- Introduction to finance

Содержание

- 2. Examination paper format Answer FOUR (4) out of SIX (6) questions Each question has a weighting

- 3. Question 1 (a) Calculation (10 marks) (b) Theory : Discuss (15 marks) (25 marks) Question 2

- 4. Question 3 Theory : Explain (25 marks) Question 4 Theory : Discuss (25 marks)

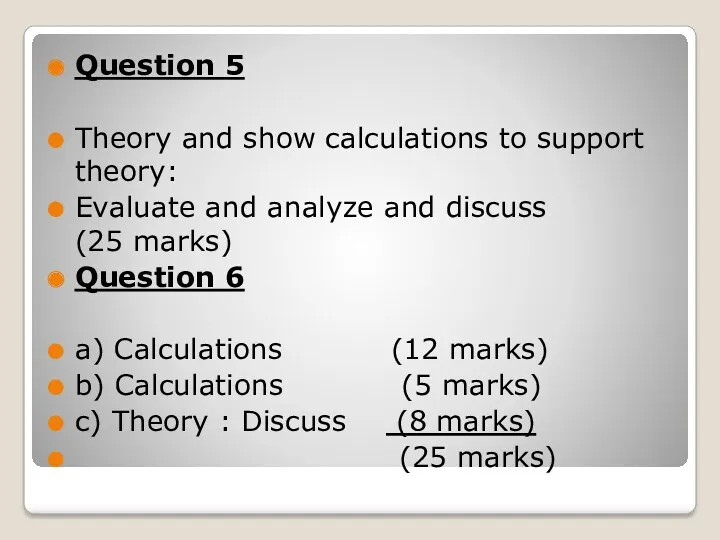

- 5. Question 5 Theory and show calculations to support theory: Evaluate and analyze and discuss (25 marks)

- 6. The Goal of the Firm The goal of the firm is to create value for the

- 7. 3 Roles of Finance in Business What long-term investments should the firm undertake? (Capital budgeting decision)

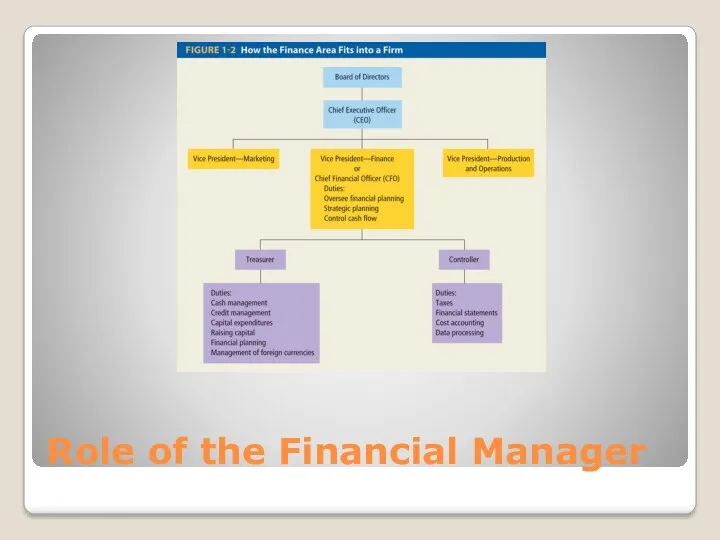

- 8. Role of the Financial Manager

- 9. Legal Forms of Business Organization

- 10. Sole Proprietorship Business owned by an individual Owner maintains title to assets and profits Unlimited liability

- 11. Partnership Two or more persons come together as co-owners General Partnership: All partners are fully responsible

- 12. Corporation Legally functions separate and apart from its owners Corporation can sue, be sued, purchase, sell,

- 13. Hybrid Organizations: S-Corporation Benefits Limited liability Taxed as partnership (no double taxation like corporations) Limitations Owners

- 14. Hybrid Organizations: Limited Liability Companies (LLCs) Benefits Limited liability Taxed like a partnership Limitations Qualifications vary

- 15. Finance and The Multinational Firm: The New Role U.S. firms are looking to international expansion to

- 16. Why Do Companies Go Abroad? To increase revenues To reduce expenses (land, labor, capital, raw material,

- 17. Risks/Challenges of Going Abroad Country risk (changes in government regulations, unstable government, economic changes in foreign

- 18. What Is Liquidity? Liquidity is the term used to describe how easy it is to convert

- 19. How Liquid Is the Firm? A liquid asset is one that can be converted quickly and

- 20. Measuring Liquidity: Perspective 1 Compare a firm’s current assets with current liabilities using: Current Ratio Acid

- 21. Table 4-1

- 22. Table 4-2

- 23. Current Ratio Current ratio compares a firm’s current assets to its current liabilities. Equation: Home Depot

- 24. Acid Test or Quick Ratio Quick ratio compares cash and current assets (minus inventory) that can

- 25. Measuring Liquidity: Perspective 2 Measures a firm’s ability to convert accounts receivable and inventory into cash:

- 26. Days in Receivables (Average Collection Period)

- 27. Days in Inventory

- 28. Certificates of deposit are slightly less liquid, because there is usually a penalty for converting them

- 29. Each of the above can be considered as cash or cash equivalents because they can be

- 30. Other examples are items like coins, stamps, art and other collectibles. If you were to sell

- 31. Cash is a company's lifeblood. In other words, a company can sell lots of widgets and

- 32. Depending on the industry, companies with good liquidity will usually have a current ratio of more

- 33. A more stringent measure is the quick ratio, sometimes called the acid test ratio. This uses

- 34. One last ratio of note is the debt/equity ratio, usually defined as total liabilities divided by

- 35. Are the Firm’s Managers Generating Adequate Operating Profits from the Company’s Assets? The focus is on

- 36. Operating Return on Assets (ORA)

- 37. Managing Operations: Operating Profit Margin (OPM)

- 38. Managing Assets: Total Asset Turnover

- 39. Managing Assets: Fixed Asset Turnover

- 40. How Is the Firm Financing Its Assets? Does the firm finance its assets by debt or

- 41. Debt Ratio

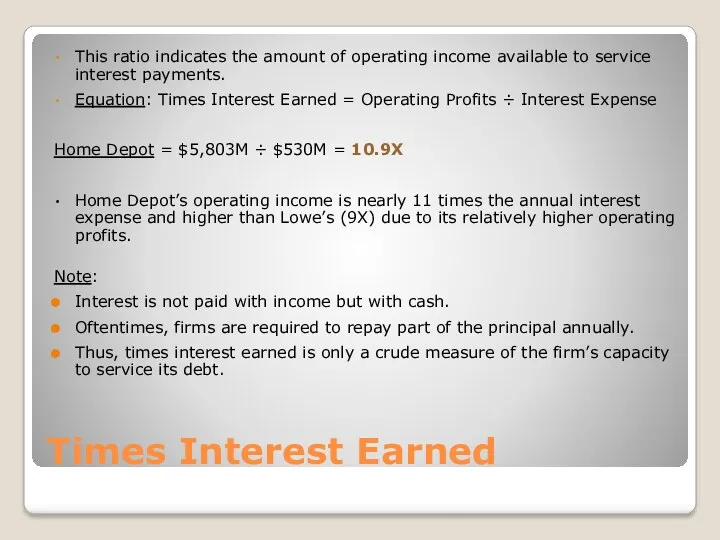

- 42. Times Interest Earned This ratio indicates the amount of operating income available to service interest payments.

- 43. Are the Firm’s Managers Providing a Good Return on the Capital Provided by the Company’s Shareholders?

- 44. ROE Home Depot = $3,338M ÷ $18,889M = 0.177 or 17.7% Owners of Home Depot are

- 45. Price/Earnings Ratio

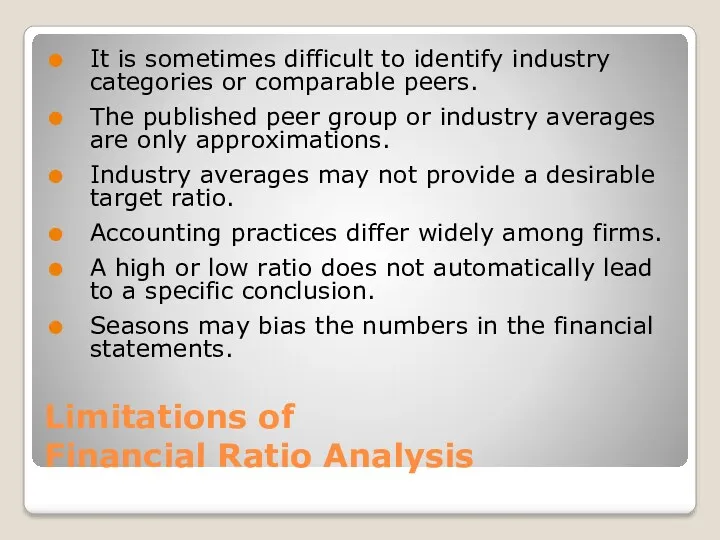

- 46. Limitations of Financial Ratio Analysis It is sometimes difficult to identify industry categories or comparable peers.

- 48. Introduction to Finance Chapter 5 – Stock valuation

- 49. Learning Objectives Identify the basic characteristics of preferred stock. Value preferred stock. Identify the basic characteristics

- 50. Preferred Stock Preferred stock is often referred to as a hybrid security because it has many

- 51. Characteristics of Preferred Stocks Multiple series of preferred stock Preferred stock’s claim on assets and income

- 52. Multiple Series If a company desires, it can issue more than one series of preferred stock,

- 53. Claim on Assets and Income Claim on Assets: Preferred stock has priority over common stock with

- 54. Cumulative Dividends Cumulative feature (if it exists) requires that all past, unpaid preferred stock dividends be

- 55. Protective Provisions Protective provisions generally allow for voting rights in the event of nonpayment of dividends,

- 56. Convertibility Convertible preferred stock can, at the discretion of the holder, be converted into a predetermined

- 57. Retirement Provisions Although preferred stock has no set maturity associated with it, issuing firms generally provide

- 58. The economic or intrinsic value of a preferred stock is equal to the present value of

- 59. Common Stock Common stock is a certificate that indicates ownership in a corporation. When you buy

- 60. Claim on Income Common shareholders have the right to residual income after bondholders and preferred stockholders

- 61. Claim on Assets Common stock has a residual claim on assets in the case of liquidation.

- 62. Limited Liability The liability of shareholders is limited to the amount of their investment. The limited

- 63. Voting Rights Most often, common stockholders are the only security holders with a vote. Majority of

- 64. Preemptive Rights Preemptive right entitles the common shareholder to maintain a proportionate share of ownership in

- 65. Valuing Common Stock Like bonds and preferred stock, the value of common stock is equal to

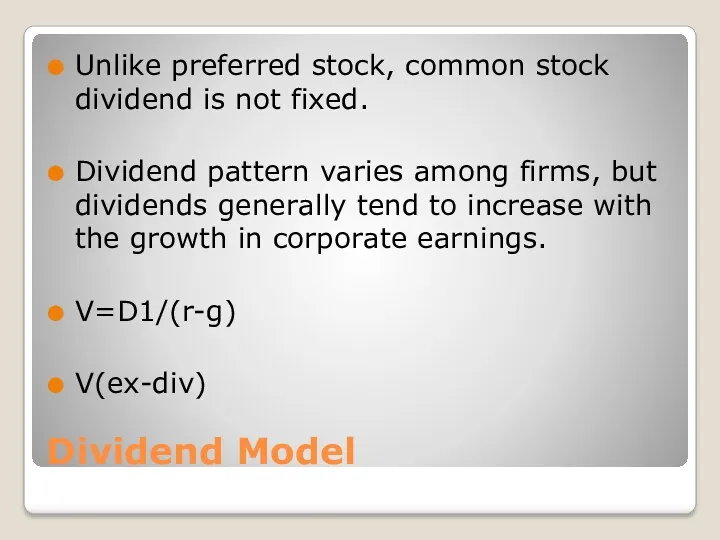

- 66. Dividend Model Unlike preferred stock, common stock dividend is not fixed. Dividend pattern varies among firms,

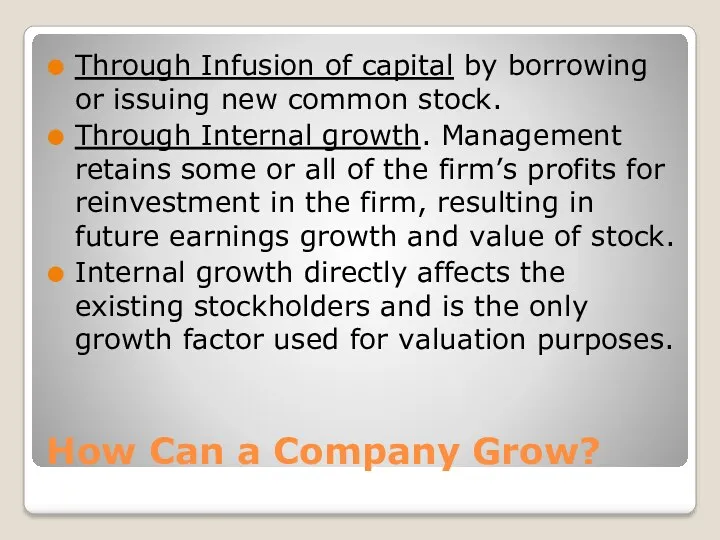

- 67. How Can a Company Grow? Through Infusion of capital by borrowing or issuing new common stock.

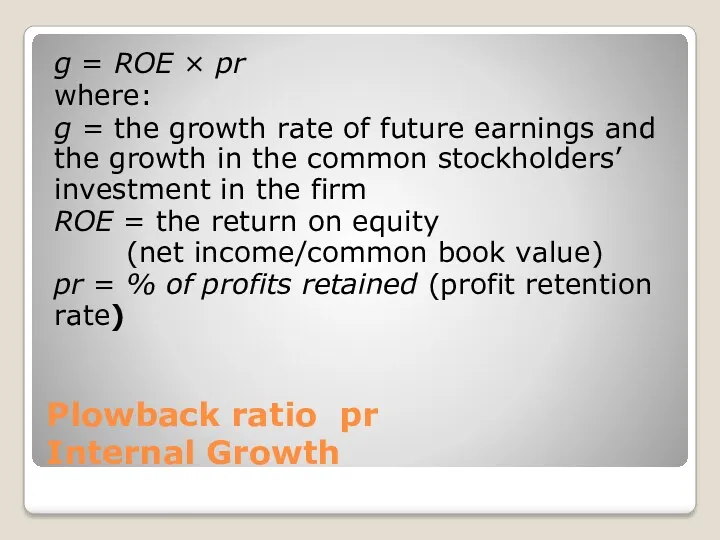

- 68. Plowback ratio pr Internal Growth g = ROE × pr where: g = the growth rate

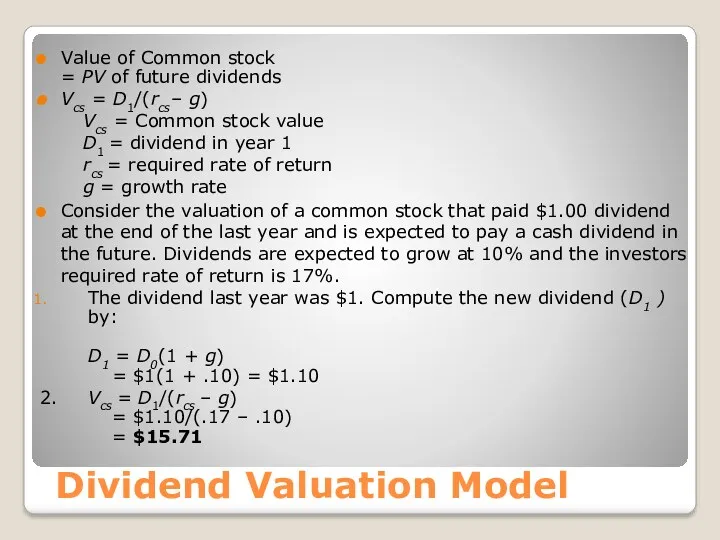

- 69. Dividend Valuation Model Value of Common stock = PV of future dividends Vcs = D1/(rcs– g)

- 70. The Expected Rate of Return of Preferred Stockholders The expected rate of return on a security

- 71. V=D1/(r-g) r-g= D1/P r=(D1/P)+g

- 72. Price versus Expected Return Typically, an investor is not concerned with the value of a stock.

- 73. Bonds Meaning: A bond is a type of debt or long-term promissory note, issued by a

- 74. Debentures Debentures are unsecured long-term debt. For an issuing firm, debentures provide the benefit of not

- 75. Subordinated Debentures There is a hierarchy of payout in case of insolvency. The claims of subordinated

- 76. Mortgage Bonds Mortgage bond is secured by a lien on real property. Typically, the value of

- 77. Eurobonds Securities (bonds) issued in a country different from the one in whose currency the bond

- 78. TERMINOLOGY AND CHARACTERISTICS OF BONDS Claims on Assets and Income Seniority in claims In the case

- 79. TERMINOLOGY AND CHARACTERISTICS OF BONDS Par Value Par value is the face value of the bond,

- 80. TERMINOLOGY AND CHARACTERISTICS OF BONDS Coupon Interest Rate The percentage of the par value of the

- 81. TERMINOLOGY AND CHARACTERISTICS OF BONDS Zero Coupon Bonds Zero coupon bonds have zero or very low

- 82. TERMINOLOGY AND CHARACTERISTICS OF BONDS Maturity Maturity of bond refers to the length of time until

- 83. TERMINOLOGY AND CHARACTERISTICS OF BONDS Call Provision Call provision (if it exists on a bond) gives

- 84. TERMINOLOGY AND CHARACTERISTICS OF BONDS Indenture An indenture is the legal agreement between the firm issuing

- 85. TERMINOLOGY AND CHARACTERISTICS OF BONDS Bond Ratings Bond ratings reflect the future risk potential of the

- 86. TERMINOLOGY AND CHARACTERISTICS OF BONDS Bond Ratings

- 87. TERMINOLOGY AND CHARACTERISTICS OF BONDS Factors Having a Favorable Effect on Bond Rating A greater reliance

- 88. TERMINOLOGY AND CHARACTERISTICS OF BONDS Junk Bonds Junk bonds are high-risk bonds with ratings of BB

- 89. Capital Capital represents the funds used to finance a firm's assets and operations. Capital constitutes all

- 90. Cost of Capital The firm’s cost of capital is also referred to as the firm’s Opportunity

- 91. Investor’s Required Rate of Return Investor’s Required Rate of Return – the minimum rate of return

- 92. Financial Policy A firm’s financial policy indicates the desired sources of financing and the particular mix

- 93. The Cost of Debt

- 94. The Cost of Debt See Example 9.1 Investor’s required rate of return on a 8% 20-year

- 95. The Cost of Preferred Stock If flotation costs are incurred, preferred stockholder’s required rate of return

- 96. The Cost of Common Equity Cost of equity is more challenging to estimate than the cost

- 97. Cost Estimation Techniques Two commonly used methods for estimating common stockholder’s required rate of return are:

- 98. The Dividend Growth Model Investors’ required rate of return (For Retained Earnings): D1 = Dividends expected

- 99. The Dividend Growth Model Example: A company expects dividends this year to be $1.10, based upon

- 100. The Capital Asset Pricing Model Example: If beta is 1.25, risk-free rate is 1.5% and expected

- 101. Capital Asset Pricing Model Variable Estimates CAPM is easy to apply. Also, the estimates for model

- 102. The Weighted Average Cost of Capital Bringing it all together: WACC To estimate WACC, we need

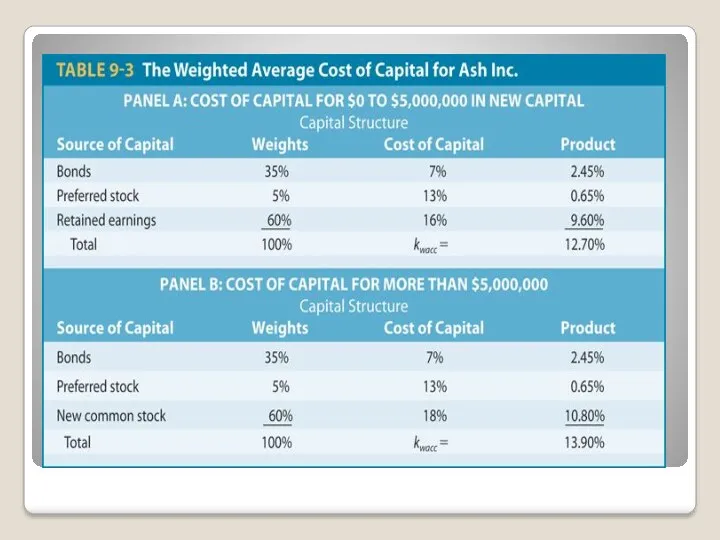

- 103. The Weighted Average Cost of Capital

- 104. Business World Cost of capital In practice, the calculation of cost of capital may be more

