- Financial accounting

Содержание

- 2. FINANCIAL ACCOUNTING Assessment -evaluation during semester (EDS) 50% -test 80% (week 5) -test quizzes 20% -exam

- 3. References Horngren, C.T., Sundem, G.L., Elliot, J.A., Philbrick, D, Introduction to Financial Accounting, 11th edition, Pearson,

- 4. Course description: Financial statements Recording Transactions Accrual Accounting and Income Balance Sheet: A +B +C A.

- 5. The Financial Statements Course 1 Copyright ©2010 Pearson Education Inc. Publishing as Prentice Hall.

- 6. Learning Objective 1 Use accounting vocabulary

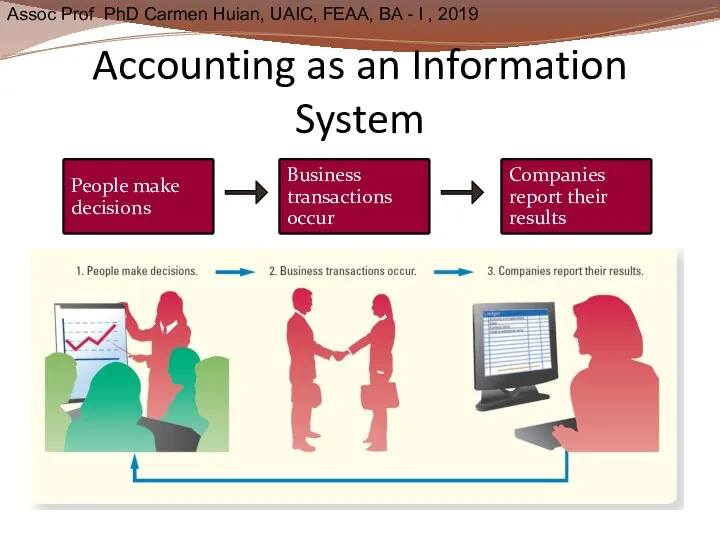

- 7. Accounting as an Information System

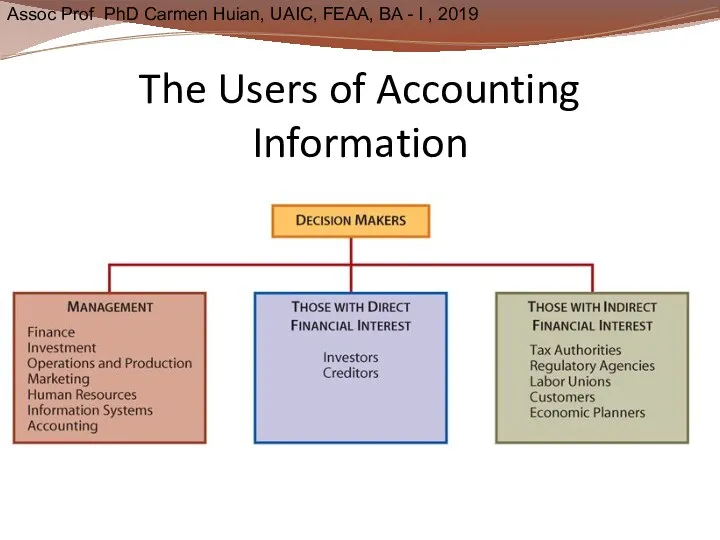

- 8. The Users of Accounting Information

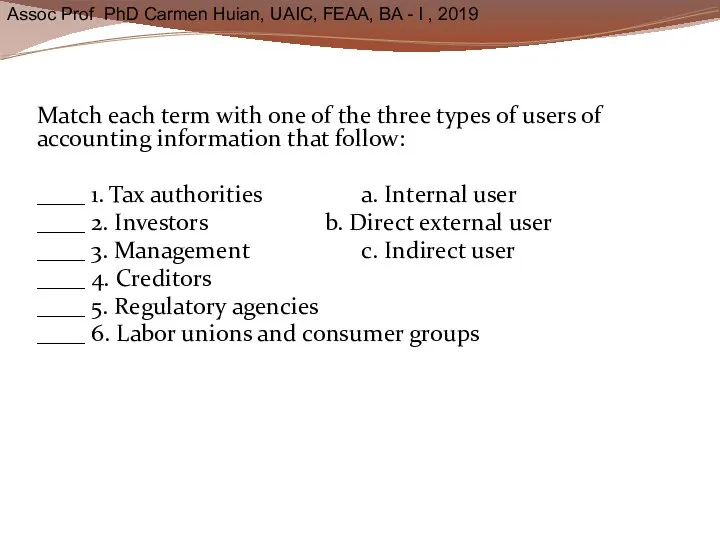

- 9. Match each term with one of the three types of users of accounting information that follow:

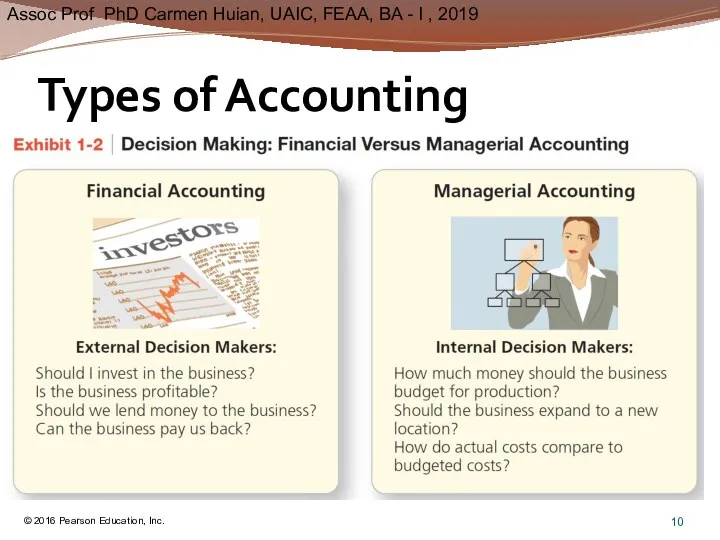

- 10. Types of Accounting © 2016 Pearson Education, Inc.

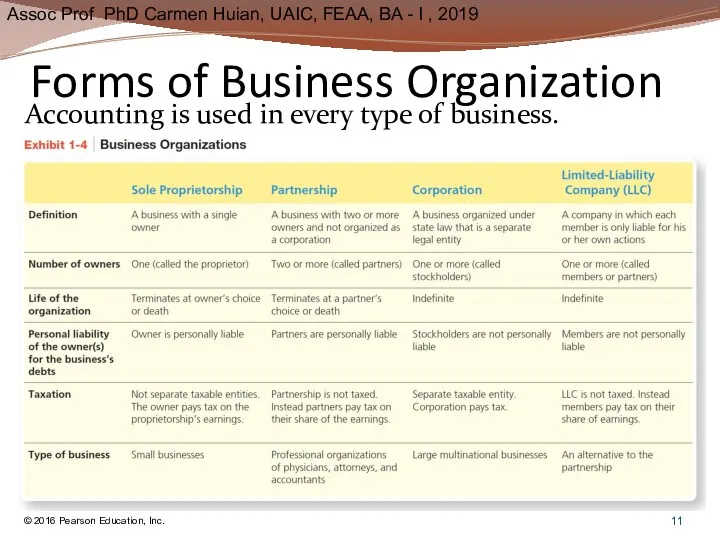

- 11. Forms of Business Organization © 2016 Pearson Education, Inc. Accounting is used in every type of

