- The role of managerial finance. (Chapter 1)

Содержание

- 2. Learning Goals LG1 Define finance and the managerial finance function. LG2 Describe the legal forms of

- 3. Learning Goals (cont.) LG4 Describe how the managerial finance function is related to economics and accounting.

- 4. What is Finance? Finance can be defined as the science and art of managing money. At

- 5. Career Opportunities in Finance: Financial Services Financial Services is the area of finance concerned with the

- 6. Career Opportunities in Finance: Managerial Finance Managerial finance is concerned with the duties of the financial

- 7. Career Opportunities in Finance: Managerial Finance (cont.) The recent global financial crisis and subsequent responses by

- 8. Focus on Practice Professional Certifications in Finance: Chartered Financial Analyst (CFA) – Offered by the CFA

- 9. Focus on Practice (cont.) Professional Certifications in Finance: American Academy of Financial Management (AAFM) – The

- 10. Legal Forms of Business Organization A sole proprietorship is a business owned by one person and

- 11. Table 1.1 Strengths and Weaknesses of the Common Legal Forms of Business Organization

- 12. Matter of Fact

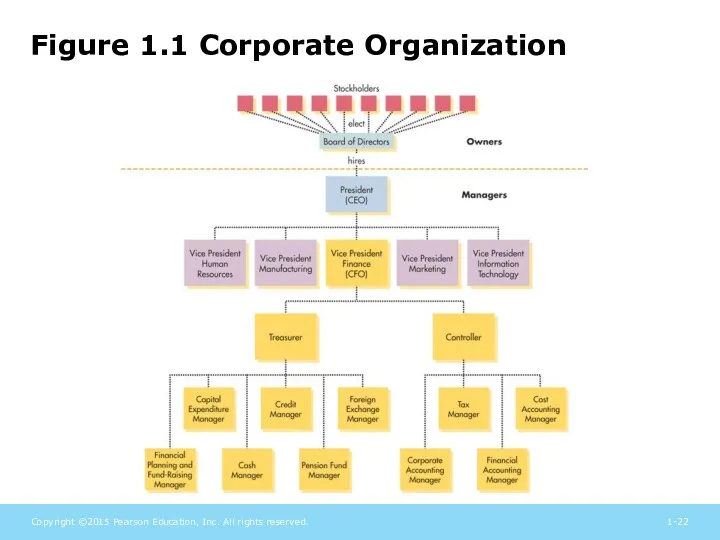

- 13. Figure 1.1 Corporate Organization

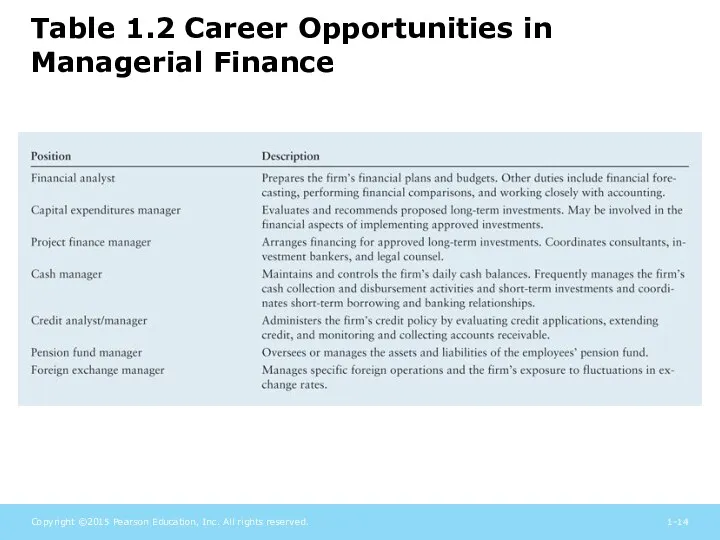

- 14. Table 1.2 Career Opportunities in Managerial Finance

- 15. Goal of the Firm: Maximize Shareholder Wealth Decision rule for managers: only take actions that are

- 16. Goal of the Firm: Maximize Profit? Profit maximization may not lead to the highest possible share

- 17. Goal of the Firm: What About Stakeholders? Stakeholders are groups such as employees, customers, suppliers, creditors,