- 107. Divisional Costs of Capital Firms with multiple operating divisions often have unique risks and different costs

- 108. Advantages of Divisional WACC Different discount rates reflect differences in the systematic risk of the projects

- 109. Using Pure Play Firms to Estimate Divisional WACCs Divisional cost of capital can be estimated by

- 110. Divisional WACC Example Table 9-4 contains hypothetical estimates of the divisional WACC for the refining and

- 111. Divisional WACC – Estimation Issues and Limitations Sample chosen may not be a good match for

- 112. Cost of Capital to Evaluate New Capital Investments Cost of capital can serve as the discount

- 113. Figure 9-1

- 114. Capital Budgeting Meaning: The process of decision making with respect to investments in fixed assets—that is,

- 115. Capital-Budgeting Decision Criteria The Payback Period Net Present Value Profitability Index Internal Rate of Return

- 116. The Payback Period Meaning: Number of years needed to recover the initial cash outlay related to

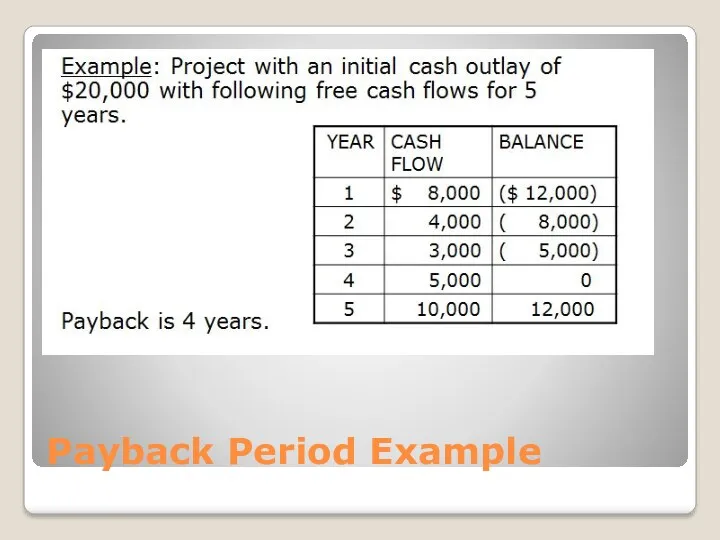

- 117. Payback Period Example

- 118. The Payback Period - Trade-Offs Benefits: Uses cash flows rather than accounting profits Easy to compute

- 119. Discounted Payback Period The discounted payback period is similar to the traditional payback period except that

- 120. Discounted Payback Period Table 10-2 shows the difference between traditional payback and discounted payback methods. With

- 121. Discounted Payback Period

- 122. Net Present Value (NPV) NPV is equal to the present value of all future free cash

- 123. NPV Example Example: Project with an initial cash outlay of $60,000 with following free cash flows

- 124. NPV Trade-Offs Benefits Considers all cash flows Recognizes time value of money Drawbacks Requires detailed long-term

- 125. The Profitability Index (PI) (Benefit-Cost Ratio) The profitability index (PI) is the ratio of the present

- 126. Profitability Index

- 127. Profitability Index Example A firm with a 10% required rate of return is considering investing in

- 128. Profitability Index Example PI = ($13,636 + $6,612 + $7,513 + $8,196 + $8,693 + $9,032)

- 129. NPV and PI When the present value of a project’s free cash inflows are greater than

- 130. Internal Rate of Return (IRR) Decision Rule: If IRR ≥ Required Rate of Return, accept If

- 131. Figure 10-1

- 132. IRR and NPV If NPV is positive, IRR will be greater than the required rate of

- 133. IRR Example Initial Outlay: $3,817 Cash flows: Yr. 1 = $1,000, Yr. 2 = $2,000, Yr.

- 134. Guidelines for Capital Budgeting To evaluate investment proposals, we must first set guidelines by which we

- 135. Guidelines for Capital Budgeting Use Free Cash Flows Rather than Accounting Profits Think Incrementally Beware of

- 136. CALCULATING A PROJECT’S FREE CASH FLOWS Three components of free cash flows: The initial outlay, The

- 137. Three Perspectives on Risk Project standing alone risk Project’s contribution-to-firm risk Systematic risk

- 138. Project Standing Alone Risk This is a project’s risk ignoring the fact that much of the

- 139. Contribution-to-Firm Risk This is the amount of risk that the project contributes to the firm as

- 140. Systematic Risk Risk of the project from the viewpoint of a well-diversified shareholder. This measure takes

- 142. Relevant Risk Theoretically, the only risk of concern to shareholders is systematic risk. Since the project’s

- 143. Incorporating Risk into Capital Budgeting Investors demand higher returns for more risky projects. As the risk

- 144. Risk Risk is variability associated with expected revenue or income streams. Such variability may arise due

- 145. Business Risk Business risk is the variation in the firm’s expected earnings attributable to the industry

- 146. Operating Risk Operating risk is the variation in the firm’s operating earnings that results from firm’s

- 147. Financial Risk Financial risk is the variation in earnings as a result of firm’s financing mix

- 148. Capital Structure Theory Theory focuses on the effect of financial leverage on the overall cost of

- 149. Capital Structure Theory Figure 12-5 shows that the firm’s value remains the same, despite the differences

- 152. Capital Structure Theory The implication of these figures for financial managers is that one capital structure

- 153. Extensions to Independence Hypothesis: The Moderate Position The moderate position considers how the capital structure decision

- 154. Impact of Taxes on Capital Structure Interest expense is tax deductible. Because interest is deductible, the

- 155. Impact of Taxes on Capital Structure Since interest on debt is tax deductible, the higher the

- 156. Impact of Bankruptcy on Capital Structure The probability that a firm will be unable to meet

- 158. Firm Value and Agency Costs

- 159. Managerial Implications Determining the firm’s financing mix is critically important for the manager. The decision to

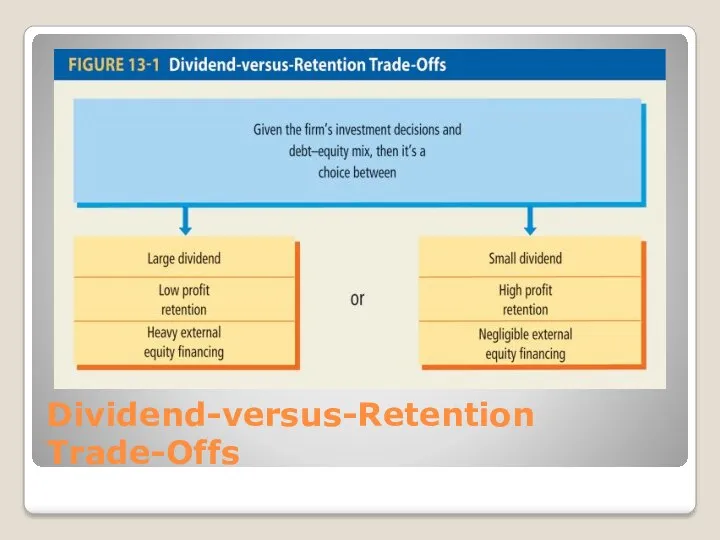

- 160. Dividends Dividends are distribution from the firm’s assets to the shareholders. Firms are not obligated to

- 161. Dividend Policy A firm’s dividend policy includes two components: Dividend Payout ratio Indicates amount of dividend

- 162. Dividend-versus-Retention Trade-Offs

- 163. DOES DIVIDEND POLICY MATTER TO STOCKHOLDERS? There are three basic views with regard to the impact

- 164. View #1 Dividend policy is irrelevant Irrelevance implies shareholder wealth is not affected by dividend policy

- 165. View #2 High dividends increase stock value This position in based on “bird-in-the-hand theory,” which argues

- 166. View #3 Low dividend increases stock values In 2003, the tax rates on capital gains and

- 167. Some Other Explanations The Residual Dividend Theory Clientele Effect The Information Effect Agency Costs The Expectations

- 168. Residual Dividend Theory Determine the optimal capital budget Determine the amount of equity needed for financing

- 169. The Clientele Effect Different groups of investors have varying preferences towards dividends. For example, some investors

- 170. The Information Effect Evidence shows that large, unexpected change in dividends can have a significant impact

- 171. Agency Costs Dividend policy may be perceived as a tool to minimize agency costs. Dividend payment

- 172. The Expectations Theory Expectation theory suggests that the market reaction does not only reflect response to

- 173. Conclusions on Dividend Policy Here are some conclusions about the relevance of dividend policy: As a

- 174. The Dividend Decision in Practice Legal Restrictions Statutory restrictions may prevent a company from paying dividends.

- 175. The Dividend Decision in Practice - Alternative Dividend Policies Constant dividend payout ratio The percentage of

- 176. The Dividend Decision in Practice - Alternative Dividend Policies A small regular dividend plus a year-end

- 177. Dividend Payment Procedures Generally, companies pay dividend on a quarterly basis. The final approval of a

- 178. Important Dates Declaration date – The date when the dividend is formally declared by the board

- 179. Stock Dividends A stock dividend entails the distribution of additional shares of stock in lieu of

- 180. Stock Splits A stock split involves exchanging more (or less in the case of “reverse” split)

- 181. Stock Repurchases A stock repurchase (stock buyback) occurs when a firm repurchases its own stock. This

- 182. Stock Repurchase -- Benefits A means of providing an internal investment opportunity An approach for modifying

- 183. A Share Repurchase as a Dividend, Financing, Investment Decision When a firm repurchases stock when it

- 184. Unsecured Sources: Trade Credit Trade credit arises spontaneously with the firm’s purchases. Often, the credit terms

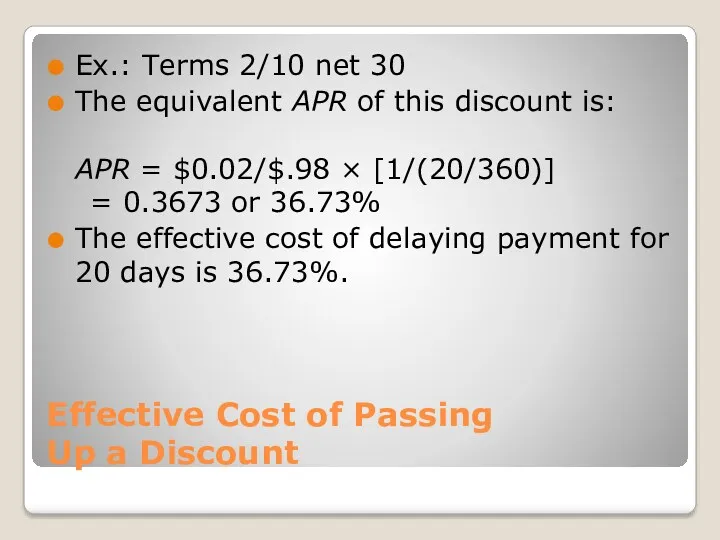

- 186. Effective Cost of Passing Up a Discount Ex.: Terms 2/10 net 30 The equivalent APR of

- 187. Unsecured Sources: Bank Credit Commercial banks provide unsecured short-term credit in two forms: Lines of credit

- 188. Line of Credit Informal agreement between a borrower and a bank about the maximum amount of

- 189. Revolving Credit Revolving credit is a variant of the line of credit form of financing. A

- 190. Transaction Loans A transaction loan is made for a specific purpose. This is the type of

- 191. Unsecured Sources: Commercial Paper The largest and most credit-worthy companies are able to use commercial paper—a

- 192. Commercial Paper: Advantages Interest rates Rates are generally lower than rates on bank loans Compensating-balance requirement

- 193. Secured Sources of Loans Secured loans have assets of the firm pledged as collateral. If there

- 194. Pledging Accounts Receivable Borrower pledges accounts receivable as collateral for a loan obtained from either a

- 195. Pledging Accounts Receivable Credit Terms: Interest rate is 2–5% higher than the bank’s prime rate. In

- 196. Pledging Accounts Receivable Factoring accounts receivable involves the outright sale of a firm’s accounts to a

- 197. Secured Sources: Inventory Loans These are loans secured by inventories. The amount of the loan that

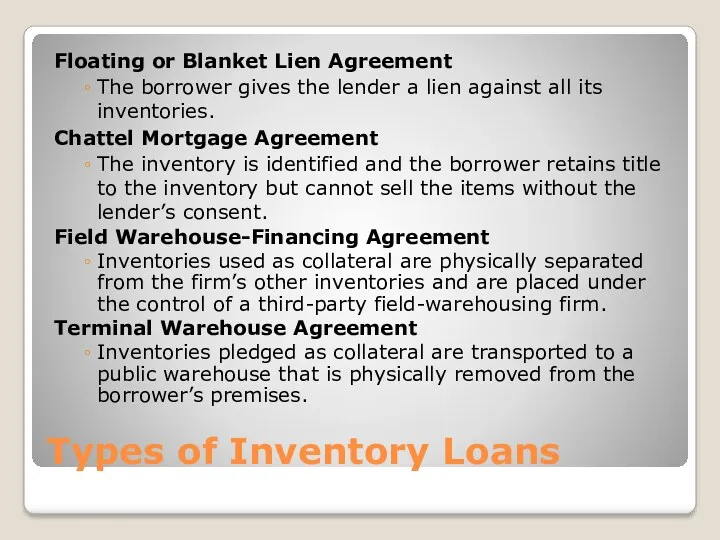

- 198. Types of Inventory Loans Floating or Blanket Lien Agreement The borrower gives the lender a lien

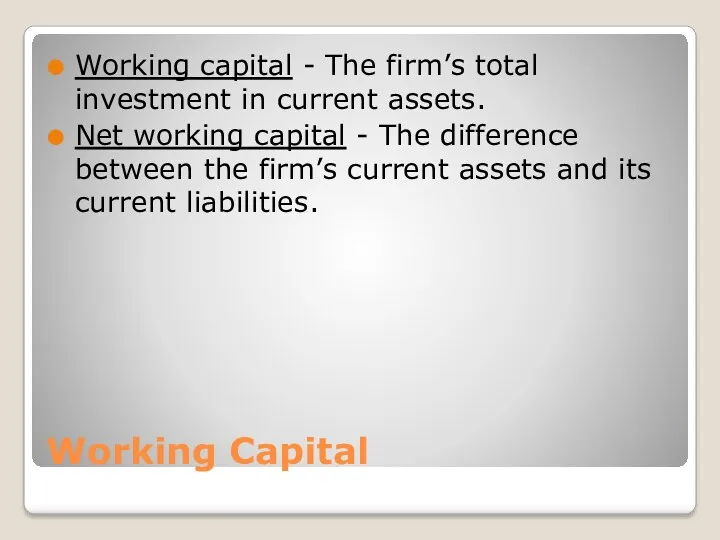

- 199. Working Capital Working capital - The firm’s total investment in current assets. Net working capital -

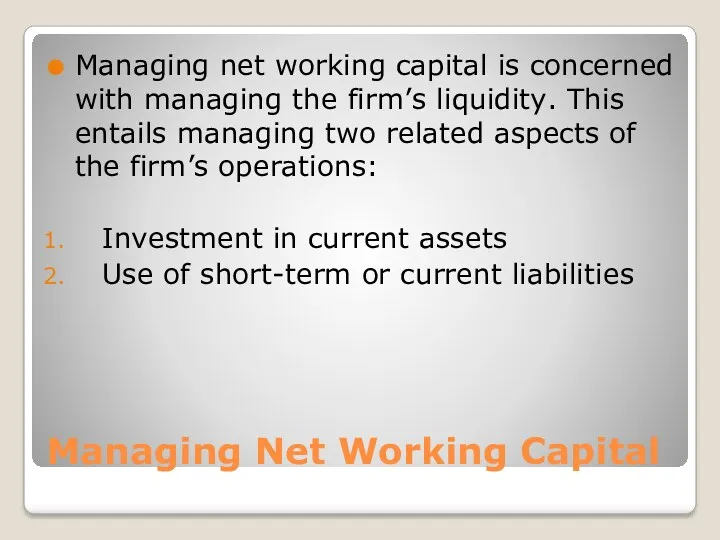

- 200. Managing Net Working Capital Managing net working capital is concerned with managing the firm’s liquidity. This

- 201. How Much Short-Term Financing Should a Firm Use? This question is addressed by hedging principle of

- 202. The Appropriate Level of Working Capital Managing working capital involves interrelated decisions regarding investments in current

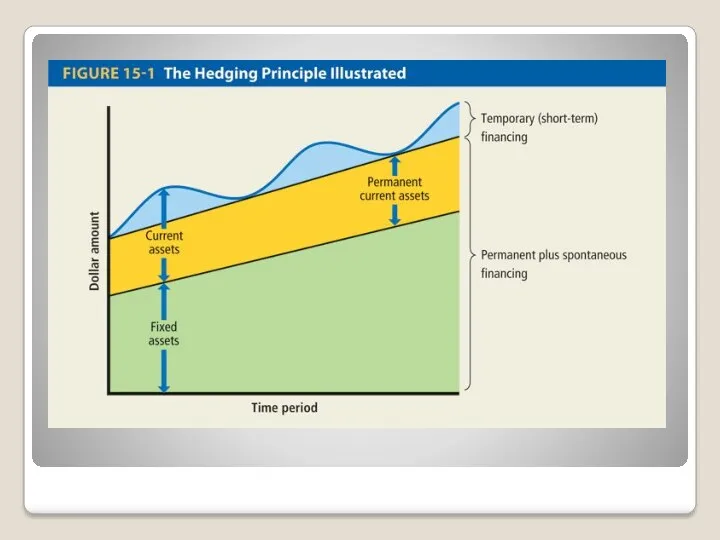

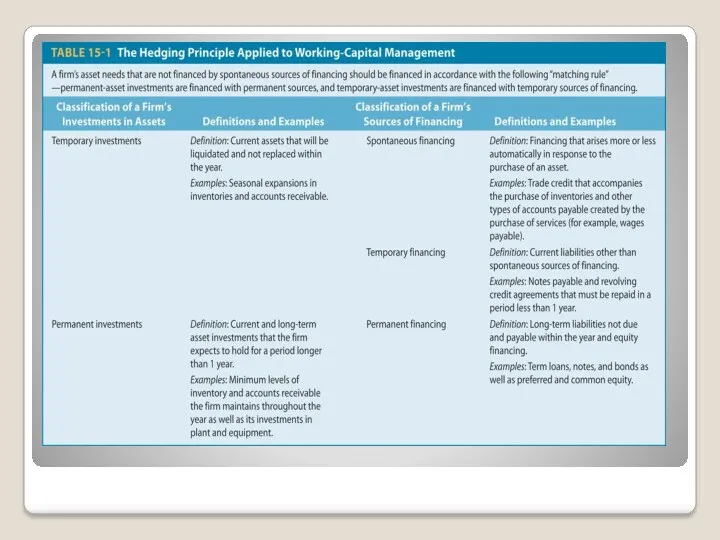

- 203. The Hedging Principle The hedging principle involves matching the cash-flow-generating characteristics of an asset with the

- 205. Permanent and Temporary Assets Permanent investments Investments that the firm expects to hold for a period

- 206. Temporary and Permanent Sources of Financing Temporary sources of financing consist of current liabilities such as