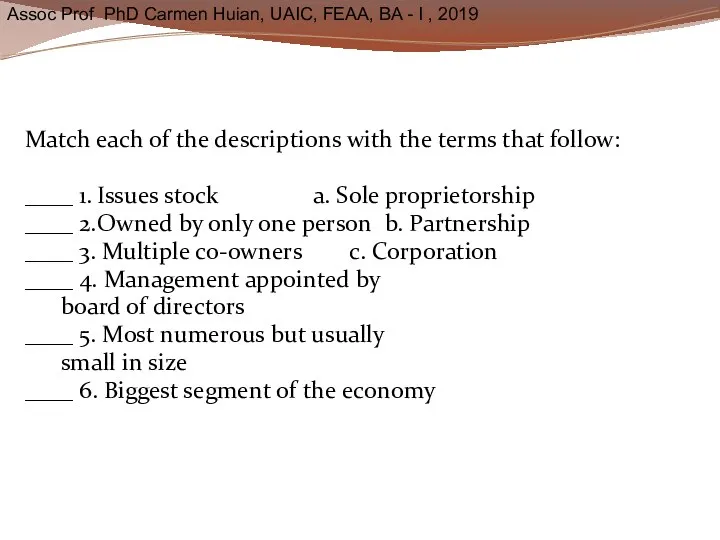

- 12. Match each of the descriptions with the terms that follow: ____ 1. Issues stock a. Sole

- 13. Learning Objective Two Learn the underlying concepts, assumptions and principles of accounting

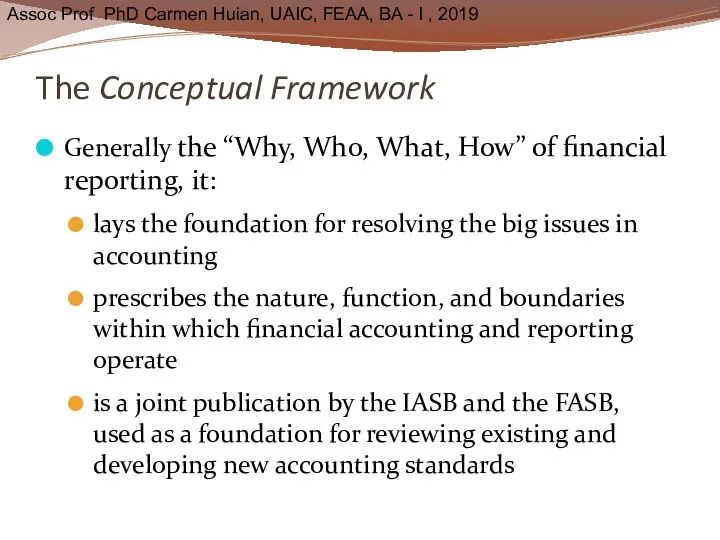

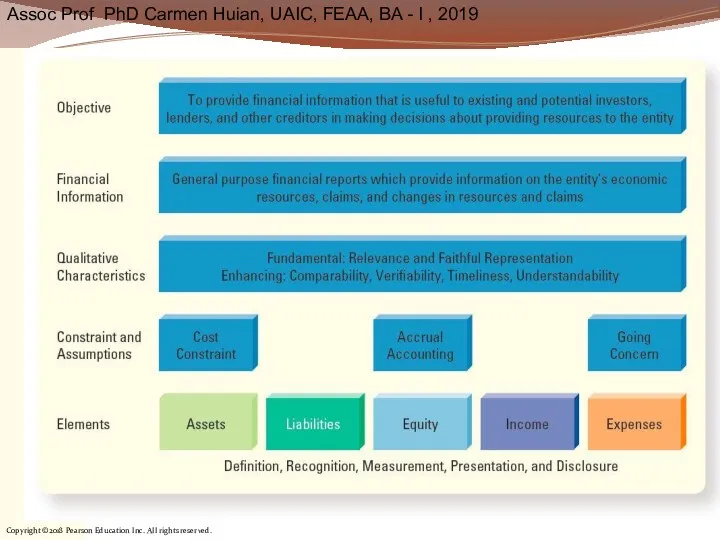

- 14. The Conceptual Framework Generally the “Why, Who, What, How” of financial reporting, it: lays the foundation

- 15. Copyright ©2018 Pearson Education Inc. All rights reserved.

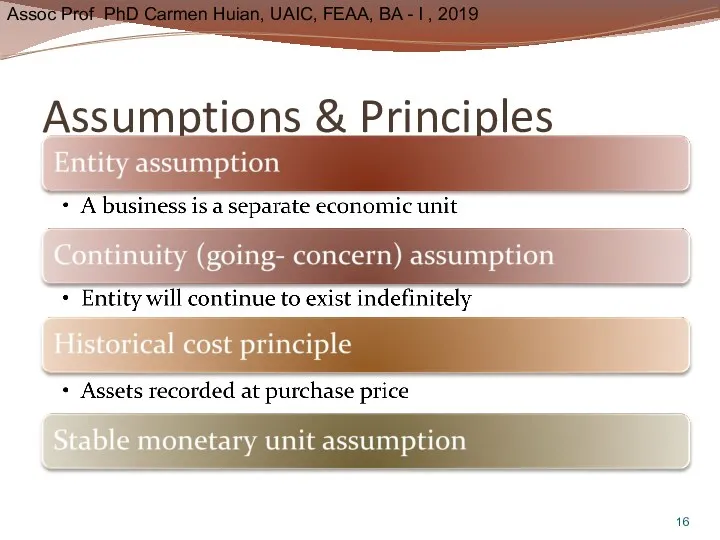

- 16. Assumptions & Principles

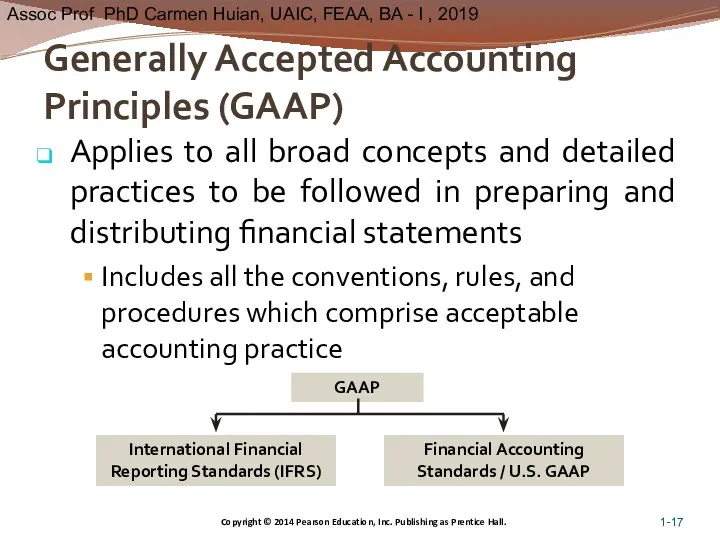

- 17. Generally Accepted Accounting Principles (GAAP) Applies to all broad concepts and detailed practices to be followed