- 18. The Role of Business Ethics Business ethics are the standards of conduct or moral judgment that

- 19. The Role of Business Ethics: Considering Ethics Robert A. Cooke, a noted ethicist, suggests that the

- 20. The Role of Business Ethics: Ethics and Share Price Ethics programs seek to: reduce litigation and

- 21. Managerial Finance Function The size and importance of the managerial finance function depends on the size

- 22. Figure 1.1 Corporate Organization

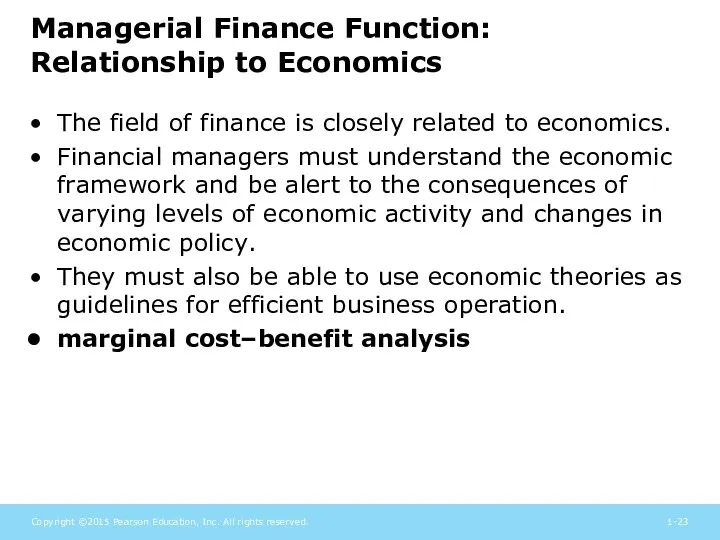

- 23. Managerial Finance Function: Relationship to Economics The field of finance is closely related to economics. Financial

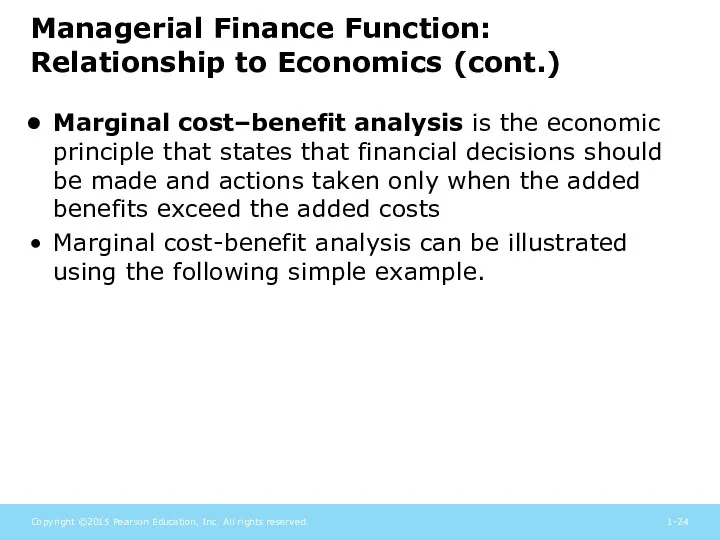

- 24. Managerial Finance Function: Relationship to Economics (cont.) Marginal cost–benefit analysis is the economic principle that states