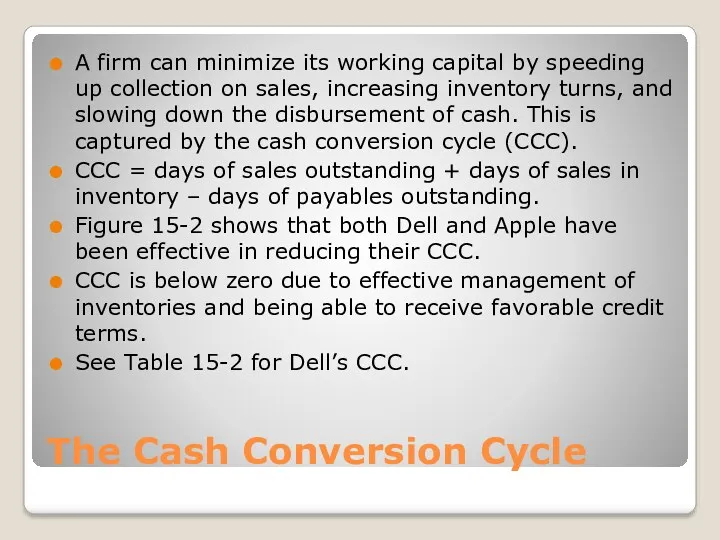

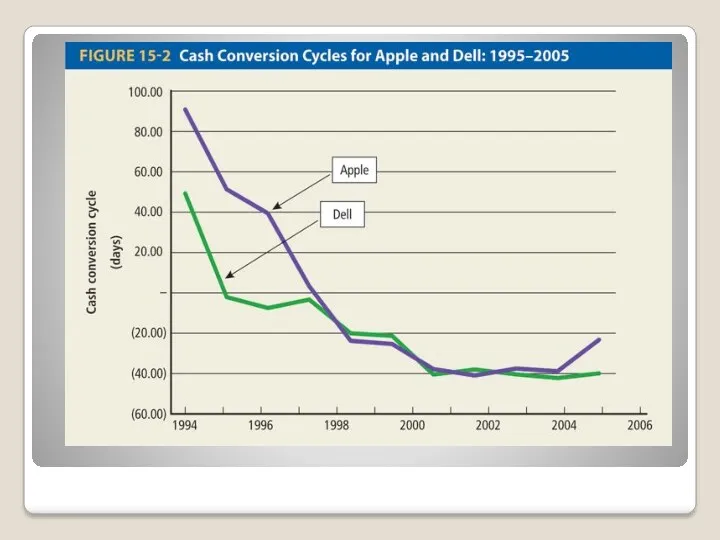

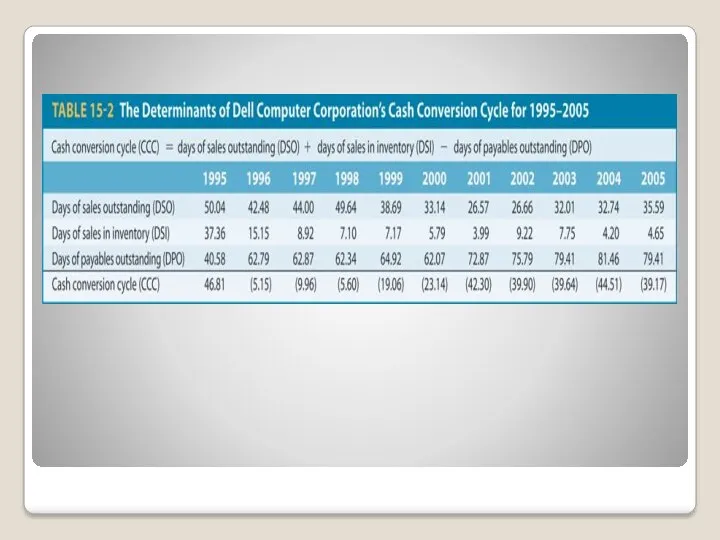

- 208. The Cash Conversion Cycle A firm can minimize its working capital by speeding up collection on

- 211. Cost of Short-Term Credit

- 212. APR example A company plans to borrow $1,000 for 90 days. At maturity, the company will

- 213. Annual Percentage Yield (APY) APR does not consider compound interest. To account for the influence of

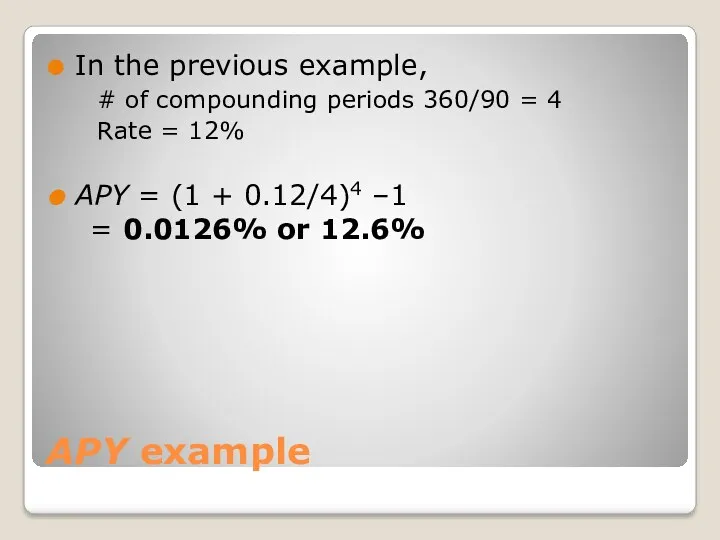

- 214. APY example In the previous example, # of compounding periods 360/90 = 4 Rate = 12%

- 216. Скачать презентацию

Examination paper format

Answer FOUR (4) out of SIX (6) questions

Each question

Examination paper format

Answer FOUR (4) out of SIX (6) questions

Each question

Question 1

(a) Calculation (10 marks)

(b) Theory : Discuss (15 marks)

(25 marks)

Question 2

(a) Calculation (13

Question 1

(a) Calculation (10 marks)

(b) Theory : Discuss (15 marks)

(25 marks)

Question 2

(a) Calculation (13

Question 3

Theory : Explain (25 marks)

Question 4

Theory : Discuss (25 marks)

Question 3

Theory : Explain (25 marks)

Question 4

Theory : Discuss (25 marks)

Question 5

Theory and show calculations to support theory:

Evaluate and analyze

Question 5

Theory and show calculations to support theory:

Evaluate and analyze

The Goal of the Firm

The goal of the firm is to

The Goal of the Firm

The goal of the firm is to

3 Roles of Finance in Business

What long-term investments should the firm

3 Roles of Finance in Business

What long-term investments should the firm

Role of the Financial Manager

Role of the Financial Manager

Legal Forms of Business Organization

Legal Forms of Business Organization

Sole Proprietorship

Business owned by an individual

Owner maintains title to assets and

Sole Proprietorship

Business owned by an individual

Owner maintains title to assets and

Partnership

Two or more persons come together as co-owners

General Partnership: All partners

Partnership

Two or more persons come together as co-owners

General Partnership: All partners

Corporation

Legally functions separate and apart from its owners

Corporation can sue, be

Corporation

Legally functions separate and apart from its owners

Corporation can sue, be

Hybrid Organizations: S-Corporation

Benefits

Limited liability

Taxed as partnership (no double taxation like corporations)

Limitations

Owners

Hybrid Organizations: S-Corporation

Benefits

Limited liability

Taxed as partnership (no double taxation like corporations)

Limitations

Owners

Hybrid Organizations:

Limited Liability Companies (LLCs)

Benefits

Limited liability

Taxed like a partnership

Limitations

Qualifications

Hybrid Organizations:

Limited Liability Companies (LLCs)

Benefits

Limited liability

Taxed like a partnership

Limitations

Qualifications

Finance and The Multinational Firm: The New Role

U.S. firms are looking

Finance and The Multinational Firm: The New Role

U.S. firms are looking

Why Do Companies Go Abroad?

To increase revenues

To reduce expenses (land, labor,

Why Do Companies Go Abroad?

To increase revenues

To reduce expenses (land, labor,

Risks/Challenges of Going Abroad

Country risk (changes in government regulations, unstable government,

Risks/Challenges of Going Abroad

Country risk (changes in government regulations, unstable government,

What Is Liquidity?

Liquidity is the term used to describe how easy

What Is Liquidity? Liquidity is the term used to describe how easy

How Liquid Is the Firm?

A liquid asset is one that can

How Liquid Is the Firm?

A liquid asset is one that can

Measuring Liquidity:

Perspective 1

Compare a firm’s current assets with current liabilities

Measuring Liquidity:

Perspective 1

Compare a firm’s current assets with current liabilities

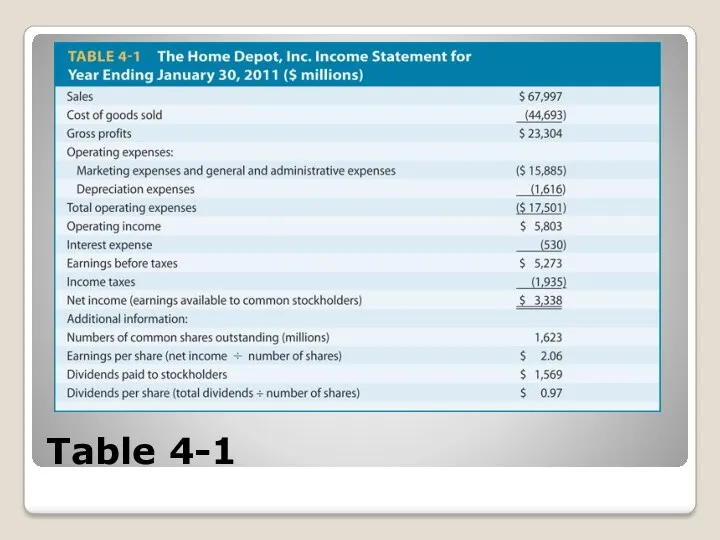

Table 4-1

Table 4-1

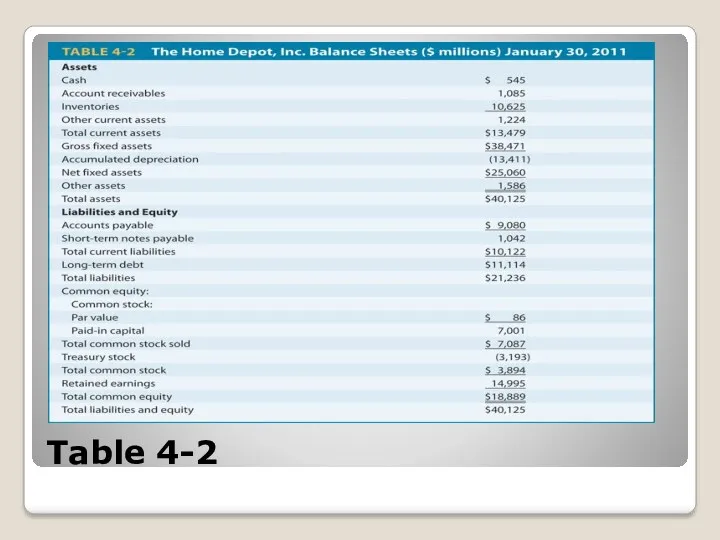

Table 4-2

Table 4-2

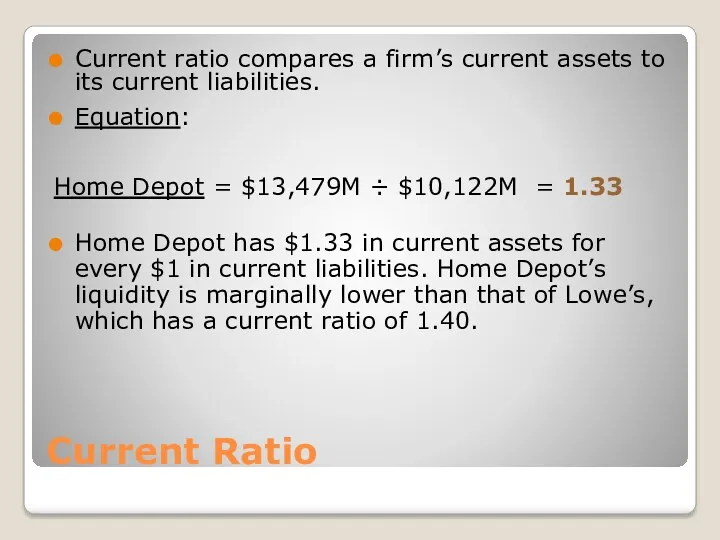

Current Ratio

Current ratio compares a firm’s current assets to its current

Current Ratio

Current ratio compares a firm’s current assets to its current

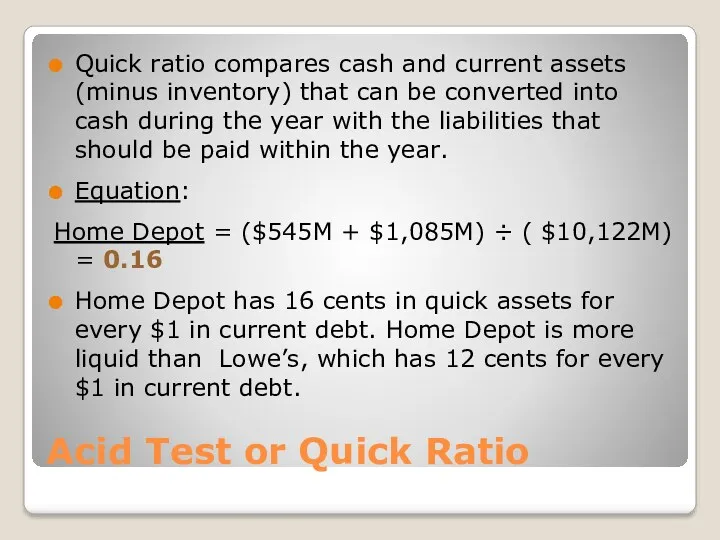

Acid Test or Quick Ratio

Quick ratio compares cash and current assets

Acid Test or Quick Ratio

Quick ratio compares cash and current assets

Measuring Liquidity:

Perspective 2

Measures a firm’s ability to convert accounts receivable and

Measuring Liquidity:

Perspective 2

Measures a firm’s ability to convert accounts receivable and

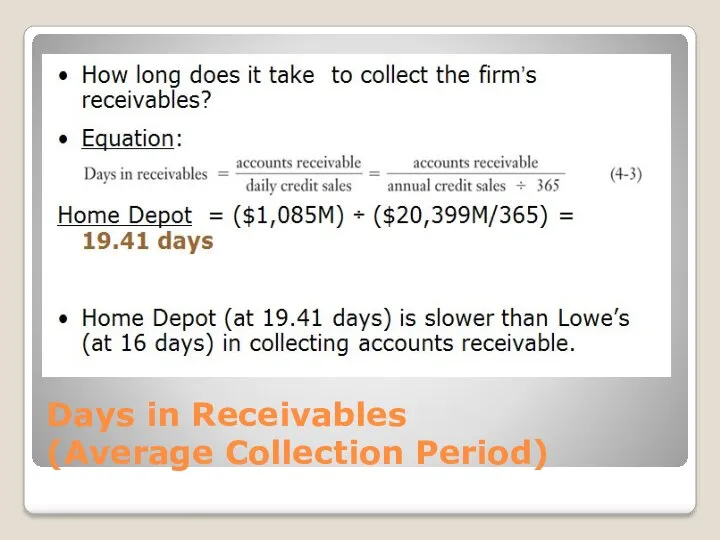

Days in Receivables

(Average Collection Period)

Days in Receivables

(Average Collection Period)

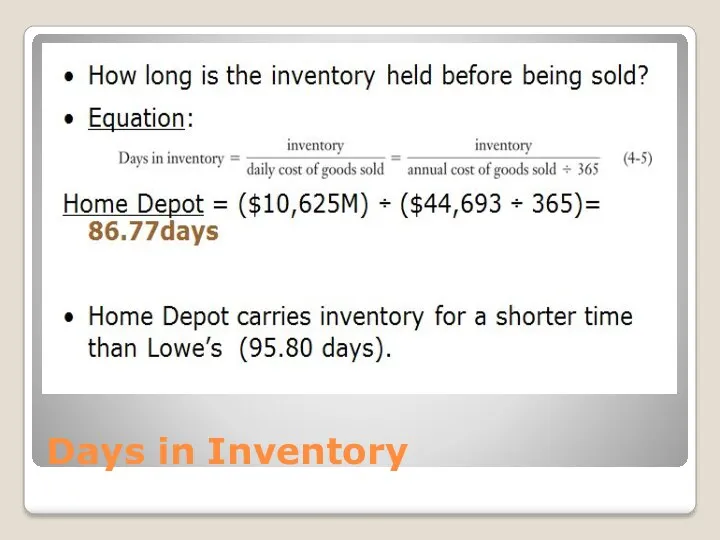

Days in Inventory

Days in Inventory

Certificates of deposit are slightly less liquid, because there is usually a

Certificates of deposit are slightly less liquid, because there is usually a

Each of the above can be considered as cash or cash

Each of the above can be considered as cash or cash

Other examples are items like coins, stamps, art and other collectibles.

Other examples are items like coins, stamps, art and other collectibles.

Cash is a company's lifeblood. In other words, a company can

Cash is a company's lifeblood. In other words, a company can

Depending on the industry, companies with good liquidity will usually have

Depending on the industry, companies with good liquidity will usually have

A more stringent measure is the quick ratio, sometimes called the acid

A more stringent measure is the quick ratio, sometimes called the acid

One last ratio of note is the debt/equity ratio, usually defined as

One last ratio of note is the debt/equity ratio, usually defined as

Are the Firm’s Managers

Generating Adequate Operating Profits from the Company’s

Are the Firm’s Managers Generating Adequate Operating Profits from the Company’s

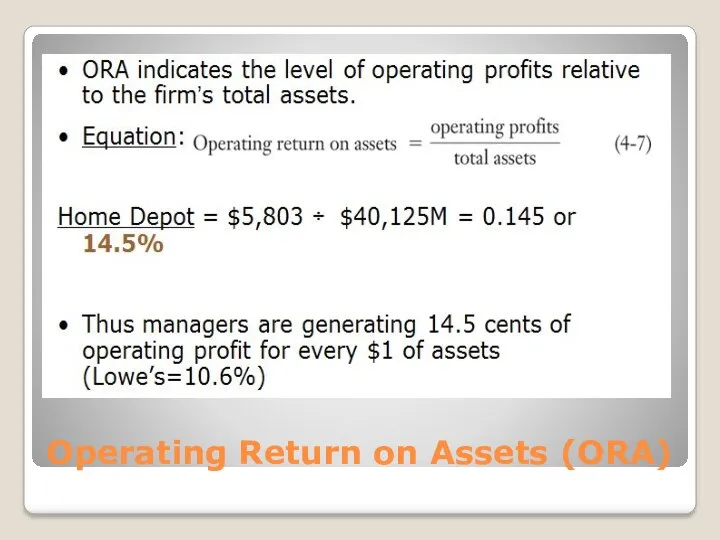

Operating Return on Assets (ORA)

Operating Return on Assets (ORA)

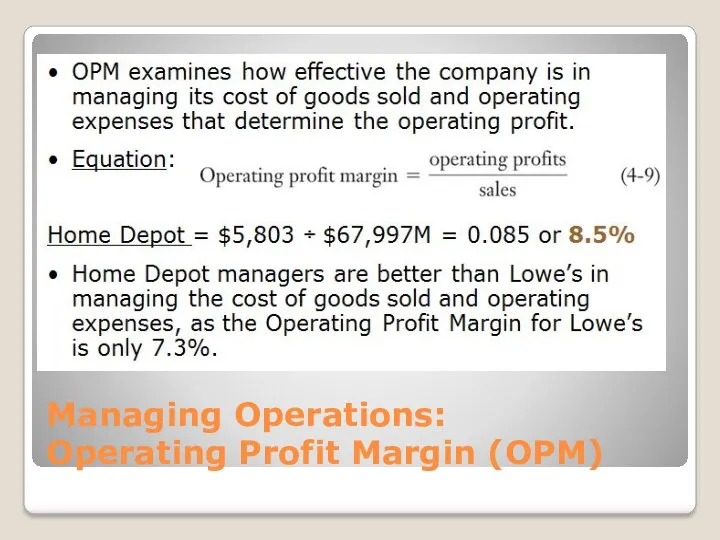

Managing Operations:

Operating Profit Margin (OPM)

Managing Operations:

Operating Profit Margin (OPM)

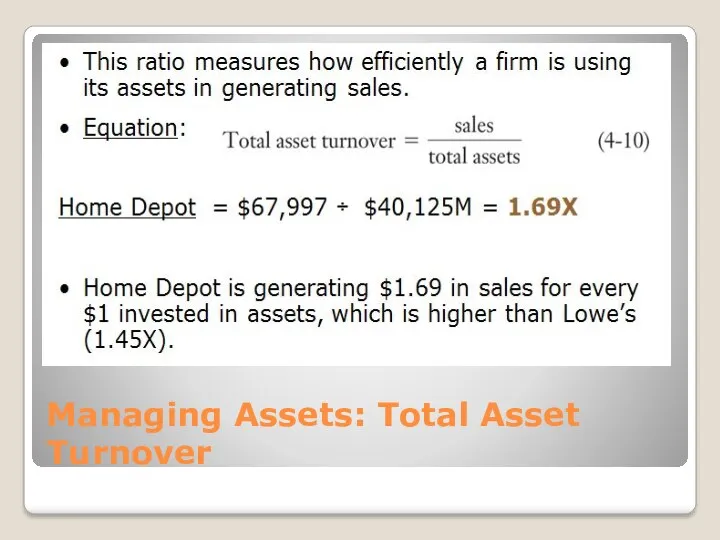

Managing Assets: Total Asset Turnover

Managing Assets: Total Asset Turnover

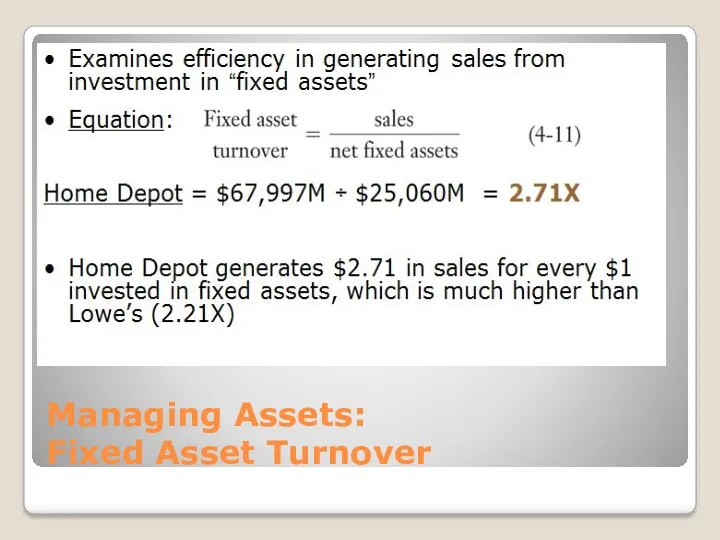

Managing Assets:

Fixed Asset Turnover

Managing Assets:

Fixed Asset Turnover

How Is the Firm Financing Its Assets?