- 18. GAAP U.S. GAAP: published by FASB Applies to financial reporting in the U.S. Used by companies

- 19. Learning Objective Three Apply the accounting equation to business organizations

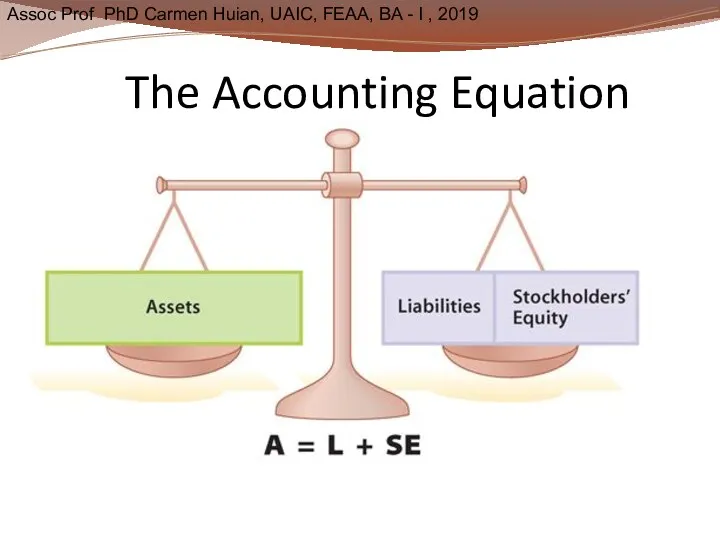

- 20. The Accounting Equation

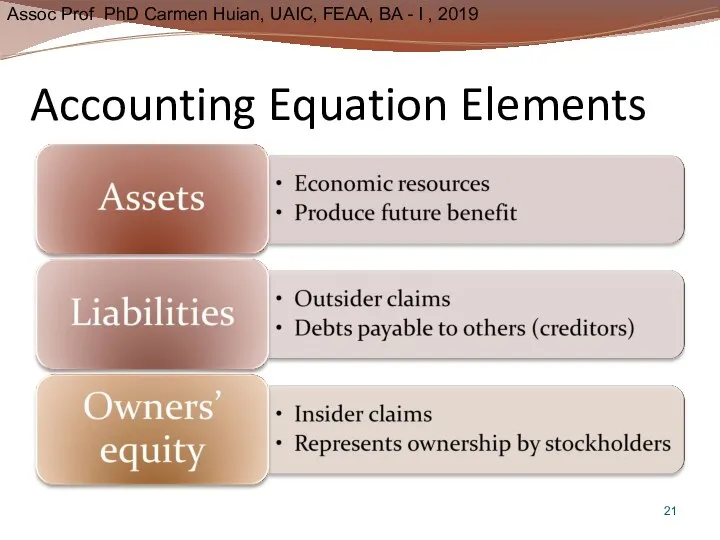

- 21. Accounting Equation Elements

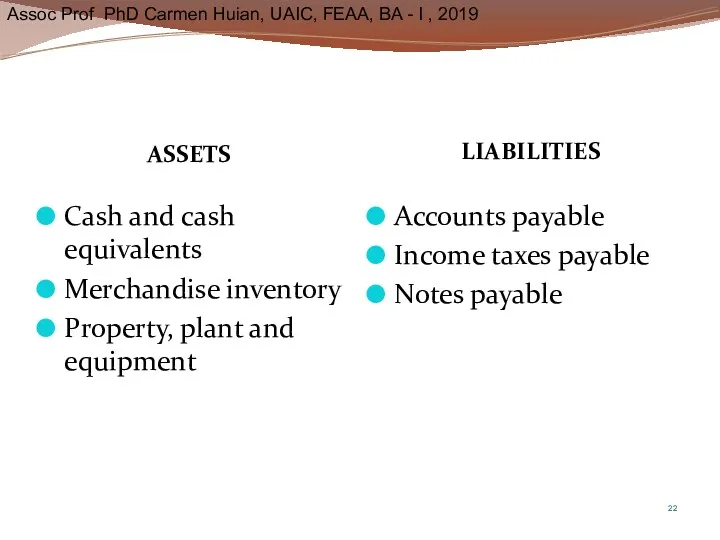

- 22. ASSETS LIABILITIES Cash and cash equivalents Merchandise inventory Property, plant and equipment Accounts payable Income taxes

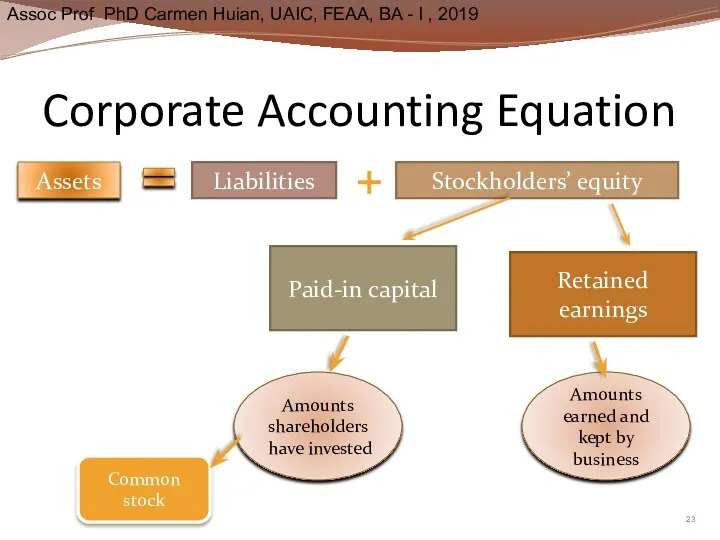

- 23. Corporate Accounting Equation Assets Liabilities Stockholders’ equity Paid-in capital Retained earnings Amounts shareholders have invested Common

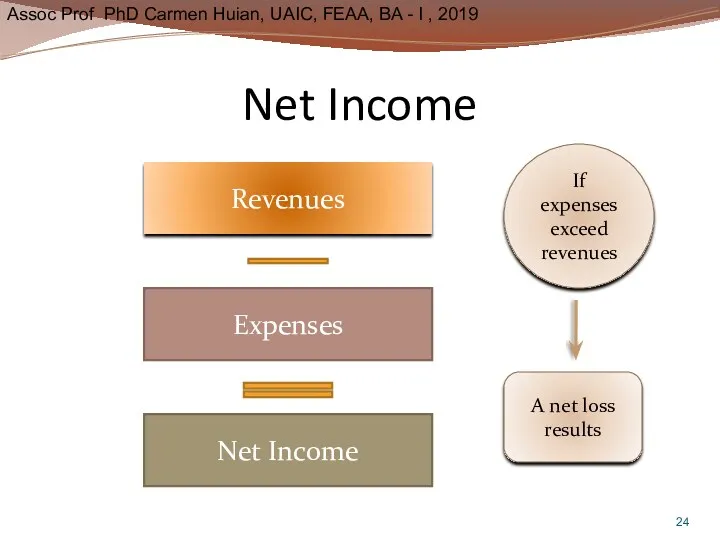

- 24. Net Income Revenues Expenses Net Income If expenses exceed revenues A net loss results