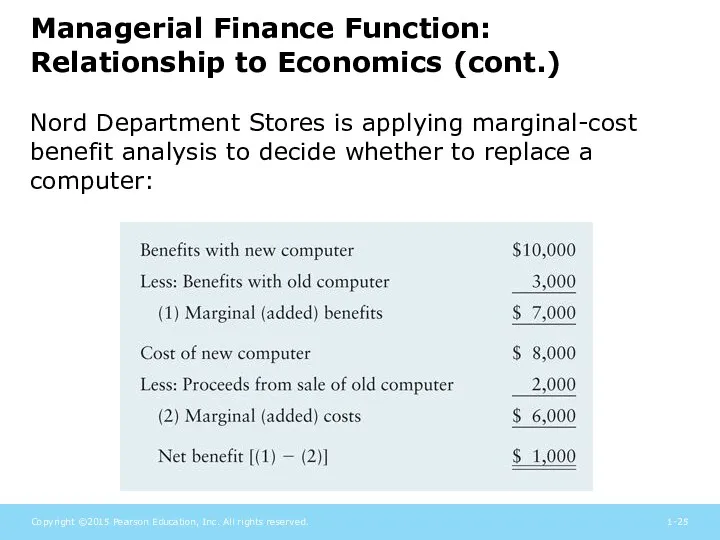

- 25. Managerial Finance Function: Relationship to Economics (cont.) Nord Department Stores is applying marginal-cost benefit analysis to

- 26. Managerial Finance Function: Relationship to Accounting The firm’s finance and accounting activities are closely-related and generally

- 27. Managerial Finance Function: Relationship to Accounting (cont.) Whether a firm earns a profit or experiences a

- 28. Managerial Finance Function: Relationship to Accounting (cont.) The Nassau Corporation experienced the following activity last year:

- 29. Managerial Finance Function: Relationship to Accounting (cont.) Now contrast the differences in performance under the accounting

- 30. Managerial Finance Function: Relationship to Accounting (cont.) Finance and accounting also differ with respect to decision-making:

- 31. Figure 1.3 Financial Activities

- 32. Governance and Agency: Corporate Governance Corporate governance refers to the rules, processes, and laws by which

- 33. Governance and Agency: Individual versus Institutional Investors Individual investors are investors who own relatively small quantities

- 34. Governance and Agency: Government Regulation Government regulation generally shapes the corporate governance of all firms. During

- 35. Governance and Agency: Government Regulation The Sarbanes-Oxley Act of 2002: established an oversight board to monitor

- 36. Governance and Agency: The Agency Issue A principal-agent relationship is an arrangement in which an agent

- 37. The Agency Issue: Management Compensation Plans In addition to the roles played by corporate boards, institutional

- 38. The Agency Issue: Management Compensation Plans Incentive plans are management compensation plans that tie management compensation

- 39. Matter of Fact—Forbes.com CEO Performance vs. Pay

- 41. Скачать презентацию

Learning Goals

LG1 Define finance and the managerial finance function.

LG2 Describe the

Learning Goals

LG1 Define finance and the managerial finance function.

LG2 Describe the

Learning Goals (cont.)

LG4 Describe how the managerial finance function is related

Learning Goals (cont.)

LG4 Describe how the managerial finance function is related

What is Finance?

Finance can be defined as the science and art

What is Finance?

Finance can be defined as the science and art

Career Opportunities in Finance: Financial Services

Financial Services is the area of

Career Opportunities in Finance: Financial Services

Financial Services is the area of

Career Opportunities in Finance: Managerial Finance

Managerial finance is concerned with the

Career Opportunities in Finance: Managerial Finance

Managerial finance is concerned with the

Career Opportunities in Finance: Managerial Finance (cont.)

The recent global financial crisis

Career Opportunities in Finance: Managerial Finance (cont.)

The recent global financial crisis

Focus on Practice

Professional Certifications in Finance:

Chartered Financial Analyst (CFA) – Offered

Focus on Practice

Professional Certifications in Finance:

Chartered Financial Analyst (CFA) – Offered

Focus on Practice (cont.)

Professional Certifications in Finance:

American Academy of Financial Management

Focus on Practice (cont.)

Professional Certifications in Finance:

American Academy of Financial Management

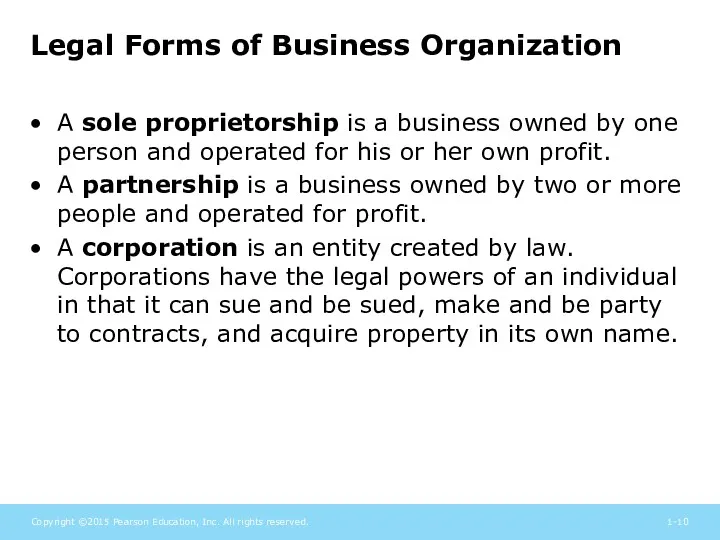

Legal Forms of Business Organization

A sole proprietorship is a business owned

Legal Forms of Business Organization

A sole proprietorship is a business owned

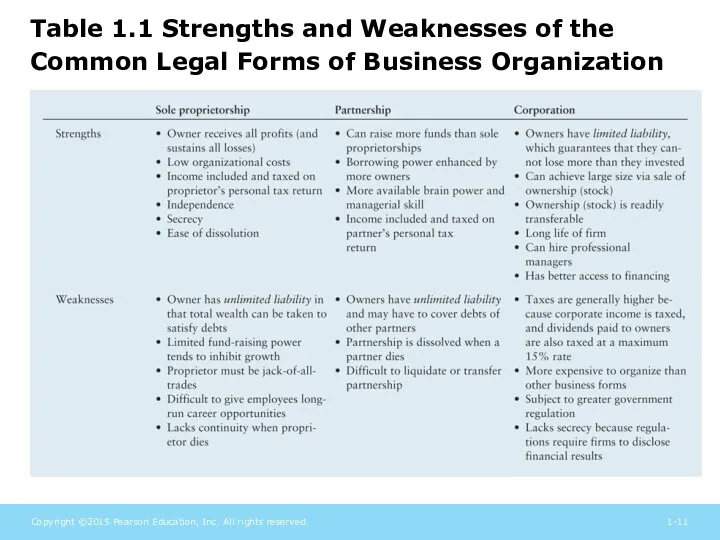

Table 1.1 Strengths and Weaknesses of the Common Legal Forms of

Table 1.1 Strengths and Weaknesses of the Common Legal Forms of

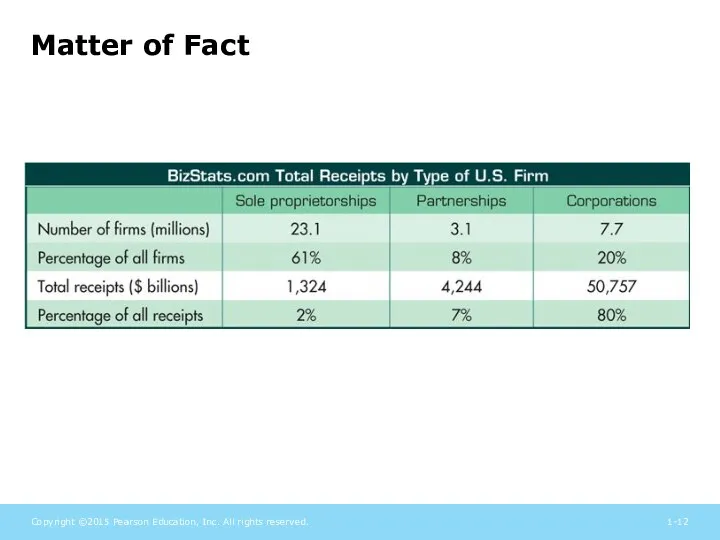

Matter of Fact

Matter of Fact

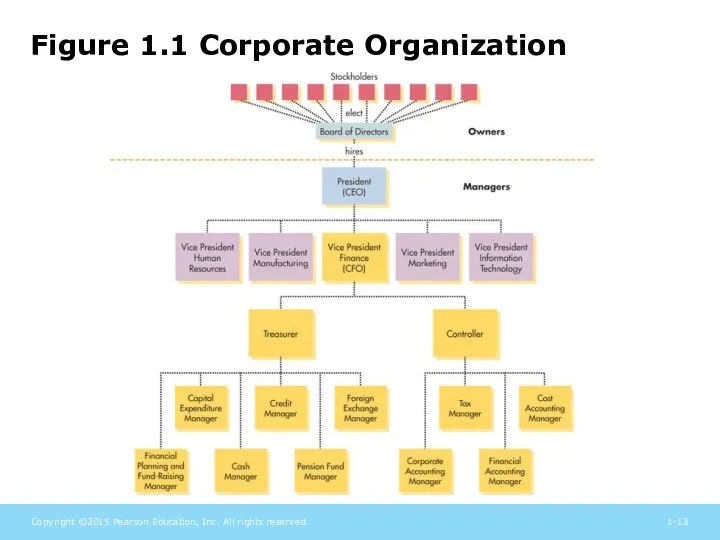

Figure 1.1 Corporate Organization

Figure 1.1 Corporate Organization