Does the firm finance its

How Is the Firm Financing Its Assets?

Does the firm finance its

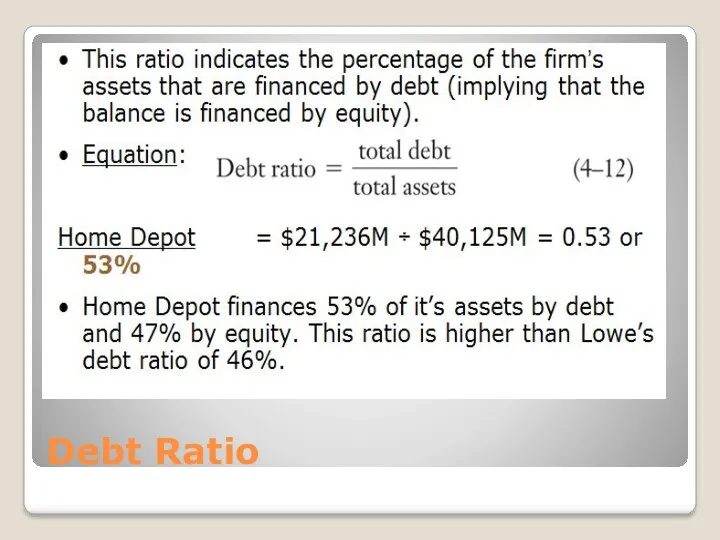

Debt Ratio

Debt Ratio

Times Interest Earned

This ratio indicates the amount of operating income available

Times Interest Earned

This ratio indicates the amount of operating income available

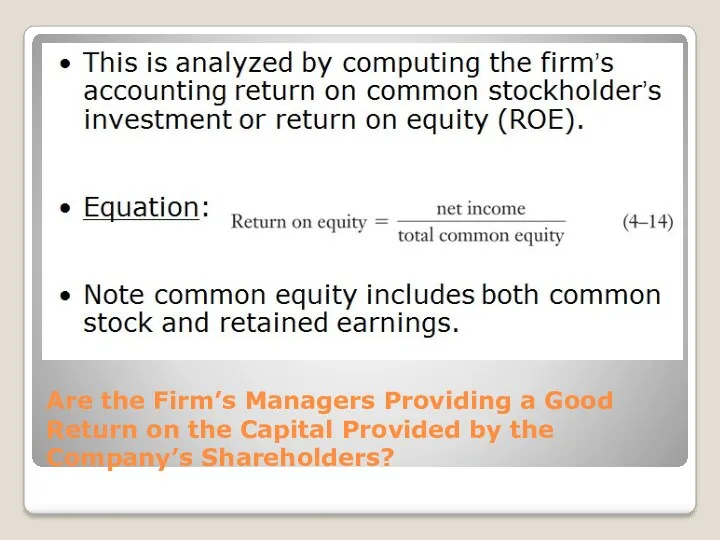

Are the Firm’s Managers Providing a Good Return on the Capital

Are the Firm’s Managers Providing a Good Return on the Capital

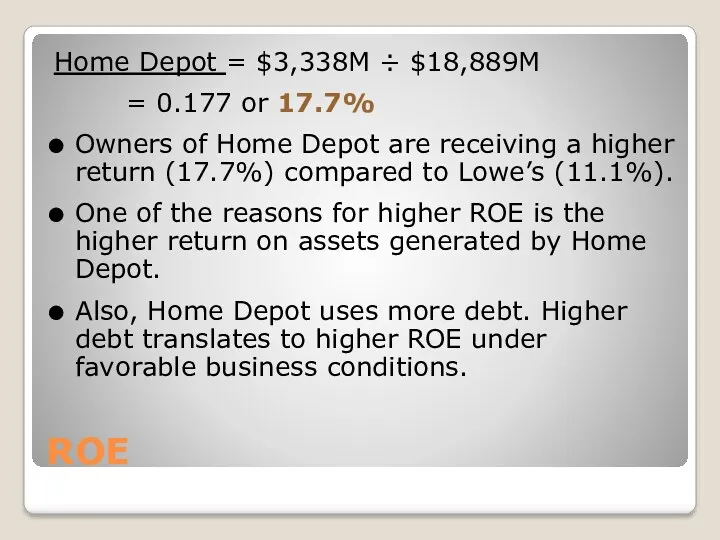

ROE

Home Depot = $3,338M ÷ $18,889M

= 0.177 or 17.7%

Owners of

ROE

Home Depot = $3,338M ÷ $18,889M

= 0.177 or 17.7%

Owners of

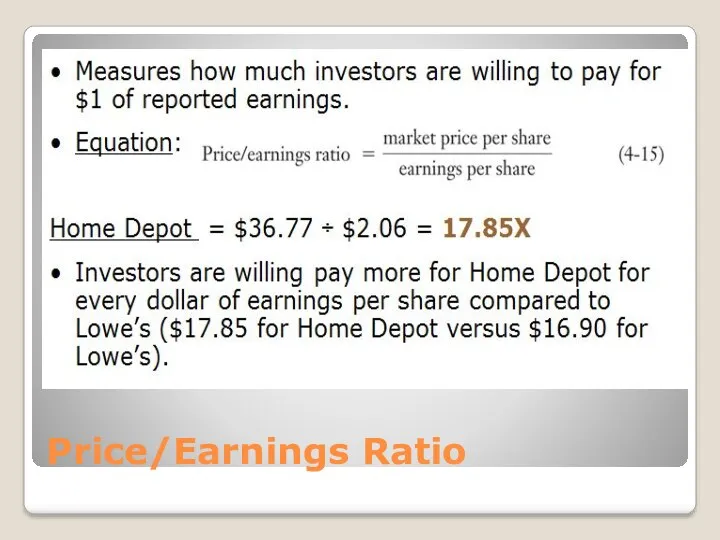

Price/Earnings Ratio

Price/Earnings Ratio

Limitations of

Financial Ratio Analysis

It is sometimes difficult to identify industry

Limitations of

Financial Ratio Analysis

It is sometimes difficult to identify industry

Introduction to Finance

Chapter 5 – Stock valuation

Introduction to Finance

Chapter 5 – Stock valuation

Learning Objectives

Identify the basic characteristics of preferred stock.

Value preferred stock.

Identify the

Learning Objectives

Identify the basic characteristics of preferred stock.

Value preferred stock.

Identify the

Preferred Stock

Preferred stock is often referred to as a hybrid security

Preferred Stock

Preferred stock is often referred to as a hybrid security

Characteristics of Preferred Stocks

Multiple series of preferred stock

Preferred stock’s claim on

Characteristics of Preferred Stocks

Multiple series of preferred stock

Preferred stock’s claim on

Multiple Series

If a company desires, it can issue more than one

Multiple Series

If a company desires, it can issue more than one

Claim on Assets and Income

Claim on Assets: Preferred stock has priority

Claim on Assets and Income

Claim on Assets: Preferred stock has priority

Cumulative Dividends

Cumulative feature (if it exists) requires that all past, unpaid

Cumulative Dividends

Cumulative feature (if it exists) requires that all past, unpaid

Protective Provisions

Protective provisions generally allow for voting rights in the event

Protective Provisions

Protective provisions generally allow for voting rights in the event

Convertibility

Convertible preferred stock can, at the discretion of the holder, be

Convertibility

Convertible preferred stock can, at the discretion of the holder, be

Retirement Provisions

Although preferred stock has no set maturity associated with it,

Retirement Provisions

Although preferred stock has no set maturity associated with it,

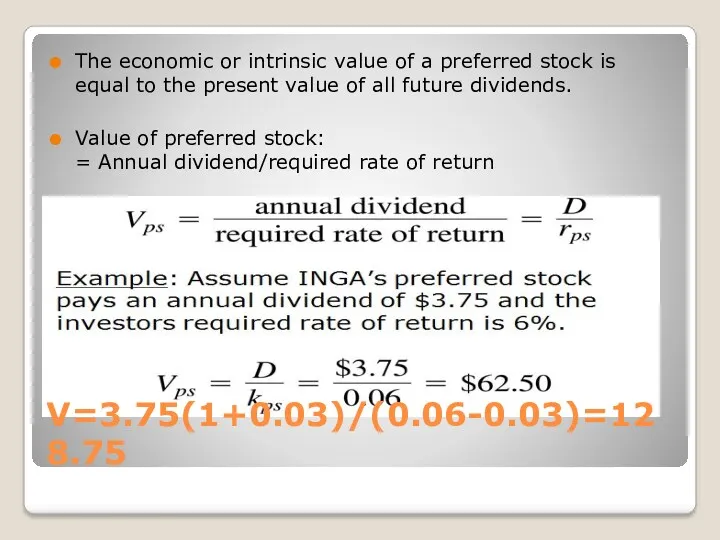

The economic or intrinsic value of a preferred stock is equal

The economic or intrinsic value of a preferred stock is equal

Common Stock

Common stock is a certificate that indicates ownership in a

Common Stock

Common stock is a certificate that indicates ownership in a

Claim on Income

Common shareholders have the right to residual income after

Claim on Income

Common shareholders have the right to residual income after

Claim on Assets

Common stock has a residual claim on assets in

Claim on Assets

Common stock has a residual claim on assets in

Limited Liability

The liability of shareholders is limited to the amount of

Limited Liability

The liability of shareholders is limited to the amount of

Voting Rights

Most often, common stockholders are the only security holders with

Voting Rights

Most often, common stockholders are the only security holders with

Preemptive Rights

Preemptive right entitles the common shareholder to maintain a proportionate

Preemptive Rights

Preemptive right entitles the common shareholder to maintain a proportionate

Valuing Common Stock

Like bonds and preferred stock, the value of common

Valuing Common Stock

Like bonds and preferred stock, the value of common

Dividend Model

Unlike preferred stock, common stock dividend is not fixed.

Dividend

Dividend Model

Unlike preferred stock, common stock dividend is not fixed.

Dividend

How Can a Company Grow?

Through Infusion of capital by borrowing

How Can a Company Grow?

Through Infusion of capital by borrowing

Plowback ratio pr

Internal Growth

g = ROE × pr

where:

g = the

Plowback ratio pr

Internal Growth

g = ROE × pr

where:

g = the

Dividend Valuation Model

Value of Common stock

= PV of future dividends

Vcs

Dividend Valuation Model

Value of Common stock

= PV of future dividends

Vcs

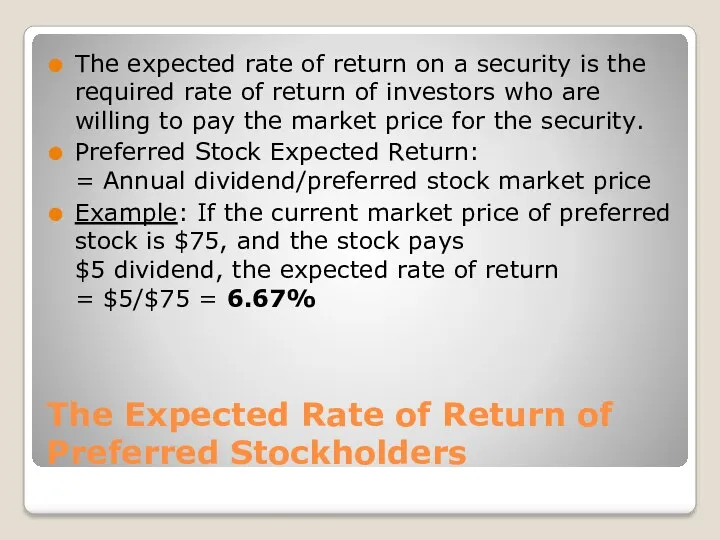

The Expected Rate of Return of Preferred Stockholders

The expected rate of

The Expected Rate of Return of Preferred Stockholders

The expected rate of

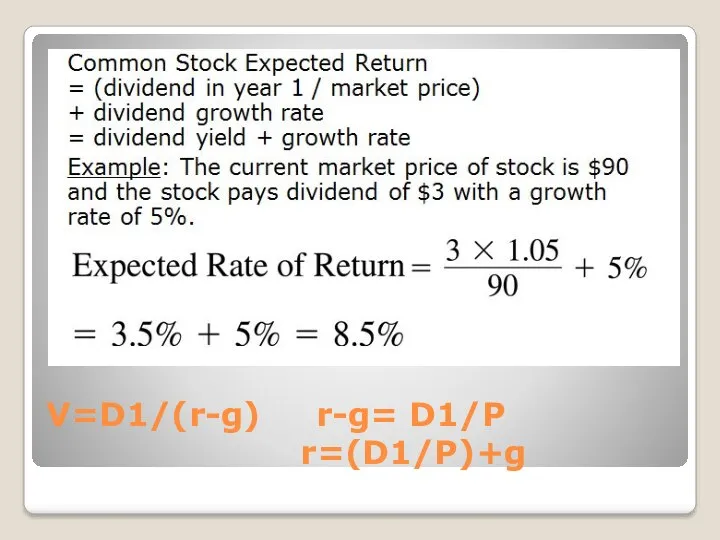

V=D1/(r-g) r-g= D1/P

r=(D1/P)+g

V=D1/(r-g) r-g= D1/P

r=(D1/P)+g

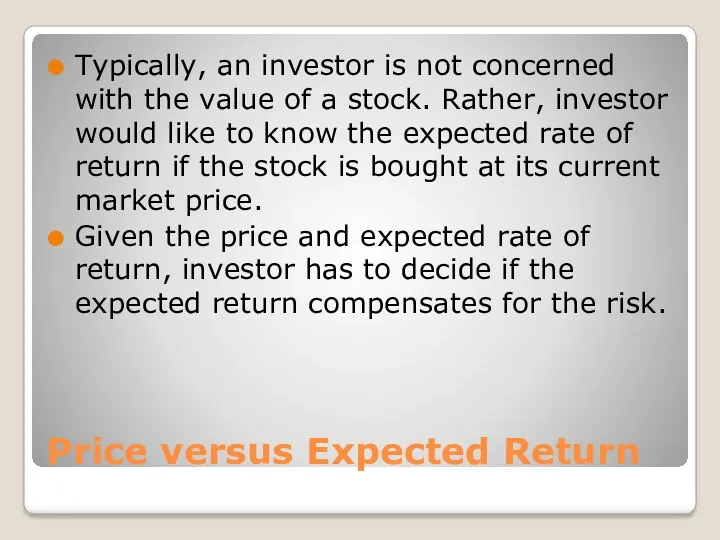

Price versus Expected Return

Typically, an investor is not concerned with the

Price versus Expected Return

Typically, an investor is not concerned with the

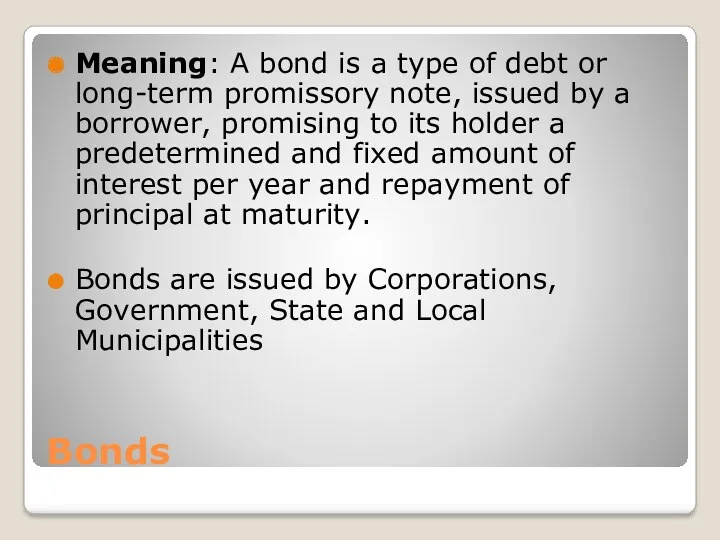

Bonds

Meaning: A bond is a type of debt or long-term promissory

Bonds

Meaning: A bond is a type of debt or long-term promissory

Debentures

Debentures are unsecured long-term debt.

For an issuing firm, debentures provide the

Debentures

Debentures are unsecured long-term debt.

For an issuing firm, debentures provide the

Subordinated Debentures

There is a hierarchy of payout in case of insolvency.

The

Subordinated Debentures

There is a hierarchy of payout in case of insolvency.

The

Mortgage Bonds

Mortgage bond is secured by a lien on real property.

Typically,

Mortgage Bonds

Mortgage bond is secured by a lien on real property.