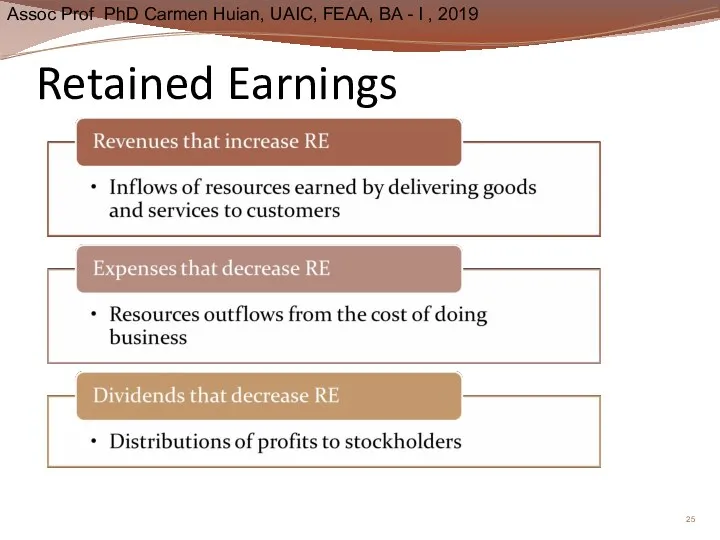

- 25. Retained Earnings

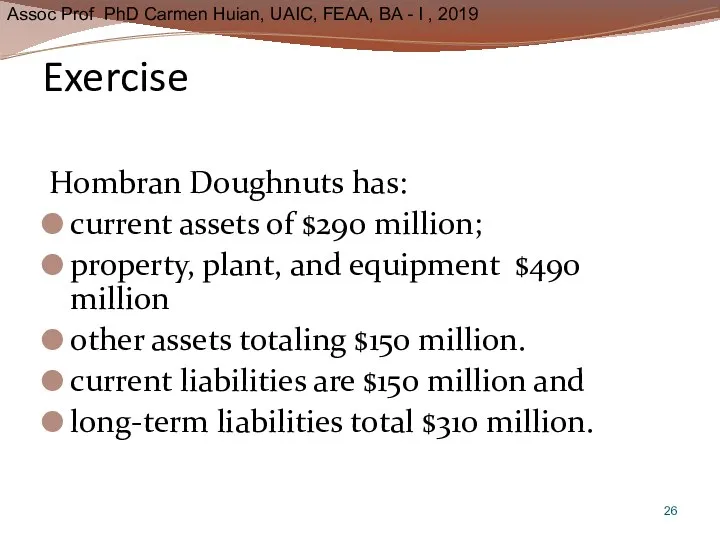

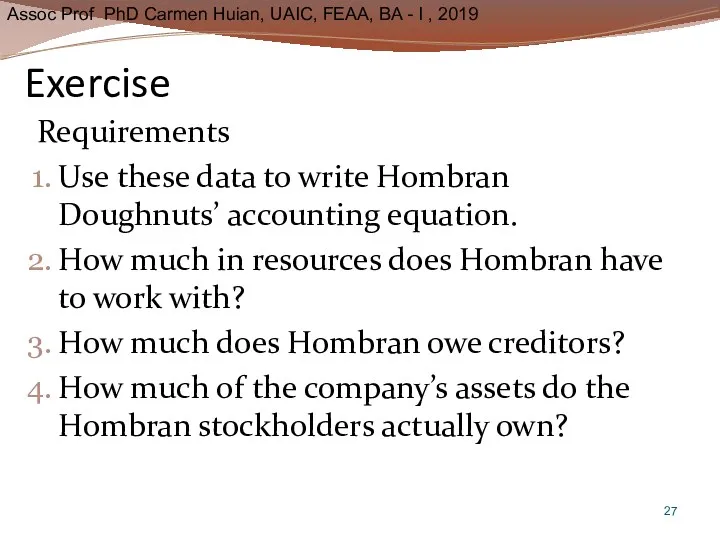

- 26. Exercise Hombran Doughnuts has: current assets of $290 million; property, plant, and equipment $490 million other

- 27. Exercise Requirements Use these data to write Hombran Doughnuts’ accounting equation. How much in resources does

- 28. Learning Objective Four Evaluate business operations

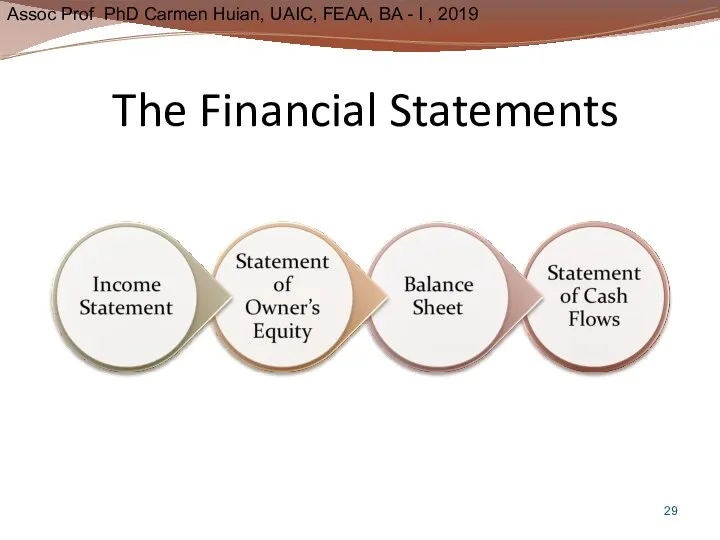

- 29. The Financial Statements

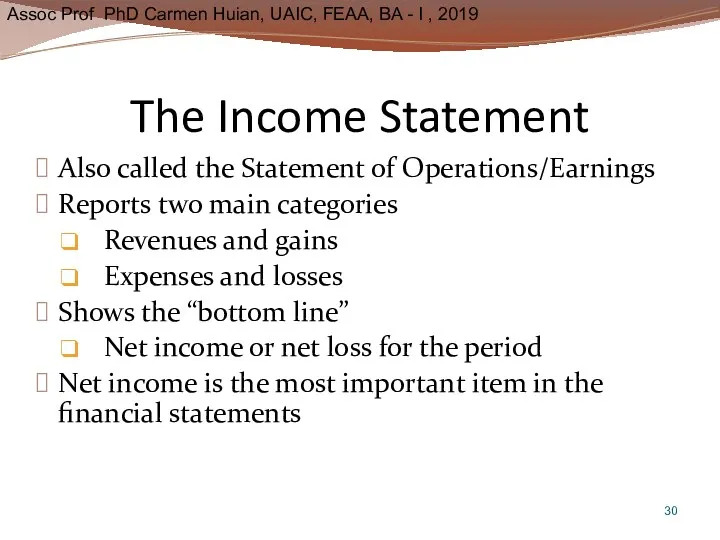

- 30. The Income Statement Also called the Statement of Operations/Earnings Reports two main categories Revenues and gains