Table 1.2 Career Opportunities in Managerial Finance

Table 1.2 Career Opportunities in Managerial Finance

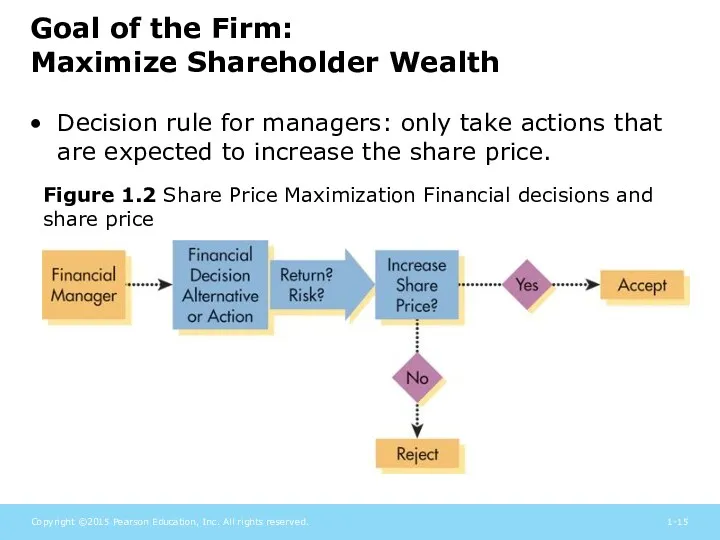

Goal of the Firm:

Maximize Shareholder Wealth

Decision rule for managers: only

Goal of the Firm:

Maximize Shareholder Wealth

Decision rule for managers: only

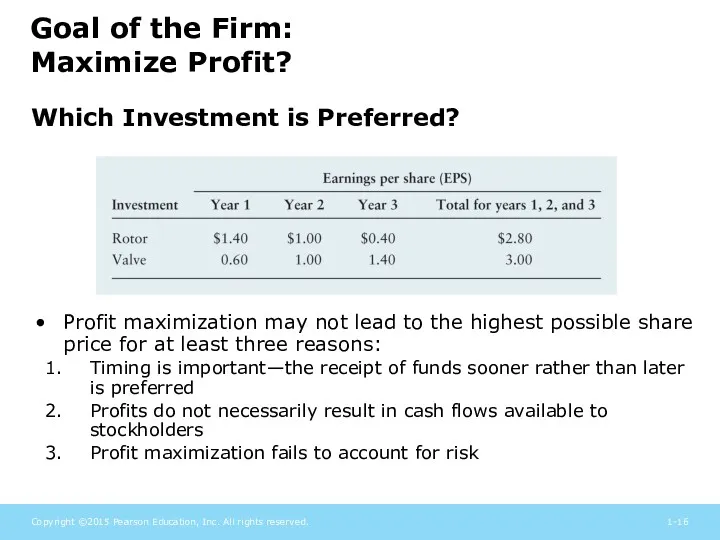

Goal of the Firm:

Maximize Profit?

Profit maximization may not lead to

Goal of the Firm:

Maximize Profit?

Profit maximization may not lead to

Goal of the Firm:

What About Stakeholders?

Stakeholders are groups such as

Goal of the Firm:

What About Stakeholders?