Typically,

Eurobonds

Securities (bonds) issued in a country different from the one in

Eurobonds

Securities (bonds) issued in a country different from the one in

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Claims on Assets and Income

Seniority in claims

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Claims on Assets and Income

Seniority in claims

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Par Value

Par value is the face value

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Par Value

Par value is the face value

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Coupon Interest Rate

The percentage of the par

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Coupon Interest Rate

The percentage of the par

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Zero Coupon Bonds

Zero coupon bonds have zero

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Zero Coupon Bonds

Zero coupon bonds have zero

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Maturity

Maturity of bond refers to the length

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Maturity

Maturity of bond refers to the length

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Call Provision

Call provision (if it exists on

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Call Provision

Call provision (if it exists on

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Indenture

An indenture is the legal agreement between

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Indenture

An indenture is the legal agreement between

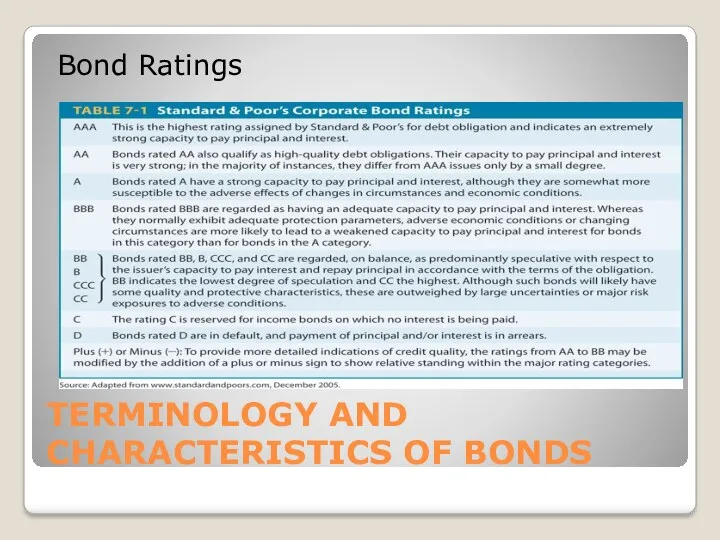

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Bond Ratings

Bond ratings reflect the future risk

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Bond Ratings

Bond ratings reflect the future risk

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Bond Ratings

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Bond Ratings

TERMINOLOGY AND CHARACTERISTICS OF BONDS

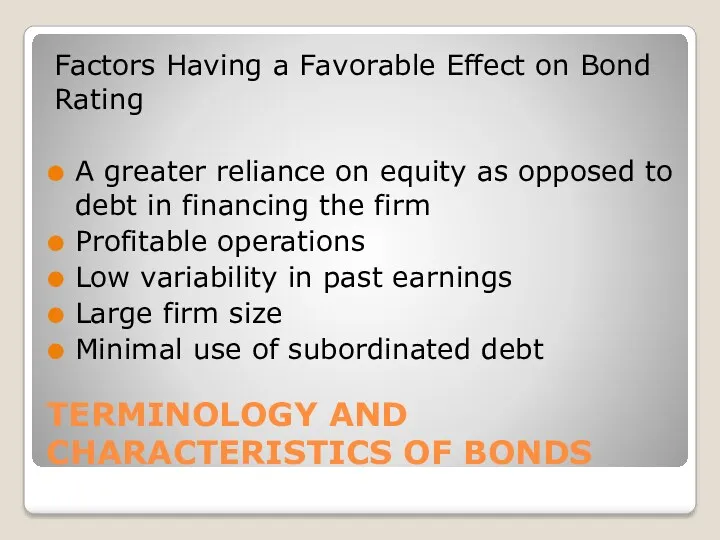

Factors Having a Favorable Effect on Bond

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Factors Having a Favorable Effect on Bond

TERMINOLOGY AND CHARACTERISTICS OF BONDS

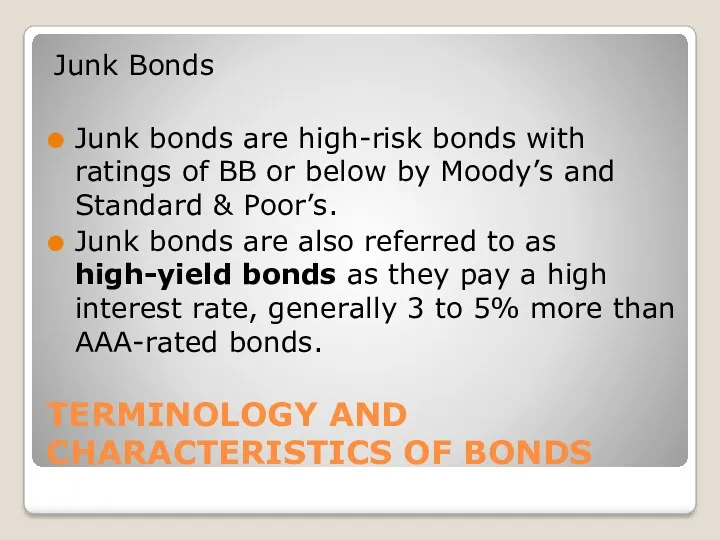

Junk Bonds

Junk bonds are high-risk bonds with

TERMINOLOGY AND CHARACTERISTICS OF BONDS

Junk Bonds

Junk bonds are high-risk bonds with

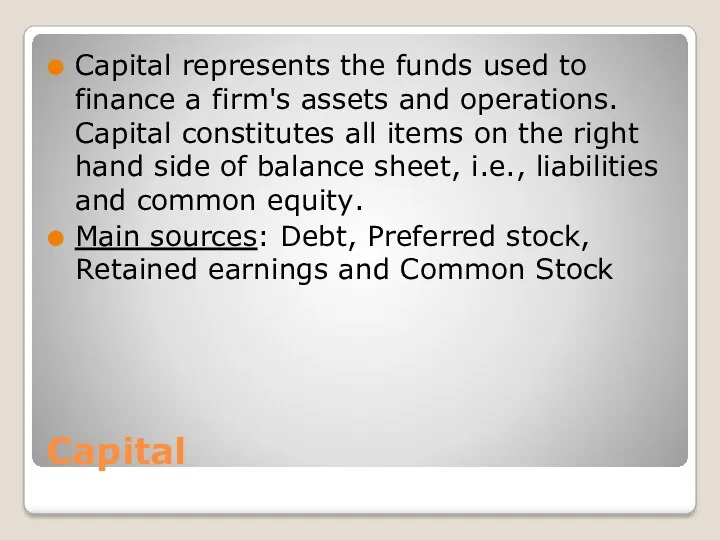

Capital

Capital represents the funds used to finance a firm's assets and

Capital

Capital represents the funds used to finance a firm's assets and

Cost of Capital

The firm’s cost of capital is also referred to

Cost of Capital

The firm’s cost of capital is also referred to

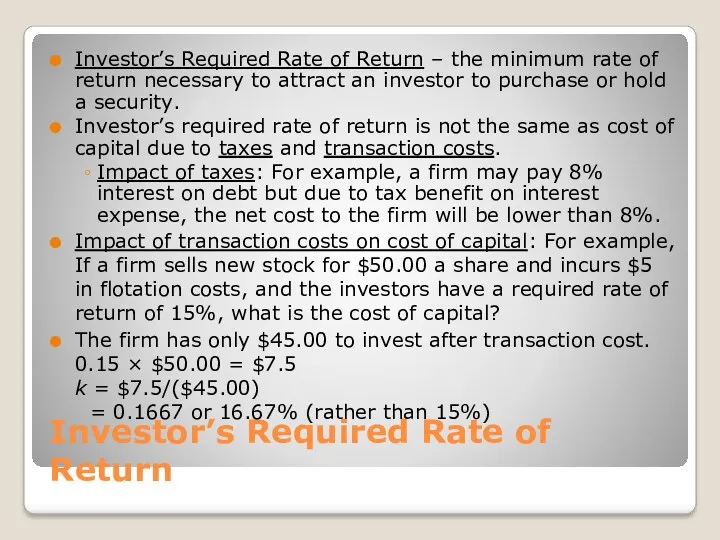

Investor’s Required Rate of Return

Investor’s Required Rate of Return – the

Investor’s Required Rate of Return

Investor’s Required Rate of Return – the

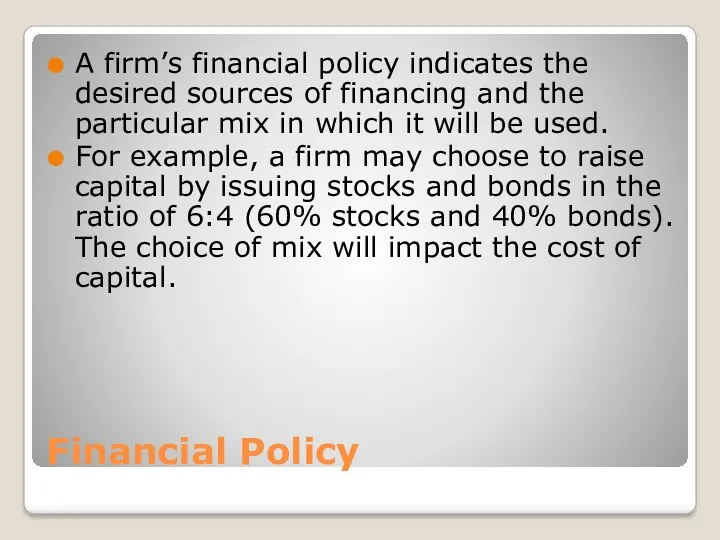

Financial Policy

A firm’s financial policy indicates the desired sources of financing

Financial Policy

A firm’s financial policy indicates the desired sources of financing

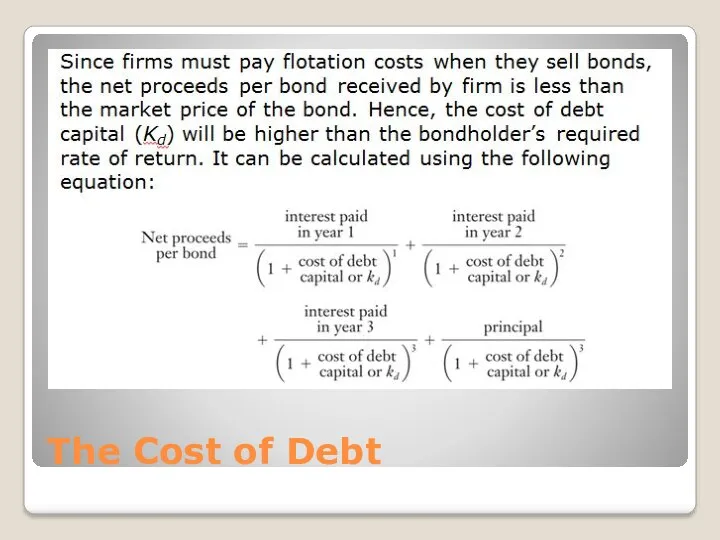

The Cost of Debt

The Cost of Debt

The Cost of Debt

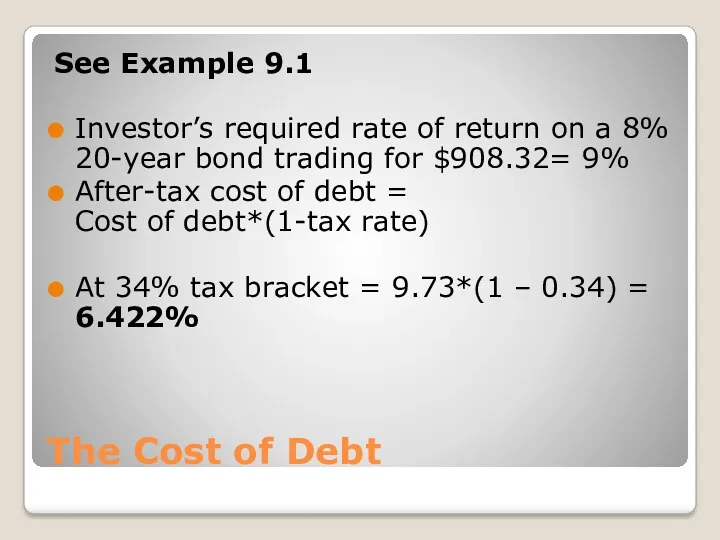

See Example 9.1

Investor’s required rate of return on

The Cost of Debt

See Example 9.1

Investor’s required rate of return on

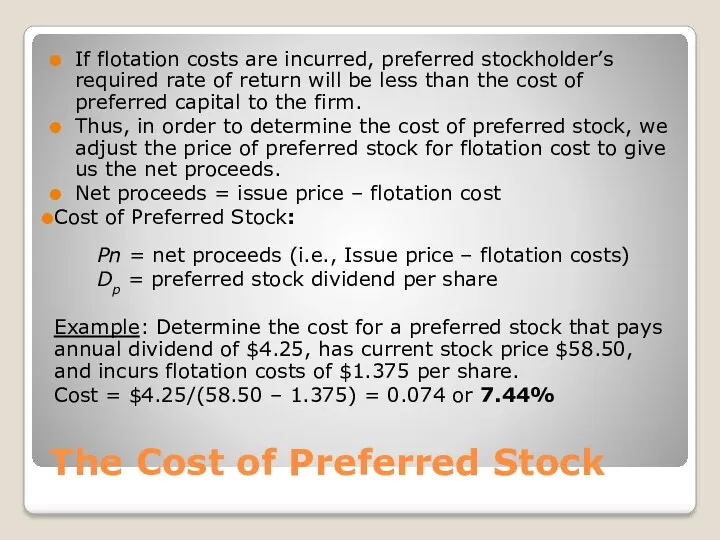

The Cost of Preferred Stock

If flotation costs are incurred, preferred stockholder’s

The Cost of Preferred Stock

If flotation costs are incurred, preferred stockholder’s

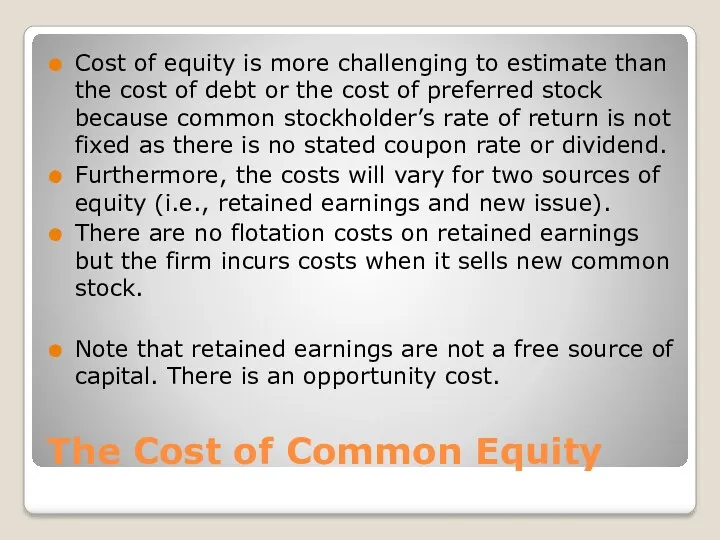

The Cost of Common Equity

Cost of equity is more challenging to

The Cost of Common Equity

Cost of equity is more challenging to

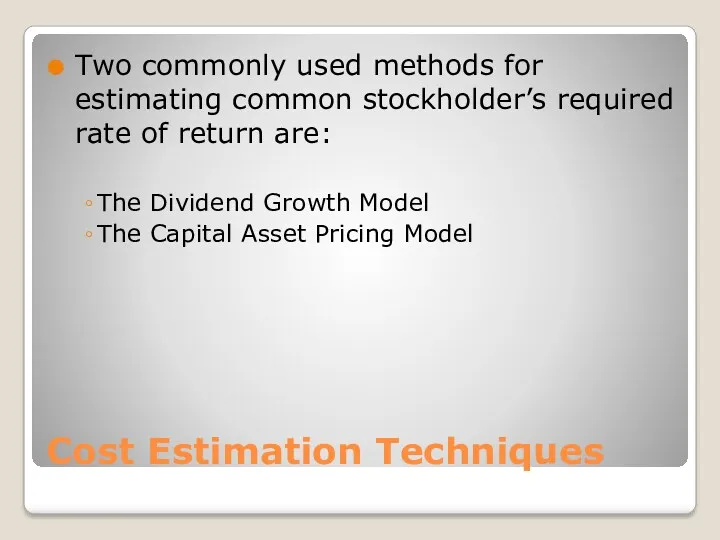

Cost Estimation Techniques

Two commonly used methods for estimating common stockholder’s required

Cost Estimation Techniques

Two commonly used methods for estimating common stockholder’s required

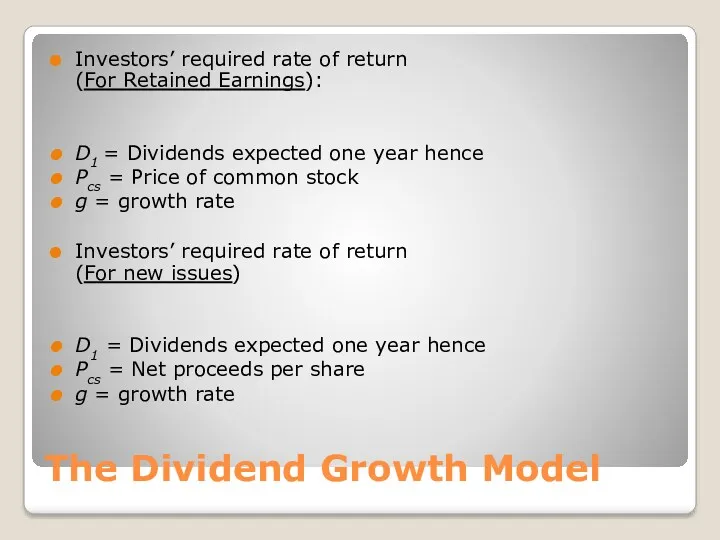

The Dividend Growth Model

Investors’ required rate of return

(For Retained Earnings):

D1

The Dividend Growth Model

Investors’ required rate of return

(For Retained Earnings):