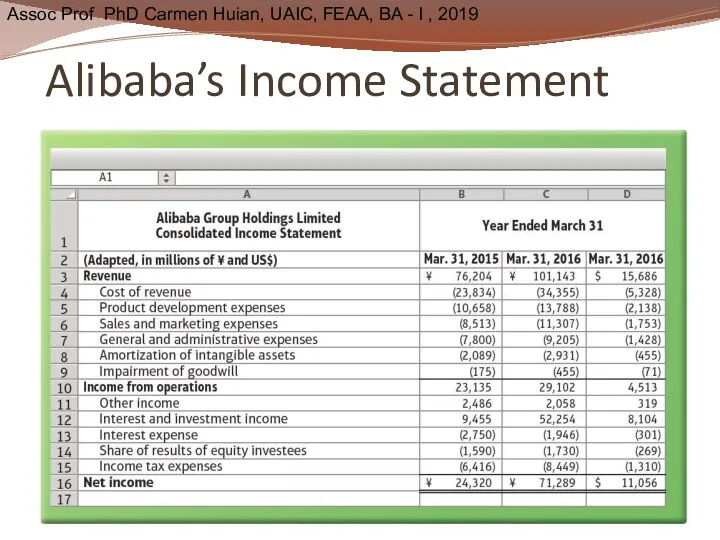

- 31. Alibaba’s Income Statement

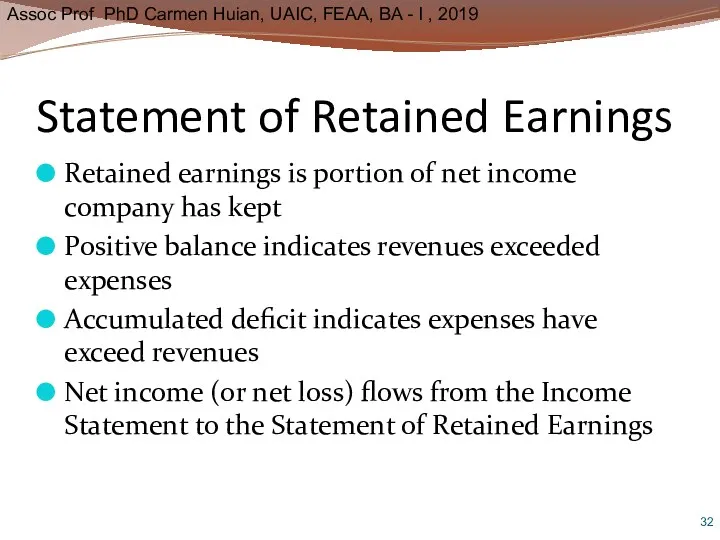

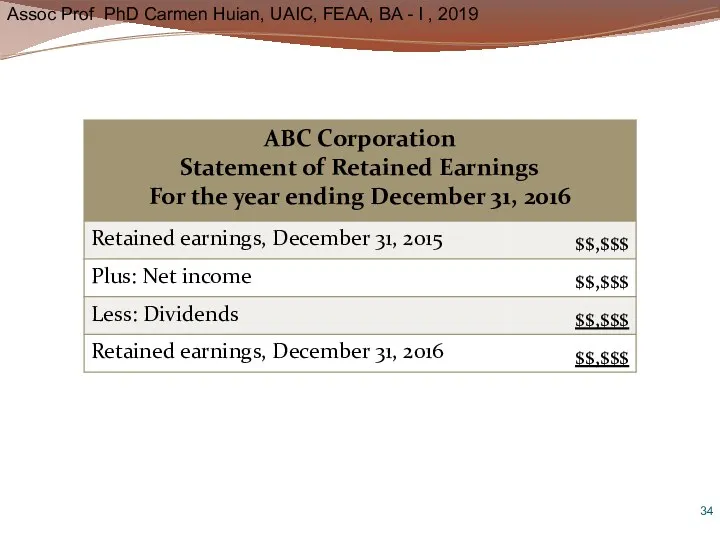

- 32. Statement of Retained Earnings Retained earnings is portion of net income company has kept Positive balance

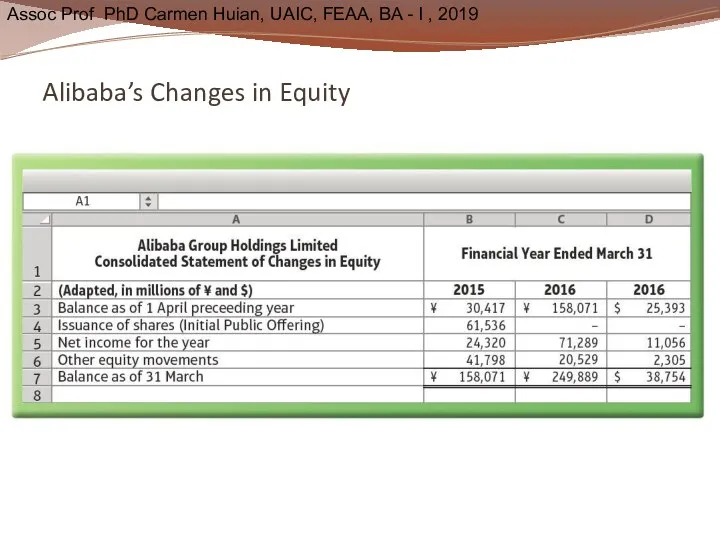

- 33. Alibaba’s Changes in Equity

- 35. The Balance Sheet Also called the Statement of Financial Position Reports Assets Liabilities Stockholders’ equity

- 36. Assets on the Balance Sheet Current Long-term Expected to be converted to cash, sold or consumed

- 37. Liabilities on the Balance Sheet Current Long-term Debts payable in the next year or within the

- 38. Stockholders’ Equity on the Balance Sheet Represents stockholders ownership of the business assets Consists of: Common

