem

Principle 12: The Agency Problem—Beware of the Sales Pitch

The agency problem

Principle 13: Pay Yourself First

For most people, savings are residual. Spend

Principle 13: Pay Yourself First

For most people, savings are residual. Spend

Principle 14: Money

Isn’t Everything

Extend financial plans to achieve future goals.

See

Principle 14: Money

Isn’t Everything

Extend financial plans to achieve future goals.

See

Финансовый рычаг и структура капитала. Принятие решений о структуре капитала

Финансовый рычаг и структура капитала. Принятие решений о структуре капитала Виды инвентаризации. Порядок проведения инвентаризации и оформления результатов инвентаризации

Виды инвентаризации. Порядок проведения инвентаризации и оформления результатов инвентаризации Учет имущества кредитной организации

Учет имущества кредитной организации Проектный фандрайзинг в сфере культуры

Проектный фандрайзинг в сфере культуры Система социального обеспечения Дании, Швеции, Норвегии, Финляндии

Система социального обеспечения Дании, Швеции, Норвегии, Финляндии Ұлттық экономикадағы қаржы және ақша несие жүйесі

Ұлттық экономикадағы қаржы және ақша несие жүйесі Предмет, метод і об’єкти організації та методики аудиту. (Тема 1)

Предмет, метод і об’єкти організації та методики аудиту. (Тема 1) Финансы и управленческий учет

Финансы и управленческий учет Бюджетный учет. Бюджетирование

Бюджетный учет. Бюджетирование Региональная бюджетная система

Региональная бюджетная система Налогообложение юридических лиц (на примере ООО Утренняя звезда)

Налогообложение юридических лиц (на примере ООО Утренняя звезда) O’zbekistonda lizing xizmatlari

O’zbekistonda lizing xizmatlari Kazkommertsbank

Kazkommertsbank Оценка рыночной стоимости объекта жилого недвижимого имущества

Оценка рыночной стоимости объекта жилого недвижимого имущества Затраты на качество

Затраты на качество Ефективність діяльності підприємства. (Тема 13)

Ефективність діяльності підприємства. (Тема 13) Технический финансовых анализ рынков

Технический финансовых анализ рынков Грошовий обіг. (Тема 2)

Грошовий обіг. (Тема 2) ВКР: Бухгалтерский учет затрат на производство продукции

ВКР: Бухгалтерский учет затрат на производство продукции Наиболее острые проблемы развития потребительского рынка в г. Костроме

Наиболее острые проблемы развития потребительского рынка в г. Костроме Финансовая грамотность - оружие устраняющее коррупцию

Финансовая грамотность - оружие устраняющее коррупцию Статистика финансовой деятельности предприятия

Статистика финансовой деятельности предприятия Исламский банк и его развитие в Пакистане

Исламский банк и его развитие в Пакистане Концепция бухгалтерской отчетности в Российской Федерации и международной практике. Тема 1

Концепция бухгалтерской отчетности в Российской Федерации и международной практике. Тема 1 Взаимосвязь логистики с планированием производства и финансами

Взаимосвязь логистики с планированием производства и финансами Discounted cash flow applications

Discounted cash flow applications Инвестиционный паспорт Котласского муниципального округа Архангельской области

Инвестиционный паспорт Котласского муниципального округа Архангельской области Финансовый результат деятельности предприятия

Финансовый результат деятельности предприятия