D1

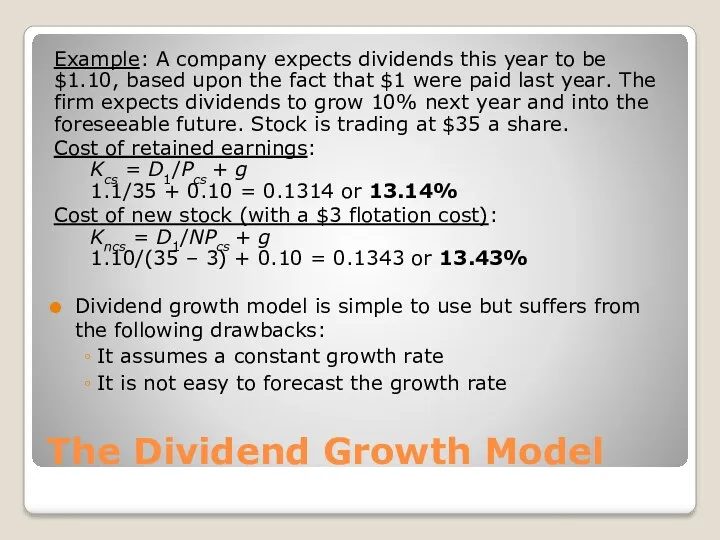

The Dividend Growth Model

Example: A company expects dividends this year to

The Dividend Growth Model

Example: A company expects dividends this year to

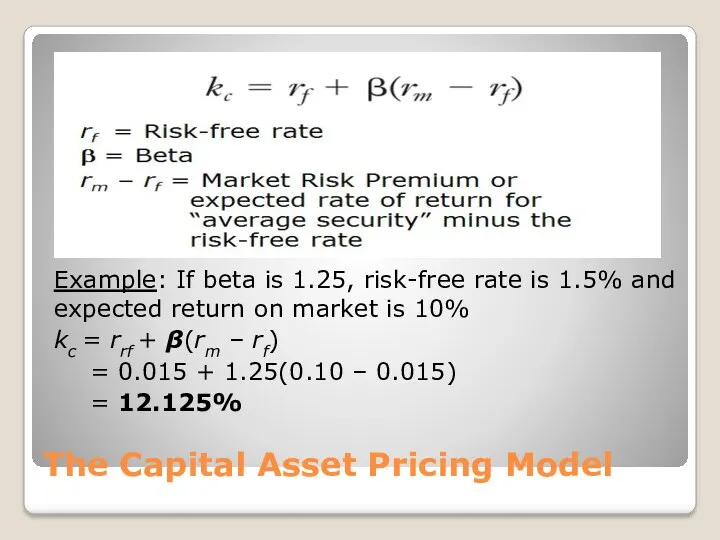

The Capital Asset Pricing Model

Example: If beta is 1.25, risk-free

The Capital Asset Pricing Model

Example: If beta is 1.25, risk-free

Capital Asset Pricing Model Variable Estimates

CAPM is easy to apply. Also,

Capital Asset Pricing Model Variable Estimates

CAPM is easy to apply. Also,

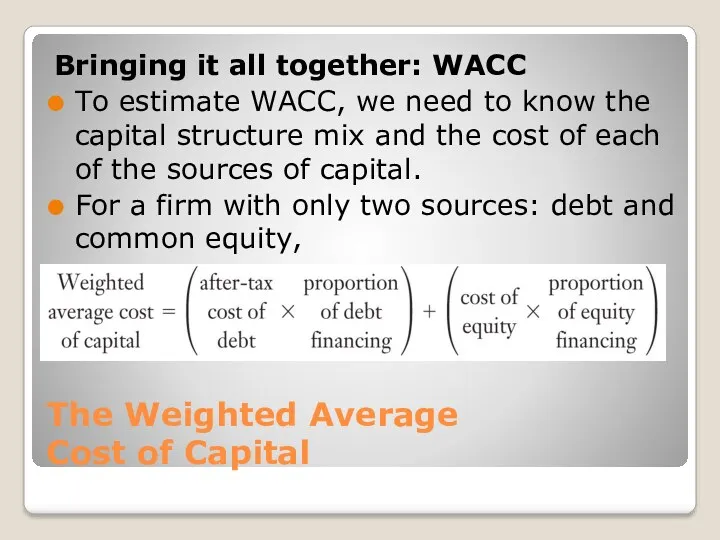

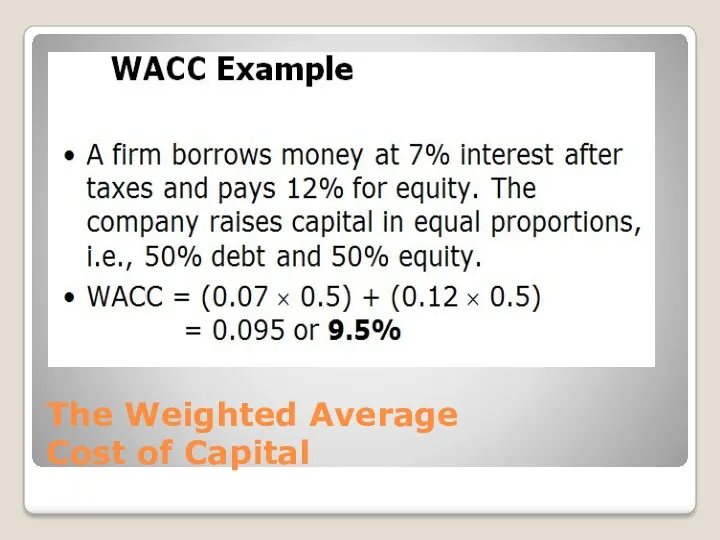

The Weighted Average

Cost of Capital

Bringing it all together: WACC

To estimate

The Weighted Average

Cost of Capital

Bringing it all together: WACC

To estimate

The Weighted Average

Cost of Capital

The Weighted Average

Cost of Capital

Business World Cost of capital

In practice, the calculation of cost of

Business World Cost of capital

In practice, the calculation of cost of

Divisional Costs of Capital

Firms with multiple operating divisions often have unique

Divisional Costs of Capital

Firms with multiple operating divisions often have unique

Advantages of Divisional WACC

Different discount rates reflect differences in the systematic

Advantages of Divisional WACC

Different discount rates reflect differences in the systematic

Using Pure Play Firms to Estimate Divisional WACCs

Divisional cost of capital

Using Pure Play Firms to Estimate Divisional WACCs

Divisional cost of capital

Divisional WACC Example

Table 9-4 contains hypothetical estimates of the divisional WACC

Divisional WACC Example

Table 9-4 contains hypothetical estimates of the divisional WACC

Divisional WACC – Estimation Issues and Limitations

Sample chosen may not be

Divisional WACC – Estimation Issues and Limitations

Sample chosen may not be

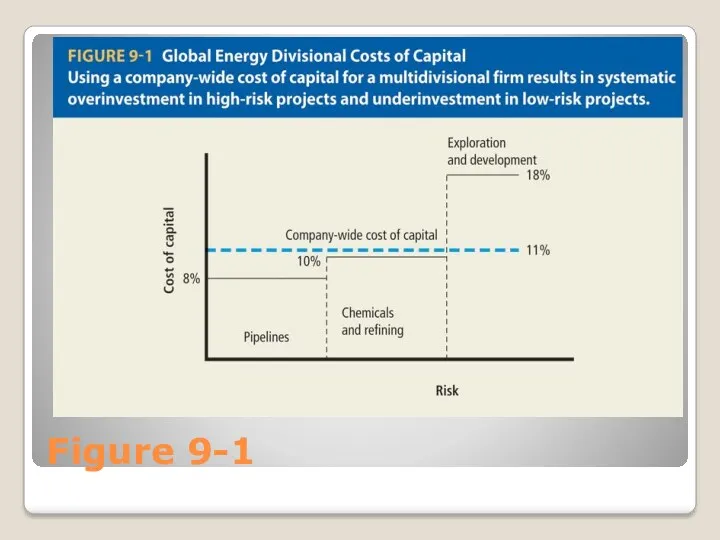

Cost of Capital to Evaluate

New Capital Investments

Cost of capital can

Cost of Capital to Evaluate

New Capital Investments

Cost of capital can

Figure 9-1

Figure 9-1

Capital Budgeting

Meaning: The process of decision making with respect to investments

Capital Budgeting

Meaning: The process of decision making with respect to investments

Capital-Budgeting Decision Criteria

The Payback Period

Net Present Value

Profitability Index

Internal Rate of Return

Capital-Budgeting Decision Criteria

The Payback Period

Net Present Value

Profitability Index

Internal Rate of Return

The Payback Period

Meaning: Number of years needed to recover the initial

The Payback Period

Meaning: Number of years needed to recover the initial

Payback Period Example

Payback Period Example

The Payback Period - Trade-Offs

Benefits:

Uses cash flows rather than accounting

The Payback Period - Trade-Offs

Benefits:

Uses cash flows rather than accounting

Discounted Payback Period

The discounted payback period is similar to the traditional

Discounted Payback Period

The discounted payback period is similar to the traditional

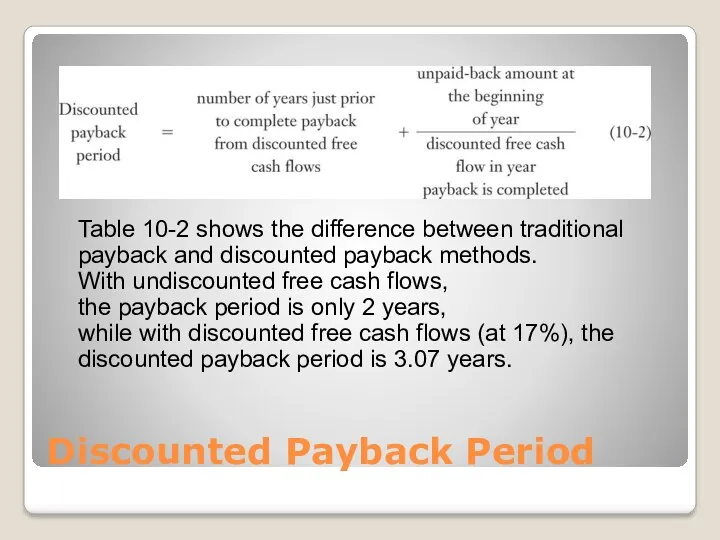

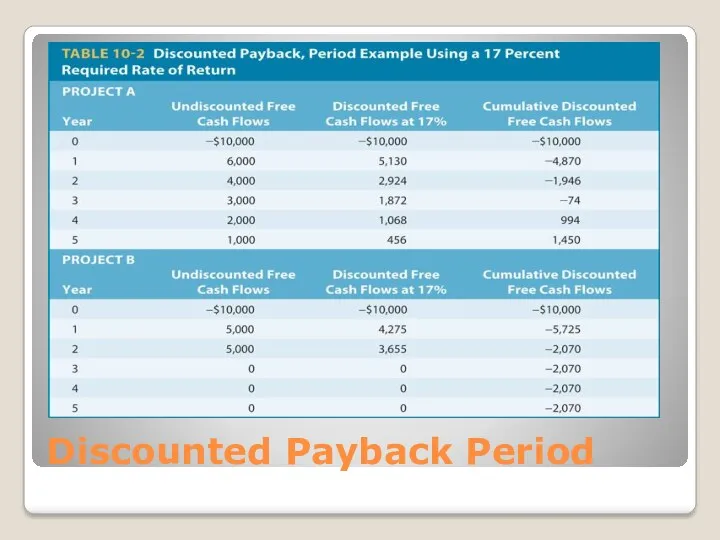

Discounted Payback Period

Table 10-2 shows the difference between traditional payback and

Discounted Payback Period

Table 10-2 shows the difference between traditional payback and

Discounted Payback Period

Discounted Payback Period

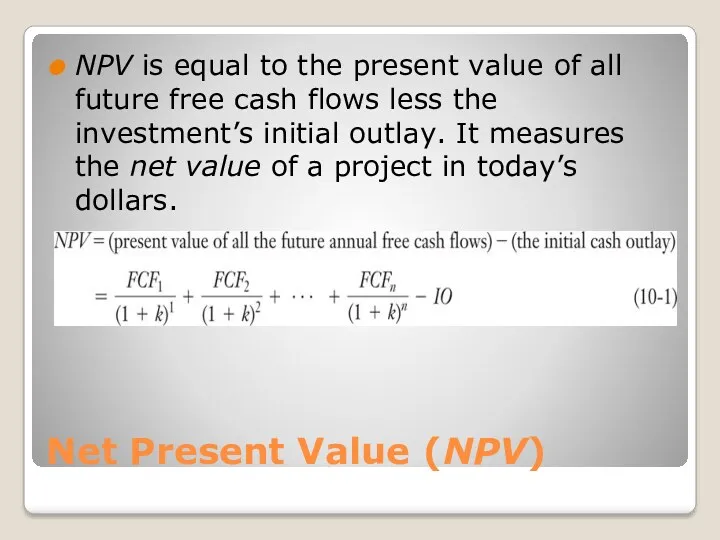

Net Present Value (NPV)

NPV is equal to the present value of

Net Present Value (NPV)

NPV is equal to the present value of

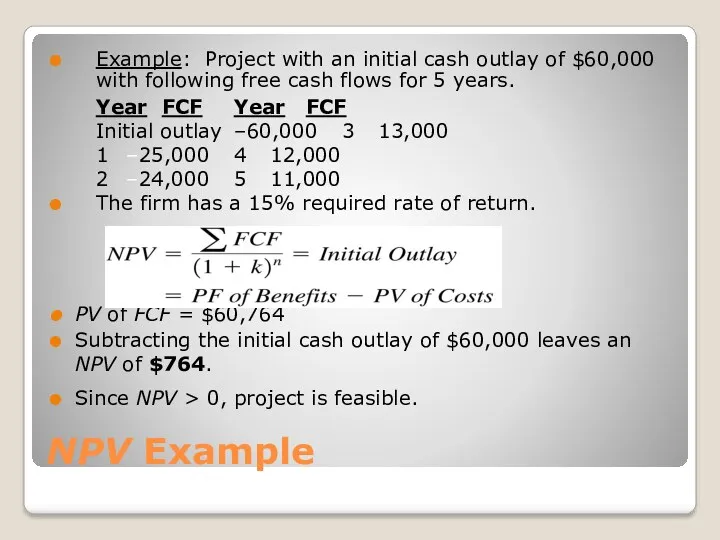

NPV Example

Example: Project with an initial cash outlay of $60,000 with

NPV Example

Example: Project with an initial cash outlay of $60,000 with

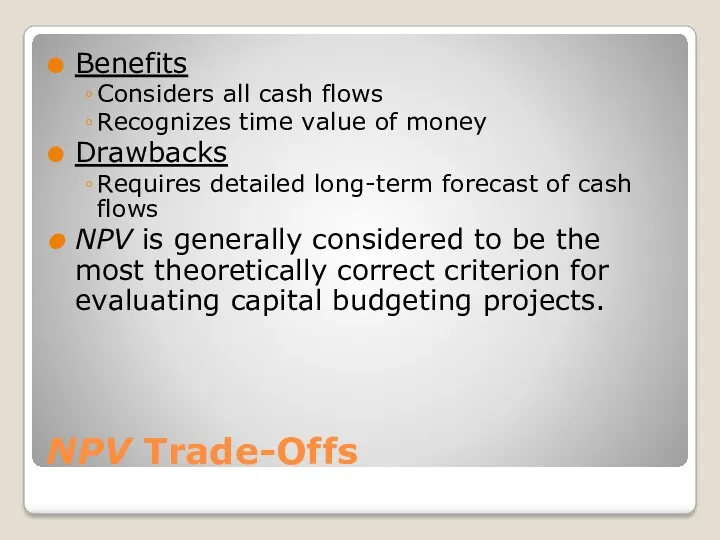

NPV Trade-Offs

Benefits

Considers all cash flows

Recognizes time value of money

Drawbacks

Requires detailed

NPV Trade-Offs

Benefits

Considers all cash flows

Recognizes time value of money

Drawbacks

Requires detailed

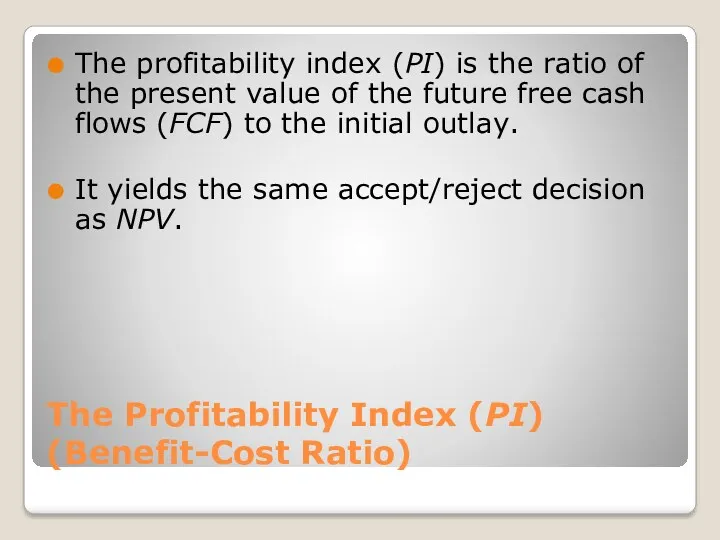

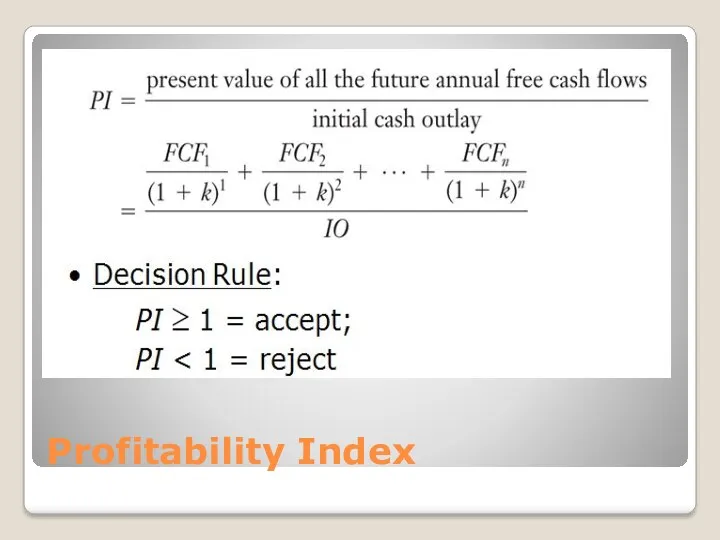

The Profitability Index (PI)

(Benefit-Cost Ratio)

The profitability index (PI) is the

The Profitability Index (PI)

(Benefit-Cost Ratio)

The profitability index (PI) is the

Profitability Index

Profitability Index

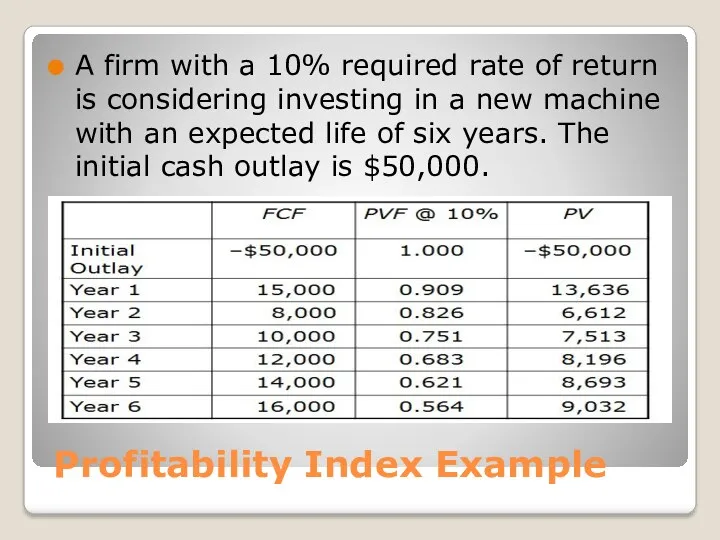

Profitability Index Example

A firm with a 10% required rate of return

Profitability Index Example

A firm with a 10% required rate of return

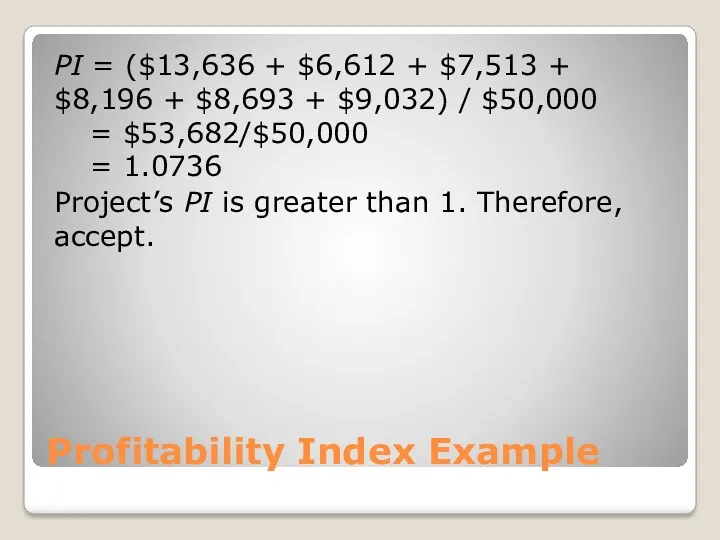

Profitability Index Example

PI = ($13,636 + $6,612 + $7,513 + $8,196

Profitability Index Example

PI = ($13,636 + $6,612 + $7,513 + $8,196

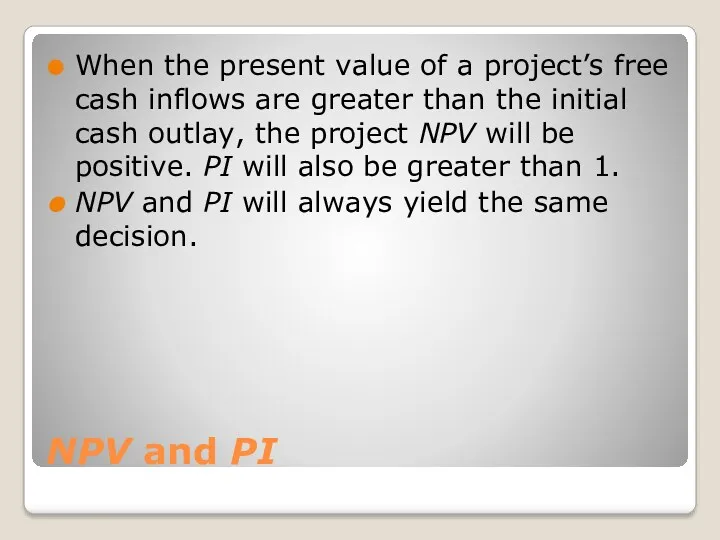

NPV and PI

When the present value of a project’s free cash

NPV and PI

When the present value of a project’s free cash

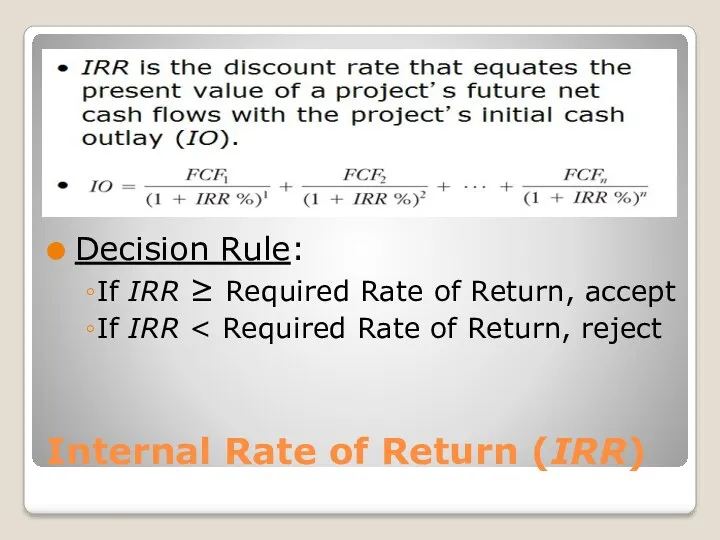

Internal Rate of Return (IRR)

Decision Rule:

If IRR ≥ Required Rate

Internal Rate of Return (IRR)

Decision Rule:

If IRR ≥ Required Rate

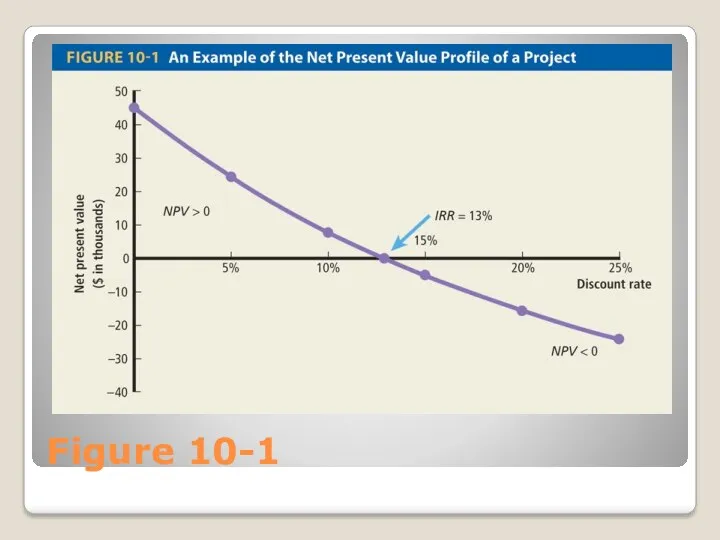

Figure 10-1

Figure 10-1

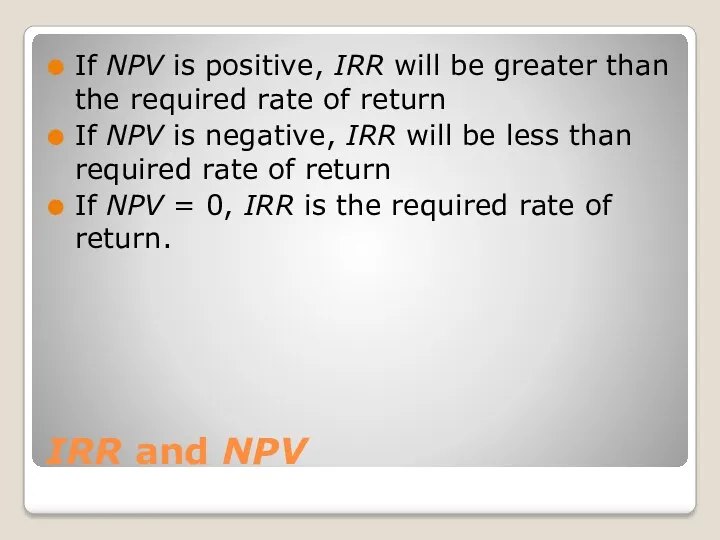

IRR and NPV

If NPV is positive, IRR will be greater than

IRR and NPV

If NPV is positive, IRR will be greater than

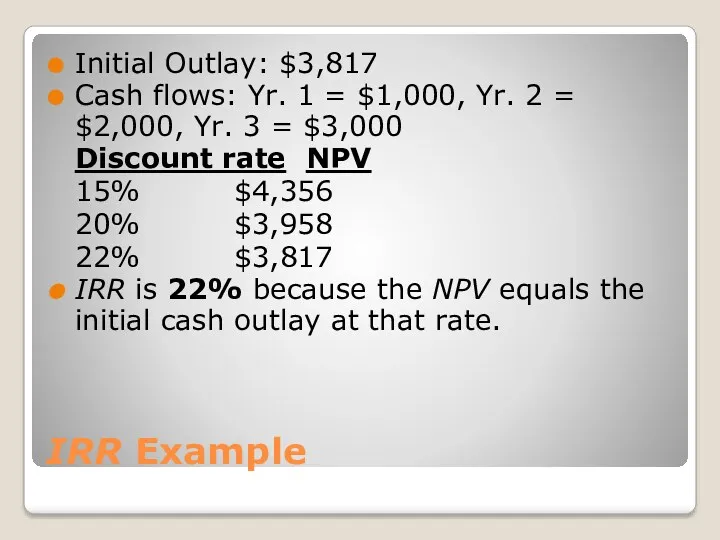

IRR Example

Initial Outlay: $3,817

Cash flows: Yr. 1 = $1,000, Yr. 2

IRR Example

Initial Outlay: $3,817

Cash flows: Yr. 1 = $1,000, Yr. 2

Guidelines for Capital Budgeting

To evaluate investment proposals, we must first set

Guidelines for Capital Budgeting

To evaluate investment proposals, we must first set

Guidelines for Capital Budgeting

Use Free Cash Flows Rather than Accounting Profits

Think

Guidelines for Capital Budgeting

Use Free Cash Flows Rather than Accounting Profits

Think

CALCULATING A PROJECT’S FREE CASH FLOWS

Three components of free cash flows:

The

CALCULATING A PROJECT’S FREE CASH FLOWS

Three components of free cash flows:

The

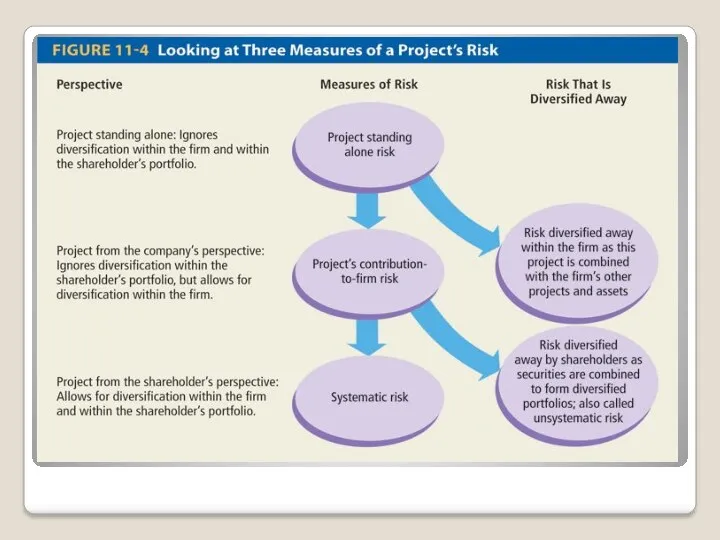

Three Perspectives on Risk

Project standing alone risk

Project’s contribution-to-firm risk

Systematic risk

Three Perspectives on Risk

Project standing alone risk

Project’s contribution-to-firm risk

Systematic risk

Project Standing Alone Risk

This is a project’s risk ignoring the fact

Project Standing Alone Risk

This is a project’s risk ignoring the fact

Contribution-to-Firm Risk

This is the amount of risk that the project contributes

Contribution-to-Firm Risk

This is the amount of risk that the project contributes

Systematic Risk

Risk of the project from the viewpoint of a well-diversified

Systematic Risk

Risk of the project from the viewpoint of a well-diversified

Relevant Risk

Theoretically, the only risk of concern to shareholders is systematic

Relevant Risk

Theoretically, the only risk of concern to shareholders is systematic

Incorporating Risk into

Capital Budgeting

Investors demand higher returns for more risky

Incorporating Risk into

Capital Budgeting

Investors demand higher returns for more risky

Risk

Risk is variability associated with expected revenue or income streams. Such

Risk

Risk is variability associated with expected revenue or income streams. Such

Business Risk

Business risk is the variation in the firm’s expected earnings

Business Risk

Business risk is the variation in the firm’s expected earnings

Operating Risk

Operating risk is the variation in the firm’s operating earnings

Operating Risk

Operating risk is the variation in the firm’s operating earnings

Financial Risk

Financial risk is the variation in earnings as a result

Financial Risk

Financial risk is the variation in earnings as a result

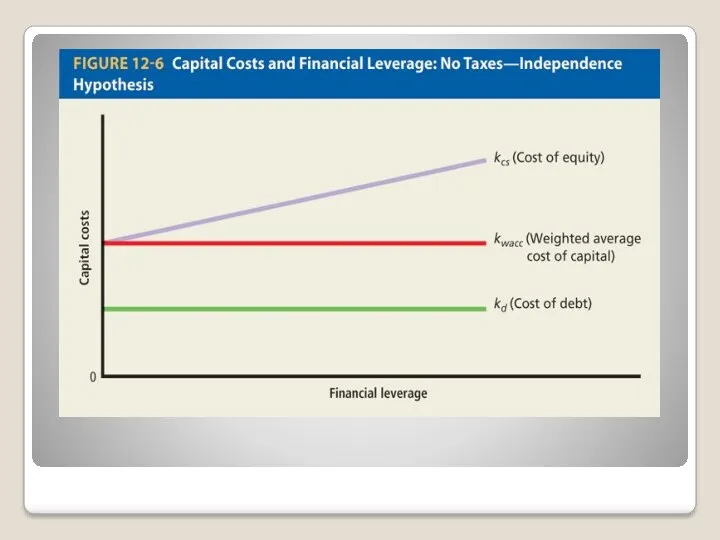

Capital Structure Theory

Theory focuses on the effect of financial leverage on

Capital Structure Theory

Theory focuses on the effect of financial leverage on

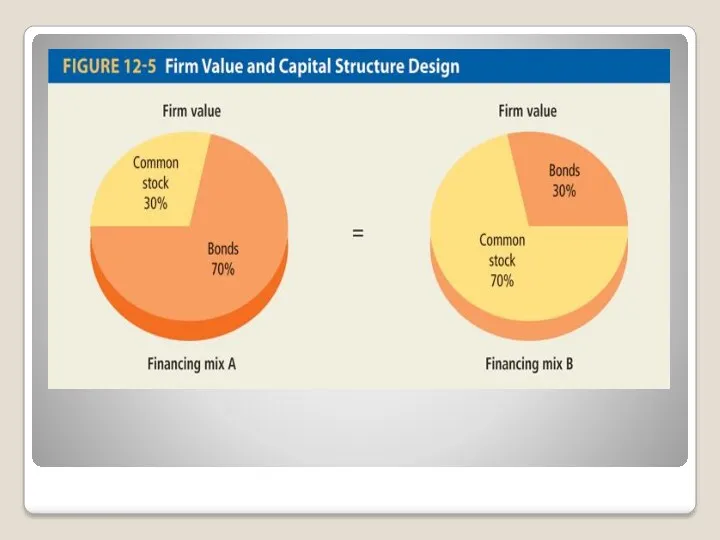

Capital Structure Theory

Figure 12-5 shows that the firm’s value remains the

Capital Structure Theory

Figure 12-5 shows that the firm’s value remains the

Capital Structure Theory

The implication of these figures for financial managers is

Capital Structure Theory

The implication of these figures for financial managers is

Extensions to Independence Hypothesis: The Moderate Position

The moderate position considers how

Extensions to Independence Hypothesis: The Moderate Position

The moderate position considers how

Impact of Taxes on Capital Structure

Interest expense is tax deductible.

Because interest

Impact of Taxes on Capital Structure

Interest expense is tax deductible.

Because interest

Impact of Taxes on Capital Structure

Since interest on debt is tax

Impact of Taxes on Capital Structure

Since interest on debt is tax

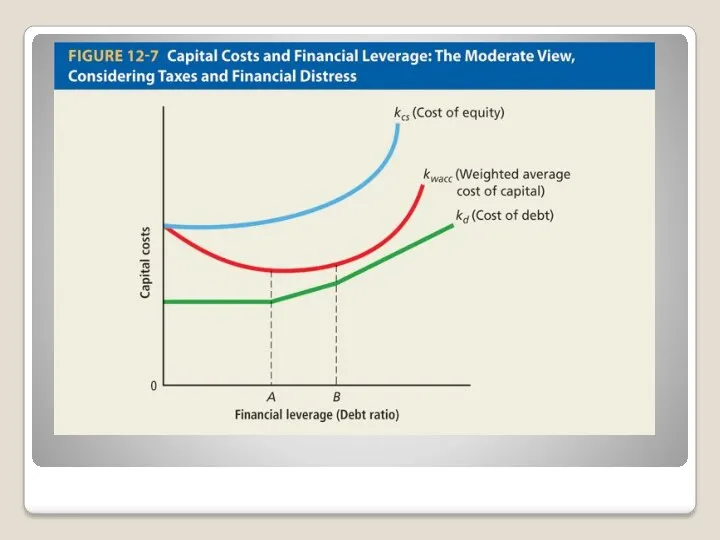

Impact of Bankruptcy on Capital Structure

The probability that a firm will

Impact of Bankruptcy on Capital Structure

The probability that a firm will

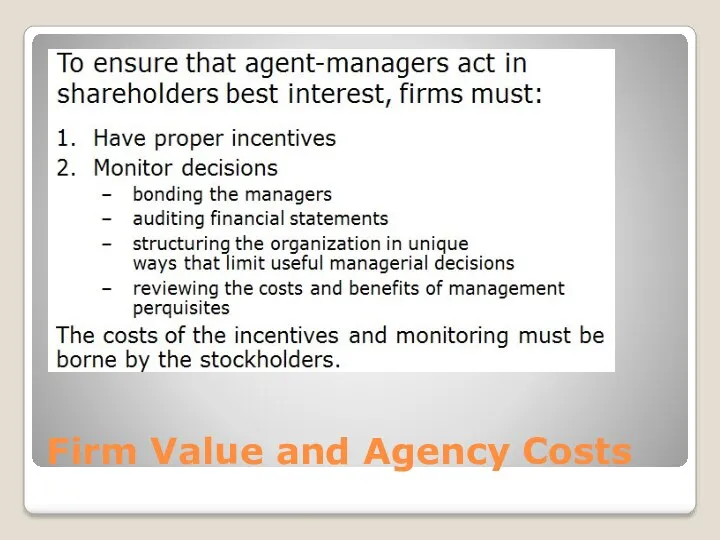

Firm Value and Agency Costs

Firm Value and Agency Costs

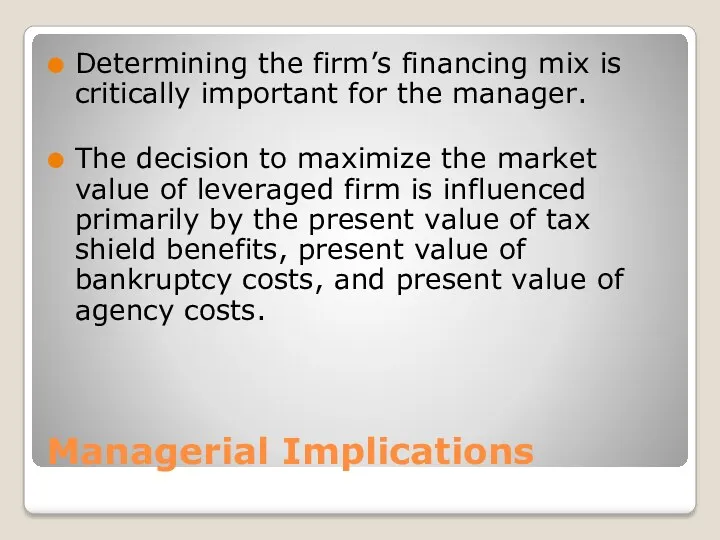

Managerial Implications

Determining the firm’s financing mix is critically important for the

Managerial Implications

Determining the firm’s financing mix is critically important for the

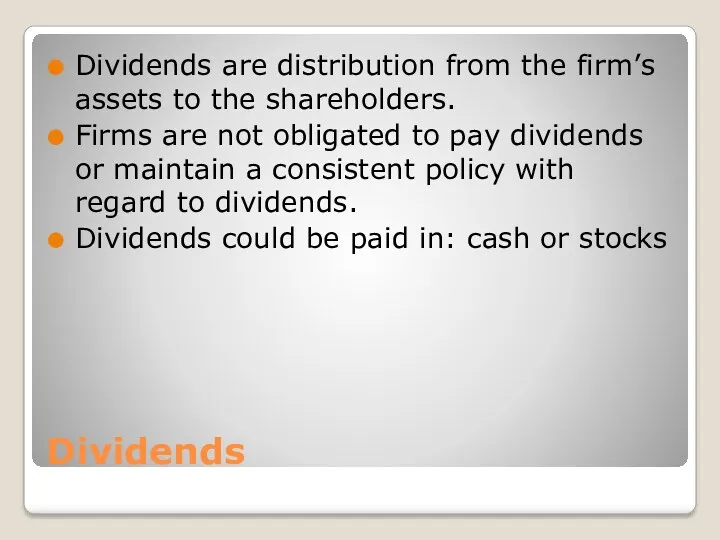

Dividends

Dividends are distribution from the firm’s assets to the shareholders.

Firms

Dividends

Dividends are distribution from the firm’s assets to the shareholders.

Firms

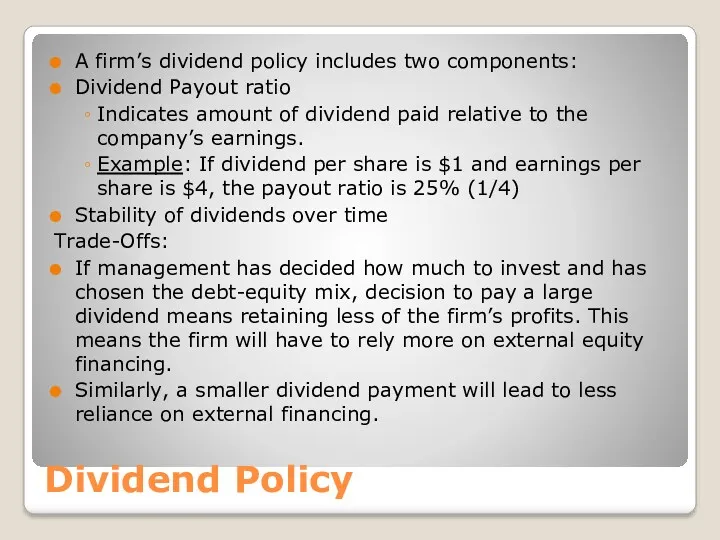

Dividend Policy

A firm’s dividend policy includes two components:

Dividend Payout ratio

Indicates amount

Dividend Policy

A firm’s dividend policy includes two components:

Dividend Payout ratio

Indicates amount

Dividend-versus-Retention Trade-Offs

Dividend-versus-Retention Trade-Offs

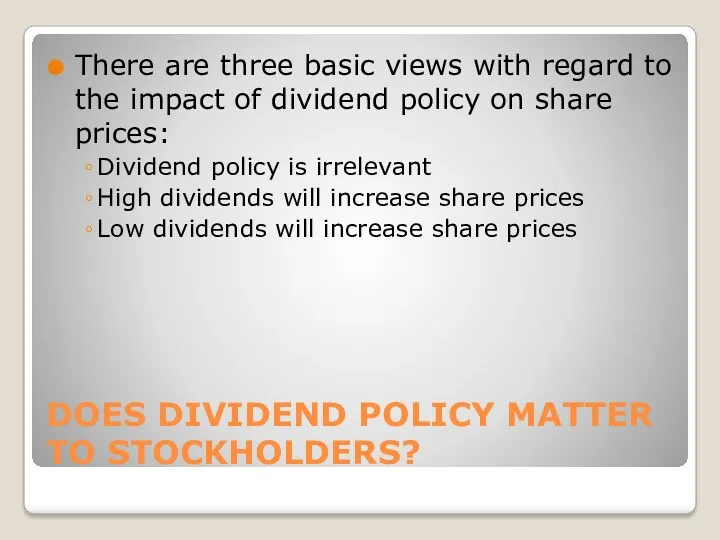

DOES DIVIDEND POLICY MATTER TO STOCKHOLDERS?

There are three basic views with

DOES DIVIDEND POLICY MATTER TO STOCKHOLDERS?