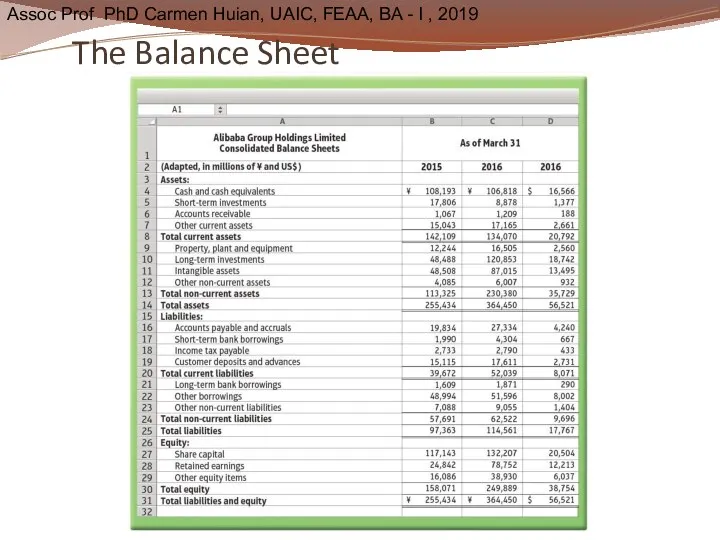

- 39. The Balance Sheet

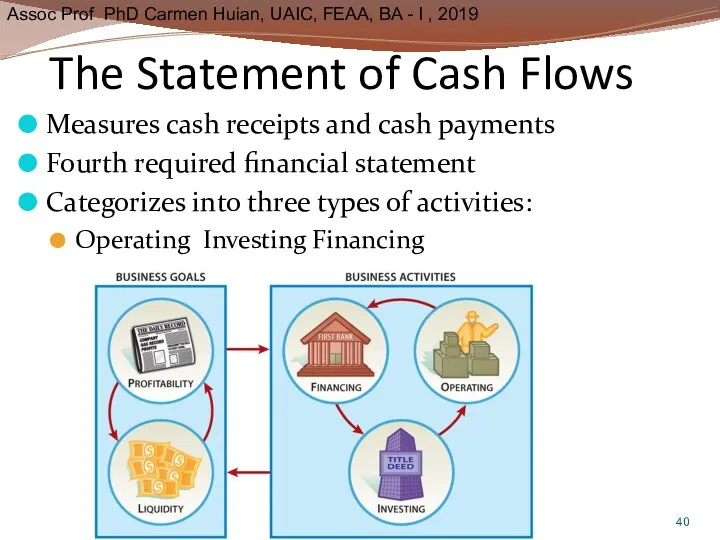

- 40. The Statement of Cash Flows Measures cash receipts and cash payments Fourth required financial statement Categorizes

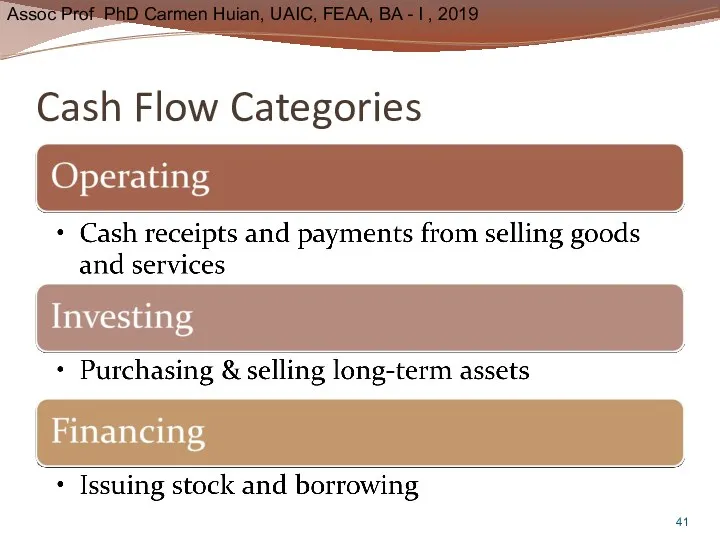

- 41. Cash Flow Categories

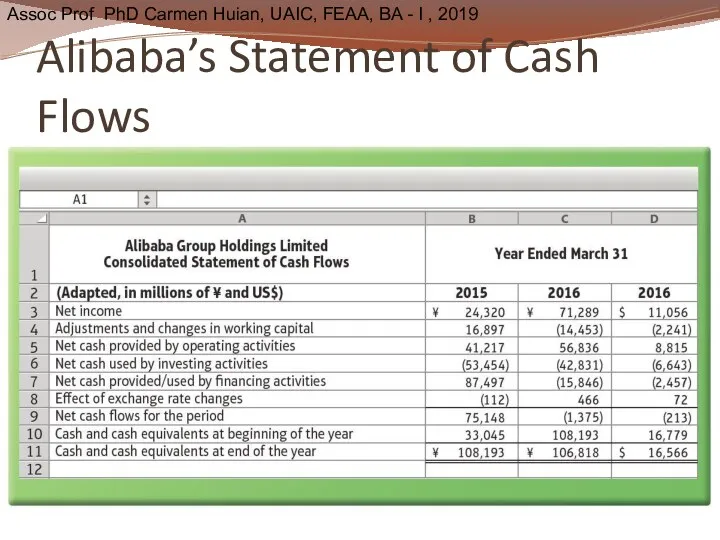

- 42. Alibaba’s Statement of Cash Flows

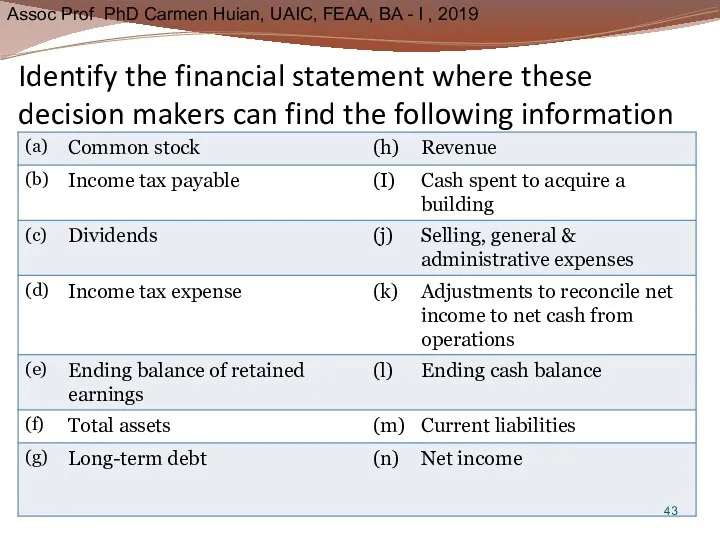

- 43. Identify the financial statement where these decision makers can find the following information

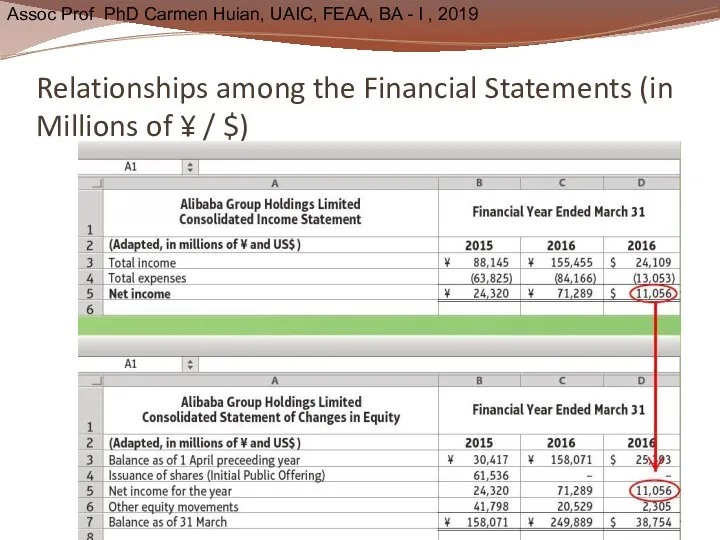

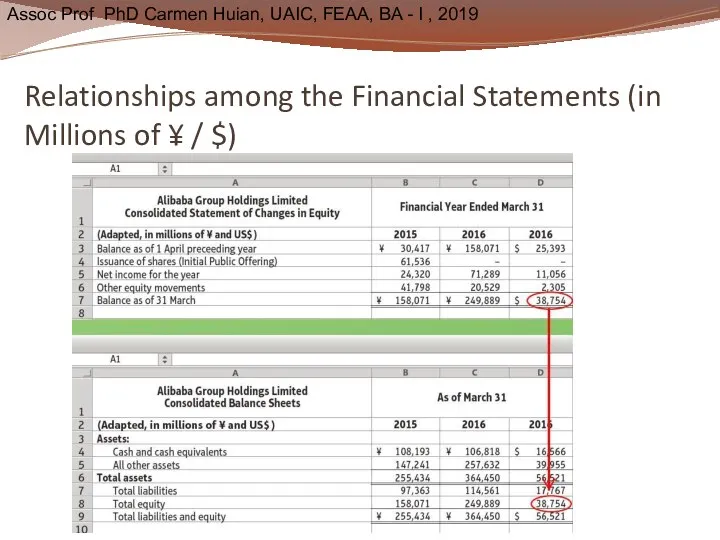

- 44. Relationships among the Financial Statements (in Millions of ¥ / $)