Stakeholders are groups such as

The Role of Business Ethics

Business ethics are the standards of conduct

The Role of Business Ethics

Business ethics are the standards of conduct

The Role of Business Ethics: Considering Ethics

Robert A. Cooke, a noted

The Role of Business Ethics: Considering Ethics

Robert A. Cooke, a noted

The Role of Business Ethics:

Ethics and Share Price

Ethics programs seek

The Role of Business Ethics:

Ethics and Share Price

Ethics programs seek

Managerial Finance Function

The size and importance of the managerial finance function

Managerial Finance Function

The size and importance of the managerial finance function

Figure 1.1 Corporate Organization

Figure 1.1 Corporate Organization

Managerial Finance Function: Relationship to Economics

The field of finance is closely

Managerial Finance Function: Relationship to Economics

The field of finance is closely

Managerial Finance Function: Relationship to Economics (cont.)

Marginal cost–benefit analysis is the

Managerial Finance Function: Relationship to Economics (cont.)

Marginal cost–benefit analysis is the

Managerial Finance Function: Relationship to Economics (cont.)

Nord Department Stores is applying

Managerial Finance Function: Relationship to Economics (cont.)

Nord Department Stores is applying

Managerial Finance Function: Relationship to Accounting

The firm’s finance and accounting activities

Managerial Finance Function: Relationship to Accounting

The firm’s finance and accounting activities

Managerial Finance Function: Relationship to Accounting (cont.)

Whether a firm earns a

Managerial Finance Function: Relationship to Accounting (cont.)

Whether a firm earns a

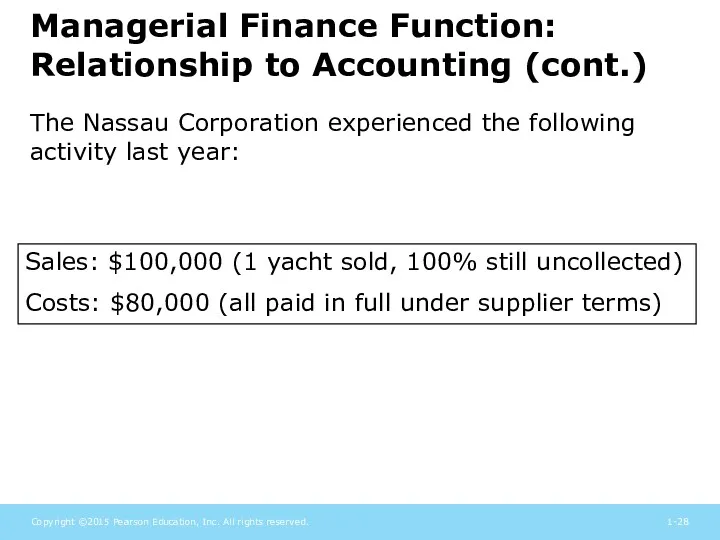

Managerial Finance Function: Relationship to Accounting (cont.)

The Nassau Corporation experienced the

Managerial Finance Function: Relationship to Accounting (cont.)

The Nassau Corporation experienced the

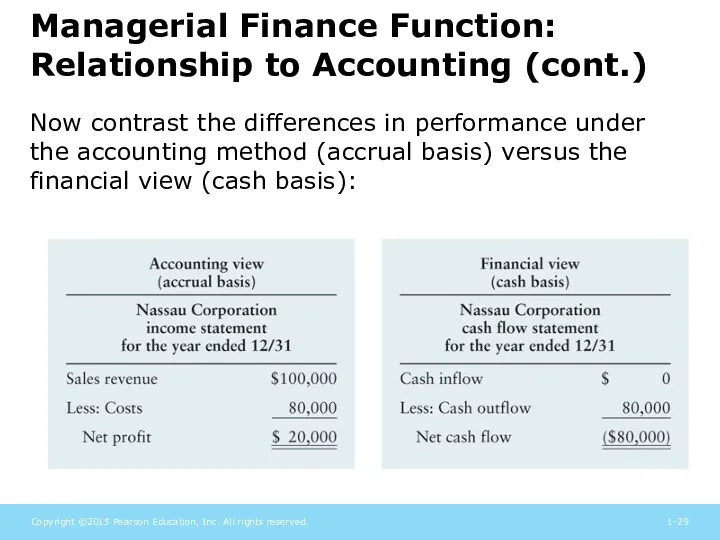

Managerial Finance Function: Relationship to Accounting (cont.)