There are three basic views with

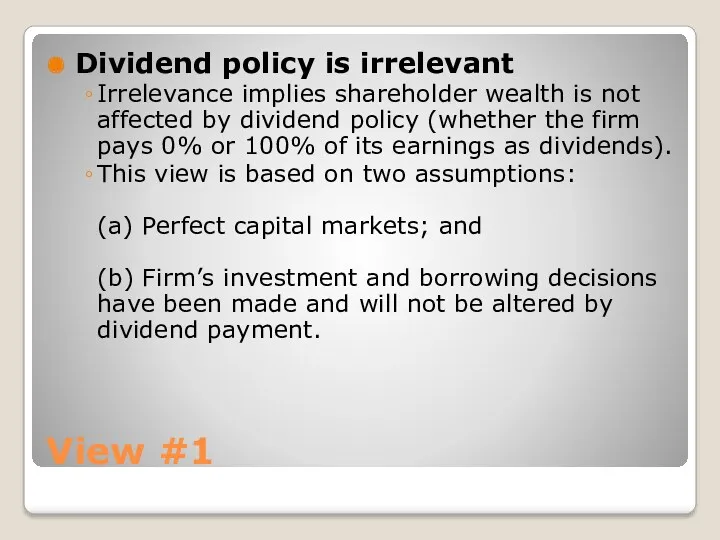

View #1

Dividend policy is irrelevant

Irrelevance implies shareholder wealth is not

View #1

Dividend policy is irrelevant

Irrelevance implies shareholder wealth is not

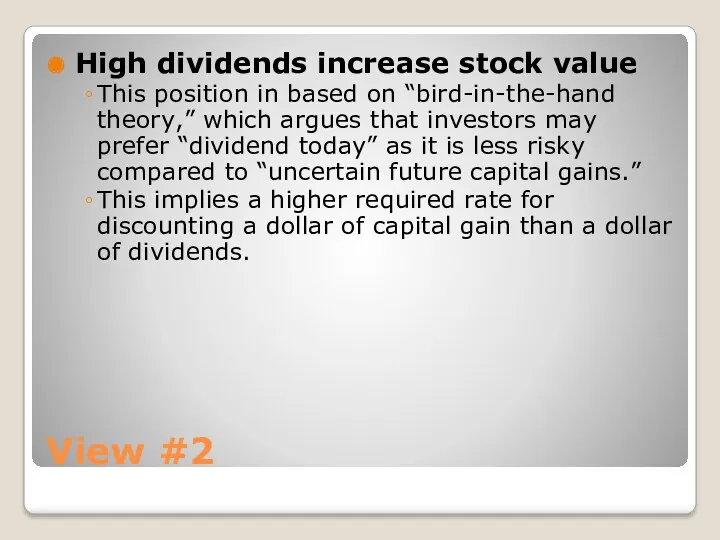

View #2

High dividends increase stock value

This position in based on “bird-in-the-hand

View #2

High dividends increase stock value

This position in based on “bird-in-the-hand

View #3

Low dividend increases stock values

In 2003, the tax rates

View #3

Low dividend increases stock values

In 2003, the tax rates

Some Other Explanations

The Residual Dividend Theory

Clientele Effect

The Information Effect

Agency Costs

The Expectations

Some Other Explanations

The Residual Dividend Theory

Clientele Effect

The Information Effect

Agency Costs

The Expectations

Residual Dividend Theory

Determine the optimal capital budget

Determine the amount of equity

Residual Dividend Theory

Determine the optimal capital budget

Determine the amount of equity

The Clientele Effect

Different groups of investors have varying preferences towards dividends.

For

The Clientele Effect

Different groups of investors have varying preferences towards dividends.

For

The Information Effect

Evidence shows that large, unexpected change in dividends can

The Information Effect

Evidence shows that large, unexpected change in dividends can

Agency Costs

Dividend policy may be perceived as a tool to minimize

Agency Costs

Dividend policy may be perceived as a tool to minimize

The Expectations Theory

Expectation theory suggests that the market reaction does not

The Expectations Theory

Expectation theory suggests that the market reaction does not

Conclusions on Dividend Policy

Here are some conclusions about the relevance of

Conclusions on Dividend Policy

Here are some conclusions about the relevance of

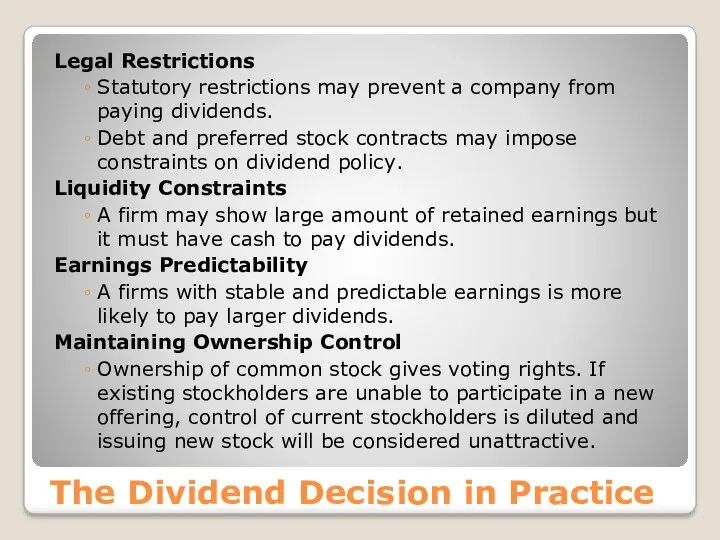

The Dividend Decision in Practice

Legal Restrictions

Statutory restrictions may prevent a company

The Dividend Decision in Practice

Legal Restrictions

Statutory restrictions may prevent a company

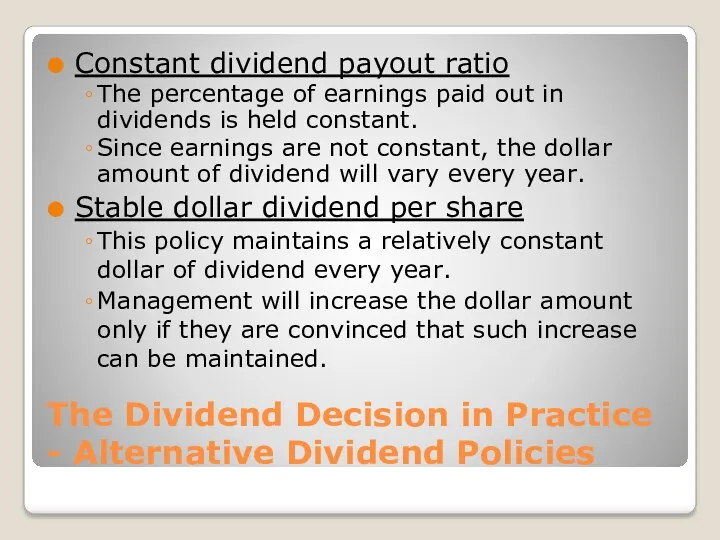

The Dividend Decision in Practice - Alternative Dividend Policies

Constant dividend payout

The Dividend Decision in Practice - Alternative Dividend Policies

Constant dividend payout

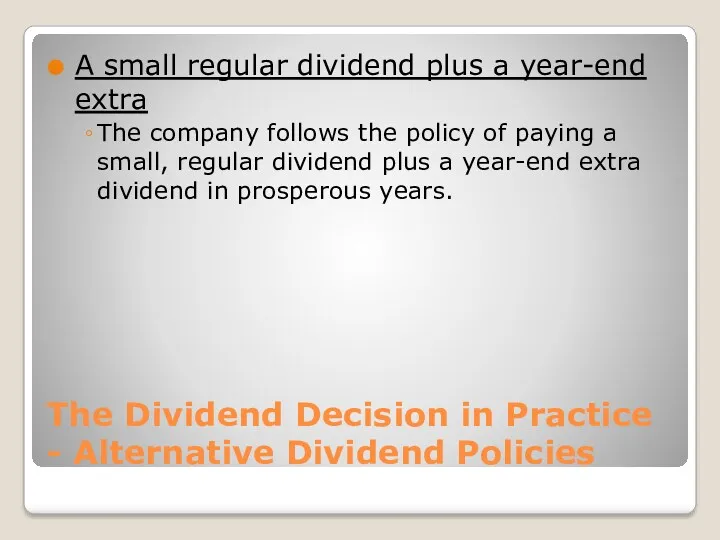

The Dividend Decision in Practice - Alternative Dividend Policies

A small regular

The Dividend Decision in Practice - Alternative Dividend Policies

A small regular

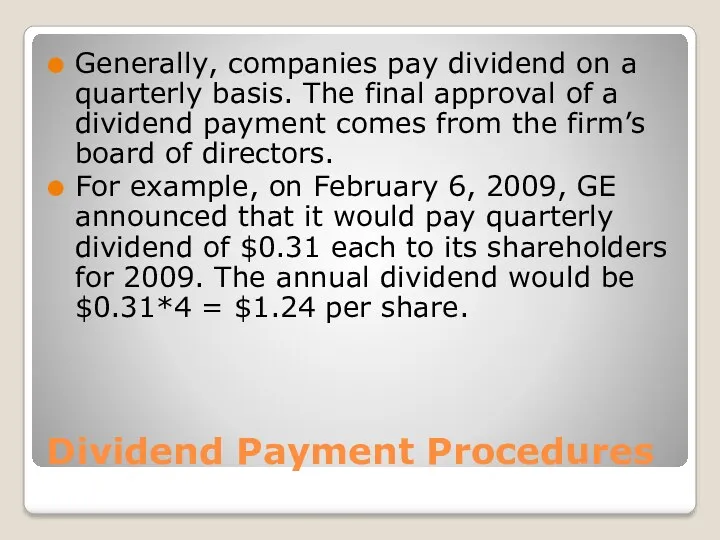

Dividend Payment Procedures

Generally, companies pay dividend on a quarterly basis. The

Dividend Payment Procedures

Generally, companies pay dividend on a quarterly basis. The

Important Dates

Declaration date – The date when the dividend is formally

Important Dates

Declaration date – The date when the dividend is formally

Stock Dividends

A stock dividend entails the distribution of additional shares of

Stock Dividends

A stock dividend entails the distribution of additional shares of

Stock Splits

A stock split involves exchanging more (or less in the

Stock Splits

A stock split involves exchanging more (or less in the

Stock Repurchases

A stock repurchase (stock buyback) occurs when a firm repurchases

Stock Repurchases

A stock repurchase (stock buyback) occurs when a firm repurchases

Stock Repurchase -- Benefits

A means of providing an internal investment opportunity

An

Stock Repurchase -- Benefits

A means of providing an internal investment opportunity

An

A Share Repurchase as a Dividend, Financing, Investment Decision

When a firm

A Share Repurchase as a Dividend, Financing, Investment Decision

When a firm

Unsecured Sources:

Trade Credit

Trade credit arises spontaneously with the firm’s purchases. Often,

Unsecured Sources:

Trade Credit

Trade credit arises spontaneously with the firm’s purchases. Often,

Effective Cost of Passing

Up a Discount

Ex.: Terms 2/10 net 30

The

Effective Cost of Passing

Up a Discount

Ex.: Terms 2/10 net 30

The

Unsecured Sources:

Bank Credit

Commercial banks provide unsecured short-term credit in two

Unsecured Sources:

Bank Credit

Commercial banks provide unsecured short-term credit in two

Line of Credit

Informal agreement between a borrower and a bank about

Line of Credit

Informal agreement between a borrower and a bank about

Revolving Credit

Revolving credit is a variant of the line of credit

Revolving Credit

Revolving credit is a variant of the line of credit

Transaction Loans

A transaction loan is made for a specific purpose. This

Transaction Loans

A transaction loan is made for a specific purpose. This

Unsecured Sources:

Commercial Paper

The largest and most credit-worthy companies are able

Unsecured Sources:

Commercial Paper

The largest and most credit-worthy companies are able

Commercial Paper: Advantages

Interest rates

Rates are generally lower than rates on bank

Commercial Paper: Advantages

Interest rates

Rates are generally lower than rates on bank

Secured Sources of Loans

Secured loans have assets of the firm pledged

Secured Sources of Loans

Secured loans have assets of the firm pledged

Pledging Accounts Receivable

Borrower pledges accounts receivable as collateral for a loan

Pledging Accounts Receivable

Borrower pledges accounts receivable as collateral for a loan

Pledging Accounts Receivable

Credit Terms: Interest rate is 2–5% higher than the

Pledging Accounts Receivable

Credit Terms: Interest rate is 2–5% higher than the

Pledging Accounts Receivable

Factoring accounts receivable involves the outright sale of a

Pledging Accounts Receivable

Factoring accounts receivable involves the outright sale of a

Secured Sources:

Inventory Loans

These are loans secured by inventories.

The amount of

Secured Sources:

Inventory Loans

These are loans secured by inventories.

The amount of

Types of Inventory Loans

Floating or Blanket Lien Agreement

The borrower gives the

Types of Inventory Loans

Floating or Blanket Lien Agreement

The borrower gives the

Working Capital

Working capital - The firm’s total investment in current assets.

Net

Working Capital

Working capital - The firm’s total investment in current assets.

Net

Managing Net Working Capital

Managing net working capital is concerned with managing

Managing Net Working Capital

Managing net working capital is concerned with managing

How Much Short-Term Financing Should a Firm Use?

This question is addressed

How Much Short-Term Financing Should a Firm Use?

This question is addressed

The Appropriate Level of Working Capital

Managing working capital involves interrelated decisions

The Appropriate Level of Working Capital

Managing working capital involves interrelated decisions

The Hedging Principle

The hedging principle involves matching the cash-flow-generating characteristics of

The Hedging Principle

The hedging principle involves matching the cash-flow-generating characteristics of

Permanent and Temporary Assets

Permanent investments

Investments that the firm expects to

Permanent and Temporary Assets

Permanent investments

Investments that the firm expects to

Temporary and Permanent Sources of Financing

Temporary sources of financing consist of

Temporary and Permanent Sources of Financing

Temporary sources of financing consist of

The Cash Conversion Cycle

A firm can minimize its working capital by

The Cash Conversion Cycle

A firm can minimize its working capital by

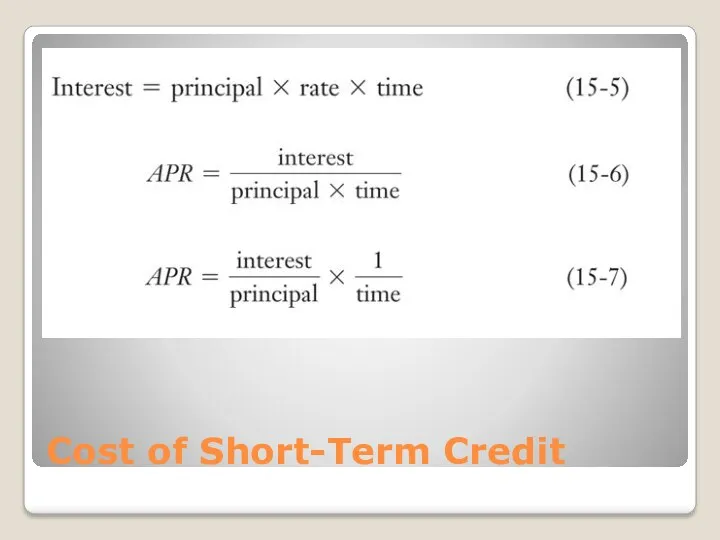

Cost of Short-Term Credit

Cost of Short-Term Credit

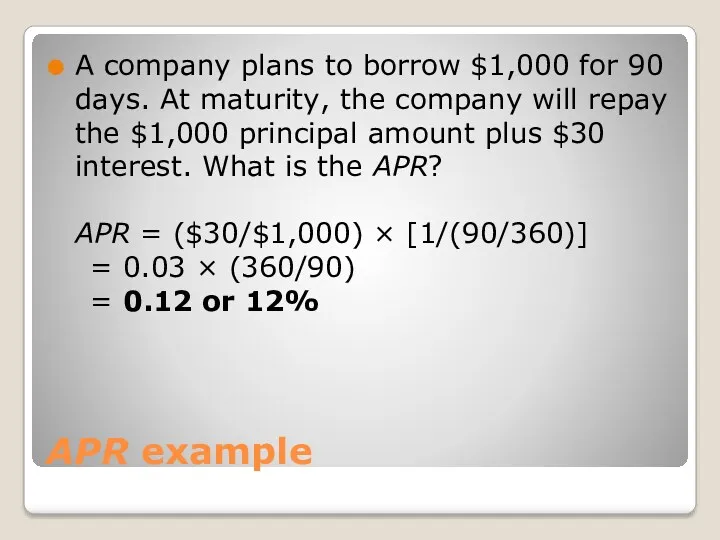

APR example

A company plans to borrow $1,000 for 90 days. At

APR example

A company plans to borrow $1,000 for 90 days. At

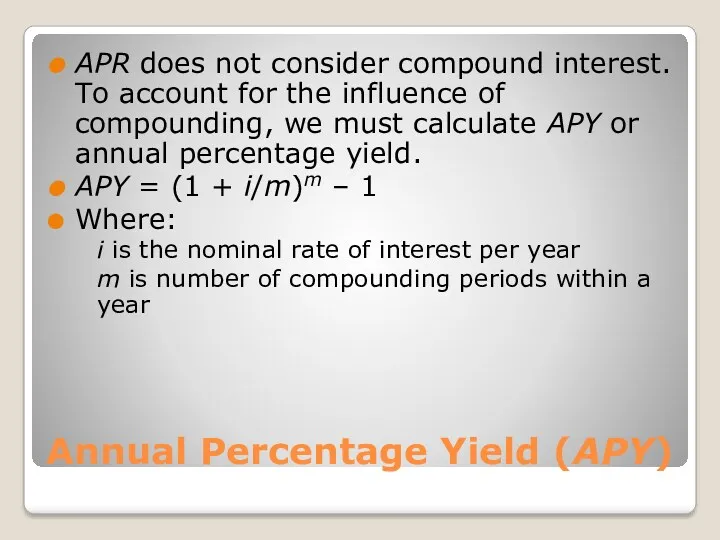

Annual Percentage Yield (APY)

APR does not consider compound interest. To account

Annual Percentage Yield (APY)

APR does not consider compound interest. To account

APY example

In the previous example,

# of compounding periods 360/90 = 4

Rate

APY example

In the previous example,

# of compounding periods 360/90 = 4

Rate

Учет продажи товаров

Учет продажи товаров Конкурс рисунка Финансовый мир глазами детей

Конкурс рисунка Финансовый мир глазами детей Страноведческие образы в бонистике

Страноведческие образы в бонистике Макроэкономическое равновесие на денежном рынке. Спрос на деньги

Макроэкономическое равновесие на денежном рынке. Спрос на деньги Банковское дело

Банковское дело Көлік салығы

Көлік салығы МСФО 7. Отчеты о движении денежных средств

МСФО 7. Отчеты о движении денежных средств Розрахунки прибутку та рентабельностi

Розрахунки прибутку та рентабельностi Учет и анализ основных средств на предприятии (на примере ООО Электросетьмонтаж)

Учет и анализ основных средств на предприятии (на примере ООО Электросетьмонтаж) Анализ платежеспособности и финансовой устойчивости предприятия и пути их повышения

Анализ платежеспособности и финансовой устойчивости предприятия и пути их повышения Жилищное ипотечное кредитование в России: состояние и перспективы развития

Жилищное ипотечное кредитование в России: состояние и перспективы развития Матеріально-технічне забезпечення інвестиційного проекту

Матеріально-технічне забезпечення інвестиційного проекту Організація обліку розрахунків за виплатами працівникам

Організація обліку розрахунків за виплатами працівникам Учет амортизации и методы ее начисления

Учет амортизации и методы ее начисления Экспресс страхование квартир в СПАО Ингосстрах

Экспресс страхование квартир в СПАО Ингосстрах Корпорация капиталының құны мен құрылымы

Корпорация капиталының құны мен құрылымы Анализ финансового состояния

Анализ финансового состояния The financial market environment. (Chapter 2)

The financial market environment. (Chapter 2) Жилищный кооператив Best Way

Жилищный кооператив Best Way Кредиты и займы

Кредиты и займы Бюджетный процесс в Российской Федерации

Бюджетный процесс в Российской Федерации Применения новых ФСБУ при аудите бухгалтерской отчетности

Применения новых ФСБУ при аудите бухгалтерской отчетности Розпорядники бюджетних коштів, їх функції та роль у виконанні бюджетних програм

Розпорядники бюджетних коштів, їх функції та роль у виконанні бюджетних програм Прямые инвестиции и международное сотрудничество

Прямые инвестиции и международное сотрудничество Микрогранты. Грантовая и экспертная служба

Микрогранты. Грантовая и экспертная служба Risk and Return

Risk and Return Бюджет для граждан на основе решения Собрания депутатов МО Котлас

Бюджет для граждан на основе решения Собрания депутатов МО Котлас Формирование учетной политики организации и оценка ее влияния на показатели деятельности организации

Формирование учетной политики организации и оценка ее влияния на показатели деятельности организации