- 45. Relationships among the Financial Statements (in Millions of ¥ / $)

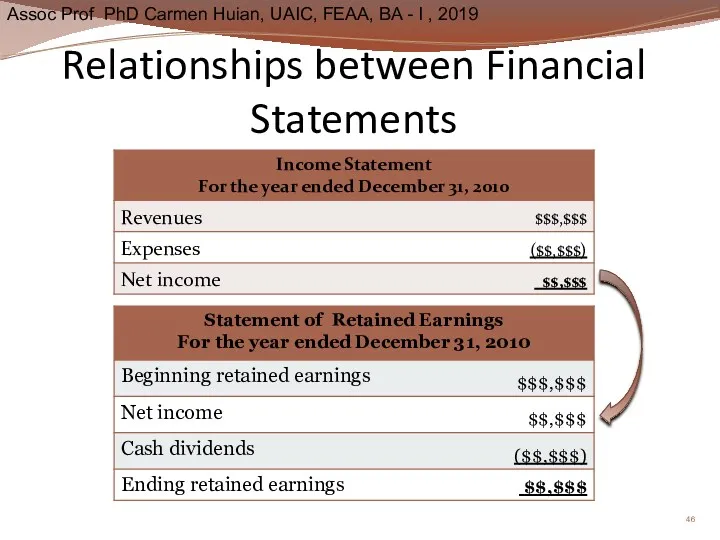

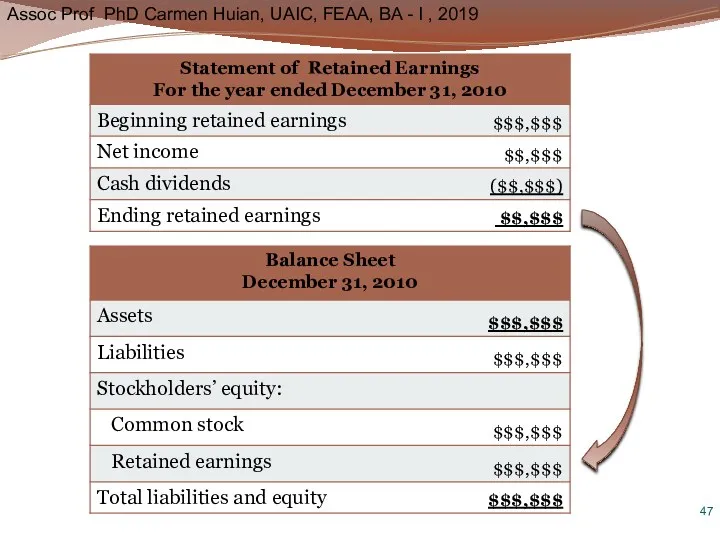

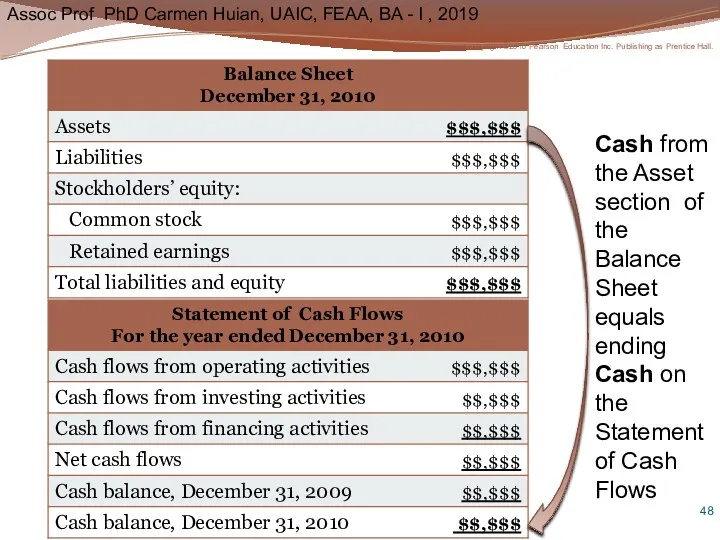

- 46. Relationships between Financial Statements

- 48. Cash from the Asset section of the Balance Sheet equals ending Cash on the Statement of

- 50. Скачать презентацию

FINANCIAL ACCOUNTING

Assessment

-evaluation during semester (EDS) 50%

-test 80% (week 5)

-test quizzes 20%

-exam

FINANCIAL ACCOUNTING

Assessment

-evaluation during semester (EDS) 50%

-test 80% (week 5)

-test quizzes 20%

-exam

References

Horngren, C.T., Sundem, G.L., Elliot, J.A., Philbrick, D, Introduction to Financial

References

Horngren, C.T., Sundem, G.L., Elliot, J.A., Philbrick, D, Introduction to Financial

Course description:

Financial statements

Recording Transactions

Accrual Accounting and Income

Balance Sheet:

Course description: Financial statements Recording Transactions Accrual Accounting and Income Balance Sheet:

The Financial Statements

Course 1

Copyright ©2010 Pearson Education Inc. Publishing as Prentice

The Financial Statements

Course 1

Copyright ©2010 Pearson Education Inc. Publishing as Prentice

Learning Objective 1

Use accounting vocabulary

Learning Objective 1

Use accounting vocabulary

Accounting as an Information System

Accounting as an Information System

The Users of Accounting Information

The Users of Accounting Information

Match each term with one of the three types of users

Match each term with one of the three types of users

Types of Accounting

© 2016 Pearson Education, Inc.

Types of Accounting

© 2016 Pearson Education, Inc.

Forms of Business Organization

© 2016 Pearson Education, Inc.

Accounting is used in

Forms of Business Organization

© 2016 Pearson Education, Inc.

Accounting is used in

Match each of the descriptions with the terms that follow:

____ 1. Issues

Match each of the descriptions with the terms that follow:

____ 1. Issues

Learning Objective Two

Learn the underlying concepts, assumptions and principles of accounting

Learning Objective Two

Learn the underlying concepts, assumptions and principles of accounting

The Conceptual Framework

Generally the “Why, Who, What, How” of financial reporting,

The Conceptual Framework

Generally the “Why, Who, What, How” of financial reporting,

Copyright ©2018 Pearson Education Inc. All rights reserved.

Copyright ©2018 Pearson Education Inc. All rights reserved.