Now contrast the differences in

Managerial Finance Function: Relationship to Accounting (cont.)

Now contrast the differences in

Managerial Finance Function: Relationship to Accounting (cont.)

Finance and accounting also differ

Managerial Finance Function: Relationship to Accounting (cont.)

Finance and accounting also differ

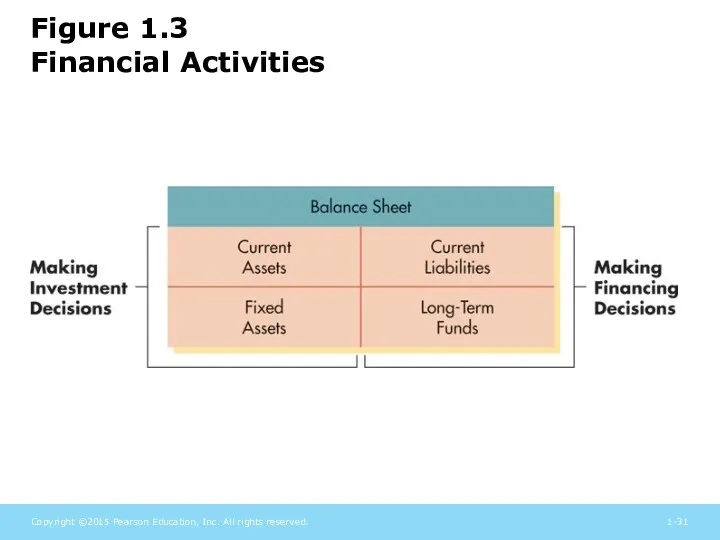

Figure 1.3

Financial Activities

Figure 1.3

Financial Activities

Governance and Agency:

Corporate Governance

Corporate governance refers to the rules, processes,

Governance and Agency:

Corporate Governance

Corporate governance refers to the rules, processes,

Governance and Agency:

Individual versus Institutional Investors

Individual investors are investors who

Governance and Agency:

Individual versus Institutional Investors

Individual investors are investors who

Governance and Agency:

Government Regulation

Government regulation generally shapes the corporate governance

Governance and Agency:

Government Regulation

Government regulation generally shapes the corporate governance

Governance and Agency:

Government Regulation

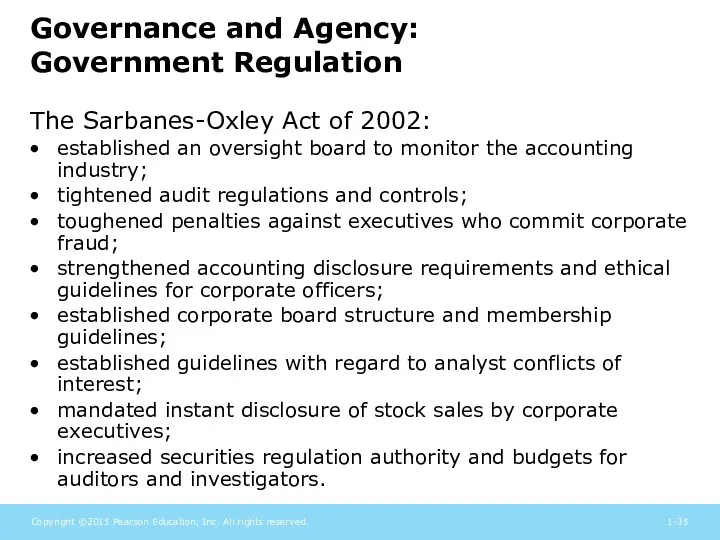

The Sarbanes-Oxley Act of 2002:

established an

Governance and Agency:

Government Regulation

The Sarbanes-Oxley Act of 2002:

established an

Governance and Agency:

The Agency Issue

A principal-agent relationship is an arrangement

Governance and Agency:

The Agency Issue

A principal-agent relationship is an arrangement

The Agency Issue:

Management Compensation Plans

In addition to the roles played

The Agency Issue:

Management Compensation Plans

In addition to the roles played

The Agency Issue:

Management Compensation Plans

Incentive plans are management compensation plans

The Agency Issue:

Management Compensation Plans

Incentive plans are management compensation plans

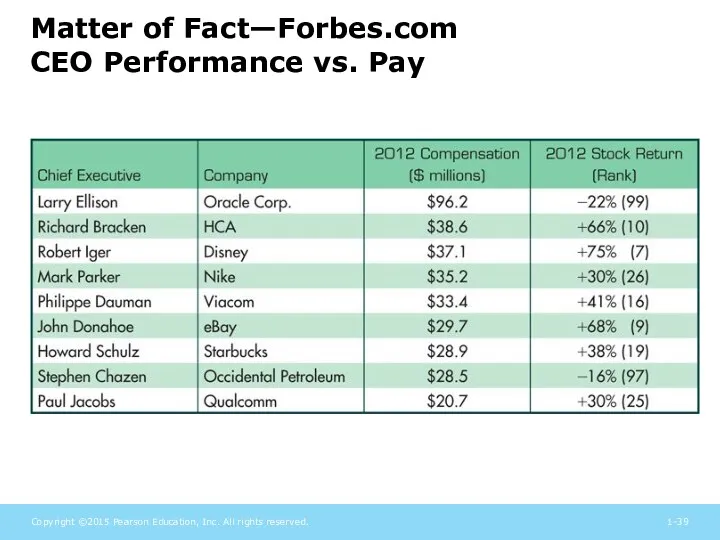

Matter of Fact—Forbes.com

CEO Performance vs. Pay

Matter of Fact—Forbes.com

CEO Performance vs. Pay

1С-Отчетность за 9 месяцев 2019 года, на что обратить внимание. Единый семинар 1С

1С-Отчетность за 9 месяцев 2019 года, на что обратить внимание. Единый семинар 1С Инструменты финансирования публичных компаний. Классификация источников средств: юридический аспект

Инструменты финансирования публичных компаний. Классификация источников средств: юридический аспект Монетарная политика (1). Тема 5

Монетарная политика (1). Тема 5 Финансовая система США

Финансовая система США Валютный рынок

Валютный рынок Денежные обязательства и расчеты

Денежные обязательства и расчеты Организация деятельности Центрального банка

Организация деятельности Центрального банка Привлечение инвестиций в точку общественного питания

Привлечение инвестиций в точку общественного питания Финансы. Введение

Финансы. Введение Порядок заполнения Уведомлений об уточнении вида и принадлежности платежа (код формы по КФД 0531809)

Порядок заполнения Уведомлений об уточнении вида и принадлежности платежа (код формы по КФД 0531809) Условия назначения страховой пенсии по старости

Условия назначения страховой пенсии по старости Оплата труда (заработная плата). Гарантии и компенсации

Оплата труда (заработная плата). Гарантии и компенсации Учет расходов. Тема 10. Часть 1

Учет расходов. Тема 10. Часть 1 Статистика денежного обращения

Статистика денежного обращения Семейный бюджет. 3 класс

Семейный бюджет. 3 класс Деньги и мораль

Деньги и мораль Водный налог

Водный налог Теоретические основы государственных и муниципальных финансов

Теоретические основы государственных и муниципальных финансов Финансовая грамотность: личное финансовое планирование

Финансовая грамотность: личное финансовое планирование Дивидендная политика корпораций

Дивидендная политика корпораций О банке, его финансовых показателях, рейтинге, продуктах и услугах

О банке, его финансовых показателях, рейтинге, продуктах и услугах Рабочий отчет департамента аналитики компании IPO

Рабочий отчет департамента аналитики компании IPO Анализ финансового состояния предприятия

Анализ финансового состояния предприятия Классификация доходов бюджета

Классификация доходов бюджета Налоги. Обязательные платежи в государственную казну

Налоги. Обязательные платежи в государственную казну Виды государственных пенсий. Роль государства в их реализации

Виды государственных пенсий. Роль государства в их реализации Сущность аудита и его содержание

Сущность аудита и его содержание Бухгалтерский учет и анализ финансовых результатов на примере ООО Гермес

Бухгалтерский учет и анализ финансовых результатов на примере ООО Гермес