Assumptions & Principles

Assumptions & Principles

Generally Accepted Accounting Principles (GAAP)

Applies to all broad concepts and detailed

Generally Accepted Accounting Principles (GAAP)

Applies to all broad concepts and detailed

GAAP

U.S. GAAP: published by FASB

Applies to financial reporting in the U.S.

GAAP

U.S. GAAP: published by FASB

Applies to financial reporting in the U.S.

Learning Objective Three

Apply the accounting equation to business organizations

Learning Objective Three

Apply the accounting equation to business organizations

The Accounting Equation

The Accounting Equation

Accounting Equation Elements

Accounting Equation Elements

ASSETS

LIABILITIES

Cash and cash equivalents

Merchandise inventory

Property, plant and equipment

Accounts payable

Income taxes payable

Notes

ASSETS

LIABILITIES

Cash and cash equivalents

Merchandise inventory

Property, plant and equipment

Accounts payable

Income taxes payable

Notes

Corporate Accounting Equation

Assets

Liabilities

Stockholders’ equity

Paid-in capital

Retained earnings

Amounts shareholders have invested

Common stock

Amounts earned

Corporate Accounting Equation

Assets

Liabilities

Stockholders’ equity

Paid-in capital

Retained earnings

Amounts shareholders have invested

Common stock

Amounts earned

Net Income

Revenues

Expenses

Net Income

If expenses exceed revenues

A net loss results

Net Income

Revenues

Expenses

Net Income

If expenses exceed revenues

A net loss results

Retained Earnings

Retained Earnings

Exercise

Hombran Doughnuts has:

current assets of $290 million;

property, plant, and equipment

Exercise

Hombran Doughnuts has:

current assets of $290 million;

property, plant, and equipment

Exercise

Requirements

Use these data to write Hombran Doughnuts’ accounting equation.

How

Exercise

Requirements

Use these data to write Hombran Doughnuts’ accounting equation.

How

Learning Objective Four

Evaluate business operations

Learning Objective Four

Evaluate business operations

The Financial Statements

The Financial Statements

The Income Statement

Also called the Statement of Operations/Earnings

Reports two main categories

Revenues

The Income Statement

Also called the Statement of Operations/Earnings

Reports two main categories

Revenues

Alibaba’s Income Statement

Alibaba’s Income Statement

Statement of Retained Earnings

Retained earnings is portion of net income company

Statement of Retained Earnings

Retained earnings is portion of net income company

Alibaba’s Changes in Equity

Alibaba’s Changes in Equity

The Balance Sheet

Also called the Statement of Financial Position

Reports

Assets

Liabilities

Stockholders’ equity

The Balance Sheet

Also called the Statement of Financial Position

Reports

Assets

Liabilities

Stockholders’ equity

Assets on the Balance Sheet

Current

Long-term

Expected to be converted to cash, sold

Assets on the Balance Sheet

Current

Long-term

Expected to be converted to cash, sold

Liabilities on the Balance Sheet

Current

Long-term

Debts payable in the next year or

Liabilities on the Balance Sheet

Current

Long-term

Debts payable in the next year or

Stockholders’ Equity on the Balance Sheet

Represents stockholders ownership of the business

Stockholders’ Equity on the Balance Sheet

Represents stockholders ownership of the business

The Balance Sheet

The Balance Sheet

The Statement of Cash Flows

Measures cash receipts and cash payments

Fourth required

The Statement of Cash Flows

Measures cash receipts and cash payments

Fourth required

Cash Flow Categories

Cash Flow Categories

Alibaba’s Statement of Cash Flows

Alibaba’s Statement of Cash Flows

Identify the financial statement where these decision makers can find the

Identify the financial statement where these decision makers can find the

Relationships among the Financial Statements (in Millions of ¥ / $)

Relationships among the Financial Statements (in Millions of ¥ / $)

Relationships among the Financial Statements (in Millions of ¥ / $)

Relationships among the Financial Statements (in Millions of ¥ / $)

Relationships between Financial Statements

Relationships between Financial Statements

Cash from the Asset section of the Balance

Sheet equals ending

Cash from the Asset section of the Balance

Sheet equals ending

Рыночный подход к оценке бизнеса. Метод рынка капитала. Метод сделок. Метод отраслевых коэффициентов

Рыночный подход к оценке бизнеса. Метод рынка капитала. Метод сделок. Метод отраслевых коэффициентов Инвестициялық стратегия

Инвестициялық стратегия Фигуры технического анализа

Фигуры технического анализа Понятие, цели и организация оценки стоимости бизнеса. (Лекция 1)

Понятие, цели и организация оценки стоимости бизнеса. (Лекция 1) Asset Securitization in Russia

Asset Securitization in Russia Сопоставимость отчетных данных и принцип последовательности: МСФО (IAS) 8 Учетная политика, изменения в бухгалтерских

Сопоставимость отчетных данных и принцип последовательности: МСФО (IAS) 8 Учетная политика, изменения в бухгалтерских Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности

Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности Индивидуальный подоходный налог в Республике Казахстан и его учет

Индивидуальный подоходный налог в Республике Казахстан и его учет Налоги и налоговая система РФ

Налоги и налоговая система РФ Місцеві податки і збори

Місцеві податки і збори Доходность и убыточность операций с ценными бумагами

Доходность и убыточность операций с ценными бумагами Налоги. 7 класс

Налоги. 7 класс Инвестициялық жобалардың қаржылық механизмі және жобалық қаржыландыру

Инвестициялық жобалардың қаржылық механизмі және жобалық қаржыландыру Налог на прибыль организаций

Налог на прибыль организаций Relationship between liquidity ratios and profitability in Russian banks using regression analysis

Relationship between liquidity ratios and profitability in Russian banks using regression analysis Шығын айналымын болжау

Шығын айналымын болжау Бухгалтерские счета как элемент метода бухгалтерского учета

Бухгалтерские счета как элемент метода бухгалтерского учета Международные стандарты финансовой отчетности МСФО (IAS) 12 Налоги на прибыль

Международные стандарты финансовой отчетности МСФО (IAS) 12 Налоги на прибыль Тенденции развития современной финансовой науки

Тенденции развития современной финансовой науки Проведение операций по потребительскому кредитованию физических лиц

Проведение операций по потребительскому кредитованию физических лиц Криптовалюта. Доп. инструменты технического анализа

Криптовалюта. Доп. инструменты технического анализа Банки: чем они могут быть вам полезны в жизни

Банки: чем они могут быть вам полезны в жизни Қазақстанның қазіргі уақытта сыртқы қарызы қанша

Қазақстанның қазіргі уақытта сыртқы қарызы қанша Проект бюджета городского округа Судак на 2015 год

Проект бюджета городского округа Судак на 2015 год Финансовые инновации, финансовый инжиниринг. (Лекция 1)

Финансовые инновации, финансовый инжиниринг. (Лекция 1) Критерии оценки инвестиционных проектов

Критерии оценки инвестиционных проектов Планирование финансово-хозяйственной деятельности, как ключевой инструмент финансового менеджмента профсоюзной организации

Планирование финансово-хозяйственной деятельности, как ключевой инструмент финансового менеджмента профсоюзной организации Страхование жизни

Страхование жизни